How to Use the Fehmarnbelt Fixed Link As Impulse for Regional Growth”

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

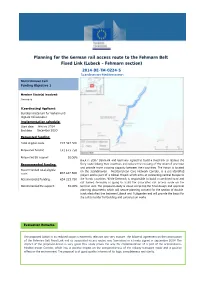

Planning for the German Rail Access Route to the Fehmarn Belt Fixed Link

Planning for the German rail access route to the Fehmarn Belt Fixed Link (Lubeck - Fehmarn section) 2014-DE-TM-0224-S Scandinavian-Mediterranean Multi-Annual Call Funding Objective 1 Member State(s) involved: Germany C:\Temp\fichemaps\20150630AfterCorrs\2014-DE-TM-022 (Coordinating) Applicant: Bundesministerium fur Verkehr und digitale Infrastruktur Implementation schedule: Image found and displayed. Start date: January 2014 End date: December 2020 Requested funding: Total eligible costs: €83 347 500 Requested funding: €41 673 750 Requested EU support: 50.00% Back in 2007 Denmark and Germany agreed to build a fixed link to replace the Recommended funding: ferry route linking their countries and reduce the crossing of the strait of one hour and provide more crossing capacity between their countries. The Action is located Recommended total eligible on the Scandinavian - Mediterranean Core Network Corridor, is a pre-identified €68 447 500 costs: project and is part of a Global Project which aims at connecting central Europe to Recommended funding: €34 223 750 the Nordic countries. While Denmark is responsible to build a combined road and rail tunnel, Germany is going to build the associated rail access route on the Recommended EU support: 50.00% German side. The proposed study is about compiling the final design and approval planning documents which will secure planning consent for the section of double- track electrified line between Lübeck and Puttgarden and will provide the basis for the call to tender for building and construction works. Evaluation Remarks The proposed Action in its reduced scope is extremely relevant and very mature. The bilateral agreement on the construction of the Fehmarn Belt Fixed Link and its associated access routes was formalised in a treaty signed in September 2008. -

Om R Å Def Or Nyelsenyk Øb Ingmidtby

BUDGET OMRÅDEFORNYELSE MIDTBY NYKØBING ARKITEKTER:JJW REDEGØRELSE 2020 1 INDHOLDSFORTEGNELSE INDLEDNING ............................................................... 5 BUDGETFORUDSÆTNINGER ........................................ 12 BUDGETAFTALE .......................................................... 14 RESULTATOVERSIGT ................................................... 19 FINANSIERINGSOVERSIGT .......................................... 20 BEVILLINGSOVERSIGT ................................................ 20 OVERSIGT OVER ANLÆGSINVESTERINGER .................. 21 ØKONOMIUDVALG .................................................... 24 Mål & Indikatorer ......................................................... 24 Politikområde: Finans ................................................... 28 Politikområde: Politik og erhverv ................................... 29 Politikområde: Administration ....................................... 32 SOCIAL, SUNDHED OG OMSORGSUDVALG ............... 35 Udvalgsstrategi ............................................................ 36 Politikområde: Omsorg ................................................. 41 Politikområde: Folkesundhed ......................................... 49 Politikområde: Socialområdet ........................................ 53 Politikområde: SSO - Administration ............................... 60 BØRN, FAMILIE OG UDDANNELSESUDVALG ............ 62 Udvalgsstrategi ............................................................ 63 Politikområde: Familierådgivning ................................... -

Dæmningen Medlemsblad for Toreby Sejlklub Nr

Dæmningen Medlemsblad for Toreby Sejlklub Nr. 2, juli 2019 - 39. årgang TEMA: Truende skyer over fritidssejlerne i Nykøbing Optrækkende uvejr over Femø Havn. Foto: Palle Tørnqvist Toreby Sejlklub Dæmningen 2, Sundby L 4800 Nykøbing F. Tlf. 54 85 78 01 Formanden har ordet [email protected] www.toreby-sejlklub.dk Bestyrelse Havne- og pæleudvalg å grund af påsken havde vi i år den fælles søsætning I pinsen havde vi den traditionelle fællestur, der igen år en uge senere end sædvanlig. Påskelørdag den 20. gik til Maltrup Vænge. Sakskøbing Bådelaug og Sejlklub Formand: Jan Krastrup, Formand: Jan Krastrup. Tlf. 23 30 88 86. P Humlevænget 1, april indledte vi officielt sæsonen med den traditionelle tog godt imod os, og de gjort alt for, at vi kunne have Sundby L. Næstformand: Tonny Cranø. Tlf. 40 10 94 84. standerhejsning. nogle fantastiske dage i deres klub. Festudvalget havde 4800 Nykøbing F. Karsten Pagh. Tlf. 22 28 74 03. Vejret i hele april måned var mildt og temperaturen var en overraskelse i ærmet, idet de havde hyret et fem Tlf. 23 30 88 86. Henrik Lundvaldt. Tlf. 20 14 26 01. Flemming Hermund. Tlf. 20 91 75 13. tilstrækkelig høj til, at vi alle havde god tid og gode be- mands orkester til at underholde os om aftenen pin- Næstformand: Hans Lund, tingelser for at få klargjort vores både, så de var klar til selørdag. Mokka Band hed orkesteret, og de spillede Bøgevej 10, Systofte Skovby. Pladsudvalg den fælles søsætning i weekenden den 27. og 28. april. populær musik, der fik alle på dansegulvet. -

Culture and National Church

Microsoft Word − 04 Culture and church.docx (X:100.0%, Y:100.0%) Created by Grafikhuset Publi PDF. Culture and National Church Museums and cultural heritage Libraries Films and media Theatres Culture, economy and structure National Church Microsoft Word − 04 Culture and church.docx (X:100.0%, Y:100.0%) Created by Grafikhuset Publi PDF. Culture and National Church Museums and cultural heritage 16.1 million visits to museums In 2015, admission rates of Danish museums reached 16.1 million visitors. Of the 254 museums included in the statistics, 130 are subsidized by the state. Museums subsidized or owned by the state had 12.7 million visitors in 2015, equal to 79 per cent of the total number of visitors in 2015. In 2015, the zoological and botanical gardens had a total of 4.9 million visitors. Louisiana the most visited museum Louisiana The Art museum Louisiana account for the highest admission rates of 725,000 visitors. With a total of 580,000 visitors, Rundetårn is now ranked as num- ber two. Figure 1 Museums - the ten highest admission rates Louisiana Museum Rundetårn The National Museum, Prinsens Palais 2015 ARoS, Aarhus Kunstmuseum 2014 Moesgård Museum The Old Town The Danish National Gallery Ny Carlsberg Glyptotek The Rosenborg Collection Frederiksborg Castle 0 100 200 300 400 500 600 700 800 Thousand visits www.statbank.dk/mus Libraries Danes borrow fewer books The population continue to visit public libraries, but they do not borrow as many books as before. Lending of physical books was 26,8 million in 2015, which is 0,8 million fewer loans than the year before. -

Alternatives for Upgrading the Nykøbing Falster - Puttgarden Railway Line

ALTERNATIVES FOR UPGRADING THE NYKØBING FALSTER - PUTTGARDEN RAILWAY LINE JOANNA PAULINA LAZEWSKA, S150897 Danmarks Tekniske Universitet MASTER THESIS AUGUST 2017 ALTERNATIVES FOR UPGRADING THE NYKØBING FALSTER - PUTTGARDEN RAILWAY LINE MAIN REPORT AUTHOR JOANNA PAULINA LAZEWSKA, S150897 MASTER THESIS 30 ETCS POINTS SUPERVISORS STEVEN HARROD, DTU MANAGEMENT ENGINEERING HENRIK SYLVAN, DTU MANAGEMENT ENGINEERING RUSSEL DA SILVA, ATKINS Alternatives for upgrading the Nykøbing F — Puttgarden railway line Joanna Paulina Lazewska, s150897, August 14th 2017 Preface This project constitutes the Master’s Thesis of Joanna Lazewska, s150897. The project is conducted at the Department of Management Engineering of the Technical University of Denmark in the spring semester 2017. The project accounts for 30 ECTS points. The official supervisors for the project have been Head of Center of DTU Management Engineering Henrik Sylvan, Senior Adviser at Atkins Russel da Silva, and Associate Professor at DTU Steven Harrod. I would like to extend my gratitude to Russel da Silva for providing skillful guidance through the completion of project. Furthermore, I would like to thank Henrik Silvan and Steven Harrod for, in addition to guidance, also providing the project with their broad knowledge about economic and operational aspects of railway. In addition, I would like to thank every one who has contributed with material, consultations and guidance in the completion of this project, especially Rail Net Denmark that provided materials and plans, as well as guidance at the technical aspects of the project. A special thank is given to Atkins, which has provided office facilities, computer software, and railway specialists’ help throughout the project. It would not be possible to realize project without their help. -

555 the Regime of Passage Through the Danish Straits Alex G. Oude

The Regime of Passage Through the Danish Straits Alex G. Oude Elferink* Netherlands Institute for the Law of the Sea, Utrecht University, The Netherlands ABSTRACT The Danish Straits are the main connection between the Baltic Sea and the world oceans. The regime of passage through these straits has been the subject of extensiveregulation, raising the question how different applicable instruments interact. Apart from applicable bilateral and multilateral treaties, it is necessaryto take into account the practice of Denmark and Swedenand other interested states, and regulatory activities within the framework of the IMO. The Case ConcerningPassage Through the Great Belt before the ICJ provides insights into the views of Denmark and Finland. The article concludesthat an 1857treaty excludesthe applicabilityof Part III of the LOS Convention to the straits, and that there are a number of difficultiesin assessingthe contents of the regimeof the straits. At the same time, these uncertaintiesdo not seem to have been a complicatingfactor for the adoption of measuresto regulate shipping traffic. Introduction The Danish Straits are the main connection between the Baltic Sea and the world oceans. The straits are of vital importance for the maritime communication of the Baltic states and squarely fall within the legal category of straits used for international navigation For a number of these states the Baltic Sea is the only outlet to the oceans (Estonia, Finland, Latvia, Lithuania and Poland). Although * An earlier version of this article was presented at the international conference, The Passage of Ships Through Straits, sponsored by the Defense Analyses Institute, Athens, 23 October 1999. The author wishes to thank the speakers and participants at that conference for the stimulating discussions, which assisted in preparing the final version of the article. -

Die Küste, Heft 74, 2008

Die Küste, 74 ICCE (2008), 379-389 379 The Ports of Schleswig-Holstein Hubs of maritime economy between North and Baltic Sea and Continental Europe By GESAMTVERBAND SCHLESWIG-HOLSTEINISCHER HÄFEN C o n t e n t s 1. Introduction . 379 2. Selected Ports as Examples for the Current Situation and Development . 380 2.1 Lübeck – Germany’s largest Baltic Port . 380 2.2 Port Operating Company Brunsbüttel/Harbour Group Brunsbüttel and Glückstadt . 382 2.3 Rendsburg District Harbour . 383 2.4 Flensburg . 384 2.5 Seaport Kiel – Logistics Hub and Germany’s most important Cruise Terminal . 385 2.6 Puttgarden . 387 3. References . 389 1. I n t r o d u c t i o n The range of Schleswig-Holstein ports is manifold: High performance installations for handling large numbers of passengers, bulk and mixed cargo, as well as of Ro-Ro freight are available in the major sea ports. A consolidated network of regular ferry and freight lines provide continuous service to the Northern European States, as well as to Russia and the Baltic States. Destination and source areas of the products handled in these ports extend from the German industrial centres far into mid-, western- and southern European Sates. Nu- merous regionally important harbours open the waterways for Schleswig-Holstein’s trades and industry, afford unobstructed traffic to the islands and create an essential basis for local fisheries. Schleswig-Holstein’s ports along the Lower Elbe between Hamburg and the North Sea are partly located on junctions of the Elbe and the Kiel Canal. Due to their location, the ports of Brunsbüttel, Glückstadt and Wedel, are ideal partners for Metropolitan Hamburg in managing its streams of goods and traffic by water, rail and road. -

Zero-Emission Ferry Concept for Scandlines

Zero-Emission Ferry Concept for Scandlines Fridtjof Rohde, Björn Pape FutureShip, Hamburg/Germany Claus Nikolajsen Scandlines, Rodby/Denmark Abstract FutureShip has designed a zero-emission ferry for Scandlines’ Vogelfluglinie (linking Puttgarden (Germany) and Rødby (Denmark), which could be deployed by 2017. The propulsion is based on liquid hydrogen converted by fuel cells for the electric propulsion. The hydrogen could be obtained near the ports using excess electricity from wind. Excess on-board electricity is stored in batteries for peak demand. Total energy needs are reduced by optimized hull lines, propeller shape, ship weight and procedures in port. 1. Introduction The “Vogelfluglinie” denotes the connection of the 19 km transport corridor between Puttgarden (Germany) and Rødby (Denmark), Fig.1. This corridor has been served for many years by Scandlines ferries, which transport cars and trains. Four ferries serve two port terminals with specifically tailored infrastructure, Fig.2. The double- end ferries do not have to turn around in port, which contributes to the very short time in port. Combined with operating speed between 15 and 21 kn, departures can be offered every 30 minutes. After decades of unchal- lenged operation, two developments appeared on the horizon which changed the business situation for Scandli- nes fundamentally: 1. New international regulations would curb permissible thresholds for emissions from ships in the Baltic Sea: Starting from 2015, only fuels with less than 0.1% sulphur, i.e. a 90% reduction compared to present opera- tion, will be permissible for Baltic Sea shipping. Starting from 2016, Tier III of MARPOL’s nitrogen oxides (NOx) regulations will become effective. -

Report 08-2021

Denmark Travel Guide A Picture of Frederiksborg Castle in Hellerod, Denmark Denmark is situated in northern Europe and it remains surrounded by the North Sea, the Baltic Sea, and Germany. Most of the landmass of this country is occupied by the Jutland peninsula and the remaining 500 islands cover the rest of the country. Denmark, one of the smallest Scandinavian countries, sprinkles a distinct charm with vivacious cities and quiet rustic villages. The most fascinating attraction in Denmark is the capital Copenhagen, which is one of the most vibrant cities in the world. Intriguing sightseeing attractions of Denmark include Tivoli Gardens, Copenhagen, Aarhus, Odense, Sonderborg, Aalborg, Ribe, Vejle, Randers, Skagen, Fredrikshavn, Billund, and Silkeborg. Apart from these major tourist destinations, the whole country of Denmark is stuffed with various attractions like parks, gardens, squares, and fountains entertain the tourists who assemble here from different corners of the world. Getting In Generally, people visit Denmark by air, but one can also prefer the sea or land route. Denmark is served by two major and several minor airports. The airport is connected by train to Copenhagen Central Station, and further to Malmo and the other towns in Sweden. Buses and taxis are also available from here for tourists. Sterling, SAS Scandinavian, and others connect Copenhagen with many cities in Europe and beyond. Easy Jet serves Copenhagen from London and Berlin. British Airways offers regional services to Oslo, Gothenburg, and Stockholm. Sterling and others connect the region with several cities in Europe. If you wish to reach Denmark by train, you must know that there are five direct trains per day from Hamburg to Copenhagen. -

Iddelaldercentret FORSØGSCENTER for HISTORISK TEKNOLOGI NYKØBING FALSTER Middelaldercentrets Nyhedsblad Forår 2009

iddelaldercentret FORSØGSCENTER FOR HISTORISK TEKNOLOGI NYKØBING FALSTER Middelaldercentrets nyhedsblad forår 2009 Tro og overtro Mindre krigsvåben Leg og lær Nålemageren Bronzestøbning side 1 www.middelaldercentret.dk · forår 2009 Indhold Formandens forord Formandens forord ............................... 2 John Brædder Tro og overtro ......................................... 3 Kåre Johannessen På vej til et grønt center ...................... 6 Allan Hansen Middelaldercentret kan om blot to år fejre sit 20 års jubilæ- um. På disse 20 år er centret gået fra at være et lille beskæf- Historien om en frugtbar dialog .......... 7 tigelseprojekt på bar mark ved Guldborgsund til at blive et Kåre Johannessen internationalt anerkendt forskning- og formidlingscenter - noget af en rejse må man sige ! En nålemage kommer til byen ............ 12 Lars Sass Jensen Middelaldercentret startede i sin tid med en vild ide om at rekonstruere er middelalderlig kastemaskine - en såkaldt blide - i forbindelse med Nykøbing Smedens hus ........................................... 13 Falsters 700 års jubilæum. Bliden blev bygget under stor national og inter- Peter Vemming national bevågenhed og omkring rekonstruktionen af denne kastemaskine Bronzestøberier i Sydindien ................. 14 rejste det nuværende center sig langsomt op, ikke hastigt og uovervejet, men Peter Vemming som led i en solid forskningsindsats. Storstrøms amt, Nykøbing F. Kom- mune og Arbejdsmarkedets Feriefond gav hinanden håndslag på at skabe Leg og Lær ............................................. -

The Fehmarnbelt Tunnel: Regional Development Perspectives 3

The Fehmarnbelt Tunnel: Regional Development Perspectives 3 PETER LUNDHUS AND CHRISTIAN WICHMANN MATTHIESSEN THE FEHMARNBELT TUNNEL: REGIONAL DEVELOPMENT PERSPECTIVES ABSTRACT One link was within Denmark; the other two Following these new strategies, the Trans- were between nations. One link connects European Transport Network was adopted The Fehmarnbelt Link between Denmark and heavy economic centres, one joins more thinly and implemented nationally in different ways. Germany, for which in September 2008 a populated regions and the last one links Some countries have been focussing on high- bilateral government treaty was signed, is the peripheral areas. Two of them (the Great Belt speed railway infrastructures, others have last of the three links uniting transportation Link – linking the Danish islands of Zealand improved airports and seaways, and in networks in Northern Europe. The three links and Funen and the Øresund Link between Denmark the three fixed links totalling a (the Great Belt and the Øresund Link being Denmark and Sweden) have been constructed €13 billion investment have been given high the other two) are impressive mega structures and are fully operational. The third – the priority in the national transport action plans. (bridges/ tunnels) spanning international Fehmarnbelt Link between Denmark and The revision of the guidelines and the new waterways. They concentrate traffic flows Germany – was decided in 2008 on a bilateral EU initiatives regarding “Green Corridors” and create strong transport corridors and government level. The three links are intends to substantially affect funding are the basis of new regional development impressive mega structures (bridges/ tunnels) programmes of the TEN-T towards fostering regimes. -

Impact of the Fixed Fehmarn Belt Link on the Transport of Forest Products from Northern to Central Europe

Impact of the Fixed Fehmarn Belt Link on the Transport of Forest Products from Northern to Central Europe TENTacle [WP 2, Activity 2.1] Version: final [05.02.2018] Pl ease add your own picture 1 Content Executive summary ................................................................................................................... 6 1 Objective and goal ............................................................................................................. 7 2 Transport of Northern European forest products to Central Europe ..................................... 8 3 The place of the FBFL in the Scandinavia -Central Europe transport system and the development of forest products shipments by 2030 ...........................................................12 4 Possible changes in the modal split forest products exports to continental Europe and shifts from the ferry lines to the FBFL.................................................................................15 5 Recommendations for the maritime industry to secure their transport shares ....................18 Annexes: Main Nordic manufacturers of forest products Annex 1: Billerudkorsnäs group- overview of sea transport................................................... 18 Annex 2: Metsä Group - overview of sea transport ............................................................... 20 Annex 3: SCA group - overview of sea transport ................................................................... 22 Annex 4: Stora-Enso group - overview of sea transport ........................................................