The New ACS Group Construction 1H/03 Revenues

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Corporate Governance Report

REPSOL S.A. 2019 Annual Corporate Governance Report Translation of a report originally issued in Spanish. In the event of a discrepancy, the Spanish language version prevails DETAILS OF ISSUER DETAILS OF ISSUER Dated end of year 31/12/2019 TAX REGISTRATION NUMBER: A-78375725 Name: Repsol, S.A. Registered office: C/ Méndez Álvaro, 44, Madrid 2 DETAILS OF ISSUER TABLE OF CONTENTS A. Executive summary ......................................................................................................................................................................... 4 1. Presentation by the Chairman of the Board of Directors .......................................................................................................... 4 2. At a glance .................................................................................................................................................................................. 5 3. The Board of Directors ............................................................................................................................................................... 9 4. Interaction with investors ........................................................................................................................................................ 12 B. The Repsol Corporate Governance System ................................................................................................................................... 15 1. Regulatory Framework ............................................................................................................................................................ -

Management Committee

CORPORATE GOVERNANCE A 105 MANAGEMENT COMMITTEE ÍÑIGO MEIRÁS CEO He is a Law graduate and holds an MBA from the Instituto de Empresa. He joined Ferrovial in 1992, was Mana- ging Director of Autopista del Sol and later on Toll Roads Director in Cintra until November 2000. Between 2000 and 2007 he headed the expansion of Ferrovial Services as Managing Director, later on as CEO, and in 2007 he was appointed CEO of Ferrovial Aeropuertos. He held the position of Group Managing Director of Ferrovial between April and October 2009, when he became CEO. MARÍA DIONIS JORGE GIL Managing Director of Human Resources CEO of Ferrovial Airports She holds a degree in Psychology from the Complu- He has a degree in Business and Law from ICADE tense University of Madrid and a Master’s in HR Mana- University. In 2010, he was appointed Director of gement from the University of Maryland. Before joining Finance and Capital Markets of Ferrovial. He began Ferrovial, she worked at Andersen Consulting, Watson his career at The Chase Manhattan Bank, where Wyatt, Soluziona and Getronics Iberia. She joined the he was part of the Corporate Finance and M&A company in 2006 as HR Development Director. In May divisions. In December 2012 he was named CEO of 2010, she became HR and Communications Director Ferrovial Airports. at Ferrovial Services. In June 2015 she became Group HR Director. ERNESTO LÓPEZ MOZO Finance Director ALEJANDRO DE LA JOYA He is a civil engineer (Polytechnical University of CEO of Ferrovial Agroman Madrid) and holds an MBA from The Wharton School He is a civil engineer who joined the company in 1991. -

Stock Market Reaction to Election Results: an Event Study Analysis

Facultat d’Economia i Empresa Memòria del Treball de Fi de Grau Stock Market reaction to Election Results: an Event Study Analysis Liliana Rebeca Dutra Duffy Grau de Administració d’Empreses Any acadèmic 2019-20 DNI de l’alumne: 41624155C Treball tutelat per Pau Balart Castro Departament d’Economia de l’empresa S'autoritza la Universitat a incloure aquest treball en el Repositori Autor Tutor Institucional per a la seva consulta en accés obert i difusió en línia, Sí No Sí No amb finalitats exclusivament acadèmiques i d'investigació Paraules clau del treball: Event study, shares, dummy variables, survey, regressions, abnormal returns... ABSTRACT The aim of this paper is to find the possible effect that estimation vote surveys have over the share prices of public companies listed in the Spanish stock market. To test this effect, we used the event study methodology. For the event study, daily data from 6 firms listed on the IBEX35 index are analyzed over the period of 1st January 2000 to 31st December 2015. Alongside the event study, another analysis has been conducted to test the economic literature that finds a positive relation between right-wing parties and the stock market. The results of this paper have not shown significant changes for the days surrounding the publication of estimation vote, known as event day. Although it can be observed a positive reaction to PP vote increases, confirming what the literature suggests. This indicates that the event indeed does affect the stock market depending on which party outcomes the other. The results also indicate that certain companies were more exposed to the political results than others. -

Acs, Servicios, Comunicaciones Y Energía, S.L

PROSPECTUS DATED 17 APRIL 2018 ACS, SERVICIOS, COMUNICACIONES Y ENERGÍA, S.L. (incorporated with limited liability in the Kingdom of Spain) €750,000,000 1.875 per cent. Green Notes due 2026 The issue price of the €750,000,000 1.875 per cent. Green Notes due 20 April 2026 (the Notes or the Green Notes) of ACS, Servicios, Comunicaciones y Energía, S.L. (the Issuer) is 99.435 per cent of their principal amount. Unless previously redeemed or cancelled, the Notes will be redeemed at their principal amount on 20 April 2026 (the Maturity Date). The Notes are subject to redemption in whole at their principal amount at the option of the Issuer at any time in the event of certain changes affecting taxation in the Kingdom of Spain. See “Terms and Conditions of the Notes—Redemption and Purchase”. In addition, if a Change of Control occurs and, during the Change of Control Period, a Rating Downgrade occurs, then each Noteholder may require the Issuer to redeem or, at the Issuer's option, purchase in whole or in part its Notes at their principal amount plus accrued and unpaid interest up to (but excluding) the date for such redemption or purchase, all as more fully set out under “Terms and Conditions of the Notes—Redemption and Purchase – Change of Control”. The Notes are subject to redemption in whole at their principal amount together with any accrued and unpaid interest up to (but excluding) the date fixed for such redemption which shall be no earlier than three months before the Maturity Date, as more fully set out under “Terms and Conditions of the Notes— Redemption and Purchase – Residual Maturity Call Option”. -

Hechos Relevantes

Hechos Relevantes Palacio de la Bolsa Plaza de la Lealtad, 1 28014 Madrid Tel.: +34 91 709 58 10 Fax: +34 91 709 53 96 [email protected] HECHOS RELEVANTES Información en tiempo real a través de la BME Data Feed y en un formato estandarizado de los Hechos Relevantes y otra información financiera remitida por los emisores a la CNMV. El servicio incluye la información en castellano que se difunde a través de la CNMV así como la información en inglés de aquellas entidades emisoras que formen parte de la red de contribuidores de este servicio. DESCRIPCION DE PRODUCTO Los clientes de Hechos Relevantes recibirán en tiempo real un mensaje con el titular/resumen del Hecho Relevante y un enlace a la documentación proporcionada por la entidad emisora. El producto ofrece la siguiente información: • Nombre de la emisora • Código ISIN de la emisora • NIF de la emisora • Hecho Relevante comunicado por la emisora (PDF, XBRL…) • Tipología de Hecho Relevante (únicamente para servicio en español) El producto se ofrece en español y en inglés (en este idioma, únicamente con la cobertura que se indica en la sección “red de contribuidores”). BENEFICIOS Punto único de información VENDORS del mercado español Estandarización FONDOS DE INVERSIÓN Información completa del FEED Hecho Relevante Tiempo Real BANCOS Rapidez “Hechos Disponibilidad de la Relevantes” MEDIOS DE COMUNICACIÓN información en inglés Servicio PUSH EMISORES OTROS 2 TIPOS DE HECHOS RELEVANTES 3 RED DE CONTRIBUIDORES (a 1 de diciembre de 2015) Hechos Relevantes en inglés IBEX 35® IBEX -

Tecnicas Reunidas

Tecnicas Reunidas Spain/ Oil Services Post results note Investment Research 11 NOVEMBER 2016 Accumulate Resultados del 3T16, en línea con lo estimado. Recommendation unchanged La noticia: Técnicas Reunidas presentó ayer los resultados del 3T16. Share price: EUR 33.75 closing price as of 10/11/2016 Nuestro análisis: Los resultados han estado en línea con lo estimado. Target price: EUR 36.00 TECNICAS REUNIDAS : 9M16 RESULTS Target Price unchanged 9M15 %sles 9M16 %sles %y/y 2Q16 3Q15 3Q16 Sales 3,006.0 100% 3,437.9 100% 14.4% 1,252.6 1,122.4 1,134.0 Reuters/Bloomberg TRE.MC/TRE SM EBITDA 159.2 5.3% 154.1 4.5% -3.2% 55.4 56.6 51.6 Daily avg. no. trad. sh. 12 mth 480 Depreciation -11.6 -0.4% -15.2 -0.4% 31.0% -5.2 -4.0 -5.0 Daily avg. trad. vol. 12 mth (m) 20,834.07 EBIT 147.6 4.9% 138.9 4.0% -5.9% 50.3 52.6 46.5 Price high 12 mth (EUR) 38.31 Financial results 4.2 0.1% -1.1 0.0% -1.4 1.0 3.2 Price low 12 mth (EUR) 21.75 EBT 151.8 5.0% 137.8 4.0% -9.2% 48.8 51.4 48.2 Abs. perf. 1 mth -6.2% Income tax -36.6 -1.2% -36.5 -1.1% -0.3% -13.2 -11.3 -12.7 Abs. perf. 3 mth 6.2% Net profit 115.2 3.8% 101.3 2.9% -12.1% 35.7 40.1 35.4 Abs. -

Iron, Steel & Metals

Hidroambiente S.A.U. Calle Mayor, 23 E, 1º 48930 Getxo (SPAIN) T: +34 94 480 40 90 - F: +34 94 480 30 76 [email protected] Hidroambiente S.A.U. Rio Rhin 56 - 6ª Planta Colonia Cuauhtemoc 06500 CDMX (MEXICO) T: +52 55 6811-6556 / +52 55 6732-1809 [email protected] | water treatment plants | Everblue Private Ltd. B-402, Ganga Osian Square, Near LG Showroom, Mankar Chawk, Wakad, Pune 411057 (INDIA) T: +91 20 6473 1585 IRON, STEEL METALS [email protected] & www.hidroambiente.es Hidroambiente, within the Elecnor Group, was This commitment is possible thanks to a very founded in 1993 to deliver Water Treatment experienced innovation-committed highly- solutions to highly demanding customers skilled staff. from the industrial and public sector. Our long-standing experience, our countless We strive to meet our customers’ satisfaction references and our prestige in the market by addressing every stage in a water treatment together with the importance of our customers project, i.e. Design, Construction, Assembly, encourage us to go on with this strategy. Commissioning, Operation & Maintenance and Technical Assistance. n Services 1 n Manufacturing of “Turn Key” Water Treatment Plants n Equipment Manufacturing n Supply of Materials n “In House” Construction and Assembly n Start-up Service n Technological Adjustment and Upgrading n Transfers and Revamping Before undertaking any Investment: n Basic Engineering Solutions n Detail Engineering n Technical Assessment on the Design of New Plants n Water Networks Audits and Solutions n Water Treatment Plants 2 Technologies: n Freshwater from Rivers and Lakes. Settler Tanks, Flotation Systems and Sand Filters n Freshwater from Wells and Reservoirs. -

Forty Years of Democratic Spain: Political, Economic, Foreign Policy

Working Paper Documento de Trabajo Forty years of democratic Spain Political, economic, foreign policy and social change, 1978-2018 William Chislett Working Paper 01/2018 | October 2018 Sponsored by Bussiness Advisory Council With the collaboration of Forty years of democratic Spain Political, economic, foreign policy and social change, 1978-2018 William Chislett - Real Instituto Elcano - October 2018 Real Instituto Elcano - Madrid - España www.realinstitutoelcano.org © 2018 Real Instituto Elcano C/ Príncipe de Vergara, 51 28006 Madrid www.realinstitutoelcano.org ISSN: 1699-3504 Depósito Legal: M-26708-2005 Working Paper Forty years of democratic Spain Political, economic, foreign policy and social change, 1978-2018 William Chislett Summary 1. Background 2. Political scene: a new mould 3. Autonomous communities: unfinished business 4. The discord in Catalonia: no end in sight 5. Economy: transformed but vulnerable 6. Labour market: haves and have-nots 7. Exports: surprising success 8. Direct investment abroad: the forging of multinationals 9. Banks: from a cosy club to tough competition 10. Foreign policy: from isolation to full integration 11. Migration: from a net exporter to a net importer of people 12. Social change: a new world 13. Conclusion: the next 40 years Appendix Bibliography Working Paper Forty years of democratic Spain Spain: Autonomous Communities Real Instituto Elcano - 2018 page | 5 Working Paper Forty years of democratic Spain Summary1 Whichever way one looks at it, Spain has been profoundly transformed since the 1978 -

Diapositiva 1

WHY ACS? January 10th, 2017 Building the world of tomorrow 7th Spain Investors Day Why ACS is an attractive investment? 1. A global leading contractor 2. Highly diversified in terms of activities and geographies 3. Resilient operating performance 4. Sustainable growth potential 5. Successful transformation process completed 6. Trading at reasonable prices 2 1. A global leading contractor… US & Canada market share(1) US & CAN total construction output $ 891br → top contractors revenues represent 8% Others ACS 21% 18% st Obayashi 1 3% Lendlease 4% Fluor 14% Jacobs 4% Bouygues Skanska 5% 9% Balfour Beatty 6% Tutor Perini BECHTEL 7% 9% ASIA PACIFIC* market share(1) Vinci Others Chinese companies 3% 5% Shimizu excluded Bouygues 17% 3% BECHTEL 13% Taisei 16% Hyundai (1) Market share: from total revenues of top contractors in the region 13% Obayashi TOP 1 INTERNATIONAL 16% Source: ENR, bloomberg, companies’ reports, internal analysis ACS CONTRACTOR 14% 3 2. Highly diversified in terms of activities and geographies North America Europe Asia Pacific 46% 22% 25% 6% 14.6 €bn 6.8 €bn 7.9 €bn 2% 3% 1% 38% 8% R 1% 5% 13% South America Africa 6% 1% 15% 1.8 €bn 0.3 €bn 1% 1% R 4% NOTE: Sales distribution excluding recent disposals of Urbaser & Sintax LTM sales as of Sep 16 4 2. Highly diversified in terms of activities and geographies Facility management EPC 5% 9% Construction Support 75% Services 11% 32% Civil Works Contract mining 5% Industrial Services 20% 38% Environment Building 5% NOTE: Sales distribution excluding recent disposals of Urbaser & Sintax 9M16 Sales. -

2019 Sustainability Committee Activity Report

Translation of the original in Spanish. In case of any discrepancy, the Spanish version prevails. SUSTAINABILITY COMMITTEE OF THE BOARD OF DIRECTORS OF REPSOL, S.A. 2019 ACTIVITIES REPORT _____________________________________ TABLE OF CONTENTS 1. BACKGROUND 2. COMPOSITION 3. REGULATION OF THE SUSTAINABILITY COMMITTEE 4. FUNCTIONING 5. COMMITTEE RESOURCES 6. MAIN ACTIVITIES DEVELOPED DURING 2019 6.1. Activities related to the environment and safety 6.2. Activities related to sustainability 6.3. Activities related to the non-financial risk management and control 6.4. Activities related to the expectations of the different stakeholders and the Company’s positioning on sustainability 6.5. Assessment of the functioning of the Sustainability Committee APPENDIX: Schedule of meetings held in 2019 1 Translation of the original in Spanish. In case of any discrepancy, the Spanish version prevails. 1. BACKGROUND In its meeting of May 27, 2015, in the framework of the assessment of its organisation and functioning conducted with external advice, the Board of Directors resolved to create the Sustainability Committee of the Board of Directors of Repsol, S.A., replacing the former Strategy, Investments and Corporate Social Responsibility Committee. The establishment of this type of specialist Committee within the Board of Directors is envisaged in Recommendation 52 of the Spanish National Securities Market Commission's Good Governance Code for Listed Companies and in article 37 of Repsol’s Articles of Association. In this regard, pursuant to article 32 of the Board Regulations, this body can create specialist committees within it, with oversight, reporting, advisory and proposal functions, as well as the others that the law, the Articles of Association or those Regulations attribute it in the scope of its competences to facilitate decision-making by means of prior studies and to strengthen the objectivity and reflection guarantees with which the Board must address certain issues. -

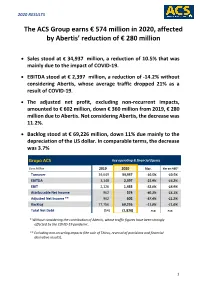

The ACS Group Earns € 574 Million in 2020, Affected by Abertis' Reduction

2020 RESULTS The ACS Group earns € 574 million in 2020, affected by Abertis’ reduction of € 280 million Sales stood at € 34,937 million, a reduction of 10.5% that was mainly due to the impact of COVID-19. EBITDA stood at € 2,397 million, a reduction of -14.2% without considering Abertis, whose average traffic dropped 21% as a result of COVID-19. The adjusted net profit, excluding non-recurrent impacts, amounted to € 602 million, down € 360 million from 2019, € 280 million due to Abertis. Not considering Abertis, the decrease was 11.2%. Backlog stood at € 69,226 million, down 11% due mainly to the depreciation of the US dollar. In comparable terms, the decrease was 3.7% Grupo ACS Key operating & financial figures Euro Million 2019 2020 Var. Var ex-ABE* Turnover 39,049 34,937 -10.5% -10.5% EBITDA 3,148 2,397 -23.9% -14.2% EBIT 2,126 1,433 -32.6% -18.9% Attributable Net Income 962 574 -40.3% -15.1% Adjusted Net Income ** 962 602 -37.4% -11.2% Backlog 77,756 69,226 -11.0% -11.0% Total Net Debt (54) (1,820) n.a. n.a. * Without considering the contribution of Abertis, whose traffic figures have been strongly affected by the COVID-19 pandemic. ** Excluding non-recurring impacts (the sale of Thiess, reversal of provisions and financial derivative results). 1 2020 RESULTS 1. Consolidated Results The Group’s 2020 ordinary net profit accounted for € 602 million, € 360 million less than the previous year. This decline is mainly due to the evolution of Abertis, whose traffic was heavily affected by the lockdown measures related to COVID- 19, reducing its contribution by € 280 million. -

Ferrovial Awarded Contract to Underground Madrid's M-30 Beltway in the Environs of the Former Calderón Stadium

CONTRACTS, SPAIN, CONSTRUCTION Ferrovial awarded contract to underground Madrid's M-30 beltway in the environs of the former Calderón stadium • Madrid City Government has awarded the contract to a joint venture of Ferrovial and Acciona • The work consists of undergrounding a section of Madrid's Calle 30 as part of the “Nuevo Mahou- Calderón” project in order to enhance mobility and accessibility in the area • Work is scheduled to commence on September and to be completed in 20 months. Madrid, 07/07/2021.- Ferrovial, via its construction subsidiary, has been awarded the contract to Corporate underground Madrid's M-30 beltway in the vicinity of the Calderón stadium. The project is intended to Communications provide continuity to the Calle 30 tunnel, as this is the only segment of the southern arc of the road that is newsroom.ferrovial.com still overground, since it ran below the western stand of the Vicente Calderón stadium. It will be carried out @ferrovial in a joint venture with Acciona. The project will also expand the “Madrid Río” park by eliminating this section of overground highway, which is a barrier to mobility. North America Mari Pillar The work consists of building a cut-and-cover tunnel 620 meters long with a width varying from 26 meters +1 832 829 6597 at its southern end to slightly over 21 meters at its northern end. [email protected] Europe The new infrastructure will have all the facilities and services required to operate it and integrate with the Paula Lacruz adjoining sections of Calle 30; the tunnel roof is designed to accommodate bushes and trees to create a +34 91 586 25 26 new green area linked to the “Madrid Río” park.