Memory: Are Challenges Ahead?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ED-7311-20.Pdf

EIAJ ED-7311-20 - 1 - EIAJ ED-7311-20 - 2 - EIAJ ED-7311-20 - 3 - EIAJ ED-7311-20 - 4 - EIAJ ED-7311-20 - 5 - EIAJ ED-7311-20 - 6 - EIAJ ED-7311-20 - 7 - EIAJ ED-7311-20 - 8 - EIAJ ED-7311-20 - 9 - EIAJ ED-7311-20 - 10 - EIAJ ED-7311-20 - 11 - EIAJ ED-7311-20 - 12 - EIAJ ED-7311-20 - 13 - EIAJ ED-7311-20 - 14 - EIAJ ED-7311-20 - 15 - EIAJ ED-7311-20 - 16 - EIAJ ED-7311-20 - 17 - EIAJ ED-7311-20 - 18 - EIAJ ED-7311-20 - 19 - EIAJ ED-7311-20 - 20 - EIAJ ED-7311-20 - 21 - EIAJ ED-7311-20 - 22 - EIAJ ED-7311-20 - 23 - EIAJ ED-7311-20 - 24 - EIAJ ED-7311-20 - 25 - EIAJ ED-7311-20 - 26 - EIAJ ED-7311-20 - 27 - EIAJ ED-7311-20 - 28 - EIAJ ED-7311-20 - 29 - EIAJ ED-7311-20 - 30 - EIAJ ED-7311-20 - 31 - EIAJ ED-7311-20 - 32 - EIAJ ED-7311-20 - 33 - EIAJ ED-7311-20 - 34 - EIAJ ED-7311-20 - 35 - EIAJ ED-7311-20 - 36 - EIAJ ED-7311-20 - 37 - EIAJ ED-7311-20 - 38 - EIAJ ED-7311-20 - 39 - EIAJ ED-7311-20 - 40 - EIAJ ED-7311-20 - 41 - EIAJ ED-7311-20 - 42 - EIAJ ED-7311-20 - 43 - EIAJ ED-7311-20 - 44 - EIAJ ED-7311-20 - 45 - EIAJ ED-7311-20 - 46 - EIAJ ED-7311-20 - 47 - EIAJ ED-7311-20 - 48 - EIAJ ED-7311-20 - 49 - EIAJ ED-7311-20 - 50 - EIAJ ED-7311-20 - 51 - EIAJ ED-7311-20 - 52 - EIAJ ED-7311-20 - 53 - EIAJ ED-7311-20 - 54 - EIAJ ED-7311-20 - 55 - EIAJ ED-7311-20 - 56 - EIAJ ED-7311-20 - 57 - EIAJ ED-7311-20 - 58 - EIAJ ED-7311-20 - 59 - EIAJ ED-7311-20 - 60 - EIAJ ED-7311-20 - 61 - EIAJ ED-7311-20 - 62 - EIAJ ED-7311-20 - 63 - EIAJ ED-7311-20 - 64 - EIAJ ED-7311-20 - 65 - EIAJ ED-7311-20 - 66 - EIAJ ED-7311-20 - 67 - EIAJ ED-7311-20 - 68 - EIAJ -

FY2008 Results Meeting

FY200FY20088 ResultsResults MeetingMeeting FY2008 : Year ended March 31, 2009 May 14, 2009 Ryosan Company, Limited Code : 8140 / Stock listings: Tokyo Stock Exchange (First Section) URL : http://www.ryosan.co.jp/eng/ Notice This presentation contains forward-looking statements regarding business performance, which may differ substantially from actual results, depending on certain risks and uncertainties, the most significant of which are listed below. z Economic conditions in key markets (Japan and the rest of Asia), rapid changes in consumption patterns and supply-demand balance for products z Sharp fluctuations in the ¥/$ exchange rate z Substantial fluctuation in prices in capital markets Consolidated results for FY 2008 FY2007 FY2008 FY2009(Forecasts) Of Total Of Total % Chg. YoY Of Total % Chg. YoY ¥ 100 million% ¥ 100 million%% ¥ 100 million %% Net sales 2,860 2,208 (22.8) 1,700 (23.0) Gross margin 251 8.8 196 8.9 (22.1) 149 8.8 (24.1) SG&A expenses 144 5.0 134 6.1 (6.8) 115 6.8 (14.7) Operating income 107 3.8 61 2.8 (42.8) 34 2.0 (44.7) Ordinary income 112 3.9 72 3.3 (35.6) 38 2.2 (47.7) Net income 67 2.4 39 1.8 (41.8) 22 1.3 (43.9) Earnings per share ¥187.15 ¥111.83 (¥75) ¥63.83 (¥48) 1 Segment results for FY2008 Unit : ¥ 100 million FY2007 FY2008 FY2009(Forecasts) OP OP OP Margin Margin % Chg. YoYMargin % Chg. YoY % % Sales 1,489 1,169 (21.5) 808 (30.9) Semiconductors Operating income 724.9% 48 4.2%(32.7) 28 3.5% (42.7) Electronic Sales 1,031 759 (26.4) 584 (23.1) Components Operating income 444.3 28 3.7 (35.9) 22 3.8 (22.1) -

Semiconductor Times, April 2020

SEMICONDUCTOR TIMES APR 2020 / 1 ® APR 2020 FOCUSED ON EMERGING SEMICONDUCTOR COMPANIES VOL 25, ISSUE 4 bandwidth in the automotive market. Christopher Mash, VP of Business De- Startup Profiles Next generation cars require multiple velopment (previously Senior Dir. layers of security protection to prevent, Automotive Apps, Product Definition Axonne detect, and adapt to evolving threats. The and Architecture at Marvell) Axonne was founded in early 2018 auto industry is increasingly adopting Craig Farnsworth, GM and Senior Dir. to develop connectivity solutions for Ethernet solutions and 2019 will see the of Engineering (previously Senior automotive and industrial applications. international standardization (IEEE) of Director of Digital Design at Peraso) The company has received funding multi-gigabit Ethernet bandwidth rates Ahmad Tavakoli, Sr. Director, Analog from Translink Capital. We believe for automotive applications. & Mixed-Signal Design (previously the company is developing automotive Sr. Hardware Engineer at Google and ethernet ICs. Ethernovia is developing an Ethernet Verily Life Sciences, and Sr. Director system sophisticated enough to process of Engineering at Aquantia) Gani Jusuf, Ph.D., Co-Founder and the bandwidth demands of future auto- 2050 Ringwood Ave Suite B CEO (previously VP of engineering motive systems by unifying in-vehicle San Jose, CA 95131 at Marvell) networks into an end to end Ethernet www.ethernovia.com William Lo, Co-Founder and CTO system. Ethernovia is developing an (previously VP, R&D Datacom En- Ethernet solution that will provide a gineering at Marvell) unified, standards-based solution built ONiO Sunnyvale, CA to meet automotive functional safety ONiO was founded in 2016 to develop www.axonne.com requirements. -

Stoxx® Global 3000 Technology Index

SUPERSECTOR INDICES 1 STOXX® GLOBAL 3000 TECHNOLOGY INDEX Stated objective Key facts The STOXX Supersector indices track supersectors of the relevant » Categorization according to their primary source of revenue benchmark index. There are 19 supersectors according to the guarantees an accurate classification of companies in their respective Industry Classification Benchmark (ICB). Companies are categorized business environments according to their primary source of revenue. The following supersectors are available: automobile and parts, banks, basic » Component capping ensures that no component can dominate the resources, chemicals, construction and materials, financial services, index food and beverage, health care, industrial goods and services, insurance, media, oil and gas, personal and household goods, real estate, communications, retail, technology, travel and leisure and utilities. Descriptive statistics Index Market cap (USD bn.) Components (USD bn.) Component weight (%) Turnover (%) Full Free-float Mean Median Largest Smallest Largest Smallest Last 12 months STOXX Global 3000 Technology Index 4,573.6 4,143.5 19.6 5.4 618.0 1.2 14.9 0.0 4.1 STOXX Global 3000 Index 48,487.0 40,843.1 13.6 5.1 618.0 1.2 1.5 0.0 3.4 Supersector weighting (top 10) Country weighting Risk and return figures1 Index returns Return (%) Annualized return (%) Last month YTD 1Y 3Y 5Y Last month YTD 1Y 3Y 5Y STOXX Global 3000 Technology Index 3.8 15.3 33.8 56.5 87.5 55.8 23.3 33.0 15.7 13.1 STOXX Global 3000 Index 2.3 7.5 21.7 51.5 87.5 31.3 11.2 21.2 14.5 13.1 -

1332:Xtks Nippon Suisan Kaisha Ltd 3 4 1 1334:Xtks Maruha Nichiro Holdings Inc. 3 4 1 1377:Xtks Sakata Seed Corp. 3 5 2 1414:Xtks SHO-BOND Holdings Co

Symbol Code Description Current Rating New rating Diff 1332:xtks Nippon Suisan Kaisha Ltd 3 4 1 1334:xtks Maruha Nichiro Holdings Inc. 3 4 1 1377:xtks Sakata Seed Corp. 3 5 2 1414:xtks SHO-BOND Holdings Co. Ltd 3 6 3 1766:xtks TOKEN Corp. 3 6 3 1801:xtks Taisei Corp. 3 5 2 1803:xtks Shimizu Corp. 3 4 1 1808:xtks Haseko Corp. 3 4 1 1812:xtks Kajima Corp. 3 5 2 1820:xtks Nishimatsu Construction Co. Ltd 3 6 3 1824:xtks Maeda Corp. 3 6 3 1833:xtks Okumura Corp. 3 6 3 1860:xtks Toda Corp. 3 5 2 1861:xtks Kumagai Gumi Co. Ltd 3 8 5 1865:xtks Asunaro Aoki Construction Co. Ltd 3 6 3 1870:xtks Yahagi Construction Co. Ltd 3 4 1 1881:xtks NIPPO Corp. 3 6 3 1883:xtks Maeda Road Construction Co. Ltd 3 6 3 1911:xtks Sumitomo Forestry Co Ltd 3 4 1 1924:xtks PanaHome Corp. 3 4 1 1925:xtks Daiwa House Industry Co. Ltd 3 4 1 1928:xtks Sekisui House Ltd 3 4 1 1934:xtks YURTEC Corp. 3 6 3 1945:xtks Tokyo Energy & Systems Inc. 3 4 1 1961:xtks Sanki Engineering Co. Ltd 3 4 1 1963:xtks JGC Corporation 3 4 1 1968:xtks Taihei Dengyo Kaisha Ltd 3 4 1 1969:xtks Takasago Thermal Engineering Co. Ltd 3 4 1 1973:xtks NEC Networks & System Integration Corp. 3 5 2 1979:xtks Taikisha Ltd 3 4 1 1983:xtks TOSHIBA PLANT SYSTEMS & SERVICES Corp. -

UNO Template

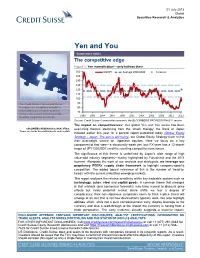

01 July 2013 Global Securities Research & Analytics Yen and You Connections Series The competitive edge Figure 1: Yen 'normalisation'—only halfway there 160 USDJPY Average 1990-2008 Forecast 150 140 130 120 110 100 The Credit Suisse Connections Series 90 leverages our exceptional breadth of 80 macro and micro research to deliver 70 incisive cross-sector and cross-border 1990 1992 1994 1997 1999 2001 2004 2006 2008 2011 2013 thematic insights for our clients. Source: Credit Suisse Commodities research, the BLOOMBERG PROFESSIONAL™ service The impact on competitiveness: Our global Yen and You series has been SECURITIES RESEARCH & ANALYTICS examining themes stemming from the 'shock therapy' the Bank of Japan Please see inside for contributors to each section initiated earlier this year. In a parallel report published today (Global Equity Strategy - Japan: The sun is still rising), our Global Equity Strategy team revisit their overweight stance on Japanese equities. Here we focus on a key component of that view—a structurally weak yen (our FX team has a 12-month target of JPY120/USD1) and the resulting competitiveness issues. The significance of this theme is underlined by Japan's wide range of high value-add industry segments—starkly highlighted by Fukushima and the 2011 tsunami. Alongside the work of our analysts and strategists, we leverage our proprietary PEERs supply chain framework to highlight company-specific competition. The added topical relevance of this is the number of 'head-to- heads' with the current embattled emerging markets. This report analyses the relative sensitivity within key tradeable sectors such as technology, autos, steel and capital goods. -

Division of Investment Department of the Treasury State of New Jersey Pension Fund June 30, 2009 and 2008 (With Independent Auditors’ Report Thereon)

F INANCIAL S TATEMENTS, M ANAGEMENT’ S D ISCUSSION AND A NALYSIS AND S UPPLEMENTAL S CHEDULES Division of Investment Department of the Treasury State of New Jersey Pension Fund June 30, 2009 and 2008 (With Independent Auditors’ Report Thereon) Division of Investment Department of the Treasury State of New Jersey Pension Fund Financial Statements June 30, 2009 and 2008 Contents Independent Auditors’ Report ..........................................................................................................1 Management’s Discussion and Analysis .........................................................................................3 Basic Financial Statements: Statements of Net Assets .................................................................................................................7 Statements of Changes in Net Assets...............................................................................................8 Notes to Financial Statements ..........................................................................................................9 Supplemental Schedules: Schedule 1 – Combining Schedule of Net Assets ..........................................................................31 Schedule 2 – Combining Schedule of Changes in Net Assets .......................................................32 Schedule 3 – Portfolio of Investments – Common Fund A ...........................................................33 Schedule 4 – Portfolio of Investments – Common Fund B ...........................................................57 -

Delaware, 1:11-Cv-00770

IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF DELAWARE HSM PORTFOLIO LLC AND § TECHNOLOGY PROPERTIES § LIMITED LLC, § § Plaintiffs, § § v. § C.A. No. 1:11-cv-00770-RGA § FUJITSU LIMITED, § JURY TRIAL DEMANDED FUJITSU AMERICA, INC., § FUJITSU SEMICONDUCTOR § AMERICA, INC., § § ADVANCED MICRO DEVICES, INC., § § QUALCOMM INCORPORATED, § § ELPIDA MEMORY, INC., § ELPIDA MEMORY (USA) INC., § § SK HYNIX INC., § SK HYNIX AMERICA INC., § HYNIX SEMICONDUCTOR § MANUFACTURING AMERICA INC., § § MICRON TECHNOLOGY, INC., § § PROMOS TECHNOLOGIES INC., § § SANDISK CORPORATION, § § SONY CORPORATION, § SONY CORPORATION OF AMERICA, § SONY ELECTRONICS INC., § SONY COMPUTER § ENTERTAINMENT INC., § SONY COMPUTER § ENTERTAINMENT AMERICA LLC, § § STMICROELECTRONICS N.V., § STMICROELECTRONICS, INC., § § PAGE 1 TOSHIBA CORPORATION, § TOSHIBA AMERICA, INC., § TOSHIBA AMERICA ELECTRONIC § COMPONENTS, INC., § § ON SEMICONDUCTOR § CORPORATION, § § ZORAN CORPORATION, § § Defendants. § PLAINTIFFS’ THIRD AMENDED COMPLAINT Plaintiffs HSM Portfolio LLC and Technology Properties Limited LLC (collectively “Plaintiffs”) by and through their undersigned counsel, file this Third Amended Complaint against Defendants Fujitsu Limited, Fujitsu America, Inc., Fujitsu Semiconductor America, Inc. (collectively “Fujitsu”), Advanced Micro Devices, Inc. (“AMD”), Qualcomm Incorporated (“Qualcomm”), Elpida Memory, Inc., Elpida Memory (USA) Inc. (collectively “Elpida”),1 SK Hynix Inc., SK Hynix America Inc., Hynix Semiconductor Manufacturing America Inc. (collectively “SK Hynix”), -

SK Hynix to Acquire Intel NAND Memory Business

SK hynix to Acquire Intel NAND Memory Business NEWS HIGHLIGHTS SK hynix will pay US $9 billion for the Intel NAND memory and storage business, which includes the NAND SSD business, the NAND component and wafer business, and the Dalian NAND memory manufacturing facility in China. SK hynix aims to enhance the competitiveness of its NAND flash solutions as one of the leading global semiconductor companies and grow the memory ecosystem to the benefit of customers, partners, employees and shareholders. Intel will retain its Intel® Optane™ business and intends to invest transaction proceeds in long-term growth priorities. SEOUL, Republic of Korea and SANTA CLARA, Calif., Oct. 20, 2020 -- SK hynix and Intel today announced that they have signed an agreement on Oct. 20, KST, under which SK hynix would acquire Intel’s NAND memory and storage business for US $9 billion. The transaction includes the NAND SSD business, the NAND component and wafer business, and the Dalian NAND memory manufacturing facility in China. Intel will retain its distinct Intel® OptaneTM business. SK hynix and Intel will endeavor to obtain required governmental approvals expected in late 2021. Following receipt of these approvals, SK hynix will acquire from Intel the NAND SSD business (including NAND SSD-associated IP and employees), as well as the Dalian facility, with the first payment of US $7 billion. SK hynix will acquire from Intel the remaining assets, including IP related to the manufacture and design of NAND flash wafers, R&D employees, and the Dalian fab workforce, upon a final closing, expected to occur in March 2025 with the remaining payment of US $2 billion. -

2008 International Symposium on Semiconductor Manufacturing

2008 International Symposium on Semiconductor Manufacturing (ISSM 2008) Tokyo, Japan 27 – 29 October 2008 IEEE Catalog Number: CFP08SSM-PRT ISBN: 978-1-61284-948-5 ISSM 2008 Program Schedule The 1st day (Monday, October 27) Tutorial Session Room: Century A/B 9:30 Tutorial Session AEC/APC Introduction of AEC/APC's history Mr. Toshihiko Osada, Senior Manager, Fujitsu Microelectronics Limited Manufacturing engineering and AEC/APC Mr. Kensuke Uriga, CEO/President, Dura Systems Corporation Application of control theory for AEC/APC in semiconductor fabrication Mr. Hiroshi Shimizu, Director/Advanced Solution Department, Advance Automation Company, Yamatake Corporation 9:00 Tutorial Session ESH SUSTAINABILITY AND ESH ASPECTS OF ADVANCED SEMICONDUCTOR MANUFACTURING Prof. Farhang Shadman, Regents Professor of Chemical and Environmental Engineering, the University of Arizona Opening Remarks Room: Century 13:00 Keynote Speech Session Room: Century 13:20 Challenges in The DRAM Business Mr.Yukio Sakamoto, President&CEO, Elpida Memory,Inc. 14:10 The New Dynamics of Semiconductor Industry Dr. Tien Wu, Chief Operating Officer, Board of Directors, Advanced Semiconductor Engineering Inc.(ASE) 15:00 Break Oral Session Room: Century A Highlight Session <Advanced Lithography Session> 15:10 PE-O-097 Phenomenology of ArF Photoresist Shrinkage Trends ..........................................................3 Benjamin Bunday, ISMI 15:30 PE-O-044 Lithography Hotspot Discovery at 70nm DRAM 300mm Fab : Process Window Qualification Using Design Based Binning...............................................................................7 -

Comparison of Leading Edge 3D NAND Memories TOSHIBA-Sandisk /SAMSUNG/SK HYNIX/INTEL- MICRON Memory Report by Belinda Dube December 2018

REVERSE COSTING® – STRUCTURAL, PROCESS & COST REPORT 3D NAND FLASH MEMORIES Comparison of Leading Edge 3D NAND Memories TOSHIBA-SanDisk /SAMSUNG/SK HYNIX/INTEL- MICRON Memory report by Belinda Dube December 2018 22 Bd. Benoni Goullin 44200 NANTES - FRANCE +33 2 40 18 09 16 [email protected] www.systemplus.fr Table of Contents Overview / Introduction 4 o SK Hynix 80 o Executive Summary Synthesis o Reverse Costing Methodology Die design Company Profile 8 Cross-Section o Toshiba/SanDisk Patents o Samsung o SK Hynix o Intel/ Micron 110 o Micron/Intel Synthesis Die design Cross-Section Technology & Market 8 o NAND Roadmap Patents o NAND Revenue Manufacturing Process Flow 146 o Global Overview Physical Analysis 14 o Wafer Fabrication Unit o Toshiba Synthesis of the Physical Analysis o Front-End Process o Toshiba Physical Analysis Methodology o Toshiba Physical analysis Cost Analysis 179 Die o Synthesis of the cost analysis Cross-Section Yields Explanation & Hypotheses o Toshiba Patents NAND wafer and die cost o Samsung Synthesis of the Physical Analysis 53 Front-End Cost o Samsung Physical Analysis Methodology Component Cost o Samsung Physical analysis Die Estimated Price and Manufacturer Gross Margin 228 Cross-Section Company services 239 o Samsung Patents Executive Summary Overview / Introduction o Executive Summary The memory semiconductor industry continues to grow due to higher memory demand in consumer electronics and o Reverse Costing Methodology mass storage. Remarkable investments are channeled into the memory manufacturing business. IoT escalates this o Glossary demand and hence manufacturers continue to increase the die density of memories at the same time aiming on Company Profile reduction of the NAND die. -

Case 1:14-Cv-01432-LPS-CJB Document 13 Filed 03/27/15 Page 1 of 57 Pageid #: 219

Case 1:14-cv-01432-LPS-CJB Document 13 Filed 03/27/15 Page 1 of 57 PageID #: 219 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF DELAWARE ELM 3DS INNOVATIONS, LLC, a ) Delaware limited liability company, ) ) Plaintiff, ) ) C.A. No. 1:14-cv-01432-LPS-CJB v. ) ) SK HYNIX INC., a Korean corporation, ) Jury Trial Demanded SK HYNIX AMERICA INC., a California ) corporation, ) HYNIX SEMICONDUCTOR ) MANUFACTURING AMERICA INC., a California corporation, and ) SK HYNIX MEMORY SOLUTIONS ) INC., a Delaware corporation, ) ) ) Defendants. FIRST AMENDED COMPLAINT FOR PATENT INFRINGEMENT Plaintiff Elm 3DS Innovations, LLC (“Plaintiff” or “Elm 3DS”), by its attorneys, for its complaint against Defendants SK hynix Inc., and its U.S. subsidiaries and related entities SK hynix America Inc., Hynix Semiconductor Manufacturing America Inc., and SK hynix Memory Solutions Inc. (individually or collectively “Defendants” or “Hynix”) hereby alleges as follows: INTRODUCTION 1. This is an action for patent infringement under the Patent Laws of the United States, 35 U.S.C. § 1 et seq., for infringing the following Elm 3DS patents: 1 Case 1:14-cv-01432-LPS-CJB Document 13 Filed 03/27/15 Page 2 of 57 PageID #: 220 (a) U.S. Patent No. 7,193,239 (“Leedy ’239 patent”), entitled “Three Dimensional Structure Integrated Circuit,” owned by Elm 3DS Innovations, LLC (attached as Exhibit 1); (b) U.S. Patent No. 7,474,004 (“Leedy ‘004 patent”), entitled “Three Dimensional Structure Memory,” owned by Elm 3DS Innovations, LLC (attached as Exhibit 2); (c) U.S. Patent No. 7,504,732 (“Leedy ‘732 patent”), entitled “Three Dimensional Structure Memory,” owned by Elm 3DS Innovations, LLC (attached as Exhibit 3); (d) U.S.