Banking & Financial Awareness

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Study on Economic Dimensions of India and China

A Study on Economic Dimensions of India and China Sunil Kumar Das Bendi Modern Institute of Technology and Management, Bhubaneswar E-mail: [email protected] Tushar Kanta Pany HOD, School of Commerce, Ravenshaw University, Cuttack E-mail: [email protected] Abstract India and China are the two emerging economies of the world. They are the two most populous countries in the world who together account for more than a third of the world’s total population. A descriptive research study has been carried out for investigating the Gross Domestic Product of India and China in nominal and purchasing power parity basis. It also compares per capita gross domestic product and GDP growth rate of India and China. It also investigates the trends in the value of Chinese Yuan Renminbi (CNY) with Indian Rupee (INR). This paper also exhibits the market share in Foreign Direct Investment in Asia Pacific region in 2015. The dramatic rise not only enabled socio- economic upsurge of India and China but it also reshaped the regional and global trade trends. India replaced China as leading recipient of capital investment in Asia-Pacific with announced FDI of $63bn, as well as an 8 per cent increase in project numbers to 697. India faced various structural bottlenecks including delays in project approval, ill-targeted subsidies, a low manufacturing base and low agricultural productivity, difficulty in land acquisition, weak transportation and power networks, strict labour regulations and skill mismatches. Keywords : Foreign Direct Investment, Gross Domestic Product 1.0 Introduction Indo-China relations refer to international relations in 1978, China’s economic growth performance has been between the People’s Republic of China (PRC) and the truly dramatic. -

The Unicode Standard, Version 6.3

Currency Symbols Range: 20A0–20CF This file contains an excerpt from the character code tables and list of character names for The Unicode Standard, Version 6.3 This file may be changed at any time without notice to reflect errata or other updates to the Unicode Standard. See http://www.unicode.org/errata/ for an up-to-date list of errata. See http://www.unicode.org/charts/ for access to a complete list of the latest character code charts. See http://www.unicode.org/charts/PDF/Unicode-6.3/ for charts showing only the characters added in Unicode 6.3. See http://www.unicode.org/Public/6.3.0/charts/ for a complete archived file of character code charts for Unicode 6.3. Disclaimer These charts are provided as the online reference to the character contents of the Unicode Standard, Version 6.3 but do not provide all the information needed to fully support individual scripts using the Unicode Standard. For a complete understanding of the use of the characters contained in this file, please consult the appropriate sections of The Unicode Standard, Version 6.3, online at http://www.unicode.org/versions/Unicode6.3.0/, as well as Unicode Standard Annexes #9, #11, #14, #15, #24, #29, #31, #34, #38, #41, #42, #44, and #45, the other Unicode Technical Reports and Standards, and the Unicode Character Database, which are available online. See http://www.unicode.org/ucd/ and http://www.unicode.org/reports/ A thorough understanding of the information contained in these additional sources is required for a successful implementation. -

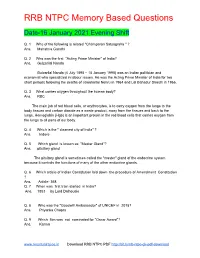

RRB NTPC 16-01-2021 Evening Shift Questions English

RRB NTPC Memory Based Questions Date-16 January 2021 Evening Shift Q. 1 Who of the following is related "Champaran Satyagraha " ? Ans. Mahatma Gandhi Q. 2 Who was the first "Acting Prime Minister" of India? Ans. Gulzarilal Nanda Gulzarilal Nanda (4 July 1898 – 15 January 1998) was an Indian politician and economist who specialized in labour issues. He was the Acting Prime Minister of India for two short periods following the deaths of Jawaharlal Nehru in 1964 and Lal Bahadur Shastri in 1966. Q. 3 What carries oxygen throughout the human body? Ans. RBC The main job of red blood cells, or erythrocytes, is to carry oxygen from the lungs to the body tissues and carbon dioxide as a waste product, away from the tissues and back to the lungs. Hemoglobin (Hgb) is an important protein in the red blood cells that carries oxygen from the lungs to all parts of our body. Q. 4 Which is the " cleanest city of India" ? Ans. Indore Q. 5 Which gland is known as "Master Gland"? Ans. pituitary gland The pituitary gland is sometimes called the "master" gland of the endocrine system because it controls the functions of many of the other endocrine glands. Q. 6 Which article of Indian Constitution laid down the procedure of Amendment Constitution ? Ans. Article- 368 Q. 7 When was first train started in India? Ans. 1853 by Lord Dalhousie Q. 8 Who was the "Goodwill Ambassador" of UNICEF in 2018? Ans. Priyanka Chopra Q. 9 Which film was not nominated for "Oscar Award"? Ans. Karma www.resultuniraj.co.in Download RRB NTPC PDF http://bit.ly/rrb-ntpc-gk-pdf-download RRB NTPC Memory Based Questions Q. -

Wg2 N3887 Iso/Iec Jtc 1/Sc 2/Wg 2 Proposal Summary Form to Accompany Submissions for Additions to the Repertoire of Iso/Iec 10646 A

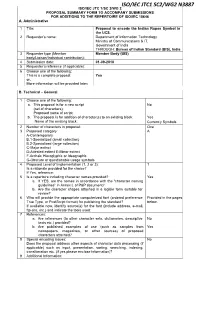

ISO/IEC JTC1 SC2/WG2 N3887 ISO/IEC JTC 1/SC 2/WG 2 PROPOSAL SUMMARY FORM TO ACCOMPANY SUBMISSIONS FOR ADDITIONS TO THE REPERTOIRE OF ISO/IEC 10646 A. Administrative 1 Title: Proposal to encode the Indian Rupee Symbol in the UCS. 2 Requester’s name: Department of Information Technology Ministry of Communications & IT, Government of India THROUGH: Bureau of Indian Standard (BIS), India 3 Requester type (Member Member Body (BIS) body/Liaison/Individual contribution): 4 Submission date: 01-09-2010 5 Requester’s reference (if applicable): 6 Choose one of the following: This is a complete proposal: Yes or, More information will be provided later: B. Technical — General 1 Choose one of the following: a. This proposal is for a new script No (set of characters): Proposed name of script: b. The proposal is for addition of character(s) to an existing block: Yes Name of the existing block: Currency Symbols 2 Number of characters in proposal: One 3 Proposed category: A A-Contemporary B.1-Specialized (small collection) B.2-Specialized (large collection) C-Major extinct D-Attested extinct E-Minor extinct F-Archaic Hieroglyphic or Ideographic G-Obscure or questionable usage symbols 4 Proposed Level of Implementation (1, 2 or 3): 1 Is a rationale provided for the choice? If Yes, reference: 5 Is a repertoire including character names provided? Yes a. If YES, are the names in accordance with the “character naming guidelines” in Annex L of P&P document? b. Are the character shapes attached in a legible form suitable for review? 6 Who will provide the appropriate computerized font (ordered preference: Provided in the pages True Type, or PostScript format) for publishing the standard? below. -

Symbols & Glyphs 1

Symbols & Glyphs Content Shortcut Category ← leftwards-arrow Arrows ↑ upwards-arrow Arrows → rightwards-arrow Arrows ↓ downwards-arrow Arrows ↔ left-right-arrow Arrows ↕ up-down-arrow Arrows ↖ north-west-arrow Arrows ↗ north-east-arrow Arrows ↘ south-east-arrow Arrows ↙ south-west-arrow Arrows ↚ leftwards-arrow-with-stroke Arrows ↛ rightwards-arrow-with-stroke Arrows ↜ leftwards-wave-arrow Arrows ↝ rightwards-wave-arrow Arrows ↞ leftwards-two-headed-arrow Arrows ↟ upwards-two-headed-arrow Arrows ↠ rightwards-two-headed-arrow Arrows ↡ downwards-two-headed-arrow Arrows ↢ leftwards-arrow-with-tail Arrows ↣ rightwards-arrow-with-tail Arrows ↤ leftwards-arrow-from-bar Arrows ↥ upwards-arrow-from-bar Arrows ↦ rightwards-arrow-from-bar Arrows ↧ downwards-arrow-from-bar Arrows ↨ up-down-arrow-with-base Arrows ↩ leftwards-arrow-with-hook Arrows ↪ rightwards-arrow-with-hook Arrows ↫ leftwards-arrow-with-loop Arrows ↬ rightwards-arrow-with-loop Arrows ↭ left-right-wave-arrow Arrows ↮ left-right-arrow-with-stroke Arrows ↯ downwards-zigzag-arrow Arrows 1 ↰ upwards-arrow-with-tip-leftwards Arrows ↱ upwards-arrow-with-tip-rightwards Arrows ↵ downwards-arrow-with-tip-leftwards Arrows ↳ downwards-arrow-with-tip-rightwards Arrows ↴ rightwards-arrow-with-corner-downwards Arrows ↵ downwards-arrow-with-corner-leftwards Arrows anticlockwise-top-semicircle-arrow Arrows clockwise-top-semicircle-arrow Arrows ↸ north-west-arrow-to-long-bar Arrows ↹ leftwards-arrow-to-bar-over-rightwards-arrow-to-bar Arrows ↺ anticlockwise-open-circle-arrow Arrows ↻ clockwise-open-circle-arrow -

Iso/Iec Jtc 1/Sc 2/Wg 2 Proposal Summary Form to Accompany Submissions for Additions to the Repertoire of Iso/Iec 10646 A

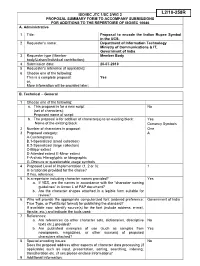

ISO/IEC JTC 1/SC 2/WG 2 PROPOSAL SUMMARY FORM TO ACCOMPANY SUBMISSIONS FOR ADDITIONS TO THE REPERTOIRE OF ISO/IEC 10646 A. Administrative 1 Title: Proposal to encode the Indian Rupee Symbol in the UCS. 2 Requester's name: Department of Information Technology Ministry of Communications & IT, Government of India 3 Requester type (Member Member Body body/Liaison/Individual contribution): 4 Submission date: 20-07-2010 5 Requester's reference (if applicable): 6 Choose one of the following: This is a complete proposal: Yes or, More information will be provided later: B. Technical – General 1 Choose one of the following: a. This proposal is for a new script No (set of characters): Proposed name of script: b. The proposal is for addition of character(s) to an existing block: Yes Name of the existing block: Currency Symbols 2 Number of characters in proposal: One 3 Proposed category: A A-Contemporary B.1-Specialized (small collection) B.2-Specialized (large collection) C-Major extinct D-Attested extinct E-Minor extinct F-Archaic Hieroglyphic or Ideographic G-Obscure or questionable usage symbols 4 Proposed Level of Implementation (1, 2 or 3): 1 Is a rationale provided for the choice? If Yes, reference: 5 Is a repertoire including character names provided? Yes a. If YES, are the names in accordance with the “character naming guidelines” in Annex L of P&P document? b. Are the character shapes attached in a legible form suitable for review? 6 Who will provide the appropriate computerized font (ordered preference: Government of India True Type, or PostScript format) for publishing the standard? If available now, identify source(s) for the font (include address, e-mail, ftp-site, etc.) and indicate the tools used: 7 References: a. -

IIT Graduate Gives Indian Rupee Its Symbol

IIT graduate gives Indian Rupee its symbol Press Trust of India, Updated: July 16, 2010 00:05 IST Comments Ads by Google HDFCERGO Health Insurance – Now Claim Process with minimum documents. Apply Online Today! HDFCERGO.com/Health_Insurance Click to Expand & Play New Delhi: The Indian rupee will soon have a unique symbol -- a blend of the Devanagri 'Ra' and Roman 'R' -- joining elite currencies like the US dollar, euro, British pound and Japanese yen in having a distinct identity. The new symbol, designed by Bombay IIT post-graduate D Udaya Kumar, was approved by the cabinet today -- reflecting that the Indian currency, backed by an over-trillion dollar economy, was finally making its presence felt on the international scene. (How do you like the symbol?) "It's a big statement on the Indian currency... The symbol would lend a distinctive character and identity to the currency and further highlight the strength and global face of the Indian economy," Information and Broadcasting Minister Ambika Soni told reporters after the cabinet meeting. Though the symbol will not be printed or embossed on currency notes or coins, it would be included in the 'Unicode Standard' and major scripts of the world to ensure that it is easily displayed and printed in the electronic and print media. Among currencies with distinctive identities, only the pound sterling has its symbol printed on the notes. Unicode is an international standard that allows text data to be interchanged globally without conflict. After incorporation in the global and Indian codes, the symbol would be used by all individuals and entities within and outside the country. -

A Request Letter to ISO/IEC Registration Authority Asking To

ISO/IEC JTC1/SC2/WG2 N3868 1324 S Winchester BL Unit 177 San Jose, California 95128 July 15, 2010 E-mail: [email protected] To: ISO Central Secretariat 1, ch. de la Voie-Creuse Case postale 56 CH-1211 Geneva 20 Switzerland Tel. + 41 22 749 01 11 Fax + 41 22 733 34 30 E-mail [email protected] Copy: (a) Shri N. Ravi Shanker, Joint Secretary (b) Director & HoD TDIL Programme, IT Department, Government of India (c) Aadarsha Ratne script users group - [email protected] (d) Nagair - Общество ревнителей санскрита (Sanscrit) – [email protected] Re: India’s National Currency Symbol Dear Madam/Sir: I propose to encode India’s national currency symbol to ISO/IEC and enclose herewith Proposal Summary Form [1], as you know that Government of India (GOI) has recently approved a new currency symbol - see [2] [3]. This new symbol may be named: XXX0 INDIAN RUPEE SIGN ( ň ) I would be highly obliged should you kindly consider my request to include this precious symbol to ISO and IEC and or as applicable. List of enclosures: [1] ISO/IEC JTC 1/SC 2/WG 2 PROPOSAL SUMMARY FORM [2] Heather Timmons, “India Adopts a New Symbol for Its Currency”, the New York Times, July 15, 2010. http://www.nytimes.com/2010/07/16/business/global/16rupee.html?_r=1&src=busln&pagewanted=print [3] “Indian government approves new symbol for rupee”, BBC News, 15 July 2010. http://www.bbc.co.uk/news/world-south+asia-10644730 Thank you for your times, and I look forward to hearing from you. -

Latest Developments in Unicode and CLDR

Software for the world: latest developments in Unicode and CLDR Mark Davis President & Co-founder Unicode Consortium Unicode Consortium All modern software: OSs, smartphones, XML,… Core Globalization Standards – and Data Encoding (the Unicode Standard) IDNA Compatibility Locales (CLDR/LDML) Collation (Sorting/Matching) Regular Expressions Security ... http://www.unicode.org/faq/specifications.html Unicode > 50% 50% 6B web pages 0% 2001 2011 Caveats: Different Regions Sample Selection CN JP XXB Unicode 6.0 Unicode Character Database: 109K characters and their properties 2,088 new characters 1000+ symbols 20B9 International Domain Names (IDN) Allow Unicode chars in domain names <a href="http://ÖBB.at"> Supported by all browsers, search engines,... Established in 2003 2010 Key Events for IDNs May Top level IDNs - ICANN internationalized entire domain names http://президент.рф August IDNA2008 - IETF UTS #46, Unicode IDNA Compatibility Processing Problems Deploying IDNA2008 Browser vendors Need to read IDNA2003 pages Need to match expectations OBB = obb but ÖBB ≠ öbb?? Search engine vendors Need to match old and new browsers Recent issue: STD3 (ASCII _,...) UTS46: IDN Mapping + Transition Mapping Principles = IDNA2003 Extends to Unicode Version X Case + Compatibility Repertoire Principles = IDNA2008 + IDNA2003 Implementation can restrict, eg to IDNA2008 Transition Period before strict IDNA2008 Defined by Data Tables Always Backwards Compatible Updated and extended for each Unicode Version Unicode Locales: CLDR Dates/time formats Number/currency -

Currency Symbols Range: 20A0–20CF

Currency Symbols Range: 20A0–20CF This file contains an excerpt from the character code tables and list of character names for The Unicode Standard, Version 14.0 This file may be changed at any time without notice to reflect errata or other updates to the Unicode Standard. See https://www.unicode.org/errata/ for an up-to-date list of errata. See https://www.unicode.org/charts/ for access to a complete list of the latest character code charts. See https://www.unicode.org/charts/PDF/Unicode-14.0/ for charts showing only the characters added in Unicode 14.0. See https://www.unicode.org/Public/14.0.0/charts/ for a complete archived file of character code charts for Unicode 14.0. Disclaimer These charts are provided as the online reference to the character contents of the Unicode Standard, Version 14.0 but do not provide all the information needed to fully support individual scripts using the Unicode Standard. For a complete understanding of the use of the characters contained in this file, please consult the appropriate sections of The Unicode Standard, Version 14.0, online at https://www.unicode.org/versions/Unicode14.0.0/, as well as Unicode Standard Annexes #9, #11, #14, #15, #24, #29, #31, #34, #38, #41, #42, #44, #45, and #50, the other Unicode Technical Reports and Standards, and the Unicode Character Database, which are available online. See https://www.unicode.org/ucd/ and https://www.unicode.org/reports/ A thorough understanding of the information contained in these additional sources is required for a successful implementation. -

Banking Awareness Question Bank 10

Bank Of India Exam Previous Paper 1. Banking OmbudsmanBanking is appointed Awareness by Question Bank a) SEBI b) NABARD c) RBI d) None of these 2. Name of Union Territory which as recently presented a tax free budge of Rs.6100 Crore for the union territory: a) Chandigarh b) Puducherry c) Dadra Nagar Haweli d) None of these 3. Maximum age for retirement for MD/CEO of all private banks is a) 60 years b) 65 years c) 70 years d) None of these 4. Two new Savings Bank products for children namely ‘PehlaKadam and PehliUdaan’ introduced by a) State Bank of India b) United Bank of India c) Axis Bank d) None of these 5. 'Financial Exclusion' is: a) Exclude the Finance b) Lack of Access to Financial Services c) Instability of Financial Services d) None of these 6. Vijay Mallya as 'Willful Defaulter' is declared by: a) United Bank of India b) Canara Bank c) Dena Bank d) None of these 7. Mutual Funds are regulated by: a) Reserve Bank of India b) Securities and Exchange Board of India c) Mutual Funds Board of India d) None of these 8. To solve the problems of Balance of Payments of membercountries is function of: a) World Bank b) IMF c) GATT d) None of these 9. Which term is not associated with banking operations: a) Equator b) Prime Lending Rate c) Corporate Finance d) None of these www,BankExamsToday.com Page 1 Banking Awareness Question Bank 10. U.T.I. officially changed into: a) Vijaya Bank b) Dena Bank c) Axis Bank d) None of these 11. -

4386-A Foreword

Draft Amendment (DAM) 2 ISO/IEC 10646:2012/Amd.2:2013 (E)/WG2 N4386-A Foreword ISO (the International Organization for Standardization) and IEC (the International Electrotechnical Com- mission) form the specialized system for worldwide standardization. National bodies that are members of ISO or IEC participate in the development of International Standards through technical committees estab- lished by the respective organization to deal with particular fields of technical activity. ISO and IEC tech- nical committees collaborate in fields of mutual interest. Other international organizations, governmental and non-governmental, in liaison with ISO and IEC, also take part in the work. In the field of information technology, ISO and IEC have established a joint technical committee, ISO/IEC JTC1. International Standards are drafted in accordance with the rules given in the ISO/IEC Directives, Part 2. The main task of the joint technical committee is to prepare International Standards. Draft International Standards adopted by the joint technical committee are circulated to national bodies for voting. Publication as an International Standard requires approval by at least 75% of the national bodies casting a vote. Attention is drawn to the possibility that some of the elements of ISO/IEC 10646 may be the subject of patent rights. ISO and IEC shall not be held responsible for identifying any or all such patent rights. This International Standard was prepared by Joint Technical Committee ISO/IEC JTC1, Information tech- nology, Subcommittee SC 2, Coded Character sets. Amendment 2 to ISO/IEC 10646:2012 was prepared by Joint Technical Committee ISO/IEC JTC1, Infor- mation technology, Subcommittee SC 2, Coded character sets.