Photovoltaic Thin Film Cells 2009

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Konarka Technologies

Colorado Renewable Energy Collaboratory Partners for Clean Energy Center for Revolutionary Solar Photoconversion updateSummer 2010 CRSP Research Profile Plasma Sheds Light on Mysteries of PV Efficiency Stars are made of plasma, an ionized gas comprising a complex mixture of gas-phase species. So it’s remarkable that CRSP researchers are using plasmas to create photovoltaic (PV) devices that can better convert energy from our own star, the sun, into power we can use here on Earth. A CRSP research team, made up of re- searchers from CSU and NREL, has been using plasmas to modify PV materials and improve the interfaces between the layers of materials in thin-film solar cells. The goal is to increase efficiency in PV devices. Ellen Fisher is an analytical/materials The CRSP plasma processing project team Ina Martin (left) and Ellen Fisher are shown chemist and the project’s principle investiga- includes Ina Martin, an analytical chemist at in the laboratory with a low-pressure rf plasma reactor. The two chemists work to- tor at CSU. “We know we can use plasmas NREL. Her role is to extend the character- gether on a CRSP project that uses plasmas to change materials and get different device ization of the modified materials and evalu- results, but we need to know exactly how it to modify PV materials and improve the ate the resulting devices under real-world interfaces between the layers of materials in works,” she says. conditions. The rest of the team includes thin-film solar cells. Credit: Jeff Shearer. The team is developing new materials for Michael Elliott, a CSU electrochemist with solar cells by taking known materials, such a background in PV device testing; Patrick McCurdy, a CSU staff scientist who special- chemistry, applying these results to as titanium dioxide (TiO2), and improv- ing their properties. -

2015-SVTC-Solar-Scorecard.Pdf

A PROJECT OF THE SILICON VALLEY TOXICS COALITION 2015 SOLAR SCORECARD ‘‘ www.solarscorecard.com ‘‘ SVTC’s Vision The Silicon Valley Toxics Coalition (SVTC) believes that we still have time to ensure that the PV sector is safe The PV industry’s rapid growth makes for the environment, workers, and communities. SVTC it critical that all solar companies envisions a safe and sustainable solar PV industry that: maintain the highest sustainability standards. 1) Takes responsibility for the environmental and health impacts of its products throughout their life- cycles, including adherence to a mandatory policy for ‘‘The Purpose responsible recycling. The Scorecard is a resource for consumers, institutional purchasers, investors, installers, and anyone who wants 2) Implements and monitors equitable environmental to purchase PV modules from responsible product and labor standards throughout product supply chains. stewards. The Scorecard reveals how companies perform on SVTC’s sustainability and social justice benchmarks 3) Pursues innovative approaches to reducing and to ensure that the PV manufacturers protect workers, work towards eliminating toxic chemicals in PV mod- communities, and the environment. The PV industry’s ule manufacturing. continued growth makes it critical to take action now to reduce the use of toxic chemicals, develop responsible For over three decades, SVTC has been a leader in recycling systems, and protect workers throughout glob- encouraging electronics manufacturers to take lifecycle al PV supply chains. Many PV companies want to pro- responsibility for their products. This includes protecting duce truly clean and green energy systems and are taking workers from toxic exposure and preventing hazardous steps to implement more sustainable practices. -

Light Trapping in Thin Film Organic Solar Cells

Light trapping in thin film organic solar cells Zheng Tang, Wolfgang Tress and Olle Inganäs Linköping University Post Print N.B.: When citing this work, cite the original article. Original Publication: Zheng Tang, Wolfgang Tress and Olle Inganäs, Light trapping in thin film organic solar cells, 2014, Materials Today, (17), 8, 389-396. http://dx.doi.org/10.1016/j.mattod.2014.05.008 Copyright: Elsevier / Elsevier: Creative Commons http://www.elsevier.com/ Postprint available at: Linköping University Electronic Press http://urn.kb.se/resolve?urn=urn:nbn:se:liu:diva-103929 Materials Today Volume 17, Number 8 October 2014 RESEARCH Review Light trapping in thin film organic solar cells RESEARCH: Zheng Tang*, Wolfgang Tress and Olle Ingana¨s* Biomolecular and Organic Electronics, IFM, and Center of Organic Electronics, Linko¨ping University, SE-581 83 Linko¨ping, Sweden A major issue in organic solar cells is the poor mobility and recombination of the photogenerated charge carriers. The active layer has to be kept thin to facilitate charge transport and minimize recombination losses. However, optical losses due to inefficient light absorption in the thin active layers can be considerable in organic solar cells. Therefore, light trapping schemes are critically important for efficient organic solar cells. Traditional light trapping schemes for thick solar cells need to be modified for organic thin film solar cells in which coherent optics and wave effects play a significant role. In this review, we discuss the light trapping schemes for organic thin film solar cells, which includes geometric engineering of the structure of the solar cell at the micro and nanoscale, plasmonic structures, and more. -

Graphene-Based Composite Thin Films for Electronics

NANO LETTERS 2009 Graphene-based Composite Thin Films Vol. 9, No. 2 for Electronics 814-818 Goki Eda and Manish Chhowalla* Rutgers UniVersity, Materials Science and Engineering, Piscataway, New Jersey 08854 Received November 21, 2008; Revised Manuscript Received January 4, 2009 ABSTRACT The electrical properties of solution-processed composite thin films consisting of functionalized graphene sheets (FGS) as the filler and polystyrene (PS) as the host material are described. We demonstrate that transistors from graphene-based composite thin films exhibit ambipolar field effect characteristics, suggesting transport via percolation among FGS in the insulating PS matrix. Device characteristics as a function of the FGS size are also reported. The results indicate that devices fabricated using the largest size FGS yield the highest mobility values. This simple and scaleable fabrication scheme based on a commodity plastic could be useful for low-cost, macro-scale electronics. Graphene-based composites are emerging as new class of introduction of percolating graphene network within an materials that hold promise for several applications.1 Graphene, insulating material may render it semiconducting. In this a single sheet of graphite, possesses extraordinary electrical, study, we show that incorporation of functionalized graphene thermal, and mechanical properties arising from its unique sheets (FGS) in polystyrene (PS) matrix results in composite structure.2 When incorporated into polymer3-6 or ceramic7 thin films that are semiconducting and exhibit ambipolar field matrices, these properties manifest as remarkable improve- effect. These composites can be deposited uniformly over ments in the host material. Graphene-based polymer com- large areas in the form of thin films from solution onto which posites exhibit extraordinarily low electrical percolation devices can be fabricated without extensive lithography. -

Research Into Fabrication and Popularization of Organic Thin Film Solar Cells, Chemical Engineering Transactions, 55, 25-30 DOI:10.3303/CET1655005 26

25 A publication of CHEMICAL ENGINEERING TRANSACTIONS VOL. 55, 2016 The Italian Association of Chemical Engineering Online at www.aidic.it/cet Guest Editors: Tichun Wang, Hongyang Zhang, Lei Tian Copyright © 2016, AIDIC Servizi S.r.l., ISBN 978-88-95608-46-4; ISSN 2283-9216 DOI: 10.3303/CET1655005 Research into Fabrication and Popularization of Organic Thin Film Solar Cells Bin Zhang*a, Yan Lia, Shanlin Qiaob, Le Lic, Zhanwen Wanga a Hebei Chemical & Pharmaceutical College, No. 88 Fangxing Road, Shijiazhuang, Hebei Province, China; b Qingdao Institute of Bioenergy and Bioprocess Technology, Chinese Academy of Sciences, No. 189 Songling Road, Qingdao, Shandong Province, China c Shijiazhuang Naienph Chemical Technology Co., Ltd, No. 12 Shifang Road, Shijiazhuang, Hebei Province, China. [email protected] An analysis was conducted herein on the research status of several popular solar cells at the present stage, including silicon solar cell, thin film photovoltaic cell, and dye-sensitized solar cell (DSSC). In doing so, we concluded that the current situations provide a favorable objective environment for the popularization of organic thin film solar cells. Finally, we reviewed the merits and demerits of the organic thin film solar cell together with the major research focus on and progress of it, and summarized obstacles to and development trails of the popularization of organic thin film solar cells. 1. Introduction As the energy crisis further deepens in the 21st century, the existing development level for solar cells has already failed to satisfy increasing social demands for energy. This phenomenon is mainly reflected in the costly high-purity silicon solar panels, in the defects at new amorphous silicon (a-Si) during energy conversion, and in the limited theoretical energy conversion efficiency (around 25%) of silicon solar panels as well. -

Reflectance in Thin Films

TECHNICAL PAPER Reflectance in Thin Films Abstract Reflectance (R) is the fraction of incident light reflected from a surface and is an intrinsic optical property of thin films. It is essential in determining color, transparency and polarization characteristics of the film. Total internal reflectance is also important in devices such as optical waveguides. Reflectance depends on the energy band structure and associated plasma frequency of charge carriers. As a result, high reflection spectral regions are different for metals, semiconductors and insulators. Basic relations that determine reflectance will be presented and related to refractive index, extinction coefficient, color and transparency of these three classes of thin film materials. Reflectance of thin films also depends on thickness and surface quality. In addition to spectral dependence, the color associated with reflectance can also be described by Tristimulus values and Chromaticity diagrams. Antireflection and high reflection multilayer thin film coatings will also be addressed. Introduction The reflectivity or reflectance (R), of a surface is an intrinsic optical property of a surface. In many optical, electrooptic, telecommunications, solar concentrator and architectural applications, reflectance must either be controlled (reduced or enhanced), or the color of the object changed (e.g., given a “gold” color). For example, heat mirrors are used to reflect infrared wavelengths to reduce heat loss or ingress through windows. Infrared reflectance must be maximized while keeping visible light transmission through the window high. Multilayer low-e and solar control coatings are used to achieve this performance but must be applied to low cost plastic films and glazings. Combined with absorption, reflectance determines color and intensity (or energy) of reflected light. -

Encapsulation of Organic and Perovskite Solar Cells: a Review

Review Encapsulation of Organic and Perovskite Solar Cells: A Review Ashraf Uddin *, Mushfika Baishakhi Upama, Haimang Yi and Leiping Duan School of Photovoltaic and Renewable Energy Engineering, University of New South Wales, Sydney 2052, Australia; [email protected] (M.B.U.); [email protected] (H.Y.); [email protected] (L.D.) * Correspondence: [email protected] Received: 29 November 2018; Accepted: 21 January 2019; Published: 23 January 2019 Abstract: Photovoltaic is one of the promising renewable sources of power to meet the future challenge of energy need. Organic and perovskite thin film solar cells are an emerging cost‐effective photovoltaic technology because of low‐cost manufacturing processing and their light weight. The main barrier of commercial use of organic and perovskite solar cells is the poor stability of devices. Encapsulation of these photovoltaic devices is one of the best ways to address this stability issue and enhance the device lifetime by employing materials and structures that possess high barrier performance for oxygen and moisture. The aim of this review paper is to find different encapsulation materials and techniques for perovskite and organic solar cells according to the present understanding of reliability issues. It discusses the available encapsulate materials and their utility in limiting chemicals, such as water vapour and oxygen penetration. It also covers the mechanisms of mechanical degradation within the individual layers and solar cell as a whole, and possible obstacles to their application in both organic and perovskite solar cells. The contemporary understanding of these degradation mechanisms, their interplay, and their initiating factors (both internal and external) are also discussed. -

DOE Solar Energy Technologies Program FY 2005 Annual

DOE Solar Energy Technologies Program Cover Photos (clockwise from lower right): On August 8, 2005, President George W. Bush visited the National Solar Thermal Test Facility at Sandia National Laboratories as part of his signing of the Energy Bill. R.J. Montoya Photo National Renewable Energy Laboratory researchers use a computer-controlled data acquisition system at the laboratory’s Outdoor Test Facility to characterize the performance and reliability of PV cells and modules. Jim Yost, PIX14094 A Cornell University student cleans the solar-powered rooftop of his team’s entry in preparation for the 2005 Solar Decathlon competition in Washington, D.C. Stefano Paltera/Solar Decathlon Global Solar Energy, a member of the Thin Film PV Partnership, produces PV material by depositing CIGS (copper indium gallium diselenide) on a lightweight, flexible polymide substrate in roll form. Global Solar Energy, PIX13419 The DOE Solar Energy Technologies Program Raymond A. Sutula, Manager, DOE Solar Energy Technologies Program The Solar Energy Technologies Program, within the U.S. Department of Energy's Office of Energy Efficiency and Renewable Energy (EERE), is responsible for developing solar energy technologies that can convert sunlight to useful energy and make that energy available to satisfy a significant portion of our nation's energy needs in a cost-effective way. The Solar Program supports research and development that addresses a wide range of applications, including on- site electricity generation, thermal energy for space heating and hot water, and large-scale power production. This is a great time to be involved with solar energy. Photovoltaic (PV) systems are being installed in the United States and around the world in unprecedented quantities. -

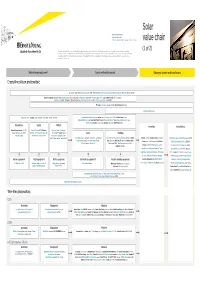

Lsoar Value Chain Value Chain

Solar Private companies in black Public companies in blue Followed by the founding date of companies less than 15 years old value chain (1 of 2) This value chain publication contains information gathered and summarized mainly from Lux Research and a variety of other public sources that we believe to be accurate at the time of ppggyublication. The information is for general guidance only and not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization nor Lux Research can accept responsibility for loss to any person relying on this publication. Materials and equipment Components and products Balance of system and installations Crystalline silicon photovoltaic GCL Silicon, China (2006); LDK Solar, China (2005); MEMC, US; Renewable Energy Corporation ASA, Norway; SolarWorld AG, Germany (1998) Bosch Solar Energy, Germany (2000); Canadian Solar, Canada/China (2001); Jinko Solar, China (2006); Kyocera, Japan; Sanyo, Japan; SCHOTT Solar, Germany (2002); Solarfun, China (2004); Tianwei New Energy Holdings Co., China; Trina Solar, China (1997); Yingli Green Energy, China (1998); BP Solar, US; Conergy, Germany (1998); Eging Photovoltaic, China SOLON, Germany (1997) Daqo Group, China; M. Setek, Japan; ReneSola, China (2003); Wacker, Germany Hyundai Heavy Industries,,; Korea; Isofoton,,p Spain ; JA Solar, China (();2005); LG Solar Power,,; Korea; Mitsubishi Electric, Japan; Moser Baer Photo Voltaic, India (2005); Motech, Taiwan; Samsung -

Solar Is Driving a Global Shift in Electricity Markets

SOLAR IS DRIVING A GLOBAL SHIFT IN ELECTRICITY MARKETS Rapid Cost Deflation and Broad Gains in Scale May 2018 Tim Buckley, Director of Energy Finance Studies, Australasia ([email protected]) and Kashish Shah, Research Associate ([email protected]) Table of Contents Executive Summary ......................................................................................................... 2 1. World’s Largest Operational Utility-Scale Solar Projects ........................................... 4 1.1 World’s Largest Utility-Scale Solar Projects Under Construction ............................ 8 1.2 India’s Largest Utility-Scale Solar Projects Under Development .......................... 13 2. World’s Largest Concentrated Solar Power Projects ............................................... 18 3. Floating Solar Projects ................................................................................................ 23 4. Rooftop Solar Projects ................................................................................................ 27 5. Solar PV With Storage ................................................................................................. 31 6. Corporate PPAs .......................................................................................................... 39 7. Top Renewable Energy Utilities ................................................................................. 44 8. Top Solar Module Manufacturers .............................................................................. 49 Conclusion ..................................................................................................................... -

Solar Photovoltaic Manufacturing: Industry Trends, Global Competition, Federal Support

U.S. Solar Photovoltaic Manufacturing: Industry Trends, Global Competition, Federal Support Michaela D. Platzer Specialist in Industrial Organization and Business January 27, 2015 Congressional Research Service 7-5700 www.crs.gov R42509 U.S. Solar PV Manufacturing: Industry Trends, Global Competition, Federal Support Summary Every President since Richard Nixon has sought to increase U.S. energy supply diversity. Job creation and the development of a domestic renewable energy manufacturing base have joined national security and environmental concerns as reasons for promoting the manufacturing of solar power equipment in the United States. The federal government maintains a variety of tax credits and targeted research and development programs to encourage the solar manufacturing sector, and state-level mandates that utilities obtain specified percentages of their electricity from renewable sources have bolstered demand for large solar projects. The most widely used solar technology involves photovoltaic (PV) solar modules, which draw on semiconducting materials to convert sunlight into electricity. By year-end 2013, the total number of grid-connected PV systems nationwide reached more than 445,000. Domestic demand is met both by imports and by about 75 U.S. manufacturing facilities employing upwards of 30,000 U.S. workers in 2014. Production is clustered in a few states including California, Ohio, Oregon, Texas, and Washington. Domestic PV manufacturers operate in a dynamic, volatile, and highly competitive global market now dominated by Chinese and Taiwanese companies. China alone accounted for nearly 70% of total solar module production in 2013. Some PV manufacturers have expanded their operations beyond China to places like Malaysia, the Philippines, and Mexico. -

Commercialization Potential of Dye-Sensitized Mesoscopic Solar Cells

Commercialization Potential of Dye-Sensitized Mesoscopic Solar Cells by Kwan Wee Tan B.Eng (Materials Engineering) Nanyang Technological University, 2006 SUBMITTED TO THE DEPARTMENT OF MATERIALS SCIENCE AND ENGINEERING IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF ENGINEERING IN MATERIALS SCIENCE AND ENGINEERING AT THE MASSACHUSETTS INSTITUTE OF TECHNOLOGY SEPTEMBER 2008 © 2008 Kwan Wee Tan. All rights reserved. The author hereby grants to MIT permission to reproduce and to distribute publicly paper and electronic copies of this thesis document in whole or in part in any medium now known or hereafter created. Signature of Author ……………………………………………………………………….... Department of Materials Science and Engineering July 16, 2008 Certified by ...……………………………………………………………………………..... Yet-Ming Chiang Kyocera Professor of Ceramics Thesis Supervisor Certified by ...……………………………………………………………………………..... Chee Cheong Wong Associate Professor, Nanyang Technological University Thesis Supervisor Accepted by ……………………………………………………………………………….... Samuel M. Allen POSCO Professor of Physical Metallurgy Chair, Departmental Committee for Graduate Students 1 Commercialization Potential of Dye-Sensitized Mesoscopic Solar Cells By Kwan Wee Tan Submitted to the Department of Materials Science and Engineering on July 16, 2008 in partial fulfillment of the requirements for the Degree of Master of Engineering in Materials Science and Engineering ABSTRACT The price of oil has continued to rise, from a high of US$100 per barrel at the beginning 2008 to a new record of above US$140 in the recent weeks (of July). Coupled with increasing insidious greenhouse gas emissions, the need to harness abundant and renewable energy sources is never more urgent than now. The sun is the champion of all energy sources and photovoltaic cell production is currently the world’s fastest growing energy market.