Commercialization of High Efficiency Low Cost CIGS Technology DE-AC36-08-GO28308 Based on Electroplating: Final Technical Progress Report, 28 5B

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2015-SVTC-Solar-Scorecard.Pdf

A PROJECT OF THE SILICON VALLEY TOXICS COALITION 2015 SOLAR SCORECARD ‘‘ www.solarscorecard.com ‘‘ SVTC’s Vision The Silicon Valley Toxics Coalition (SVTC) believes that we still have time to ensure that the PV sector is safe The PV industry’s rapid growth makes for the environment, workers, and communities. SVTC it critical that all solar companies envisions a safe and sustainable solar PV industry that: maintain the highest sustainability standards. 1) Takes responsibility for the environmental and health impacts of its products throughout their life- cycles, including adherence to a mandatory policy for ‘‘The Purpose responsible recycling. The Scorecard is a resource for consumers, institutional purchasers, investors, installers, and anyone who wants 2) Implements and monitors equitable environmental to purchase PV modules from responsible product and labor standards throughout product supply chains. stewards. The Scorecard reveals how companies perform on SVTC’s sustainability and social justice benchmarks 3) Pursues innovative approaches to reducing and to ensure that the PV manufacturers protect workers, work towards eliminating toxic chemicals in PV mod- communities, and the environment. The PV industry’s ule manufacturing. continued growth makes it critical to take action now to reduce the use of toxic chemicals, develop responsible For over three decades, SVTC has been a leader in recycling systems, and protect workers throughout glob- encouraging electronics manufacturers to take lifecycle al PV supply chains. Many PV companies want to pro- responsibility for their products. This includes protecting duce truly clean and green energy systems and are taking workers from toxic exposure and preventing hazardous steps to implement more sustainable practices. -

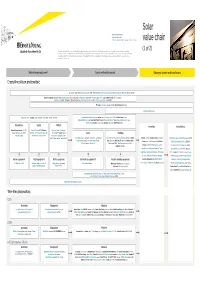

Lsoar Value Chain Value Chain

Solar Private companies in black Public companies in blue Followed by the founding date of companies less than 15 years old value chain (1 of 2) This value chain publication contains information gathered and summarized mainly from Lux Research and a variety of other public sources that we believe to be accurate at the time of ppggyublication. The information is for general guidance only and not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization nor Lux Research can accept responsibility for loss to any person relying on this publication. Materials and equipment Components and products Balance of system and installations Crystalline silicon photovoltaic GCL Silicon, China (2006); LDK Solar, China (2005); MEMC, US; Renewable Energy Corporation ASA, Norway; SolarWorld AG, Germany (1998) Bosch Solar Energy, Germany (2000); Canadian Solar, Canada/China (2001); Jinko Solar, China (2006); Kyocera, Japan; Sanyo, Japan; SCHOTT Solar, Germany (2002); Solarfun, China (2004); Tianwei New Energy Holdings Co., China; Trina Solar, China (1997); Yingli Green Energy, China (1998); BP Solar, US; Conergy, Germany (1998); Eging Photovoltaic, China SOLON, Germany (1997) Daqo Group, China; M. Setek, Japan; ReneSola, China (2003); Wacker, Germany Hyundai Heavy Industries,,; Korea; Isofoton,,p Spain ; JA Solar, China (();2005); LG Solar Power,,; Korea; Mitsubishi Electric, Japan; Moser Baer Photo Voltaic, India (2005); Motech, Taiwan; Samsung -

Solar Photovoltaic Manufacturing: Industry Trends, Global Competition, Federal Support

U.S. Solar Photovoltaic Manufacturing: Industry Trends, Global Competition, Federal Support Michaela D. Platzer Specialist in Industrial Organization and Business January 27, 2015 Congressional Research Service 7-5700 www.crs.gov R42509 U.S. Solar PV Manufacturing: Industry Trends, Global Competition, Federal Support Summary Every President since Richard Nixon has sought to increase U.S. energy supply diversity. Job creation and the development of a domestic renewable energy manufacturing base have joined national security and environmental concerns as reasons for promoting the manufacturing of solar power equipment in the United States. The federal government maintains a variety of tax credits and targeted research and development programs to encourage the solar manufacturing sector, and state-level mandates that utilities obtain specified percentages of their electricity from renewable sources have bolstered demand for large solar projects. The most widely used solar technology involves photovoltaic (PV) solar modules, which draw on semiconducting materials to convert sunlight into electricity. By year-end 2013, the total number of grid-connected PV systems nationwide reached more than 445,000. Domestic demand is met both by imports and by about 75 U.S. manufacturing facilities employing upwards of 30,000 U.S. workers in 2014. Production is clustered in a few states including California, Ohio, Oregon, Texas, and Washington. Domestic PV manufacturers operate in a dynamic, volatile, and highly competitive global market now dominated by Chinese and Taiwanese companies. China alone accounted for nearly 70% of total solar module production in 2013. Some PV manufacturers have expanded their operations beyond China to places like Malaysia, the Philippines, and Mexico. -

Expanding the Photovoltaic Supply Chain in the United States: Opportunities and Challenges

Expanding the Photovoltaic Supply Chain in the United States: Opportunities and Challenges Brittany L. Smith and Robert Margolis NREL is a national laboratory of the U.S. Department of Energy Technical Report Office of Energy Efficiency & Renewable Energy NREL/TP-6A20-73363 Operated by the Alliance for Sustainable Energy, LLC July 2019 This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications. Contract No. DE-AC36-08GO28308 Expanding the Photovoltaic Supply Chain in the United States: Opportunities and Challenges Brittany L. Smith and Robert Margolis Suggested Citation Smith, Brittany L., and Robert Margolis. (2019). Expanding the Photovoltaic Supply Chain in the United States: Opportunities and Challenges. Golden, CO: National Renewable Energy Laboratory. NREL/TP-6A20-73363. https://www.nrel.gov/docs/fy19osti/73363.pdf. NREL is a national laboratory of the U.S. Department of Energy Technical Report Office of Energy Efficiency & Renewable Energy NREL/TP-6A20-73363 Operated by the Alliance for Sustainable Energy, LLC July 2019 This report is available at no cost from the National Renewable Energy National Renewable Energy Laboratory Laboratory (NREL) at www.nrel.gov/publications. 15013 Denver West Parkway Golden, CO 80401 Contract No. DE-AC36-08GO28308 303-275-3000 • www.nrel.gov NOTICE This work was authored by the National Renewable Energy Laboratory, operated by Alliance for Sustainable Energy, LLC, for the U.S. Department of Energy (DOE) under Contract No. DE-AC36- 08GO28308. Funding provided by the U.S. Department of Energy Office of Energy Efficiency and Renewable Energy Solar Energy Technologies Office. -

The Seeds of Solar Innovation: How a Nation Can Grow a Competitive Advantage by Donny Holaschutz

The Seeds of Solar Innovation: How a Nation can Grow a Competitive Advantage by Donny Holaschutz B.A. Hispanic Studies (2004), University of Texas at Austin B.S. Aerospace Engineering (2004), University of Texas at Austin M.S.E Aerospace Engineering (2007), University of Texas at Austin Submitted to the System Design and Management Program In Partial Fulfillment of the Requirements for the Degree of Master of Science in Engineering and Management ARCHIVES MASSACHUSETTS INSTITUTE at the OF TECHNOLOGY Massachusetts Institute of Technology February 2012 © 2012 Donny Holaschutz. All rights reserved The author hereby grants to MIT permission to reproduce and to distribute publicly paper and electronic copies of this thesis document in whole or in part in any medium now known or hereqfter reated. Signed by Author: Donny Holaschutz Engineering Systems Division and Sloan School of Management January 20, 2012 Certified by: James M. Utterback, Thesis Supervisor David . McGrath jr (1959) Professor of Management and Innovation and Professor of neering SysemsIT oan School of Management Accepted by: Patrick C.Hale Director otS ystem Design and Management Program THIS PAGE INTENTIONALLY LEFT BLANK Table of Contents Fig u re List ...................................................................................................................................................... 5 T ab le List........................................................................................................................................................7 Executive -

US Solar Photovoltaic Manufacturing

U.S. Solar Photovoltaic Manufacturing: Industry Trends, Global Competition, Federal Support Michaela D. Platzer Specialist in Industrial Organization and Business May 30, 2012 Congressional Research Service 7-5700 www.crs.gov R42509 CRS Report for Congress Prepared for Members and Committees of Congress U.S. Solar PV Manufacturing: Industry Trends, Global Competition, Federal Support Summary Every President since Richard Nixon has sought to increase U.S. energy supply diversity. In recent years, job creation and the development of a domestic renewable energy manufacturing base have joined national security and environmental concerns as rationales for promoting the manufacturing of solar power equipment in the United States. The federal government maintains a variety of tax credits, loan guarantees, and targeted research and development programs to encourage the solar manufacturing sector, and state-level mandates that utilities obtain specified percentages of their electricity from renewable sources have bolstered demand for large solar projects. The most widely used solar technology involves photovoltaic (PV) solar modules, which draw on semiconducting materials to convert sunlight into electricity. By year-end 2011, the total number of grid-connected PV systems nationwide reached almost 215,000. Domestic demand is met both by imports and by about 100 U.S. manufacturing facilities employing an estimated 25,000 U.S. workers in 2011. Production is clustered in a few states, including California, Oregon, Texas, and Ohio. Domestic PV manufacturers operate in a dynamic and highly competitive global market now dominated by Chinese and Taiwanese companies. All major PV solar manufacturers maintain global sourcing strategies; the only U.S.-based manufacturer ranked among the top 10 global cell producers in 2010 sourced the majority of its panels from its factory in Malaysia. -

About to Explode

PHOTOVOLTAICS USA/MANUFACTURERS About to explode Projects in the non- Similar to other PV markets, the development in the United States is residential market segment, such as this characterized by excess capacities in manufacturing and a rapid price rooftop PV system in decline for component of solar power plants. Nevertheless, the US industry California, have been the driving force behind representatives are less pessimistic about the future than their colleagues the US solar market. Photo: Europressedienst in Europe. It shows that the markets are quite different from each other. ata by the Solar Energy Industries Association range of 31.14 % for companies found to benefit from (SEIA) suggests that the newly installed PV ca unfair subsidies and price dumping as well as Dpacity on the US market had reached 1,855 MW 249.96 % for companies that did not collaborate with in 2011, exceeding the previous record year 2010 the US customs service or failed to provide the infor (887 MW) by nearly 110 %. Generally, the solar indus mation needed. “The decision by the US Department try has therefore reason to be pleased with the devel of Commerce encourages us to believe that we can re opment in the last year. The newly installed capacities turn to fair competition,” explains Frank Asbeck, CEO had been equivalent to a market share of 7 % (2010: of SolarWorld. The path on the US market seems now 5 %) in the global new installa tions. The trend is ex open for a positive trend that could be comparable to pected to continue over the next few years – not least the last year. -

Photovoltaic Thin Film Cells 2009

i Photovoltaic Thin Film Cells 2009 France Innovation Scientifique & Transfert FRINNOV 83 Boulevard Exelmans 75016 PARIS, FRANCE Tel.: +33 (0)1 40 51 00 90 Fax: +33 (0)1 40 51 78 58 www.frinnov.fr Patent Mapping - A new tool to decipher market trends MULTI-CLIENT PATENT LANDSCAPE ANALYSIS IP Overview is a report that analyses all patent families filed on a given thematic Available reports in engineering sciences are Carbon nanotubes, Photovoltaic cells (3 reports), LiMPO4 batteries TAILOR-MADE PATENT LANDSCAPE ANALYSIS IP Overview On Demand is similar to IP Overview but 100% tailored to your needs Ask your questions and we will answer by a specific analysis of the patent landscape of your area of interest CUSTUMIZED STUDIES OF PATENT PORTFOLIOS Position your patent portfolio or the one of your competitors PRIOR-ART SEARCH Need more information? Free access to the interactive database Contact us at [email protected] is provided for studies published since 2010 Photovoltaic Thin Film Cells CContents METHODOLOGY 11 INTRODUCTION 12 1. BRIEF OUTLINE OF THE PHOTOVOLTAICS MARKET 14 2. GLOBAL OVERVIEW OF PHOTOVOLTAIC PATENTS 17 2.1. Technological segmentation 18 2.2. Segmentation by application 20 2.3. Zoom on companies involved in the market 22 2.4. Zoom on CANON 24 2.4.1. History of patent application filings and ambitions 24 2.4.2. Segmentation of the patent portfolio 25 2.4.3. Filing policy 26 2.4.4. Analysis of the patent portfolio 28 3. THIN FILM CELL PATENTS - WORLD ANALYSIS 31 3.1. Protection strategies 31 3.1.1. -

DOE Solar Energy Technologies Program FY 2007 Annual Report

DOE Solar Energy Technologies Program Welcome to the fiscal year (FY) 2007 Annual Report for the U.S. Department of Energy’s Solar Energy Technologies Program (Solar Program). The Solar Program is responsible for carrying out the federal role of researching, developing, demonstrating, and deploying solar energy technologies. This document presents a detailed description of the activities funded by DOE during FY 2007. FY 2007 was a year of incredible importance for the Solar Program and its partners. Announced during President Bush’s 2006 State of the Union address, the Advanced Energy Initiative includes the Solar America Initiative (SAI), a presidential initiative with the goal of achieving grid parity for solar electricity, produced by photovoltaic (PV) systems, across the nation by 2015. FY 2007 was the first official year of SAI and represented a shift in Solar Program operations, budget, activities, and partnerships. As a 9-year initiative, SAI is dependent upon wise choices made during its early years. I am pleased to report that FY 2007 represented a successful start to this critically important effort. A few of the many highlights achieved in FY 2007 and discussed in greater detail within this report include: • Launch of the Technology Pathway Partnerships (TPPs), public-private partnerships with industry designed to create fully scalable PV systems that meet the SAI cost goals. The TPPs are characterized by rigorous review and down-selection processes, as well as ambitious timetables. • Establishment of the PV Incubator activity, which funds the development of PV-system components to shorten their timeline to commercialization. • Initiation of a groundbreaking market transformation effort to help commercialize solar technologies by eliminating market barriers and promoting deployment opportunities through outreach activities. -

Tim Dwight, Falcons Standout, Headlines 8Th Annual Solar Summit

Tim Dwight, Falcons Standout, Headlines 8th Annual Solar Summit FROM THE DESK OF THE CHAIRMAN As the solar revolution continues at a torrid pace, it's more important now than ever to keep up with the latest news, trends, policy, and players that shape and form the solar industry in Georgia. Let's face it, this is not always easy to do. It's challenging enough with our busy modern lives to balance work, family and community, let alone keep up with this rapidly changing industry. Which is why for one day each year GA Solar pulls out all the stops to bring industry stakeholders together under one roof to learn and network. Whether you're an industry insider, just getting into the market, a curious solar advocate, or student, you are invited to join us for the 8th Annual Southern Solar Summ it on Thursday October 20th at Georgia Tech's GTRI Conference Center. This year we have a stellar lineup including keynote speakers Terry Jester, a years-long solar veteran, and Tim Dwight, Atlanta Falcon fan favorite turned solar advocate. Hear from 4 of the 5 Public Service Commissioners with updates from this year's IRP. Find out how Stephanie S. Benfield, Atlanta Office of Sustainability, is turning Atlanta into a leader in solar and a model for local governments. Meet Dr . Marilyn Brown, Brook Byers Professor of Sustainable Systems at the Georgia Institute of Technology. Get an update from Georgia Power with Ervin Hancock. And get caught up with four panel and roundtable discussions featuring top industry experts discussing the latest industry trends. -

Crystalline Silicon Photovoltaic Cells and Modules from China

Crystalline Silicon Photovoltaic Cells and Modules From China Investigation Nos. 701-TA-481 and 731-TA-1190 (Final) Publication 4360 November 2012 U.S. International Trade Commission Washington, DC 20436 U.S. International Trade Commission COMMISSIONERS Irving A. Williamson, Chairman Daniel R. Pearson Shara L. Aranoff Dean A. Pinkert David S. Johanson Meredith M. Broadbent Robert B. Koopman Director, Office of Operations Staff assigned Christopher Cassise, Senior Investigator Andrew David, Industry Analyst Aimee Larsen, Economist Samantha Day, Economist David Boyland, Accountant Mary Jane Alves, Attorney Lita David-Harris, Statistician Jim McClure, Supervisory Investigator Address all communications to Secretary to the Commission United States International Trade Commission Washington, DC 20436 U.S. International Trade Commission Washington, DC 20436 www.usitc.gov Crystalline Silicon Photovoltaic Cells and Modules From China Investigation Nos. 701-TA-481 and 731-TA-1190 (Final) Publication 4360 November 2012 C O N T E N T S Page Determinations ................................................................. 1 Views of the Commission ......................................................... 3 Dissenting opinion of Chairman Irving A. Williamson and Commissioner Dean A. Pinkert on critical circumstances ......................................................... 47 Part I: Introduction ............................................................ I-1 Background .................................................................. I-1 Organization -

U.S. Solar Market Insight Report | Q4 2011 & 2011 Year-In-Review | Full Report

Q1 Q2 Q3 Q4 Q4 Q3 Q2 Q1 Q1 Q2 Q3 Q4 Q3 Q2 Q1 Q1 Q2 Q3 Q4 Q4 Q3 Q2 Q1 Q4 Q3 Q2 Q1 Q1 Q2 Q3 Q4 Q4 Q3 Q2 Q1 Q2 Q3 Q4 Q4 Q3 Q2 Q1 Q1 Q2 Q3 Q4 U.S. SOLAR MARKET INSIGHT REPORT | Q4 2011 & 2011 YEAR-IN-REVIEW | FULL REPORT A Greentech Media Company U.S. Solar Market Insight ™ U.S. Solar Market InsightTM TABLE OF CONTENTS 1. INTRODUCTION 5 2. PHOTOVOLTAICS (PV) 6 2.1 Installations 8 2.1.1 Shipments vs. Installations 9 2.1.2 By Market Segment 10 2.1.3 By State 17 2.2 Installed Price 31 2.3 Manufacturing 36 2.3.1 Active U.S. Manufacturing Plants 38 2.3.2 New Plants in 2012 and 2013 39 2.3.3 Polysilicon 41 2.3.4 Wafers 41 2.3.5 Cells 42 2.3.6 Modules 42 2.3.7 Inverters 44 2.4 Component Pricing 49 2.4.1 Polysilicon, Wafers, Cells and Modules 49 2.4.2 Inverters 50 2.5 Installation Forecast 50 3. CONCENTRATING SOLAR POWER (CSP) 54 3.1 Installations 54 3.2 Manufacturing Production 57 3.3 Demand Projections 57 APPENDIX A: METRICS & CONVERSIONS 60 PHOTOVOLTAICS 60 CONCENTRATING SOLAR POWER 60 APPENDIX B: METHODOLOGY AND DATA SOURCES 61 HISTORICAL INSTALLATIONS (NUMBER, CAPACITY, AND OWNERSHIP STRUCTURE): 61 AVERAGE SYSTEM PRICE: 62 MANUFACTURING PRODUCTION & COMPONENT PRICING: 63 A Greentech Media Company © Copyright 2012 SEIA/GTM Research 2 U.S. Solar Market Insight ™ U.S. Solar Market InsightTM LIST OF FIGURES Figure 2-1: U.S.