Stock Market Reaction to Election Results: an Event Study Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Acs, Servicios, Comunicaciones Y Energía, S.L

PROSPECTUS DATED 17 APRIL 2018 ACS, SERVICIOS, COMUNICACIONES Y ENERGÍA, S.L. (incorporated with limited liability in the Kingdom of Spain) €750,000,000 1.875 per cent. Green Notes due 2026 The issue price of the €750,000,000 1.875 per cent. Green Notes due 20 April 2026 (the Notes or the Green Notes) of ACS, Servicios, Comunicaciones y Energía, S.L. (the Issuer) is 99.435 per cent of their principal amount. Unless previously redeemed or cancelled, the Notes will be redeemed at their principal amount on 20 April 2026 (the Maturity Date). The Notes are subject to redemption in whole at their principal amount at the option of the Issuer at any time in the event of certain changes affecting taxation in the Kingdom of Spain. See “Terms and Conditions of the Notes—Redemption and Purchase”. In addition, if a Change of Control occurs and, during the Change of Control Period, a Rating Downgrade occurs, then each Noteholder may require the Issuer to redeem or, at the Issuer's option, purchase in whole or in part its Notes at their principal amount plus accrued and unpaid interest up to (but excluding) the date for such redemption or purchase, all as more fully set out under “Terms and Conditions of the Notes—Redemption and Purchase – Change of Control”. The Notes are subject to redemption in whole at their principal amount together with any accrued and unpaid interest up to (but excluding) the date fixed for such redemption which shall be no earlier than three months before the Maturity Date, as more fully set out under “Terms and Conditions of the Notes— Redemption and Purchase – Residual Maturity Call Option”. -

Tecnicas Reunidas

Tecnicas Reunidas Spain/ Oil Services Post results note Investment Research 11 NOVEMBER 2016 Accumulate Resultados del 3T16, en línea con lo estimado. Recommendation unchanged La noticia: Técnicas Reunidas presentó ayer los resultados del 3T16. Share price: EUR 33.75 closing price as of 10/11/2016 Nuestro análisis: Los resultados han estado en línea con lo estimado. Target price: EUR 36.00 TECNICAS REUNIDAS : 9M16 RESULTS Target Price unchanged 9M15 %sles 9M16 %sles %y/y 2Q16 3Q15 3Q16 Sales 3,006.0 100% 3,437.9 100% 14.4% 1,252.6 1,122.4 1,134.0 Reuters/Bloomberg TRE.MC/TRE SM EBITDA 159.2 5.3% 154.1 4.5% -3.2% 55.4 56.6 51.6 Daily avg. no. trad. sh. 12 mth 480 Depreciation -11.6 -0.4% -15.2 -0.4% 31.0% -5.2 -4.0 -5.0 Daily avg. trad. vol. 12 mth (m) 20,834.07 EBIT 147.6 4.9% 138.9 4.0% -5.9% 50.3 52.6 46.5 Price high 12 mth (EUR) 38.31 Financial results 4.2 0.1% -1.1 0.0% -1.4 1.0 3.2 Price low 12 mth (EUR) 21.75 EBT 151.8 5.0% 137.8 4.0% -9.2% 48.8 51.4 48.2 Abs. perf. 1 mth -6.2% Income tax -36.6 -1.2% -36.5 -1.1% -0.3% -13.2 -11.3 -12.7 Abs. perf. 3 mth 6.2% Net profit 115.2 3.8% 101.3 2.9% -12.1% 35.7 40.1 35.4 Abs. -

Cloud Managed Services and Hosting Sector Review | Q1 2020

CLOUD MANAGED SERVICES AND HOSTING SECTOR REVIEW | Q1 2020 Technology Cloud Managed Services and Hosting| Q1 2021 TECHNOLOGY, MEDIA & TELECOM PAGE | 0 Cloud Managed Services and Hosting Taxonomy WEB HOSTING MANAGED SERVICES IT OUTSOURCING Refers to a service in which a vendor offers the Refers to the delivery of network, application, system Refers to the use of external service providers to housing of business-to-business or business-to- and e-management services across a network to effectively deliver IT-enabled business process, consumer eCommerce websites via vendor-owned multiple enterprises, using a pay-as-you-go pricing application service and infrastructure solutions shared or dedicated servers and applications for model for business outcomes enterprises at the provider-controlled facilities SELECTED MARKET PARTICIPANTS SELECTED MARKET PARTICIPANTS SELECTED MARKET PARTICIPANTS S E L E C T E D HW CLOUD MANAGED SERVICES AND HOSTING TRANSACTIONS & has made a significant has been acquired by has acquired have been acquired by has been acquired by has been acquired by investment in Provider of a post-warranty Provider of mass hosting Provider of services Provider of web domains, Provider of managed Provider of SME-focused alternative for storage, server services for SMEs, including allowing SMEs to move shared web hosting and technology services with hosting and cloud solutions, and networking hardware web hosting, domains, their IT infrastructure and value-added services with national scale in the US and including domain and maintenance -

The New ACS Group Construction 1H/03 Revenues

Global Construction Conference November,November, 20032003 Index Highlights The new ACS Group Outlook for 2003 Conclusions 2 Highlights Strategic rationale of the merger Creation of a European leader • #1 in the most profitable market: Spain • Market leader in all businesses related to the development and management of infrastructures Excellent growth opportunities • Diversified portfolio of activities • Government Investment Plans Potential synergies from the merger Financial strength Industry’s reference stock • Market Capitalization > € 4.3 bn • Liquidity > € 20 mn daily 3 Highlights Creation of a market leader … # 1 in Spanish Construction # 1 in Industrial Services in Spain, Portugal & Latam # 1 in Waste Management in Spain # 1 in Ports and Logistics Services in Spain Core shareholder in the # 1 transport infrastructure concessions company worldwide (by # of concessions) 4 Highlights … of European size … Comp. EBIT 03e* € million 650 Margin on sales 6,0% 525 425 4,3% 3,3% 285 3,0% 250 1,9% 200 1,6% Sales 03e (€ bn) ACS Vinci Bouygues Skanska Ferrovial** Hochtieff Total Sales 10.8 17.5 21.5 14.9 7.0 12.3 Comp. Sales* 10.8 15.7 14.2 12.3 5.8 12.3 * Comparable data are estimated figures in those activities carried out by all companies:Construction, Services & Industrial. It does not include data from Concessions, Real Estate and other businesses. ** Ferrovial figures include CESPA & Amey full year data Source: Analysts’ Reports and Companies data 5 Highlights … and invested in Concessions Equity Investments in Concessions* € billion 3.0 1.7 1.0 Vinci Ferrovial ACS Main Cofiroute(85%), carparks, Cintra (60%), including Abertis (12%), highways, Assets airports & ASF (17%) ETR 407, carparks & airports airports & railroads Accounting Global consolidation Global consolidation Equity accounted method (except ASF: Equity acc.) * Source: Companies’ Reports. -

Forty Years of Democratic Spain: Political, Economic, Foreign Policy

Working Paper Documento de Trabajo Forty years of democratic Spain Political, economic, foreign policy and social change, 1978-2018 William Chislett Working Paper 01/2018 | October 2018 Sponsored by Bussiness Advisory Council With the collaboration of Forty years of democratic Spain Political, economic, foreign policy and social change, 1978-2018 William Chislett - Real Instituto Elcano - October 2018 Real Instituto Elcano - Madrid - España www.realinstitutoelcano.org © 2018 Real Instituto Elcano C/ Príncipe de Vergara, 51 28006 Madrid www.realinstitutoelcano.org ISSN: 1699-3504 Depósito Legal: M-26708-2005 Working Paper Forty years of democratic Spain Political, economic, foreign policy and social change, 1978-2018 William Chislett Summary 1. Background 2. Political scene: a new mould 3. Autonomous communities: unfinished business 4. The discord in Catalonia: no end in sight 5. Economy: transformed but vulnerable 6. Labour market: haves and have-nots 7. Exports: surprising success 8. Direct investment abroad: the forging of multinationals 9. Banks: from a cosy club to tough competition 10. Foreign policy: from isolation to full integration 11. Migration: from a net exporter to a net importer of people 12. Social change: a new world 13. Conclusion: the next 40 years Appendix Bibliography Working Paper Forty years of democratic Spain Spain: Autonomous Communities Real Instituto Elcano - 2018 page | 5 Working Paper Forty years of democratic Spain Summary1 Whichever way one looks at it, Spain has been profoundly transformed since the 1978 -

ETF Accion IBEX

Acción Ibex ETF ¿Qué es el IBEX 35? El IBEX 35 es el índice oficial del Mercado Contínuo español. Está formado por las 35 compañías más líquidas negociadas en el Mercado Contínuo español. Es calculado, supervisado y publicado por Sociedad de Bolsas. ¿Qué valores lo componen? Abertis Infraestructuras SA Gamesa Corp Tecnologica SA Acciona SA Gas Natural SDG SA Acerinox SA Gestevision Telecinco SA ACS Actividades Cons y Serv Grupo Ferrovial SA Altadis SA Iberdrola SA Antena 3 de Television SA Iberia Lineas Aereas de Espana Banco Bilbao Vizcaya Argentaria SA Inditex SA Banco Espanol de Credito SA Indra Sistemas SA Banco Popular Espanol SA Metrovacesa SA Banco Sabadell SA NH Hoteles SA Banco Santander Central Hispano SA Promotora de Informaciones SA Bankinter SA Red Electrica de Espana Cintra Concesiones de Infraestructuras d Repsol YPF SA Corp Mapfre SA Sacyr Vallehermoso SA Enagas Sogecable SA Endesa SA Telefonica SA Fadesa Inmobiliaria SA Union Fenosa SA Fomento de Construcciones y Contratas SA Dónde se puede seguir su evolución y la de sus activos respectivos La evolución del IBEX 35, se puede seguir en Bloomberg y Reuters. También en periódicos como Expansión, Cinco días, ABC. BBVA Gestión de Activos Acción Ibex ETF Descripción del nuevo ETF: recordar cómo funciona y su operativa Acción IBEX ETF es un Fondo de Inversión, cuyo objetivo es replicar el índice IBEX 35. En definitiva, se trata de un producto a medio camino entre un fondo de inversión y una acción. Se contrata igual que cualquier acción que cotiza en el mercado español, pudiendo contratarse en cualquier momento de la sesión bursátil. -

Business Services M&A Outlook Q3 2017

Business Services M&A Outlook Q3 2017 About Us Calabasas Capital is a boutique investment banking firm focused on serving lower middle-market privately-held companies. We specialize in representing and advising businesses on sell-side and buy-side mergers and acquisitions and we raise private equity and debt capital. Overview of M&A Activity • M&A activity in the business services space has continued to be strong through the second quarter of 2017. Business Services M&A Volume* 4,000 3,599 3,500 3,278 3,084 3,000 2,829 2,839 2,851 2,589 2,477 2,531 2,500 2,154 2,000 1,500 1,192 1,000 500 - 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017** *Represents the number of all announced or closed M&A transactions in the U.S. and Canada. **Sources: Harris Williams, FactSet. 1 News/Trends by Sector • Business Process Outsourcing Cognizant Technology Solutions, which reported 9% year-over-year growth in 2Q2017 revenue, continues to be acquisitive with its most recent deal to acquire TMG Health completed in August 2017. Cognizant (NASDAQ: CTSH) is one of the world's leading professional services companies, with a focus on transforming clients' business, operating and technology models for the digital era. TMG Health is a leading national provider of business process services to the Medicare Advantage, Medicare Part D and Managed Medicaid markets in the United States, supporting 32 health plans and more than 4.4 million members in all 50 states. • Consulting On its first quarter earnings call Accenture announced it completed 10 acquisitions in 1Q 2017 and plans to spend $1 billion on acquisitions in 2017 as it seeks to accelerate growth and outspend its competition. -

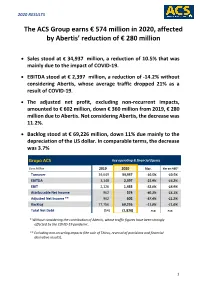

The ACS Group Earns € 574 Million in 2020, Affected by Abertis' Reduction

2020 RESULTS The ACS Group earns € 574 million in 2020, affected by Abertis’ reduction of € 280 million Sales stood at € 34,937 million, a reduction of 10.5% that was mainly due to the impact of COVID-19. EBITDA stood at € 2,397 million, a reduction of -14.2% without considering Abertis, whose average traffic dropped 21% as a result of COVID-19. The adjusted net profit, excluding non-recurrent impacts, amounted to € 602 million, down € 360 million from 2019, € 280 million due to Abertis. Not considering Abertis, the decrease was 11.2%. Backlog stood at € 69,226 million, down 11% due mainly to the depreciation of the US dollar. In comparable terms, the decrease was 3.7% Grupo ACS Key operating & financial figures Euro Million 2019 2020 Var. Var ex-ABE* Turnover 39,049 34,937 -10.5% -10.5% EBITDA 3,148 2,397 -23.9% -14.2% EBIT 2,126 1,433 -32.6% -18.9% Attributable Net Income 962 574 -40.3% -15.1% Adjusted Net Income ** 962 602 -37.4% -11.2% Backlog 77,756 69,226 -11.0% -11.0% Total Net Debt (54) (1,820) n.a. n.a. * Without considering the contribution of Abertis, whose traffic figures have been strongly affected by the COVID-19 pandemic. ** Excluding non-recurring impacts (the sale of Thiess, reversal of provisions and financial derivative results). 1 2020 RESULTS 1. Consolidated Results The Group’s 2020 ordinary net profit accounted for € 602 million, € 360 million less than the previous year. This decline is mainly due to the evolution of Abertis, whose traffic was heavily affected by the lockdown measures related to COVID- 19, reducing its contribution by € 280 million. -

SOCIETE GENERALE Comisión Nacional Del Mercado De Valores

SOCIETE GENERALE Comisión Nacional del Mercado de Valores Calle Edison nº 4 28010 Madrid Madrid, 23 de marzo de 2020 Muy señores nuestros: En relación con las emisiones de Warrants realizadas por SOCIÉTÉ GÉNÉRALE sobre activos españoles, con fechas de emisión 31 de mayo de 2019, y 19 de septiembre de 2019, y fecha de vencimiento 20 de marzo de 2020, y de conformidad con lo dispuesto en las Condiciones Finales de dichas emisiones, les comunicamos a continuación los Precios de Referencia y los Importes de Liquidación unitarios de los Warrants mencionados: Precio de Liquidación Código Tipo de del Activo Importe de Código ISIN Bolsa Subyacente Tipo Strike Ratio cambio Subyacente liquidación LU1946231435 H4268 ACCIONA, S.A. CALL 100 0,1 1 105 0,5 LU1946231518 H4269 ACCIONA, S.A. CALL 110 0,1 1 105 0 LU1946231609 H4270 ACCIONA, S.A. PUT 90 0,1 1 105 0 LU1946231781 H4271 ACERINOX CALL 8 0,5 1 5,924 0 LU1946231864 H4272 ACERINOX CALL 10 0,5 1 5,924 0 DE000CJ30845 H3102 ACERINOX CALL 11 0,5 1 5,924 0 LU1946231948 H4273 ACERINOX PUT 8 0,5 1 5,924 1,038 ACS,ACTIVIDADES DE CONSTRUCCION Y LU1946232086 H4274 SERVICIOS,S.A. CALL 36 0,2 1 13,375 0 ACS,ACTIVIDADES DE CONSTRUCCION Y LU1946232169 H4275 SERVICIOS,S.A. CALL 42 0,2 1 13,375 0 ACS,ACTIVIDADES DE CONSTRUCCION Y LU1946232243 H4276 SERVICIOS,S.A. PUT 33 0,2 1 13,375 3,925 LU1946232672 H4279 AENA CALL 160 0,05 1 126 0 LU1946232755 H4280 AENA CALL 180 0,05 1 126 0 LU1946232839 H4281 AENA PUT 150 0,05 1 126 1,2 AMADEUS IT HOLDING, LU2000322417 H5411 S.A. -

Temporary Prohibition of Short Selling

11/13/2020 Temporary prohibition of short selling Temporary prohibition of short selling The FCA notifies that it temporarily prohibits short selling in the following instruments under Articles 23 (1) and 26 (4) of Regulation (EU) No 236/2012 of the European Parliament and of the Council of 14 March 2012. This follows a decision made by another EU Competent Authority. Details of the Financial Instruments concerned: • ABENGOA CLASE B (ISIN: ES0105200002) • ACCIONA, S.A. (ISIN: ES0125220311) • ACCIONES FOMENTO DE (ISIN: ES0122060314) • ACCIONES IBERDROLA (ISIN: ES0144580Y14) • ACERINOX, S.A. (ISIN: ES0132105018) • ACS,ACTIVIDADES DE CO (ISIN: ES0167050915) • AEDAS HOMES, S.A (ISIN: ES0105287009) • AENA, S.M.E., S.A. (ISIN: ES0105046009) • AIRBUS (ISIN:NL0000235190) • AMADEUS IT GROUP, S.A. (ISIN: ES0109067019) • APERAM (ISIN: LU0569974404) • APPLUS SERVICES, S.A. (ISIN: ES0105022000) • ARCELORMITTAL SA (ISIN: LU1598757687) • ATRESMEDIA CORPORAC (ISIN: ES0109427734) • AUDAX RENOVABLES, S.A (ISIN: ES0136463017) • BANCO BILBAO VIZCAYA (ISIN: ES0113211835) • BANCO DE SABADELL (ISIN: ES0113860A34) • BANCO SANTANDER S.A. (ISIN: ES0113900J37) • BANKIA, S.A. (ISIN: ES0113307062) • BANKINTER, S.A. (ISIN: ES0113679I37) • BIOSEARCH, S.A. (ISIN: ES0172233118) • CAIXABANK, S.A. (ISIN: ES0140609019) • CELLNEX TELECOM, S.A. (ISIN: ES0105066007 • CIE AUTOMOTIVE, S.A. (ISIN: ES0105630315) https://www.fca.org.uk/news/news-stories/temporary-prohibition-short-selling/printable/print 1/5 11/13/2020 Temporary prohibition of short selling • COCA-COLA EUROPEAN P (ISIN: GB00BDCPN049) • CODERE S.A. (ISIN: ES0119256032) • COMPAÑIA DE DISTRIBUC (ISIN: ES0105027009) • CONSTRUCCIONES Y AUX (ISIN: ES0121975009) • ENAGAS,S.A. (ISIN: ES0130960018) • ENCE ENERGIA Y CELULO (ISIN: ES0130625512) • ENDESA,S.A. (ISIN: ES0130670112) • ERCROS (ISIN: ES0125140A14) • EUSKALTEL, S.A. (ISIN: ES0105075008) • FAES FARMA, S.A. -

Indra Sistemas S.A., Military SYSTEMS Systems and Border Militarization by Centre Delàs (Spain)

INDRA Indra Sistemas S.A., military SYSTEMS systems and border militarization By Centre Delàs (Spain) About the corporation INDRA Sistemas, military systems and border militarization Name: INDRA Sistemas, S.A. Address: Avda. Bruselas, 35, Alcobendas, Madrid Indra is one of the main military companies in Spain and Website: http://www.INDRAcompany.com/ one of Europe’s leading defence and security corpora- tions. 22% of INDRA’s activities are related to the de- Shareholder Structure 20161 fence and military sector with products such as weap- % of Share ons for warships, planes and other military vehicles as Shareholder Shares Capital Sociedad Estatal de 33.057.734 20.14% well as various surveillance and security products for Participaciones Industriales border management. Alba Participaciones, S.A. 18.587.155 11.32% FMR 16.642.000 10.14% Indra has a strong presence in lobby groups across T. Rowe Price Associates 5.294.295 3.23% Europe and is tightly affiliated with the Spanish gov- Schroders PLC 4.976.416 3.03% ernment (18.7% of its shares are owned by SEPI – a Other shareholders 85.574.939 52.14% Total 164.132.539 100.0% state owned corporation), and the corporation’s active lobbying has resulted in a number of projects On 31 December 2017, the main shareholders of the and contracts. Together with other transnational Parent company with an ownership interest of more than corporations (TNCs) in the defence industry, Indra 3% were: SEPI (18.7%), Alba Financial Corporation (10.5%), Fidelity Management & Research LLC (9.4%), T. Rowe played a role in drafting the strategic guidelines of the Price Associates (5.1%), Norges Bank (4.1%), Allianz Global European Security Research Program, among others. -

![Sectorwatch: IT Consulting February 2020 IT Consulting February 2020 Sector Dashboard [4]](https://docslib.b-cdn.net/cover/4577/sectorwatch-it-consulting-february-2020-it-consulting-february-2020-sector-dashboard-4-2204577.webp)

Sectorwatch: IT Consulting February 2020 IT Consulting February 2020 Sector Dashboard [4]

Sectorwatch: IT Consulting February 2020 IT Consulting February 2020 Sector Dashboard [4] Public Basket Performance [5] Operational Metrics [7] Valuation Comparison [10] Recent Deals [13] Appendix [15] 7 Mile Advisors appreciates the opportunity to present this confidential information to the Company. This document is meant to be delivered only in conjunction with a verbal presentation, and is not authorized for distribution. Please see the Confidentiality Notice & Disclaimer at the end of the document. All data cited in this document was believed to be accurate at the time of authorship and came from publicly available sources. Neither 7 Mile Advisors nor 7M Securities make warranties or representations as to the accuracy or completeness of third-party data contained herein. This document should be treated as confidential and for the use of the intended recipient only. Please notify 7 Mile Advisors if it was distributed in error. 2 Overview 7MA provides Investment Banking & Advisory Services to the Business Services and Technology Industries globally. We advise on M&A and private capital transactions, and provide market assessments and benchmarking. As a close knit team with a long history together and a laser focus on our target markets, we help our clients sell their companies, raise capital, grow through acquisitions, and evaluate new markets. We publish our sectorwatch, a review of M&A and operational trends in the industries we focus. Dashboard Valuation Comparison • Summary metrics on the sector • Graphical, detailed comparison of valuation • Commentary on market momentum by multiples for the public basket comparing the most recent 12-month performance against the last 3-year averages.