Finance Project

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Developing Employees As Organisational Assets

Developing Employees as Organisational Assets INTRODUCTION The Kingfisher Recruitment • The Person Specification How KMDS is evolving commercial and afterwards in key functions The Group requires from prospec- Kingfisher plc is one of Europe’s leading retailers based Management Development Scheme Investing in a trainee over ten years tive KMDS trainees: The KMDS was launched in 1995 and • a post-graduate certificate in man- around three main sectors - DIY, electrical and general involves significant cost as well as today has 172 individuals on the scheme agement studies from Templeton • excellent interpersonal skills merchandise. The company employs over 130,000 people in invest- risk. The risk includes choosing the working across the Group. All individu- College, Oxford The KMDS represents a key • enthusiasm and drive to become ment by the organisation in its human wrong type of person and equally als following the KMDS route joined in • a ‘skills tool-box’ consisting of 2,900 stores across 15 countries and has some of the best senior managers within 7-10 years assets. The scheme takes high-poten- importantly losing the person to anoth- their early 20s. Recently Kingfisher has day-release training to develop per- known retail brands in Europe, including B&Q, Castorama, • innovative approach to challenges tial graduates who want to make a er organisation during the training recognised that there are benefits in sonal skills Comet, Darty, BUT, Woolworths and Superdrug among opening up the process to existing high- career in retail, and provides them with process. For this reason, Kingfisher • the ability to analyse and make • a ‘buddy’ who is already on the others. -

Iurc Public's Exhibit No. 1

FILED March 2, 2020 INDIANA UTILITY REGULATORY COMMISSION STATE OF INDIANA INDIANA UTILITY REGULATORY COMMISSION PETITION OF DUKE ENERGY INDIANA, LLC FOR ) OFFICIAL (1) APPROVAL OF ITS PROPOSED PLAN FOR ) DEMAND SIDE MANAGEMENT AND ENERGY ) EXHIBITS EFFICIENCY PROGRAMS FOR 2020-2023; (2) ) AUTHORITY TO RECOVER ALL PROGRAM COSTS, ) INCLUDING LOST REVENUES AND FINANCIAL ) INCENTIVES IN ACCORDANCE WITH IN. CODE §§ ) 8-1-8.5-3, 8-1-8.5-10, 8-l-2-42(A)AND PURSUANT TO ) CAUSE NO. 43955 170 IAC 4-8-5 AND 170 IAC 4-8-6; (30 AUTHORITY TO ) DSM-08 DEFER ALL SUCH COSTS INCURRED UNTIL SUCH ) TIME THEY ARE REFLECTED IN RETAIL RATES; ) (4) REVISIONS TO STANDARD CONTRACT RIDER ) IURC 66A; AND (5) INTERIM AUTHORITY TO CONTINUE ) PUBLIC'S OFFERING ITS CURRENT DEMAND SIDE MANAGEMENT AND ENERGY EFFICIENCY ) ~IW:O.- -o2D ·/ A I ~ PROGRAMS UNTIL A FINAL ORDER IS ISSUED IN ) 0Al£ REPORTER THIS CAUSE. ) INDIANA OFFICE OF UTILITY CONSUMER COUNSELOR PUBLIC'S EXHIBIT NO.1 PUBLIC (REDACTED) TESTIMONY OF OUCC WITNESS JOHN E. HASELDEN March 2, 2020 ~~L~ Je frey M. Reed -; V 1 Attorney No. 11651-49 Deputy Consumer Counselor Public's Exhibit No. 1 Cause No. 43955 DSM 8 Page 1 of35 TESTIMONY OF OUCC WITNESS JOHN E. HASELDEN CAUSE NO. 43955 DSM 8 DUKE ENERGY INDIANA, LLC I. INTRODUCTION 1 Q: Please state your name, business address, and employment capacity. 2 A: My name is John E. Haselden. My business address is 115 West Washington Street, 3 Suite 1500 South, Indianapolis, Indiana 46204. I am a Senior Utility Analyst in the 4 Electric Division of the Indiana Office of Utility Consumer Counselor ("OUCC"). -

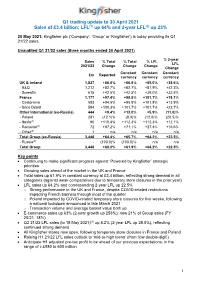

Q1 Trading Update to 30 April 2021 Sales of £3.4 Billion; LFL(1) up 64% and 2-Year LFL(2) up 23%

Q1 trading update to 30 April 2021 Sales of £3.4 billion; LFL(1) up 64% and 2-year LFL(2) up 23% 20 May 2021: Kingfisher plc (‘Company’, ‘Group’ or ‘Kingfisher’) is today providing its Q1 21/22 sales. Unaudited Q1 21/22 sales (three months ended 30 April 2021) % 2-year Sales % Total % Total % LFL LFL 2021/22 Change Change Change Change Constant Constant Constant £m Reported currency currency currency UK & Ireland 1,827 +66.8% +66.8% +65.0% +38.6% - B&Q 1,212 +82.7% +82.7% +81.9% +42.3% - Screwfix 615 +42.5% +42.5% +39.0% +32.5% France 1,177 +97.4% +98.8% +101.7% +18.1% - Castorama 583 +94.5% +95.8% +101.8% +13.9% - Brico Dépôt 594 +100.3% +101.7% +101.7% +22.7% Other International (ex-Russia) 444 +9.4% +13.0% +5.9% (11.0)% - Poland 281 (12.1)% (8.9)% (12.0)% (20.5)% - Iberia(3) 90 +110.8% +112.3% +112.3% +12.1% - Romania(4) 72 +67.2% +71.1% +27.4% +16.6% - Other(5) 1 n/a n/a n/a n/a Total Group (ex-Russia) 3,448 +64.4% +65.7% +64.2% +22.5% - Russia(6) - (100.0)% (100.0)% n/a n/a Total Group 3,448 +60.0% +61.9% +64.2% +22.5% Key points • Continuing to make significant progress against ‘Powered by Kingfisher’ strategic priorities • Growing sales ahead of the market in the UK and France • Total sales up 61.9% in constant currency at £3.4 billion, reflecting strong demand in all categories (against weak comparatives due to temporary store closures in the prior year) • LFL sales up 64.2% and corresponding 2-year LFL up 22.5% o Strong performance in the UK and France, despite COVID-related restrictions impacting French banners through most -

First Quarter Trading Update 2012

EMBARGOED UNTIL 0700 HOURS – Thursday 31 May 2012 Kingfisher reports Q1 total sales down 3.6% and Q1 retail profit down 8.6% impacted by poor weather across Europe and adverse foreign currency translation Group Financial Summary (13 weeks ended 28 April 2012) Retail Sales % Total % Total % LFL Profit % Total % Total 20 12/13 Change Change Change 20 12/13 Change Change £m (Reported) (Constant (Constant £m (Reported) (Constant currency) currency) currency) France 1,089 (1.8)% 2.2% 0.7% 78 0.1% 4.2% UK & Ireland 1,105 (7.0)% (6.9)% (10.4)% 75 (9.8)% (9.8)% Other 438 1.0% 5.8% (2.0)% 7 (48.1)% (36.9)% International Total Group 2,632 (3.6)% (1.3)% (4.8)% 160 (8.6 )% (5.5 )% Note: Joint Venture (Koçta ş JV) and Associate (Hornbach) sales are not consolidated. Retail profit is operating profit stated before central costs, exceptional items, amortisation of acquisition intangibles and the Group’s share of interest and tax of JVs and Associates. Highlights in constant currencies: • Sales and profit impacted by record adverse weather in the UK and across continental Europe, compounded by the comparison with a favourable Q1 this time last year • Seasonal sales across the Group were down 22% impacting profit by around £29 million. However, on-going gross margin and cost initiatives helped limit the Q1 overall profit decline • Net cash was £165 million (30 April 2011: net cash of £283 million) Ian Cheshire, Group Chief Executive, said: “We anticipated the first quarter would be challenging, compared with last year’s strong growth which was boosted by favourable spring weather and public holidays. -

Screwfix Builds Bricks and Mortar Presence with 300Th Store

SCREWFIX BUILDS BRICKS AND MORTAR PRESENCE WITH 300TH STORE Trade and DIY retailer Screwfix is now even more accessible for busy tradesmen on the move across the UK, with the launch of its 300th trade counter in Birstall, West Yorkshire. Screwfix started life as a mail order catalogue-based business, but in response to customers needing to get their tools quickly and conveniently, a rapid store expansion has followed, with 60 stores being opened in 2013 alone. The national store network now gives the nation’s tradesmen, which includes builders, plumbers and electricians, as well as serious DIY-ers, greater access to tools and supplies when on the move in-between jobs. Meeting this 300th store milestone is equally significant given that Screwfix opened its very first store just eight years ago in Yeovil, Somerset. This need for a fast and easy shopping experience has been boosted by an early adoption of a multi-channel model as Screwfix chief executive Andrew Livingston explains: “It really is a case of time is money for our customers because they are busy out and about on the road, from job to job. So we’re doing all we can to help them buy the tools and accessories they need as quickly and easily as possible. As we open the doors to more and more stores across the country, we become even more convenient for our customers. This, topped with our Click & Collect technology, mobile website and smartphone apps means that customers can shop when they want and how they want. “Tradesmen rely on us for the ease and speed of online and over-the-phone ordering, but they also enjoy the store experience thanks to regular – often daily - interaction with staff, many of whom have a background in the trade.” The 300th Screwfix store will open its doors in Birstall, West Yorkshire, joining 8 other stores across West Yorkshire. -

The Revitalized Castorama Store of Ormesson Is Testing Geopositioning with Pricer Search

The revitalized Castorama store of Ormesson is testing geopositioning with Pricer Search Guyancourt, January 25th, 2017. Castorama Ormesson is piloting the Pricer geopositioning solution and is offering its customers a kiosk through which they can easily search the products they are looking for. Locate a product using Infrared trilateration Pricer, the worldwide leader of electronic shelf label (ESL) digital solutions, has developed a unique application based on Infrared (IR) trilateration. The store’s ESLs reply to Pricer’s communication platform, each using a different signal strength enabling their geopositioning and therefore automatically providing the product’s position in the store. Easily find products with the Pricer Search kiosk Relying on the IR infrastructure of the Ormesson store, Pricer has implemented a kiosk allowing customers to easily locate products in the store. The kiosk combines an intuitive « article search » function and a digital map of the store. The automated solution greatly improves the customer’s experience in a DIY world where searching for products can be difficult. Geolocalize with Pricer’s unified platform Trilateration is one the most important components of Pricer’s digital solutions. The Pricer platform associates both hardware (SmartFLASH ESLs) and software solutions composing a unique value added offer which can be easily integrated in any IT environment. Automatic product geolocation provides a better customer experience. Pricer has won the Paris Retail Awards 2016 in the Customer Experience (360) category with its automatic product positioning solution for stores. About Castorama Castorama is part of Kingfisher plc, the European leader of home improvement which operates nearly 1,200 stores in 10 countries in Europe. -

The Industryls Annual Report

2 0 1 5 t doesn’t take an Ivy League economist to we have seen this year, consumers were still explain what happens when consumers very wary about whether these conditions were have more money in their pockets, their tenable. This uneasiness appears to have waned homes’ values increase and they are more in 2015 and can be attributed to several things. MARKET confident about their employment pros- First, consumer confidence was buoyed Ipects and generally comfortable with the state of throughout the year by growth in the job market. the economy overall. They spend more money. Though the job market had expanded in Such has been the case so far in 2015 as home previous, post-recessionary years, unemploy- values headed up, unemployment continued to ment remained high enough that consumers move down and other positive factors came into were still cautious when it came to hopes for play that made average consumers feel a bit more sustained stability. comfortable opening their wallets. Throughout 2015, we saw the unemployment Of course what they did once their wallets were rate drop from 5.7 percent in January down to MEASURE 1 open is also important, and this year consumers 5.0 percent in October , the lowest rate since THE INDUSTry’s AnnuAL REPORT showed their willingness to once again spend April 2008. money to improve and maintain their homes. This rate not only represents the lowest When the year settles out, the North American unemployment in nearly 90 months, but it Retail Hardware Association (NRHA) is predict- is also much more in line with the rates the ing that these favorable economic factors should economy was posting in the four years leading translate to an increase of about 4.9 percent in up to the recession, when home improvement home improvement retail sales for 2015. -

Ireu 2 0 1 8 Top500 Report

INTERNETRETAILING In partnership with IREU 2 0 1 8 TOP500 REPORT THIS LATEST ANNUAL INSIDE internetretailing.net/ireu [email protected] EDITION OF OUR • The Top500 European retailers assessed RESEARCH ASSESSES and ranked LEADING EUROPEAN • How and why Elite retailers RETAILERS FROM A outperform competitors UNIQUE, PERFORMANCE- • We outline the challenges facing European retailers BASED PERSPECTIVE in 2018/19 5992 - KLA - Internet Retailing Magazine_A4_AW.indd 1 07/09/2018 16:43 FROM THE EDITOR-IN-CHIEF Introduction Welcome to the Top500 IREU for 2018, which assesses the performance of European retailers after what has been an eventful 12 months. It’s been a year of significant and continuous improvement among existing and new members of the index, and this has reshaped the retail landscape. The effect of that continuous improvement is now so marked that there are retailers that have fallen out of the Elite level of this ranking that are performing more strongly than when they achieved that ranking last year. They’re being replaced by businesses operating at a new level of excellence. No doubt that change will continue next year as retailers and brands across Europe continue to raise their games. This year we’ve noted that direct-to-consumer brands are playing a larger part in the index as they move at scale to adopt the multichannel techniques that have worked well for retailers that were previously the primary sellers of their goods. This change is likely to be felt painfully by general merchants that previously led the way in using digital to sell goods. Now brands are taking those proven techniques that have worked well for the traders that developed and honed them, and using them to meet demand from customers who are now eager to buy direct as well as through retailers. -

Plan De Vigilance 2020-2021

PLAN DE VIGILANCE 2020-2021 1 Edito du directeur général de Kingfisher France Débutée il y a 30 ans en faveur de la gestion durable des forêts, la démarche d’engagement responsable du Groupe Kingfisher s’est par la suite structurée pour prendre en compte l’ensemble des impacts sociétaux et environnementaux de ses activités. Convaincus que les entreprises ne sont pas des entités hors du monde, nous avons à cœur d’agir de façon responsable vis-à-vis de l’ensemble de nos parties prenantes : nos collaborateurs en premier lieu, en veillant à leur santé, leur sécurité et au respect de leurs libertés ; nos partenaires et tous ceux qui travaillent pour eux, afin qu’ils puissent le faire dans un cadre qui respecte leurs droits fondamentaux ; notre environnement, avec pour objectif de préserver les ressources naturelles, limiter notre empreinte carbone ainsi que celle de nos clients lorsqu’ils utilisent nos produits ; et enfin les communautés locales qui nous entourent. Pour y parvenir, Kingfisher s’est doté d’objectifs ambitieux dans quatre domaines prioritaires : l’inclusion, parce nous voulons donner leur chance à tous les profils ; la lutte contre le changement climatique et la préservation des forêts ; l’accès à des logements plus sains et plus « verts » pour nos clients ; et enfin la lutte contre le mal-logement. Parce que cela relève de notre responsabilité, mais également parce que nous sommes persuadés que ces risques que nous devons éviter sont aussi des opportunités de mieux faire notre métier, en cohérence avec nos valeurs, devenant ainsi un élément essentiel de notre performance. -

Kingfisher Plc 2018-19 Full Year Results Q&A Transcript

Kingfisher plc 2018-19 full year results Q&A transcript - 20 March 2019 __________________________________________________________________________________ 12 months ended 31 January 2019 __________________________________________________________________________________ Speakers: Veronique Laury (VL), CEO Andy Cosslett, (AC), Chairman Karen Witts (KW), CFO Maj Nazir (MN), IR Director __________________________________________________________________________________ GL: Hi there, Geoff Lowery at Redburn. Two questions please. Can you sort of compare and contrast Brico Depot and Castorama for us in terms of the way the new ranges have landed, how you’ve executed that, how you feel about their competitive positions now? It’s just so striking to see such a big delta in top line between your two businesses. And second one, a question for the Chairman. Given your comments about the Board being a hundred percent behind the existing strategy. What flexibility is there for the next CEO if he or she, were to come in and say actually we want to do things differently, we want to trade business differently, the equity market’s not recognising the value of Screwfix therefore we need to change? What scope is there for evolution in strategy? VL: I probably should answer the first one. So, I think that the starting points in Castorama and Brico Depot were very different. The offer was different. You had a starting point, the number of categories that were covering both businesses were not the same, the number of SKU was, as I just said, Brico Depot store is 11,000 SKU today, Castorama is more 50,000 SKU. So, the way the new offer has landed was different. In Brico we have had coverage of customer needs and as well the price positioning of Brico Depot was good at the beginning. -

Strategic Retail Management Text and International Cases 3Rd Edition Strategic Retail Management Joachim Zentes • Dirk Morschett • Hanna Schramm-Klein

Joachim Zentes Dirk Morschett Hanna Schramm-Klein Strategic Retail Management Text and International Cases 3rd Edition Strategic Retail Management Joachim Zentes • Dirk Morschett • Hanna Schramm-Klein Strategic Retail Management Text and International Cases 3rd Edition Joachim Zentes Hanna Schramm-Klein FB Wirtschaftswissenschaften, Universität Siegen Universität des Saarlandes Siegen, Germany Saarbrücken, Germany Dirk Morschett Universität Fribourg Fribourg, Switzerland ISBN 978-3-658-10182-4 ISBN 978-3-658-10183-1 (eBook) DOI 10.1007/978-3-658-10183-1 Springer Gabler Library of Congress Control Number: 2016954795 Springer Gabler © Springer Fachmedien Wiesbaden GmbH 2007, 2011, 2017 This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or part of the material is concerned, specifically the rights of translation, reprinting, reuse of illustrations, recitation, broadcasting, repro- duction on microfilms or in any other physical way, and transmission or information storage and retrieval, elec- tronic adaptation, computer software, or by similar or dissimilar methodology now known or hereafter developed. The use of general descriptive names, registered names, trademarks, service marks, etc. in this publication does not imply, even in the absence of a specific statement, that such names are exempt from the relevant protective laws and regulations and therefore free for general use. The publisher, the authors and the editors are safe to assume that the advice and information in this book are believed to be true and accurate at the date of publication. Neither the publisher nor the authors or the editors give a warranty, express or implied, with respect to the material contained herein or for any errors or omissions that may have been made. -

Home Depot Introduction

HOME DEPOT INTRODUCTION: The Home Depot is an American retailer of home improvement and construction products and services. Headquartered in Vinings, just outside Atlanta in unincorporated Cobb County, Georgia, the Home Depot employs more than 355,000 people and operates 2,141 big-box format stores across the United States (including the 50 U.S. states, the District of Columbia, Puerto Rico, the Virgin Islands and Guam), Canada (ten provinces), Mexico and China. Currently, the world's second largest Home Depot opened on November 14, 2007 on the island of Guam. Established in 1978 by Bernie Marcus and Arthur Blank, the Home Depot Corporation opened its first store in Atlanta, becoming the world’s largest home improvement retailer. They are now the second largest retailer in the United States, offering 40,000 to 50,000 different types of home improvement supplies, building materials, and lawn and garden products. They carry a wide assortment of low-cost products, and offer expert advice and exceptional customer service. As an innovator of the home improvement industry, Home Depot has expanded into Canada, Mexico, Argentina, Chile, and Puerto Rico. Currently there are 1,459 stores including fifty EXPO Design Centers, one Floor Store, and three Home Depot Landscape Supply stores. Home Depot caters to Do-It-Yourself customers, as well as home improvement, construction and building maintenance professionals. Home Depot’s stock went public in 1981 and is traded in the New York Stock Exchange under the ticker symbol, "HD". It is included in the Dow Jones Industrial Average and the Standard and Poor's 500 Index.