How Can Retail Flow Add Value in the Institutional Efx Market?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Finn-Ancial Times Finncap Financials & Insurance Quarterly Sector Note

finn-ancial Times finnCap Financials & Insurance quarterly sector note Q3 2020 | Issue 9 Highlights this quarter: Elevated uncertainty and volatility have been hallmarks of the last 18 months, with Brexit, the UK General Election and more recently COVID-19 all contributing to the challenges that face investors wishing to carve out solid and stable returns amid these ‘unprecedented’ times. With this is mind, and simulating finnCap’s proven Slide Rule methodology, we found the highest quality and lowest value stocks across the financials space, assessing how the make-up of these lists changed over the period January 2019 to July 2020, tracking indexed share price performance over the period as well as movements in P/E and EV/EBIT valuations. The top quartile list of Quality companies outperformed both the Value list and the FTSE All Share by rising +2.5% over the period versus -5.4% for the All Share and -14.3% for Value stocks. Furthermore, the Quality list had protection on the downside in the market crash between February and March 2020, and accelerated faster amid the market rally between late March and July 2020. From high to low (January to March), Quality moved -36.3% against the Value list at -45.5%, while a move off the lows to July was +37.4% for Quality and +34.0% for Value. There was some crossover between the Quality and Value lists, with 7 companies of the top quartile (16 companies in total) appearing in both the Quality and Value lists. This meant that a) investors could capture what we call ‘Quality at Value’ (i.e. -

FTSE Factsheet

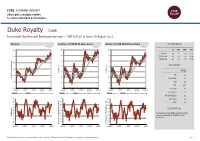

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Duke Royalty DUKE Investment Banking and Brokerage Services — GBP 0.4125 at close 10 August 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 10-Aug-2021 10-Aug-2021 10-Aug-2021 0.45 140 140 1D WTD MTD YTD Absolute -2.4 -1.2 -1.8 35.2 130 130 0.4 Rel.Sector -2.4 -0.5 -3.6 25.9 Rel.Market -2.8 -1.7 -3.7 20.9 120 120 0.35 VALUATION 110 110 0.3 Trailing 100 100 Relative Price Relative Price Relative 0.25 PE -ve Absolute Price (local (local currency) AbsolutePrice 90 90 EV/EBITDA -ve 0.2 80 80 PB 2.0 PCF 28.1 0.15 70 70 Div Yield 4.6 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Price/Sales -ve Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.2 90 90 90 Div Payout -ve 80 80 80 ROE -ve 70 70 70 Share Index) Share Share Sector) Share - 60 - 60 60 DESCRIPTION 50 50 50 40 40 The Company is a globally focused investment 40 RSI RSI (Absolute) 30 30 company specialising in diversified royalty investment. -

Morningstar Report

Report as of 25 Sep 2021 Aberdeen Standard Equity Inc Trust plc , (GB0006039597) Morningstar Rating™ Peer Group Classification Last Close Last Actual NAV (23 Sep 2021) Discount Estimated Nav QQ Morningstar IT UK Equity 345.00 379.95 -9.20 379.95 Income Investment Objective Performance The fund aims to provide shareholders with an above 169 average income while also providing real growth in 146 capital and income. It will invest in a diversified 123 portfolio consisting mainly of quoted UK equities 100 which will normally comprise between 50 and 70 77 individual equity holdings. 54 2016 2017 2018 2019 2020 2021-08 -10.88 23.83 -12.55 9.46 -19.70 19.51 Fund 16.75 13.10 -9.47 19.17 -9.82 14.66 Benchmark 8.76 10.73 -10.56 18.95 -12.56 15.52 Category Management Fee Summary Management fee of 0.65% p.a. of NA on the first GBP 175m and 0.55% thereafter. No performance fee. Contract terminable on notice period of 6 months. Portfolio 31/08/2021 Asset Allocation % Long Short Net Equity Style Box™ Mkt Cap % Fund America Europe Asia Large Size Stocks 113.11 0.00 113.11 Giant 17.55 Bonds 0.00 0.00 0.00 Mid Large 18.27 Cash 0.00 13.11 -13.11 Medium 22.91 Other 0.00 0.00 0.00 Small Small 24.92 Value Blend Growth Micro 16.35 Style Average Mkt Fund Cap (Mil) Ave Mkt Cap GBP 4,115.7 <25 25-50 50-75 >75 7 Top Holdings Stock Sector Weightings % Fund World Regions % Fund Name Sector % hCyclical 66.41 Americas 2.36 BHP Group PLC r 4.54 rBasic Materials 13.25 United States 2.36 Rio Tinto PLC r 4.30 tConsumer Cyclical 14.81 Canada 0.00 CMC Markets PLC y 3.99 -

Fintech Monthly Market Update | July 2021

Fintech Monthly Market Update JULY 2021 EDITION Leading Independent Advisory Firm Houlihan Lokey is the trusted advisor to more top decision-makers than any other independent global investment bank. Corporate Finance Financial Restructuring Financial and Valuation Advisory 2020 M&A Advisory Rankings 2020 Global Distressed Debt & Bankruptcy 2001 to 2020 Global M&A Fairness All U.S. Transactions Restructuring Rankings Advisory Rankings Advisor Deals Advisor Deals Advisor Deals 1,500+ 1 Houlihan Lokey 210 1 Houlihan Lokey 106 1 Houlihan Lokey 956 2 JP Morgan 876 Employees 2 Goldman Sachs & Co 172 2 PJT Partners Inc 63 3 JP Morgan 132 3 Lazard 50 3 Duff & Phelps 802 4 Evercore Partners 126 4 Rothschild & Co 46 4 Morgan Stanley 599 23 5 Morgan Stanley 123 5 Moelis & Co 39 5 BofA Securities Inc 542 Refinitiv (formerly known as Thomson Reuters). Announced Locations Source: Refinitiv (formerly known as Thomson Reuters) Source: Refinitiv (formerly known as Thomson Reuters) or completed transactions. No. 1 U.S. M&A Advisor No. 1 Global Restructuring Advisor No. 1 Global M&A Fairness Opinion Advisor Over the Past 20 Years ~25% Top 5 Global M&A Advisor 1,400+ Transactions Completed Valued Employee-Owned at More Than $3.0 Trillion Collectively 1,000+ Annual Valuation Engagements Leading Capital Markets Advisor >$6 Billion Market Cap North America Europe and Middle East Asia-Pacific Atlanta Miami Amsterdam Madrid Beijing Sydney >$1 Billion Boston Minneapolis Dubai Milan Hong Kong Tokyo Annual Revenue Chicago New York Frankfurt Paris Singapore Dallas -

Weekend News Summary

Weekend News Summary THE SUNDAY TIMES INDICES THIS MORNING Current (%) 1W% Change Sirius seeks light at end of the tunnel: Work continued at Sirius Value Change* Minerals’ Woodsmith mine in North Yorkshire, even as shares in the FTSE 100 7,415.0 -0.2% 1.1% company fell to new lows amid fears over its future. The company so DAX 30 12,383.8 0.02% -0.7% far has completed just over a mile of a planned 23-mile tunnel to take CAC 40 5,647.2 0.1% -0.9% polyhalite deposits from its site near Whitby to Teesside for export as DJIA** 26,820.3 - -0.4% fertiliser. S&P 500** 2,961.8 - -1.0% Clipper Logistics delivers warning with higher profit: A logistics NASDAQ Comp.** 7,939.6 - -2.2% company that processes online orders for retailers including John Nikkei 225 21,755.8 -0.6% -0.9% Lewis and Boohoo.com has posted a strong increase in annual Hang Seng 40 26,092.3 0.5% -1.8% earnings but warned of potential trading turbulence in the year Shanghai Comp 2,905.2 -0.9% -2.5% ahead. Kospi 2,063.1 0.6% -2.0% Fosun ‘discussing bid’ for Thomas Cook brand name: The Chinese BSE Sensex 38,642.5 -0.5% 2.1% company that was working on a rescue deal for Thomas Cook before S&P/ASX 200 6,688.3 -0.4% -0.2% it collapsed is interested in buying the brand name of the 178-year- Current Values as at 10:15 BST, *%Chg from Friday Close, ** As on Friday Close old tour operator. -

ASLIT Investor Update Presentation

Aberforth Partners LLP Presentation to ASLIT Investors May 2021 14 Melville Street ‐ Edinburgh EH3 7NS Tel 0131 220 0733 ‐ Fax 0131 220 0735 [email protected] ‐ www.aberforth.co.uk Aberforth Partners LLP is authorised and regulated by the Financial Conduct Authority Aberforth Unit Trust Managers Limited is authorised and regulated by the Financial Conduct Authority Aberforth Partners update . Over 30 years of value investing ─ We remain committed to the self‐imposed ceiling on the business ─ AUM capped at c.1.5% of the NSCI (XIC)’s market cap ─ Unchanged ownership structure, collegiate approach, investment focus . A consistent process as the partnership continues its natural evolution ─ Sonya Kim joined as an investment manager on 1 March 2021 ─ The investment managers’ biographies are included in the appendix . Alignment of interests through the managers’ significant holdings . UK Stewardship Code 2020 – updated report available on our website Aberforth Partners LLP 1 Performance – periods to 30 April CAGR 16 months to Total Return %YTD1 YearApril 2021 *Launch **Inception FTSE All‐Share 9.7 25.9 ‐1.1 3.6 3.6 FTSE 250 (XIC) 12.2 41.2 2.7 5.8 5.8 FTSE SmallCap (XIC) 23.4 69.5 25.5 8.2 8.2 NSCI (XIC) 16.9 55.9 11.9 6.9 6.9 ASLIT Total Assets 22.8 55.1 ‐1.9 3.2 2.4 ASLIT ORD NAV 31.5 83.3 ‐2.8 3.4 2.5 ASLIT ORD share price 22.0 85.8 ‐5.4 ‐0.5 ‐ ASLIT ZDP share price 3.2 5.2 2.8 2.9 ‐ *Excludes the effects of launch costs **Inception date for ASLIT was 30/06/2017 . -

Execu on Counterpar

Execu�on Counterpar�es A list of all execu�on counterpar�es, used in 2018, including those upon which Brewin Dolphin Capital & Investment (Ireland) Limited places significance reliance on, are stated below. Please note that this list is not exhaus�ve. We reserve the right to use to trade with other counterpar�es addi�onal to those not listed below if we believe that it is in the best interest of a client and in accordance with our Best Execu�on Policy and to remove any venues from the list. The list will be reviewed and updated at least annually as part of our review of best execu�on arrangements or in accordance with our Best Execu�on Policy to sa�sfy that the execu�ons and service provided will give us the best possible result. r s Counterparty s s t t o e s e f n n s t c g d r e e e t c t n n e e c � b e a i d h a e r du t r h a e t o rum r rum D c qu O r t t n T x ff E s s i P E o n n D C I I BANK OF AMERICA MERRILL LYNCH BARCLAYS CAPITAL SECURITIES LTD BLOOMBERG TRADING FACILITY LIMITED BNP PARIBAS CANACCORD GENUITY LIMITED CANTOR FITZGERALD EUROPE CANTOR FITZGERALD IRELAND LIMITED CBOE EUROPE LIMITED CENKOS SECURITIES PLC CITIGROUP GLOBAL MARKETS LIMITED CMC MARKETS COMMERZBANK AG COWEN EXECUTION SERVICES LIMITED DZ BANK EURONEXT DUBLIN FINNCAP LTD FLOW TRADERS B.V. -

FTSE Russell Publications

2 FTSE Russell Publications 19 August 2021 FTSE 250 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Infrastructure 0.43 UNITED Bytes Technology Group 0.23 UNITED Edinburgh Investment Trust 0.25 UNITED KINGDOM KINGDOM KINGDOM 4imprint Group 0.18 UNITED C&C Group 0.23 UNITED Edinburgh Worldwide Inv Tst 0.35 UNITED KINGDOM KINGDOM KINGDOM 888 Holdings 0.25 UNITED Cairn Energy 0.17 UNITED Electrocomponents 1.18 UNITED KINGDOM KINGDOM KINGDOM Aberforth Smaller Companies Tst 0.33 UNITED Caledonia Investments 0.25 UNITED Elementis 0.21 UNITED KINGDOM KINGDOM KINGDOM Aggreko 0.51 UNITED Capita 0.15 UNITED Energean 0.21 UNITED KINGDOM KINGDOM KINGDOM Airtel Africa 0.19 UNITED Capital & Counties Properties 0.29 UNITED Essentra 0.23 UNITED KINGDOM KINGDOM KINGDOM AJ Bell 0.31 UNITED Carnival 0.54 UNITED Euromoney Institutional Investor 0.26 UNITED KINGDOM KINGDOM KINGDOM Alliance Trust 0.77 UNITED Centamin 0.27 UNITED European Opportunities Trust 0.19 UNITED KINGDOM KINGDOM KINGDOM Allianz Technology Trust 0.31 UNITED Centrica 0.74 UNITED F&C Investment Trust 1.1 UNITED KINGDOM KINGDOM KINGDOM AO World 0.18 UNITED Chemring Group 0.2 UNITED FDM Group Holdings 0.21 UNITED KINGDOM KINGDOM KINGDOM Apax Global Alpha 0.17 UNITED Chrysalis Investments 0.33 UNITED Ferrexpo 0.3 UNITED KINGDOM KINGDOM KINGDOM Ascential 0.4 UNITED Cineworld Group 0.19 UNITED Fidelity China Special Situations 0.35 UNITED KINGDOM KINGDOM KINGDOM Ashmore -

Artemis Strategic Assets Fund

Artemis Strategic Assets Fund Half-Yearly Report (unaudited) for the six months ended 28 February 2021 Keep up to date ... ... with the performance of this and other Artemis funds throughout the year on Artemis’ website ■ Monthly fund commentaries and factsheets ■ Market and fund insights ■ Fund briefings and research articles ■ The Hunters’ Tails, our weekly market newsletter ■ Daily fund prices ■ Fund literature artemisfunds.com General information Objective and investment policy Company profile Objective To grow the value of your investment by greater than 3% above the Consumer Price Index (CPI) per annum after Artemis is a leading UK-based fund manager, offering a range fees over a minimum five year period. of funds which invest in the UK, Europe, the US and around Investment What the fund • Company shares the world. policy invests in • Bonds • Property and commodities, indirectly by As a dedicated, active investment house, we specialise in investing through exchange-traded notes and collective investment schemes investment management for both retail and institutional • Other investment funds investors across Europe. • Money market instruments, cash and near cash Independent and owner-managed, Artemis opened Use of The fund may use derivatives to: derivatives • achieve the fund objective, including taking for business in 1997. Its aim was, and still is, exemplary long and short positions investment performance and client service. All Artemis’ • produce additional income or growth • reduce risk staff share these two precepts – and the same flair and • manage the fund efficiently enthusiasm for fund management. • create leverage Where the • Globally The firm now manages some £26.3 billion* across a range fund invests of funds, two investment trusts and both pooled and Industries the • Any segregated institutional portfolios. -

International Smallcap Separate Account As of July 31, 2017

International SmallCap Separate Account As of July 31, 2017 SCHEDULE OF INVESTMENTS MARKET % OF SECURITY SHARES VALUE ASSETS AUSTRALIA INVESTA OFFICE FUND 2,473,742 $ 8,969,266 0.47% DOWNER EDI LTD 1,537,965 $ 7,812,219 0.41% ALUMINA LTD 4,980,762 $ 7,549,549 0.39% BLUESCOPE STEEL LTD 677,708 $ 7,124,620 0.37% SEVEN GROUP HOLDINGS LTD 681,258 $ 6,506,423 0.34% NORTHERN STAR RESOURCES LTD 995,867 $ 3,520,779 0.18% DOWNER EDI LTD 119,088 $ 604,917 0.03% TABCORP HOLDINGS LTD 162,980 $ 543,462 0.03% CENTAMIN EGYPT LTD 240,680 $ 527,481 0.03% ORORA LTD 234,345 $ 516,380 0.03% ANSELL LTD 28,800 $ 504,978 0.03% ILUKA RESOURCES LTD 67,000 $ 482,693 0.03% NIB HOLDINGS LTD 99,941 $ 458,176 0.02% JB HI-FI LTD 21,914 $ 454,940 0.02% SPARK INFRASTRUCTURE GROUP 214,049 $ 427,642 0.02% SIMS METAL MANAGEMENT LTD 33,123 $ 410,590 0.02% DULUXGROUP LTD 77,229 $ 406,376 0.02% PRIMARY HEALTH CARE LTD 148,843 $ 402,474 0.02% METCASH LTD 191,136 $ 399,917 0.02% IOOF HOLDINGS LTD 48,732 $ 390,666 0.02% OZ MINERALS LTD 57,242 $ 381,763 0.02% WORLEYPARSON LTD 39,819 $ 375,028 0.02% LINK ADMINISTRATION HOLDINGS 60,870 $ 374,480 0.02% CARSALES.COM AU LTD 37,481 $ 369,611 0.02% ADELAIDE BRIGHTON LTD 80,460 $ 361,322 0.02% IRESS LIMITED 33,454 $ 344,683 0.02% QUBE HOLDINGS LTD 152,619 $ 323,777 0.02% GRAINCORP LTD 45,577 $ 317,565 0.02% Not FDIC or NCUA Insured PQ 1041 May Lose Value, Not a Deposit, No Bank or Credit Union Guarantee 07-17 Not Insured by any Federal Government Agency Informational data only. -

Annual Report and Financial Statements 2021

CMC Markets plc CMC Markets Annual Report and Financial Statements 2021 and Financial Statements Annual Report CMC Markets plc Annual Report and Financial Statements 2021 OUR PURPOSE Strategic report 2 CMC at a glance 4 Highlights 2021 “Our purpose is to 5 Investment case 6 Chairman’s statement constantly maintain a 8 Stakeholder engagement 10 Chief Executive Officer’s statement superior and unrivalled 14 Our markets 16 Our strategy technology experience 18 Key performance indicators 20 Our business model for our clients.” 22 Technology and product 26 People and sustainability Lord Cruddas 32 Financial review 37 Risk management Founder and CEO 39 Principal risks Corporate governance 46 Board of Directors 48 Governance report The business was started in 1989 54 Group Audit Committee with a simple ethos: to make financial 58 Group Risk Committee 60 Group Nomination Committee markets truly accessible for investors. 62 Directors’ Remuneration Report This fundamental belief remains at the 86 Regulated entities heart of everything we do at CMC 87 Directors’ report Markets and staying true to that has been pivotal to our success. Financial Statements 92 Independent auditors’ report 99 Consolidated income statement 100 Consolidated statement of comprehensive income 101 Consolidated statement of financial position 102 Parent company statement of financial position 103 Consolidated and parent company statements of changes in equity 104 Consolidated and parent company statements of cash flows 105 Notes to the consolidated and parent company Financial