Ethekwini Municipality Economic Review 2006/2007

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

230 South Beach Road, La Mercy

LANDMARK INDIAN OCEAN BEACH HOTEL 230 SOUTH BEACH ROAD, LA MERCY WEB#: AUCT-000854 | www.in2assets.com ADDRESS: 230 South Beach Road, La Mercy AUCTION VENUE: The Durban Country Club, Isaiah Ntshangase Road, Durban AUCTION DATE & TIME: 07 February 2019 | 11h00 VIEWING: By Appointment CONTACT: Luke Hearn | 071 351 8138 | 031 574 7600 | [email protected] REGISTRATION FEE: R 50 000-00 (Refundable Bank Guaranteed Cheque) AUCTIONEER: Andrew Miller CONTENTS 230 SOUTH BEACH ROAD, LA MERCY 1318 Old North Coast Road, Avoca CPA LETTER 2 PROPERTY DESCRIPTION 3 PROPERTY LOCATION 4 PICTURE GALLERY 5 ADDITIONAL INFORMATION 12 TERMS AND CONDITIONS 14 SG DIAGRAMS 15 TITLE DEED 19 ZONING CERTIFICATE 28 BUILDING PLANS 31 LICENCES 38 DISCLAIMER: Whilst all reasonable care has been taken to provide accurate information, neither In2assets Properties (Pty) Ltd nor the Seller/s guarantee the correctness of the information, provided herein and neither will be held liable for any direct or indirect damages or loss, of whatsoever nature, suffered by any person as a result of errors or omissions in the information provided, whether due to the negligence or otherwise of In2assets Properties (Pty) Ltd or the Sellers or any other person. The Consumer Protection Regulations as well as the Rules of Auction can be viewed at www.In2assets.com or at Unit 504, 5th Floor, Strauss Daly Place, 41 Richefond Circle, Ridgeside Office Park, Umhlanga Ridge. Bidders must register to bid and provide original proof of identity and residence on registration. Version V4: 17.01.2019 1 CPA LETTER 230 SOUTH BEACH ROAD, LA MERCY 1318 Old North Coast Road, Avoca In2Assets would like to offer you, our valued client, the opportunity to pre-register as a bidder prior to the auction day. -

Promoting Green Urban Development in African Cities

Public Disclosure Authorized Promoting Green Urban Development in African Cities ETHEKWINI, SOUTH AFRICA Urban Environmental Profile Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Promoting Green Urban Development in African Cities ETHEKWINI, SOUTH AFRICA Urban Environmental Profile COPYRIGHT © 2016 International Bank for Reconstruction and Development / The World Bank 1818 H Street NW Washington DC 20433 Telephone: 202-473-1000 Internet: www.worldbank.org This work is a product of the staff of The World Bank with external contributions. The findings, interpretations, and conclusions expressed in this work do not necessarily reflect the views of The World Bank, its Board of Executive Directors, or the governments they represent. The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries. February 2016 RIGHTS AND PERMISSIONS The material in this work is subject to copyright. Because The World Bank encourages dissemination of its knowledge, this work may be reproduced, in whole or in part, for noncommercial purposes as long as full attribution to this work is given. Any queries on rights and licenses, including subsidiary rights, should be addressed to the Publishing and Knowledge Division, The World Bank Group, 1818 H Street NW, Washington, DC 20433, USA; fax: 202-522-2625; e-mail: [email protected]. ACKNOWLEDGEMENTS The Promoting Green Urban Development in African Cities, Urban Environmental Profile for eThekwini, South Africa was prepared by a core study team led by Roland White (Global Lead: City Management, Governance and Financing - Task Team Leader) and included Chyi-Yun Huang (Urban Specialist) and a consultant team from AECOM including John Bachmann, Diane Dale, Brian Goldberg, Maritza Pechin and Dr. -

ETHEKWINI MUNICIPALTY Water and Sanitation

EWS Planning of Water and Sanitation 13/02/2015 . Strategic Objectives . Legislation driving the business plan . Time horizon – Long term, medium term and short term plan – in terms in terms of legislated submission cycle . Beyond Urban Edge . Backlogs . Drought Strategic Objectives . Customer Perspective: Deliver quality and affordable services to our customers and customers take good care of the infrastructure. Financial Perspective: Achieve financial sustainability (sustainable tariffs, controlling costs, increased allocation of grants, etc.). Process Perspective: . Deliver fast, efficient, and effective service delivery (effective performance, removing constraints and bottlenecks, and improving efficiency). Ensure compliance to legislation and relevant governance prescripts (SCM, Environmental legislation, Health & Safety, etc.). Identify and effectively manage exposure to all risks. Achieve an unqualified audit. Organisational Capacity Perspective: . Ensure availability of adequate and appropriately skilled workforce. Sound (condition) and adequate (capacity) infrastructure to support current and future demand for water and sanitation services. Collaborate with relevant stakeholders to increase water resources sustainability. Legislations & Policies Driving the Business Plan . National Water Services Act . Water Supply Bylaws . Blue Drop certification requirements . Green Drop certification requirements . No Drop certification requirements . Environmental policies and Acts . Water Services Development Plan (WSDP) . Policies and Practices -

An Investigation Into Factors Increasing Contamination Risk Posed by Fuel Storage Facilities and Concomitant Methods to Mitigate These Risks

AN INVESTIGATION INTO FACTORS INCREASING CONTAMINATION RISK POSED BY FUEL STORAGE FACILITIES AND CONCOMITANT METHODS TO MITIGATE THESE RISKS by Torin Pfotenhauer BSc(Hons) University of Natal Submitted in fulfilment of the academic requirements for the degree of MASTER OF ENGINEERING in the School of Chemical Engineering University of KwaZulu-Natal Howard College DURBAN June 2011 - ii - As the candidates Supervisor, I agree / do not agree to the submission of this dissertation. Name______________________ Signature____________________ Date__________ - iii - ACKNOWLEDGEMENTS The author acknowledges the following people for their invaluable contribution: Professor Chris Buckley for his extraordinary talent, open mind, insight and care. Dr Jennifer Pretorius who conceived the project. Kantey & Templer for unequivocal support. The Institute of Groundwater Studies from the University of the Free State who funded the project. The South African Petroleum Industry Association who supported the project. Chris Brouckaert who assisted with the data and statistics. Natalie Way-Jones who supported my endeavours. Dr Robert Palmer who sent the laughter down the passage during those late nights. Professor Glenda Matthews who unselfishly submerged herself in my project, understood my data nuances and led me through the data analysis and modelling. - iv - ABSTRACT Light Non-Aqueous Phase Liquids (LNAPLs) are used throughout the world for numerous applications, the most well-known being automotive fuels, such as petrol and diesel. The widespread production, distribution, storage and use of LNAPLs results in the ubiquitous occurrence of spillage to ground (Geller et al, 2000). Considering the hazardous nature of most LNAPLs due to their explosive and toxic characteristics, releases of LNAPLs to ground have well documented human health and ecological consequences. -

Cultural and Heritage Impact Assessment

APPENDIX M Cultural and Heritage Impact Assessment eThembeni Cultural Heritage Heritage Impact Assessment Report Proposed Lanele Terminal 1. (Lot 1) Project, Ambrose Park, Bayhead Durban Harbour eThekweni Municipality Report prepared for: Report prepared by: Golder Associates Africa (Pty) Ltd. eThembeni Cultural Heritage Building 1, Golder House, Maxwell Office Park, P O Box 20057 Magwa Crescent West, Waterfall City ASHBURTON P.O. Box 6001, Halfway House, 1685 3213 Midrand, South Africa, 1685 Tel: +27 11 254 4800 | Fax: +27 86 582 1561 16 January 2019 DECLARATION OF INDEPENDENCE I, Leonard van Schalkwyk, declare that – I act as the independent specialist in this application. I will perform the work relating to the application in an objective manner even if this results in views and findings that are not favourable to the applicant. I declare that there are no circumstances that may compromise my objectivity in performing such work. I have no, and will not engage in, conflicting interests in the undertaking of the activity. I undertake to disclose to the applicant and the competent authority all material information in my possession that reasonably has or may have the potential of influencing any decision to be taken with respect to the application by the competent authority; and the objectivity of any report, plan or document to be prepared by myself for submission to the competent authority. All the particulars furnished by me in this form are true and correct. Signed 16 January 2019 EXECUTIVE SUMMARY INTRODUCTION eThembeni Cultural Heritage was appointed by Golder Associates Africa (Pty) Ltd, to conduct a Phase1 Heritage Impact Assessment (HIA) for the establishment of a new liquid fuel storage and handling facility, the Lanele Oil Terminal 1 (Lot 1) project, on a portion of the Kings Royal Flats No. -

Portfolio of Land for Conversion in Kwazulu-Natal – November 2014

PORTFOLIO OF LAND FOR CONVERSION IN KWAZULU-NATAL NOVEMBER 2014 Tongaat hulett has an unequalled portfolio of 8 150 developable hectares of land in prime locations, prepared for unlocking substantial value and UNLOCKING cash flow. The 2014 Integrated Annual Report included details of the portfolio as at 31 March 2014. It indicated that sales over the next 5 years were likely to SUBSTANTIAL come out of 3 710 developable hectares of land in key focus areas. This document contains details of the transactions concluded in the VALUE IN 6 months to 30 September 2014. A total of 49 developable hectares were THE LAND sold, generating profit of R435 million. The portfolio, as at 30 September 2014 is detailed further in this document. The intention is to update this overview of the land portfolio regularly, to PORTFOLIO provide details of progress made, significant events and key indicators including profits realised. The step-up in value realisation and the Profit achieved R1,080 billion earned from sales of 259 hectares Area Description (R million per of land in the year ended 31 March 2014 is also developable hectare) an indication of the momentum established and Ridgeside Prime, high density, mixed use 34 the way forward. precinct with sea views Umhlanga Ridge High density mixed use urban The profit achieved per hectare of land sold Town Centre precinct 29,4 is increasing with the steadily improving land conversion platform and varies based on usage Izinga / Kindlewood Low density upper market residential suburbs 3,5 to 6,7 and location. In the past 18 months, the range achieved varied from R2,4 million to R34,0 million Cornubia Industrial and Light industrial, logistics, Business Estate warehousing and business parks 6 to 9,5 per developable hectare. -

Earthworm Species Occurrence in Agroecosystems in the Midlands, Kwazulu-Natal, South Africa

African Invertebrates 62(2): 411–425 (2021) doi: 10.3897/AfrInvertebr.62.67875 RESEARCH ARTICLE https://africaninvertebrates.pensoft.net Earthworm species occurrence in agroecosystems in the Midlands, KwaZulu-Natal, South Africa Thembeka C. Nxele1,3, Tarombera Mwabvu2,3, Inam Yekwayo4 1 KwaZulu-Natal Museum, Private Bag 9070, Pietermaritzburg, 3200, South Africa 2 School of Biology & Environmental Sciences, University of Mpumalanga, Private Bag X11283, Mbombela, 1200, South Africa 3 School of Life Sciences, University of KwaZulu-Natal, Private Bag X54001, Westville campus, Durban, 4001, South Africa 4 Department of Biological and Environmental Sciences, Walter Sisulu University, Private Bag X1, Mthatha, 5127, South Africa Corresponding author: Thembeka C. Nxele ([email protected]) Academic editor: Burgert Muller | Received 26 April 2021 | Accepted 2 August 2021 | Published 12 August 2021 http://zoobank.org/A87C1D0F-0D1A-4EBD-AAE4-01E8D7850053 Citation: Nxele TC, Mwabvu T, Yekwayo I (2021) Earthworm species occurrence in agroecosystems in the Midlands, KwaZulu-Natal, South Africa. African Invertebrates 62(2): 411–425. https://doi.org/10.3897/AfrInvertebr.62.67875 Abstract Little is known about the species composition of earthworms in agroecosystems in South Africa even though earthworms provide soil ecosystem services and are useful biological indicators of changes in the habitats. Given the land use and management impact biodiversity, the aim of this study was to docu- ment earthworm species that occur under cultivated land in the KwaZulu-Natal -

Following Is a Load Shedding Schedule That People Are Advised to Keep

Following is a load shedding schedule that people are advised to keep. STAND-BY LOAD SHEDDING SCHEDULE Monday Tuesday Wednesday Thursday Friday Saturday Sunday Block A 04:00-06:30 08:00-10:30 04:00-06:30 08:00-10:30 04:00-06:30 08:00-10:30 08:00-10:30 Block B 06:00-08:30 14:00-16:30 06:00-08:30 14:00-16:30 06:00-08:30 14:00-16:30 14:00-16:30 Block C 08:00-10:30 16:00-18:30 08:00-10:30 16:00-18:30 08:00-10:30 16:00-18:30 16:00-18:30 Block D 10:00-12:30 12:00-14:30 10:00-12:30 12:00-14:30 10:00-12:30 12:00-14:30 12:00-14:30 Block E 12:00-14:30 10:00-12:30 12:00-14:30 10:00-12:30 12:00-14:30 10:00-12:30 10:00-12:30 Block F 14:00-16:30 18:00-20:30 14:00-16:30 18:00-20:30 14:00-16:30 18:00-20:30 18:00-20:30 Block G 16:00-18:30 20:00-22:30 16:00-18:30 20:00-22:30 16:00-18:30 20:00-22:30 20:00-22:30 Block H 18:00-20:30 04:00-06:30 18:00-20:30 04:00-06:30 18:00-20:30 04:00-06:30 04:00-06:30 Block J 20:00-22:30 06:00-08:30 20:00-22:30 06:00-08:30 20:00-22:30 06:00-08:30 06:00-08:30 Area Block Albert Park Block D Amanzimtoti Central Block B Amanzimtoti North Block B Amanzimtoti South Block B Asherville Block H Ashley Block J Assagai Block F Athlone Block G Atholl Heights Block J Avoca Block G Avoca Hills Block C Bakerville Gardens Block G Bayview Block B Bellair Block A Bellgate Block F Belvedere Block F Berea Block F Berea West Block F Berkshire Downs Block E Besters Camp Block F Beverly Hills Block C Blair Atholl Block J Blue Lagoon Block D Bluff Block E Bonela Block E Booth Road Industrial Block E Bothas Hill Block F Briardene Block G Briardene -

ANNUAL REPORT 2018/2019 ANNUAL REPORT 2018/2019 Ii Design and Layout: Artworks | 1 KWAZULU-NATALKWAZULU-NATAL TOURISM TOURISM AUTHORITY AUTHORITY

ANNUAL REPORT 2018/2019 ANNUAL REPORT 2018/2019 II Design and layout: Artworks | www.artworks.co.za 1 KWAZULU-NATALKWAZULU-NATAL TOURISM TOURISM AUTHORITY AUTHORITY Contents Part A: General Information Public Entity’s General Information .........................................................................................................2 List of Acronyms/Abbreviations ................................................................................................................3 MEC’s Foreword ...............................................................................................................................................4 Chairperson’s Statement ..............................................................................................................................6 Acting CEO’s Overview .................................................................................................................................8 Statement of Responsibility for the Year Ended 31 March 2019 ................................................. 14 Strategic Overview ...................................................................................................................................... 16 Legislative and Other Mandates ........................................................................................................... 18 Organisational Structure ........................................................................................................................... 20 Board of Directors ............................................................................................................................... -

Seia for Dube Tradeport Cottonlands Tradezone 4

SEIA FOR DUBE TRADEPORT COTTONLANDS INDUSTRIAL PARK – DRAFT 1 FOR COMMENT – 27/02/2017 Socio Economic Impact Assessment Tradezone 4 (Cottonlands) - 2016 DUBE TRADEPORT COTTONLANDS INDUSTRIAL PARK SOCIO- ECONOMIC IMPACT ASSESSMENT Page 1 of 62 SEIA FOR DUBE TRADEPORT COTTONLANDS INDUSTRIAL PARK – DRAFT 1 FOR COMMENT – 27/02/2017 Prepared by: Urban-Econ Development Economists P O Box 50834, Musgrave, 4062 Tel: 031-202 9673 Email: [email protected] Prepared for: Element Consulting Engineers PO Box 1071, Westville, Durban,3630 Tel: 031 266 9699 Page 2 of 62 SEIA FOR DUBE TRADEPORT COTTONLANDS INDUSTRIAL PARK – DRAFT 1 FOR COMMENT – 27/02/2017 TABLE OF CONTENTS 1 Introduction ................................................................................................................................................................ 5 2 Spatial Analysis ........................................................................................................................................................ 10 3 Socio-Economic Profile ........................................................................................................................................... 15 4 General Market Trends ............................................................................................................................................ 18 5 Office, Residential, Retail and Industrial Trend Analysis ...................................................................................... 22 6 Market Assessment ................................................................................................................................................. -

Appendix E: Public Participation Part I

PART I APPENDIX E: PUBLIC PARTICIPATION PART I APPENDIX E.1: I&AP DATABASE 1 APPENDIX E.2. CORRESPONDENCE TO I&APS RELATING TO FSR 10 LETTER 4 TO I&APS 10 PROOF OF CORRESPONDENCE WITH I&APS - REGISTERED MAIL RECEIPTS 13 PROOF OF CORRESPONDENCE WITH I&APS - COURIER WAYBILLS 28 EMAIL TO I&APS (RELEASE OF FSR) 30 APPENDIX E.3: CORRESPONDENCE FROM I&APS PRIOR TO RELEASE OF DRAFT EIA REPORT (AFTER RELEASE OF FSR) 43 APPENDIX E.4. CORRESPONDENCE TO I&APS – RELEASE OF DRAFT EIA REPORT 77 LETTER 5 TO I&APS 77 PROOF OF CORRESPONDENCE WITH I&APS - REGISTERED MAIL RECEIPTS 81 EMAIL TO I&APS 85 ADVERTISEMENTS 93 SITE NOTICES 99 APPENDIX E.5: CORRESPONDENCE FROM I&APS AFTER RELEASE OF DRAFT EIA REPORT 100 Copyright 2018 © CSIR – June 2018 Appendix E, Public Participation APPENDIX E.1: I&AP DATABASE Copyright 2018 © CSIR – June 2018 Appendix E, Public Participation, Page E-1 ORGANS OF STATE National Department of Environmental Affairs Ms Matlhodi Mogorosi National Department of Environmental Affairs Mr H Alberts Department of Environmental Affairs: Oceans and Coasts Mrs Nitasha Baijnath-Pillay Department of Environmental Affairs: Oceans and Coasts Mr Mulalo Tshikotshi Department of Energy Sandile Ntanzi Department of Mineral Resources KZN Ms N Khanyile Department of Public Works – KwaZulu-Natal Mr Nkosi Vilakazi Department of Transport Mrs J Reddy Department of Water Affairs and Sanitation Attention: Central Point Department of Agriculture, Forestry and Fisheries: Land Use and Soil Ms Anneliza Collet Management Department of Agriculture, Forestry and Fisheries Ms Mashudu Marubini Department of Land Affairs Ms Thembisile Mabaso KZN Department of Economic Development, Tourism and Ms Yugeshni Govender Environmental Affairs KZN Department of Economic Development, Tourism and Ms. -

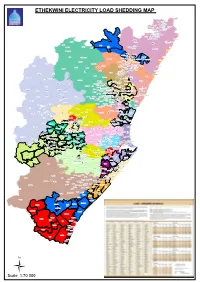

Ethekwini Electricity Load Shedding Map

ETHEKWINI ELECTRICITY LOAD SHEDDING MAP Lauriston Burbreeze Wewe Newtown Sandfield Danroz Maidstone Village Emona SP Fairbreeze Emona Railway Cottage Riverside AH Emona Hambanathi Ziweni Magwaveni Riverside Venrova Gardens Whiteheads Dores Flats Gandhi's Hill Outspan Tongaat CBD Gandhinagar Tongaat Central Trurolands Tongaat Central Belvedere Watsonia Tongova Mews Mithanagar Buffelsdale Chelmsford Heights Tongaat Beach Kwasumubi Inanda Makapane Westbrook Hazelmere Tongaat School Jojweni 16 Ogunjini New Glasgow Ngudlintaba Ngonweni Inanda NU Genazano Iqadi SP 23 New Glasgow La Mercy Airport Desainager Upper Bantwana 5 Redcliffe Canelands Redcliffe AH Redcliff Desainager Matata Umdloti Heights Nellsworth AH Upper Ukumanaza Emona AH 23 Everest Heights Buffelsdraai Riverview Park Windermere AH Mount Moreland 23 La Mercy Redcliffe Gragetown Senzokuhle Mt Vernon Oaklands Verulam Central 5 Brindhaven Riyadh Armstrong Hill AH Umgeni Dawncrest Zwelitsha Cordoba Gardens Lotusville Temple Valley Mabedlane Tea Eastate Mountview Valdin Heights Waterloo village Trenance Park Umdloti Beach Buffelsdraai Southridge Mgangeni Mgangeni Riet River Southridge Mgangeni Parkgate Southridge Circle Waterloo Zwelitsha 16 Ottawa Etafuleni Newsel Beach Trenance Park Palmview Ottawa 3 Amawoti Trenance Manor Mshazi Trenance Park Shastri Park Mabedlane Selection Beach Trenance Manor Amatikwe Hillhead Woodview Conobia Inthuthuko Langalibalele Brookdale Caneside Forest Haven Dimane Mshazi Skhambane 16 Lower Manaza 1 Blackburn Inanda Congo Lenham Stanmore Grove End Westham