PDF, 102 KB, Datei Ist Nicht

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Jsc Avtovaz Avtovaz Group* Operating Highlights for 2003

ANNUAL REPORT | 2003 | JSC AVTOVAZ AVTOVAZ GROUP* OPERATING HIGHLIGHTS FOR 2003 Vehicle unit sales, JSC AVTOVAZ 2003 2002 Change 000’s units 000’s units % Domestic market 626 577 8.49 Export market 92 98 (6.12) Total 718 675 6.3 Automotive assembly kits sales 98 101 (2.97) RR mln RR mln % Net sales 130,772 119,432 9.49 Operating income 5,941 5,591 6.26 Consolidated Statement 2003 2002 Change of Income** RR mln RR mln % For the year ended 31 December Net sales 130,772 119,432 9.49 Cost of sales (110,003) (99,331) 10.74 Gross profit 20,769 20,101 3.32 Interest expense (3,416) (3,077) (11.02) Other expense, net (14,402) (15,896) (9.4) Net income for the year 2,951 1,128 161.61 Consolidated Balance Sheet** 2003 2002 Change At 31 December RR mln RR mln % Cash and cash equivalents 6,767 2,751 145.98 Other current assets 37,069 33,393 11.01 Non-current assets 108,228 102,836 5.24 Total liabilities 72,562 62,166 16.72 Minority interest 1,290 1,587 (18.71) Total shareholders’ equity 78,212 75,227 3.97 Share price and dividend 2003 2002 Change development, JSC AVTOVAZ*** Share price RR RR % For the year ended 31 December Ordinary share Closing 774.7 679.72 +13.97 Annual high 906.42 1201.31 -24.55 Annual low 582.06 558.64 +4.19 Preference share Closing 471.88 371.17 +27.13 Annual high 525.68 667.54 -21.25 Annual low 339.77 319.10 +6.48 Dividends Per ordinary share 6.00 5.00 +20.0 Per preference share 95.00 17.00 +458.82 * The AVTOVAZ Group mentioned hereinafter is the parent company (JSC AVTOVAZ or the “Company”) and all of its subsidiaries and associated companies. -

STORM Hatchback

Ignition Leads 2013 Introduction Standard Motor Products Europe (SMPE) is one of Europe’s leading manufacturers of high quality, proprietary and private brand ignition leads and sets for the automotive aftermarket. Based in England, SMPE were one of the first specialist aftermarket ignition lead manufacturers in Europe; as such SMPE currently supply many of the major names in the European aftermarket. The extensive KERR NELSON HighVolt product offering is designed, manufactured and supplied utilising state of the art systems and processes. It is this commitment to employing the highest quality systems and processes, which has resulted in SMPE becoming one of the first specialist aftermarket ignition lead suppliers to be awarded ISO9001 ccreditation. A key requirement of ISO9001 is continuous improvement. This philosophy has been embraced in all aspects of SMPE’s business. Evidence of SMPE’s commitment to continuous improvement can be seen in the just-in-time manufacturing process and flexible production setup allowing efficient assembly for a large variety of part numbers to satisfy market requirements. SMPE are focused on new product development driven from a European vehicle parc database and industry leading applications cataloguing. The current KERR NELSON HighVolt programme of ignition leads provides the latest development of a range that has continually evolved to keep pace with the changing demands of both vehicle technology and customer requirements. By embracing the philosophy of continued product improvement SMPE is able to offer: Respected Brand Comprehensive Product Offering Premium Quality Product Outstanding Availability Excellent Technical Support Guaranteed Customer Satisfaction The Role of Ignition Leads in a Conventional Ignition System The primary function of the ignition system is to initiate the firing of the air/fuel mixture in a spark ignition engine. -

Guide to Assembly Plants in Europe

AN_071112_16_17.qxd 3/13/08 4:11 PM Page 16 PAGE 16 · www.autonew seurope.com November 12, 2007 Guide to assembly plants in Europe BMW GROUP A San Benedetto Val di Sangro, Italy (Sevel Sud: Fiat 50%, (2008). Note: GM has temporary plant on site until 4 Flins, France – Renault Clio III, Clio II (See also 3 , 25 ) PSA 50%) – Citroen Jumper/Relay; Fiat Ducato; permanent plant opens in 2008. 5 Maubeuge, France – Passenger cars: Kangoo, new 1 Dingolfing, Germany – BMW 5-series sedan, station Peugeot Boxer 11 Asaka, Uzbekistan (UzDaewoo: joint venture of GM, Kangoo; LCV: new Kangoo Express, new Kangoo Express wagon, 6-series coupe, convertible, 7-series sedan, B Lieu Saint-Amand, France (Sevel Nord: Fiat 50%, PSA GM Daewoo and Uzautosanoat) – Daewoo Tico, Matiz, Compact; Nissan Kubistar M5 sedan, station wagon, M6 coupe, convertible 50%) – Citroen Atlante/C8, Dispatch/Jumpy; Fiat Scudo, Damas, Nexia, Lacetti; (from kits** starting in 2008) 6 Sandouville, France – Renault Laguna III Sport Tourer and 2 Leipzig, Germany – BMW 1-series 3 door, coupe, Scudo Panorama, Ulysse; Lancia Phedra; Peugeot 807, Chevrolet Epica, Tacuma, Captiva hatchback, Espace IV, Vel Satis convertible, 3-series sedan Expert, TePee A Togliatti, Russia (joint venture of GM and AvtoVAZ) – 7 Palencia, Spain – Renault Megane II hatchback, sport 3 Munich, Germany – BMW 3-series sedan, station wagon Chevrolet Niva, Viva; Opel car (2008) hatch, sport station wagon 4 Regensburg, Germany – BMW 1-series 5 door, 3-series FORD B Warsaw, Poland (FSO: UkrAvto 60%, GM Daewoo 40%) – 8 Valladolid, -

Avtovaz Stakes on Lada Priora

AVTOVAZ STAKES ON LADA PRIORA BY KIRILL LEBEDEV, IFS SENIOR ANALYST, D. PANKRATOVA, IFS ANALYST, FEBRUARY 19, 2010 Russia’s largest carmaker, AvtoVAZ, emerged in the domestic market last year as a competitive carmaker. Even upsetting sales (nearly 350 thousand vehicles were sold in 2009 versus 600 thousand in the previous years) cannot be reckoned as a reason to consider the plant uncompetitive (see Figure 1). Figure 1. AvtoVAZ sales in Russia 700 600 500 400 300 thousand units thousand 200 100 0 2006 2007 2008 2009 Source: AvtoVAZ Many automakers are seeing sinking sales as the global crises pushed down the demand for cars. Foreign car make sales (including popular models manufactured in Russia) have plummeted drastically (see Table 1). Table 1. Car sales in Russia, thousand units sales versus 2008 domestically manufactured cars 390 -44% including AutoVAZ 349.5 -43.8% foreign cars assembled in Russia 360 -38% foreign cars (new) 640 -69% foreign cars (used) 12 -96.6% total 1402 -56% Source: Association of European Businesses However, negative quantitative results are accompanied by positive qualitative changes. Particularly, new models currently prevail in the AutoVAZ sales mix (see Figure 2). Figure 2. AutoVAZ sales mix 100% 80% 4x4 60% Kalina VAZ 2105/2107 40% Samara Priora 20% 0% 2007 2008 2009 Source: AK&M information agency The list of 2009 bestselling cars proves the competitive power of AutoVAZ: Priora tops the list and Kalina is among the top five models (see Table 2). The first full-fledged replacement of the model range (Lada 110 family has been replaced with the Lada Priora versions) has been successfully completed. -

VAZ: ORIGIN, DEVELOPMENT, the CHARACTERISTIC of MODELS D.S.Kolomytsev, S.A.Gusev Scientific Supervisor - Associate Professor R.V

629.113.(114) VAZ: ORIGIN, DEVELOPMENT, THE CHARACTERISTIC OF MODELS D.S.Kolomytsev, S.A.Gusev Scientific supervisor - Associate professor R.V. Aronova Siberian Federal University AvtoVAZ is a Russian automobile manufacturer, also known as VAZ, Volzhsky Au- tomobilny Zavod, and better known to the world as Lada was set up in the late 1960s in colla- boration with Fiat. It is 25% owned by French giant Renault. The VAZ factory is one of the biggest in the world, has over 90 miles (144 km) of production lines and is unique in that most of the components for the cars are made in-house. The original Lada was a basic car, lacking in most luxuries expected in cars of its time and was patterned after the Fiat 124. Ladas were available in several Western countries during the 1970s and 1980s, including Canada, the United Kingdom, France, Belgium, Luxembourg and the Netherlands, though trade sanctions banned their export to the United States. The plant was set up as a collaboration between Italy and the Soviet Union and built on the banks of the Volga river in 1966. A new part of town Togliatti, named after the Italian Communist Party leader Palmiro Togliatti, was built around the factory. The Lada was envi- saged as a "people's car" like the Citroën 2CV or the VW Beetle. The lightweight Italian Fiat 124 was adapted into something intended to survive trea- cherous Russian driving conditions. Among many changes, aluminium brake drums were added to the rear, and the original Fiat engine was dropped in favour of a newer design. -

Cluster of Automotive Industry of Samara Region Cluster of Automotive Industry of Samara Region

Catalogue of cluster members Cluster of Automotive Industry of Samara Region Cluster of Automotive Industry of Samara Region Dear colleagues! The Samara region is one of the leading industrial centers of Russia. In volume of industrial production, it consistently ranks in the top ten among all Russian regions. Automobile production is one of foundations for the development of region’s economy, and it performs a serious social function. The government of the region takes an active part in problems solving and in the formation of the industry's development strategy. An important tool here is the Cluster of Automotive Industry of Samara Region, which is included in the register of Russian industrial clusters. Cluster members have an access to comprehensive state support at the federal and regional levels, and this fact is their competitive advantage, allowing to realize significant joint projects for the region related to the creation of a new, or modified final product of the сluster - car. More than fifty companies are cluster members, including small and Sergey medium-sized businesses. The most important measures of state support are Aleksandrovich focused on the development of these companies. Totally, the region has more Bezrukov than 100 automotive companies that can potentially be united under the aegis of Deputy Chairman of the new association. The сluster forms entire value added chain and leads it to final Government – Minister of manufacturer of cars by aggregating capacities of Samara region’s enterprises. Industry and Technology of the Samara region. One of the most important tasks is to develop the cooperation of cluster enterprises with global suppliers of automotive components in order to build optimal supply chain with the aim to increase the localization level of products in the region and exports from the Russian Federation. -

AVTOVAZ Group* Operating Highlights for 2004

AVTOVAZ Group* Operating Highlights for 2004 Vehicle unit sales by JSC AVTOVAZ 2004 2003 Change 000’s units 000’s units % Domestic market 630 626 + 0.6 Export market 92 92 Total 722 718 + 0.6 Assembly kit unit sales 301 203 + 48 RR million RR million Net sales 160,536 130,772 + 23 Operating income 9,496 5,941 + 60 Consolidated Statement of Operations** Year ended 31 December 2004 2003 Change RR million RR million % Net sales 160,536 130,772 + 23 Cost of sales (133,687) (110,120) + 21 Gross profit 26,849 20,652 + 30 Interest expenses (3,451) (3,416) + 1 Other expenses, net (18,823) (14,285) + 32 Net income for the year 4,575 2,951 + 55 Consolidated Balance Sheet** At 31 December 2004 2003 Change RR million RR million % Cash and cash equivalents 11,966 6,871 + 74 Other current assets 42,048 37,364 + 12 Non-current assets 111,845 107,829 + 4 Total liabilities 82,369 72,562 + 13 Minority interest 1,616 1,290 + 25 Total shareholders’ equity 81,874 78,212 + 5 AVTOVAZ | 2004 JSC AVTOVAZ’s share price and dividend development *** For the year ended 31 December 2004, RR 2003, RR Change, % Share price Ordinary share Closing (weighted average) 775.95 774.7 + 0.16 Annual high (weighted average) 896.33 906.42 - 1.11 Annual low (weighted average) 622.32 582.06 + 6.92 Preference share Closing (weighted average) 773.94 471.88 + 64.01 Annual high (weighted average) 823.30 525.68 + 56.62 Annual low (weighted average) 474.91 339.77 + 39.77 Dividends per ordinary share 23 6.0 + 383.33 per preference share 23 95.0 - 75.79 * The AVTOVAZ Group mentioned hereinafter is the parent company (JSC AVTOVAZ or the “Company”) and all of its subsidiaries and associated companies. -

Guide to Assembly Plants in Europe FINLAND

AN_061113_18_19.qxd 14.11.2006 9:33 Uhr Page 18 Guide to assembly plants in Europe FINLAND 36 NORWAY 5 15 1112 ESTONIA 27 10 12 U. K. 11 SWEDEN DENMARK LATVIA 9 IRELAND 21 2 LITHUANIA 22 14 5 5 6 3 1 19 38 15 9 4 1 8 4 1 4 17 5 BELARUS 1 NETH. 14 13 2 4 6 18 POLAND GERMANY 18 6 35 BELGIUM10 9 1 5 3 2 11 4 28 7 3 7 3 6 B 2 17 5 3 3 16 15 9 C 2 8 8 4 4 1 CZECH REPUBLIC 11 UKRAINE 1 5 1 6 2 12 29 6 12 FRANCE 3 3 SLOVAKIA 6 3 2 10 34 7 5 19 32 AUSTRIA 20 SWITZERLAND 16 MOLDOVA HUNGARY ROMANIA 26 SLOVENIA 6 5 10 25 4 7 10 2 BOSNIA 8 7 8 9 CROATIA and 17 7 13 HERZ. 21 5 PORTUGAL 6 37 8 SPAIN SERBIA 7 8 20 10 7 ITALY A MONTENEGRO BULGARIA MACEDONIA 24 10 13 1 14 30 9 4 2 9 4 ALBANIA 11 GREECE TURKEY 3 NORTH CYPRUS MALTA BMW GROUP (See also 4 16 38 ) 4 Newport Pagnell, UK – Aston Martin Vanquish S 9 Ryton, UK – Peugeot 206 hatchback, station wagon (closes January 2007) 11 Regensburg, Germany – BMW 1 and 3 series 5 Castle Bromwich, UK – Jaguar S-Type, XJ, XK, Daimler Super Eight 10 Trnava, Slovakia – Peugeot 207 2 Munich, Germany – BMW 3 series 6 Solihull, UK – Land Rover Defender, Discovery 3, Range Rover, AA San Benedetto Val di Sangro, Italy (Sevel Sud: Fiat 50%, PSA 50%) – 3 Dingolfing, Germany – BMW 5, 6 and 7 series Range Rover Sport Citroen Jumper/Relay; Fiat Ducato; Peugeot Boxer 4 Oxford, UK – Mini, Mini cabriolet 7 Cologne, Germany – Ford Fiesta, Fusion B Lieu Saint-Amand, France (Sevel Nord: Fiat 50%, PSA 50%) – Citroen Atlante 5 Leipzig, Germany – BMW 3 series 8 Saarlouis, Germany – Ford Focus, Focus C-Max C8, Dispatch/Jumpy; Fiat Scudo, -

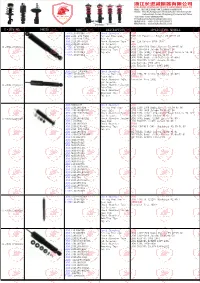

E·Win No. Photo Part No. Description

E·WIN NO. PHOTO PART NO. DESCRIPTION APPLICATION MODELS E·WIN:17430143 Shock Absorber FIAT LADA:2101-291 5402 Fitting Position FIAT 124 Familiare Estate 67.04-75.03 LADA:2121-291 5402 Rear Axle SEAT LADA:2121291540201 Shock Absorber Type Seat 124 Estate 1970-1976 LADA:2101291540204 Oil Pressure LADA E·WIN:17430143 E·WIN:17430141 Shock Absorber LADA 1200-1500 Kombi Estate 73.09-85.06 E·WIN:16430141 Mounting Type LADA 1200-1600 Saloon 70.01-87.01 E·WIN:17430164 Top eye LADA NIVA (2121) Closed Off-Road Vehicle 76.12-/ E·WIN:16430164 LADA NOVA (2105) Saloon 81.05-/ LADA NOVA Kombi (2104) Estate 85.09-/ LADA TOSCANA (2107) Saloon 83.09-/ Lada Kalinka 1981-2001 Lada Kalinka Estate 1985-1994 LADA:2123-2905004 Shock Absorber LADA E·WIN:17430145 Fitting Position LADA NIVA II (2123) Hatchback 02.09-/ E·WIN:16430145 Front Axle CHEVROLET Shock Absorber Type Chevrolet Niva 2002- Gas Pressure E·WIN:17430145 Shock Absorber System Twin-Tube Shock Absorber Mounting Type Top pin LADA:04006798 Shock Absorber LADA LADA:21012905004 Fitting Position LADA 1200-1500 Kombi Estate 73.09-85.06 LADA:2101290500407 Front Axle LADA 1200-1600 Saloon 70.01-87.01 LADA:2101-290 5402 Shock Absorber Type LADA NIVA (2121) Closed Off-Road Vehicle 76.12-/ LADA:67112 Gas Pressure LADA NOVA (2105) Saloon 81.05-/ E·WIN:17430149 LADA:2101290540204 Shock Absorber System LADA NOVA Kombi (2104) Estate 85.09-/ LADA:12410700 Twin-Tube LADA TOSCANA (2107) Saloon 83.09-/ LADA:210129054024 Shock Absorber SKODA LADA:210102905402 Mounting Type SKODA FAVORIT (781) Hatchback 90.10-94.09 LADA:2121-209 -

Spark Plugs Catalog

LPG Techniek VAN MEENEN Catalogus Bougies LPG [email protected] www.vanmeenen.com Tel. +3293786823 PRODUCER MODEL TYPE Litre power (kW) Prod. from Prod. to Engine code Cyl. mm GAS LPG TYPE ALFA ROMEO 145 1.4 i.e. 1.4 66 08.1994 11.1996 AR33.501 4 0,6 04G FE65PS ALFA ROMEO 145 1.6 i.e. 1.6 76 08.1994 11.1996 AR33.201 4 0,6 04G FE65PS ALFA ROMEO 146 1.3 i.e. 1.3 66 07.1995 11.1997 AR33.201 4 0,6 04G FE65PS ALFA ROMEO 146 1.4 i.e. 1.4 66 08.1994 02.1997 AR33.501 4 0,6 04G FE65PS ALFA ROMEO 146 1.6 i.e. 1.6 76 07.1994 12.1997 AR33.201 4 0,6 04G FE65PS ALFA ROMEO 147 1.6 T.S. 16 V 1.6 77 10.2000 AR37.203 4 0,6 17G SFE65PS ALFA ROMEO 155 1.7 i. T.S. 1.7 86 02.1992 04.1993 AR67.103 4 0,6 17G SFE65PS ALFA ROMEO 155 1.7 LT.S. 1.7 95 05.1993 07.1996 AR67.105 4 0,6 17G SFE65PS ALFA ROMEO 155 1.8 i. Twin Spark 1.8 93 02.1992 07.1996 AR67.102 4 0,6 17G SFE65PS ALFA ROMEO 155 1.8 LT.S. 1.8 93 04.1994 07.1996 AR67.101-67.102 4 0,6 17G SFE65PS ALFA ROMEO 155 2.0 i. Turbo 4x4 2.0 137 08.1992 04.1998 AR67.203 4 0,6 04G FE65PS ALFA ROMEO 155 2.0 i. -

Kia Lada (Avtovaz)

C O kW y l Stock-N LPG / CNG KIA SORENTO 1 Sorento 3.3 JC 3.3 177 6 .06- G6DB 1,1 IFR5G11 7854 Sorento 3.5 JC 3.5 143 6 .02- G6CU 1,1 PFR5N-11 5838 Sorento 3.8 JC 3.8 6 .06- G6DA 1,1 IFR5G11 7854 SORENTO 2 Sorento 2.4 CVVT XM 2.4 128 4 11.09- G4KE 1,1 LFR5A-11 6376 LPG 7 SOUL Soul 1.6 CVVT AM 1.6 77 4 02.09- G4FC 1,0 LZKR6B-10E 1578 Soul 1.6 AM 1.6 93 4 02.09- G4FC 1,0 LZKR6B-10E 1578 SPORTAGE 1 Sportage K00 2.0 70 4 .94-12.02 SOHC 0,8 BKR5E 1667 35 LPG 1 Sportage 16V K00 2.0 94 4 .94-08.04 DOHC 16V 1,1 BKR6E-11 2756 14 LPG 1 SPORTAGE 2 Sportage 2.0 JE 2.0 104 4 .06- G4GC 1,1 BKR5ES-11 2382 33 LPG 1 Sportage 2.5 JE 2.5 129 6 09.04- 1,1 BKR5ES-11 2382 33 LPG 1 Sportage 2.7 JE 2.7 129 6 .06- G6BA V6 1,1 PFR5N-11 5838 SPORTAGE 3 Sportage 2.0 CVVT SL 2.0 120 4 07.10- G4KD 1,1 LFR5A-11 6376 LPG 7 VENGA Venga 1.4 YN 1.4 66 4 10.09- G4FA 1,0 LZKR6B-10E 1578 Venga 1.6 YN 1.6 92 4 10.09- G4FC 1,0 LZKR6B-10E 1578 LADA (AVTOVAZ) 112 2112 16V 1.5 54 4 01.96- VAZ-2111 0,8 BPR6ES 4008 2 LPG 2 112 Gli 1.5 67 4 .03- 16V 1,1 BCPR6ES-11 7121 11 LPG 3 1200 1.2 4 0,8 BP5ES 6511 8 LPG 2 2101, 21011, 21012, 21013, 21014 1.2-1.5 ltr 44 4 0,7 BP6ES 7811 4 LPG 2 2107 Lada 1300 L 1.3 4 0,7 BP6ES 7811 4 LPG 2 2107 Lada 1500 L 1.5 4 0,7 BP6ES 7811 4 LPG 2 2108 Samara / Fun 1100 1.1 4 0,7 BP6ES 7811 4 LPG 2 2108 Samara / Fun 1300 1.3 4 0,7 BP6ES 7811 4 LPG 2 2108 Samara / Fun 1500 1.5 4 0,7 BP6ES 7811 4 LPG 2 210993 Samara 1.5 1.5 53 4 01.90- 0,8 BPR6ES 4008 2 LPG 2 210993 Samara 1.5i 1.5 57 4 VAZ-2111 1,1 BPR6ES-11 4824 13 LPG 2 2110 1.5 1.5 53 4 06.96- 0,8 BPR6ES -

THE MARKET of CARS: BEFORE and AFTER CRISIS 1. on The

1 2 R.M.Nureev , D.I.Kondratov THE MARKET OF CARS: BEFORE AND AFTER CRISIS QUALIFIER JEL codes: D24, D43, E23, E27, L13. Keywords: the market of cars, world production, market structures, the analysis costs-benefits, state regulation, the forecast, features of the Russian market. THE SUMMARY In article the market of cars before crisis, features of its growth on a boundary of centuries is considered, manufacturers are investigated world production of vehicles on segments and the largest companies. Change of manufacture of cars for last 20 years is shown. Dynamics of structure of the market of cars in Russia in 2001-2008 is analyzed considered, how modern crisis will affect repartition of the world market of cars and the tendency of its development (in countries and price aspects). Authors do the short-term and long-term forecast of development of the Russian market of cars. 1. On the threshold of crisis. The automobile market has nowadays black times. Recession in the industry in world production has appeared unusually deep. It has captured all countries, but most of all Russia. What reasons of a consequence and expected prospects of its development are problems which are widely discussed in the press. And correctly to answer them it is necessary to analyze tendencies of development which we observed in the XXI-st century beginning. Our first article therefore is devoted the situations which have developed in this market on the threshold of crisis. 1.1. The market of cars: features of growth on a boundary of centuries World production of cars last years grew fast enough rates.