Financial Stability Report 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SC13-2384 Exhibit D (Lavalle)

EXHIBIT D REPORT ON NYE LAVALLE’S INVESTIGATIONS, RESEARCH BACKGROUND, BONA FIDES, EXPERTISE, & EXPERIENCE IN PREDATORY MORTGAGE SECURITIZATION, SERVICING, FORECLOSURE & ROBO-SIGNING PRACTICES INTRODUCTION 1. My name is Aneurin Adlai Lavalle. I am most commonly referred to as Nye Lavalle. I am a resident of the State of Florida. 2. I provide this report based upon facts and information personally known by me and to me and gathered from my research and investigation over a period of more than twenty-years. 3. I have a research background and as a consumer and shareholder advocate, I have developed a series of skills, procedures, and protocols over 20-years that has led me to be an expert in predatory mortgage securitization, servicing, and foreclosure fraud issues with a specialty in robo-signing.1 4. I have been accepted by Courts as an expert in matters relating to predatory mortgage securitization, servicing, and foreclosure fraud issues. 5. My findings, analyses, opinions, and many of my protocols, opinions, and conclusions have been reviewed, corroborated, and adopted by state and Federal regulatory agencies such as the Federal Reserve, Office of Comptroller of the Currency; Federal Deposit Insurance Corporation, Federal Housing Financing Agency, U.S. Attorney General and Attorneys General from all 50 states, FILED, 02/04/2015 12:11 am, JOHN A. TOMASINO, CLERK, SUPREME COURT including Florida, but especially by those in New York, Delaware, Nevada, and California. 1 http://en.wikipedia.org/wiki/Nye_Lavalle 1 6. In addition, numerous state and federal courts, including the Supreme and highest courts of the states of Massachusetts,2 Maryland,3 and Kansas4 have agreed with some of my opinions, findings, conclusions, and analyses I have developed over the last twenty-years. -

Housing and the Financial Crisis

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Housing and the Financial Crisis Volume Author/Editor: Edward L. Glaeser and Todd Sinai, editors Volume Publisher: University of Chicago Press Volume ISBN: 978-0-226-03058-6 Volume URL: http://www.nber.org/books/glae11-1 Conference Date: November 17-18, 2011 Publication Date: August 2013 Chapter Title: The Future of the Government-Sponsored Enterprises: The Role for Government in the U.S. Mortgage Market Chapter Author(s): Dwight Jaffee, John M. Quigley Chapter URL: http://www.nber.org/chapters/c12625 Chapter pages in book: (p. 361 - 417) 8 The Future of the Government- Sponsored Enterprises The Role for Government in the US Mortgage Market Dwight Jaffee and John M. Quigley 8.1 Introduction The two large government- sponsored housing enterprises (GSEs),1 the Federal National Mortgage Association (“Fannie Mae”) and the Federal Home Loan Mortgage Corporation (“Freddie Mac”), evolved over three- quarters of a century from a single small government agency, to a large and powerful duopoly, and ultimately to insolvent institutions protected from bankruptcy only by the full faith and credit of the US government. From the beginning of 2008 to the end of 2011, the two GSEs lost capital of $266 billion, requiring draws of $188 billion under the Treasured Preferred Stock Purchase Agreements to remain in operation; see Federal Housing Finance Agency (2011). This downfall of the two GSEs was primarily a question of “when,” not “if,” given that their structure as a public/private Dwight Jaffee is the Willis Booth Professor of Banking, Finance, and Real Estate at the University of California, Berkeley. -

Primers Federal Home Loan Banks Feb. 8, 2021

The NAIC’s Capital Markets Bureau monitors developments in the capital markets globally and analyzes their potential impact on the investment portfolios of U.S. insurance companies. Please see the Capital Markets Bureau website at INDEX. Federal Home Loan Banks Analyst: Jennifer Johnson Executive Summary • The Federal Home Loan Bank (FHLB) system was established in 1932 for the purpose of providing liquidity and transparency to the capital markets. • It is comprised of 11 regional banks that are government-sponsored entities (GSEs) and support the market for homes. These FHLB regional banks provide low-cost financing to member financial institutions, which in turn make loans to individuals. • Each FHLB regional bank is structured as a cooperative of mortgage lenders, or members, which sets its credit standards and lending policies. To become a member, a financial institution must purchase shares of the regional bank. • FHLB regional bank members may apply for a loan or “advance” based on required credit limits and borrowing capacity. Each loan or advance is secured by eligible collateral, and lending capacity is based on applicable discount rates on the eligible collateral. The more liquid and easily valued the collateral, the lower the discount rate. • Eligible collateral may include U.S. government or government agency securities; residential mortgage loans; residential mortgage-backed securities (RMBS); multifamily mortgage loans; cash; deposits in an FHLB regional bank; and other real estate-related assets such as commercial What is thereal FHLB estate? loans. • U.S. insurers interact with the FHLB system via borrowing, investing in FHLB debt and owning stock in FHLB regional banks. -

Financial Crises and Policy Responses

Financial Crises and Policy Responses A MARKET-BASED VIEW FROM THE SHADOW FINANCIAL REGULATORY COMMITTEE, 1986–2015 ROBERT LITAN NOVEMBER 2016 AMERICAN ENTERPRISE INSTITUTE Financial Crises and Policy Responses A MARKET-BASED VIEW FROM THE SHADOW FINANCIAL REGULATORY COMMITTEE, 1986–2015 ROBERT LITAN NOVEMBER 2016 AMERICAN ENTERPRISE INSTITUTE © 2016 by the American Enterprise Institute. All rights reserved. The American Enterprise Institute (AEI) is a nonpartisan, nonprofit, 501(c)(3) educational organization and does not take institutional posi- tions on any issues. The views expressed here are those of the author(s). Table of Contents Preface ................................................................................................................................................................................... v I. Financial Crises and Challenges: The Origins of the Shadow Financial Regulatory Committee ..... 1 II. A Brief 30-Year History of Finance ..................................................................................................................... 5 III. The S&L Crises of the 1980s ................................................................................................................................. 7 IV. The Banking Crises of the 1980s and Policy Responses .............................................................................. 11 V. Deposit Insurance and Safety-Net Reform .................................................................................................... 17 VI. Banking Regulation -

Elizabeth a Duke: a Framework for Analyzing Bank Lending

Elizabeth A Duke: A framework for analyzing bank lending Speech by Ms Elizabeth A Duke, Member of the Board of Governors of the US Federal Reserve System, at the 13th Annual University of North Carolina Banking Institute, Charlotte, North Carolina, 30 March 2009. The original speech, which contains figures and various links to the documents mentioned, can be found on the US Federal Reserve System’s website. * * * In August 2008 I joined the Board of Governors of the Federal Reserve System, leaving behind a 30-year career as a commercial banker to become a central banker. My time as a commercial banker spanned numerous business cycles. It also encompassed at least one severe financial system crisis, in the late 1980s through the early 1990s, albeit one that was not as severe as the current one. From my time as a commercial banker, I already understood the factors considered by bankers in the initial lending decision as well as those in loss mitigation when collecting those same loans. As a central banker, I have come to appreciate even more fully the role of credit in our economic well-being. So I thought it would be appropriate for me to provide my perspective on credit conditions in our economy and the current crisis. Today, I would like to discuss a three-dimensional view of the flow of credit to households and businesses and describe the evolving role of banks in the U.S. economy. I will begin by taking a look at recent trends in aggregate borrowing by households and by the nonfinancial business sector. -

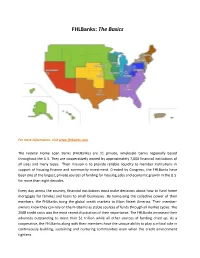

Fhlbanks: the Basics

FHLBanks: The Basics For more information, visit www.fhlbanks.com. The Federal Home Loan Banks (FHLBanks) are 11 private, wholesale banks regionally based throughout the U.S. They are cooperatively owned by approximately 7,000 financial institutions of all sizes and many types. Their mission is to provide reliable liquidity to member institutions in support of housing finance and community investment. Created by Congress, the FHLBanks have been one of the largest, private sources of funding for housing, jobs and economic growth in the U.S. for more than eight decades. Every day across the country, financial institutions must make decisions about how to fund home mortgages for families and loans to small businesses. By harnessing the collective power of their members, the FHLBanks bring the global credit markets to Main Street America. Their member- owners know they can rely on the FHLBanks as stable sources of funds through all market cycles. The 2008 credit crisis was the most recent illustration of their importance. The FHLBanks increased their advances outstanding to more than $1 trillion while all other sources of funding dried up. As a cooperative, the FHLBanks along with their members have the unique ability to play a critical role in continuously building, sustaining and nurturing communities even when the credit environment tightens. 2 FHLBanks are regionally focused and controlled. This structure allows each FHLBank to be responsive to the specific community credit needs in its geography. At the same time, the FHLBanks collectively use their combined size and strength to obtain funding at the lowest possible cost for their members. -

Recent Trends in Federal Home Loan Bank Advances to Jpmorgan Chase and Other Large Banks

Federal Housing Finance Agency Office of Inspector General Recent Trends in Federal Home Loan Bank Advances to JPMorgan Chase and Other Large Banks Evaluation Report EVL-2014-006 April 16, 2014 Recent Trends in Federal Home Loan Bank Advances to JPMorgan Chase and Other Large Banks Why OIG Did This Report The Federal Home Loan Bank System (System) is comprised of 12 regional Federal Home Loan Banks (FHLBanks) and the Office of Finance. The FHLBanks make secured loans, known as advances, to their members and do At A so primarily to promote housing finance. After peaking at about $1 trillion in 2008, advances declined 62% to $381 billion by March 2012. However, since Glance then, advances have climbed to nearly $500 billion primarily due to advances to the four largest members of the System: JPMorgan Chase, Bank of ——— America, Citigroup, and Wells Fargo. From March 31, 2012, to December 31, 2013, advances to these four System members surged by 158% to $135 billion. April 16, 2014 This report identifies potential causes for the surge in advances to the four largest members, identifies the associated benefits and risks, and assesses the Federal Housing Finance Agency’s (FHFA/Agency) oversight of this area. OIG Analysis and Finding New Bank Liquidity Standards Contributed to the Recent Surge in Advances According to officials from FHFA and an FHLBank as well as Agency documents, the surge in advances to the four largest members is attributable, in large part, to bank liquidity standards established by the international Basel Committee on Bank Supervision in December 2010. Under these standards, banks, such as JPMorgan Chase, must increase their holdings of high quality liquid assets, such as U.S. -

The Complete Idiot's Guide to Starting an Ebay Business, Second Edition

Starting an eBay Business Second Edition by Barbara Weltman and Malcolm Katt A member of Penguin Group (USA) Inc. Starting an eBay Business Second Edition by Barbara Weltman and Malcolm Katt A member of Penguin Group (USA) Inc. This book is dedicated to all the eBay sellers, present and future, who prove that the entrepreneurial spirit is indomitable. ALPHA BOOKS Published by the Penguin Group Penguin Group (USA) Inc., 375 Hudson Street, New York, New York 10014, USA Penguin Group (Canada), 90 Eglinton Avenue East, Suite 700, Toronto, Ontario M4P 2Y3, Canada (a division of Pearson Penguin Canada Inc.) Penguin Books Ltd, 80 Strand, London WC2R 0RL, England Penguin Ireland, 25 St. Stephen’s Green, Dublin 2, Ireland (a division of Penguin Books Ltd.) Penguin Group (Australia), 250 Camberwell Road, Camberwell, Victoria 3124, Australia (a division of Pearson Australia Group Pty. Ltd.) Penguin Books India Pvt. Ltd., 11 Community Centre, Panchsheel Park, New Delhi—110 017, India Penguin Group (NZ), 67 Apollo Drive, Rosedale, North Shore, Auckland 1311, New Zealand (a division of Pearson New Zealand Ltd.) Penguin Books (South Africa) (Pty.) Ltd, 24 Sturdee Avenue, Rosebank, Johannesburg 2196, South Africa Penguin Books Ltd., Registered Offices: 80 Strand, London WC2R 0RL, England Copyright © 2008 by Barbara Weltman and Malcolm Katt All rights reserved. No part of this book shall be reproduced, stored in a retrieval system, or transmitted by any means, electronic, mechanical, photocopying, recording, or otherwise, without written permission from the pub- lisher. No patent liability is assumed with respect to the use of the information contained herein. Although every precaution has been taken in the preparation of this book, the publisher and authors assume no responsibility for errors or omissions. -

New Developments in Clearing and Settlement Arrangements for OTC Derivatives

Committee on Payment and Settlement Systems New developments in clearing and settlement arrangements for OTC derivatives March 2007 Copies of publications are available from: Bank for International Settlements Press & Communications CH-4002 Basel, Switzerland E-mail: [email protected] Fax: +41 61 280 9100 and +41 61 280 8100 This publication is available on the BIS website (www.bis.org). © Bank for International Settlements 2007. All rights reserved. Brief excerpts may be reproduced or translated provided the source is cited. ISBN 92-9131-738-1 (print) ISBN 92-9197-738-1 (online) Foreword Since the publication by the BIS in 1998 of a report on OTC derivatives: settlement procedures and counterparty risk management, the markets for OTC derivatives have continued to expand and develop rapidly, while risk management practices have evolved and significant changes in market infrastructures have occurred. In early 2006, the CPSS set up a Working Group, comprising representatives of its member central banks and prudential supervisors of major derivatives dealers, to analyse existing arrangements and risk management practices in the broader OTC derivatives market and evaluate the potential for risks to be mitigated by greater use of, and enhancements to, market infrastructure. This project complemented an earlier supervisory initiative that at the time was focused primarily on confirmation backlogs in the credit derivatives markets. The Working Group conducted interviews with some 35 major dealers in OTC derivatives in the G10 countries and Hong Kong SAR. It also met with industry groups and providers of post-trade processing services. Finally, upon completion of the report, it discussed its findings in a roundtable with these entities. -

Vol. 83 Wednesday, No. 60 March 28, 2018 Pages 13183–13374

Vol. 83 Wednesday, No. 60 March 28, 2018 Pages 13183–13374 OFFICE OF THE FEDERAL REGISTER VerDate Sep 11 2014 22:04 Mar 27, 2018 Jkt 244001 PO 00000 Frm 00001 Fmt 4710 Sfmt 4710 E:\FR\FM\28MRWS.LOC 28MRWS amozie on DSK30RV082PROD with FRONT MATTER WS II Federal Register / Vol. 83, No. 60 / Wednesday, March 28, 2018 The FEDERAL REGISTER (ISSN 0097–6326) is published daily, SUBSCRIPTIONS AND COPIES Monday through Friday, except official holidays, by the Office PUBLIC of the Federal Register, National Archives and Records Administration, Washington, DC 20408, under the Federal Register Subscriptions: Act (44 U.S.C. Ch. 15) and the regulations of the Administrative Paper or fiche 202–512–1800 Committee of the Federal Register (1 CFR Ch. I). The Assistance with public subscriptions 202–512–1806 Superintendent of Documents, U.S. Government Publishing Office, Washington, DC 20402 is the exclusive distributor of the official General online information 202–512–1530; 1–888–293–6498 edition. Periodicals postage is paid at Washington, DC. Single copies/back copies: The FEDERAL REGISTER provides a uniform system for making Paper or fiche 202–512–1800 available to the public regulations and legal notices issued by Assistance with public single copies 1–866–512–1800 Federal agencies. These include Presidential proclamations and (Toll-Free) Executive Orders, Federal agency documents having general FEDERAL AGENCIES applicability and legal effect, documents required to be published Subscriptions: by act of Congress, and other Federal agency documents of public interest. Assistance with Federal agency subscriptions: Documents are on file for public inspection in the Office of the Email [email protected] Federal Register the day before they are published, unless the Phone 202–741–6000 issuing agency requests earlier filing. -

Justin Bio Handout 2020-01-21

Justin S. Weddle Founder 212-997-5518 [email protected] Justin Weddle is a skilled trial lawyer, litigation strategist, counselor, and Education appellate advocate. When the stakes are high, clients rely on his tenacity Columbia University School of Law, J.D. 1995 Managing Editor, Columbia Law Review and incisive analysis for tailor-made strategies and solutions in both Kent Scholar, Stone Scholar domestic and cross-border criminal, civil, and regulatory matters. As a Haverford College, B.A. 1992 result, Justin Weddle is a regular participant in the highest-profile Bar Admissions investigations, trials, and appeals, such as: New York Massachusetts LIBOR criminal cases U.S. District Courts: Southern District of New York, Eastern District of New York, and The FIFA corruption case District of Massachusetts U.S. Courts of Appeals: First, Second, Third, Circuit Court cases on SEC disgorgement and ALJ appointment issues Tenth, Eleventh, and D.C. Circuits U.S. Supreme Court U.S. investigation and litigation relating to Brazil’s Lava Jato Recognitions investigation Recognized by Super Lawyers as a Top Rated The Supreme Court Lucia decision rejecting the SEC’s ALJs as White Collar Crimes Attorney in New York, NY, since 2017 unconstitutional Listed in Who’s Who Legal, Business Crime Defense for both Corporates and The KPMG-PCAOB leaks criminal jury trial in the Southern District of Individuals New York Professional Activities Justin prosecuted white collar crime for more than 12 years as an Assistant Chair of the Appeals Subcommittee NYC Bar Association Federal Courts United States Attorney in the Southern District of New York, building and Committee trying complex fraud cases. -

ISDA Fpml Survey January 2011

ISDA FpML Survey January 2011 ISDA® INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION, INC. INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION ISDA, which represents participants in the privately negotiated derivatives industry, is among the world’s largest global financial trade associations as measured by number of member firms. ISDA was chartered in 1985, and today has over 800 member institutions from 54 countries on six continents. These members include most of the world’s major institutions that deal in privately negotiated derivatives, as well as many of the businesses, governmental entities and other end users that rely on over-the-counter derivatives to manage efficiently the financial market risks inherent in their core economic activities. Since its inception, ISDA has pioneered efforts to identify and reduce the sources of risk in the derivatives and risk management business. Among its most notable accomplishments are: developing the ISDA Master Agreement; publishing a wide range of related documentation materials and instruments covering a variety of transaction types; producing legal opinions on the enforceability of netting and collateral arrangements (available only to ISDA members); securing recognition of the risk-reducing effects of netting in determining capital requirements; promoting sound risk management practices, and advancing the understanding and treatment of derivatives and risk management from public policy and regulatory capital perspectives. About FpML FpML (Financial products Markup Language) is the freely licensed business information exchange standard for electronic dealing and processing of privately negotiated derivatives and structured products. It establishes the industry protocol for sharing information on, and dealing in, financial derivatives and structured products over the Internet. FpML is based on XML (Extensible Markup Language), the standard meta-language for describing data shared between applications.