Supply Outpacing Demand Robert Patterson Research Analyst | Downtown Chicago

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rachel Michelin, AIA, LEED AP BD+C Vice President

1 | December 2019 Rachel Michelin, AIA, LEED AP BD+C Vice President Summary Rachel Michelin joined Thornton Tomasetti in 2005. She plays an essential role in building envelope improvement and renovation projects. She investigates building material and building envelope problems and designs repairs for masonry, concrete, stone, curtain walls, roofi ng and waterproofi ng. Rachel is a certifi ed Building Enclosure Commissioning Agent and has extensive experience in the forensic evaluation of building envelopes. Education Select Project Experience • M. Arch. (Structures Option), 2005, University of Illinois at Litigation Support Urbana-Champaign Individual Members/Unit Owners of the Hemingway House • B.S. Architectural Studies, 2003, University of Illinois at Condominium Assn. vs. Hemingway House Condominium Urbana-Champaign Association, regarding the necessity of proposed facade repairs. Continuing Education Facade Investigations and Restorations •University of Wisconsin, Commissioning Building Enclosure Assemblies and Systems 350 E. Cermak Road, Façade Repairs and Window Replacement, Chicago, IL. Professional services for façade Registrations repairs and window replacement at the historic R.R. Donnelly •Registered Architect in Illinois Building located at 350 East Cermak, which is a fully occupied data center and Landmarked building. The construction scope •NCARB Certifi cate Holder included brick masonry, limestone, and terra cotta façade repairs •LEED Accredited Professional, Building Design+Construction and window replacement throughout the -

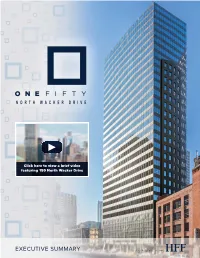

150 North Wacker Drive

Click here to view a brief video featuring 150 North Wacker Drive EXECUTIVE SUMMARY Holliday Fenoglio Fowler, L.P. (“HFF”) Holliday Fenoglio Fowler, L.P. (“HFF”) is pleased to present the sale of the 100% fee simple interest in 150 North Wacker Drive (the “Property”) located in the heart of Chicago’s Central Business District’s (“CBD”) most desirable submarket, the West Loop. The 31-story office tower is located one block east of Chicago’s Ogilvie Transportation Center on Wacker Drive – the home to many of Chicago’s most prestigious firms. The Property, consisting of 246,613 rentable square feet (“RSF”), is currently 91.9% leased and offers a significant mark to market opportunity in a best-in-class location on Wacker Drive. The Property is easily accessible via three major highways and the Chicago Transit Authority’s (“CTA”) transit and bus system, yet is still located in one of the most walkable areas of the city. Given the extensive common area renovations and recent leasing momentum, 150 North Wacker is a truly unique investment opportunity to acquire a rare asset with a premier Wacker Drive address and significant upside potential. KEY PROPERTY STATISTICS Location: 150 North Wacker Submarket: West Loop Total Rentable Area: 246,613 RSF Stories: 31 Percent Leased: 91.9% Weighted Average Lease Term: 4.0 Years Date Completed/Renovated: 1970/2002/2015 Average Floor Plates: 9,300 RSF Finished Ceiling Height: 8'9'' Slab to Slab Ceiling Height: 11'8'' Architect: Joel R. Hillman Parking: 134 Parking Stalls; Valet facilitates up to 160 Vehicles Transit Score: 100 Walk Score: 98 2 EXECUTIVE SUMMARY INVESTMENT HIGHLIGHTS NO. -

Les Numéros En Bleu Renvoient Aux Cartes

276 Index Les numéros en bleu renvoient aux cartes. 10 South LaSalle 98 American Writers Museum 68 35 East Wacker 88 Antiquités 170, 211 55 West Monroe Building 96 Aon Center 106 57th Street Beach 226 Apollo Theater 216 63rd Street Beach 226 Apple Michigan Avenue 134 75 East Wacker Drive 88 Aqua Tower 108 77 West Wacker Drive 88 Archbishop Quigley Preparatory Seminary 161 79 East Cedar Street 189 Architecture 44 120 North LaSalle 98 Archway Amoco Gas Station 197 150 North Riverside 87 Argent 264 181 West Madison Street 98 Arrivée 256 190 South LaSalle 98 Arthur Heurtley House 236 225 West Wacker Drive 87 Articles de voyage 145 300 North LaSalle Drive 156 Art Institute of Chicago 112 311 South Wacker Drive Building 83 Artisanat 78 321 North Clark 156 Art on theMART 159 A 325 North Wells 159 Art public 49 330 North Wabash 155 Arts and Science of the Ancient World: 333 North Michigan Avenue 68 Flight of Daedalus and Icarus 98 333 West Wacker Drive 87 Arts de la scène 40 360 CHICAGO 138 Astor Court 190 INDEX 360 North Michigan Avenue 68 Astor Street 189 400 Lake Shore Drive 158 AT&T Plaza 118 515 North State Building 160 Atwood Sphere 127 543-545 North Michigan Avenue 134 Auditorium Building 73 606, The 233 Auditorium Theatre 80 646 North Michigan Avenue 134 Autocar 258 730 North Michigan Avenue Building 137 Avion 256 860-880 North Lake Shore Drive 178 Axis Apartments & Lofts 179 875 North Michigan Avenue 138 900 North Michigan Shops 139 919 North Michigan Avenue 139 B 1211 North LaSalle Street 192 Baha’i House of Worship 247 1260 North Astor -

Image and Perception of the Top Five American Tourist Cities As Represented by Snow Globes Caitlin Malloy

University of Arkansas, Fayetteville ScholarWorks@UARK Architecture Undergraduate Honors Theses Architecture 5-2017 Image and Perception of the Top Five American Tourist Cities as Represented by Snow Globes Caitlin Malloy Follow this and additional works at: http://scholarworks.uark.edu/archuht Part of the American Popular Culture Commons, Architectural History and Criticism Commons, Marketing Commons, Other Architecture Commons, and the Tourism and Travel Commons Recommended Citation Malloy, Caitlin, "Image and Perception of the Top Five American Tourist Cities as Represented by Snow Globes" (2017). Architecture Undergraduate Honors Theses. 19. http://scholarworks.uark.edu/archuht/19 This Thesis is brought to you for free and open access by the Architecture at ScholarWorks@UARK. It has been accepted for inclusion in Architecture Undergraduate Honors Theses by an authorized administrator of ScholarWorks@UARK. For more information, please contact [email protected], [email protected]. IMAGE AND PERCEPTION OF THE TOP FIVE AMERICAN TOURIST CITIES AS REPRESENTED BY SNOW GLOBES A thesis submitted in partial fulfillment of the requirements of the Honors Program of the Department of Architecture in the School of Architecture + Design Caitlin Lee Malloy May 2017 University of Arkansas at Fayetteville Professor Frank Jacobus Thesis Director Professor Windy Gay Doctor Ethel Goodstein-Murphree Committee Member Committee Member ACKNOWLEDGEMENTS I am so grateful for my time at the Fay Jones School of Architecture + Design – during the past five years, I have had the opportunity to work with the best faculty and have learned so much. My thesis committee in particular has been so supportive of my academic endeavors. My deepest appreciation for my committee chair, Frank Jacobus. -

John Hancock 600000 Visitors Aon Center Unlimited

Aon iconic Pathwayto Possible Chicago, IL Lakeshore east facts Lakeshore East N Cityfront Plaza Dr r D r e w E Hubbard St o L e r N Park Dr N Rush St N New St o e 13,210,000 SF v E Lower No A rth W ater St E North Water St office space n N Wabash Ave t a e S N McClurg Ct zi g E Kin i h N Lake Sh c i 41 r M E River Dr we Chicago River o N Columbus Dr 63,790 L N business population e v A n E Irv Kupcinet Brg E Low W er W l a acker D cker r e Dr ga i v e h L c Chicago i E W e ack M er c Se 8,063 rvi E Wacker Dr i ce Le r vel v E Wacker Dr e r residential units e p p S U n o N N s Breakwater Acc t e t S E Waterside Dr Dr N E Wacker Pl E South Water St N Field Dr s 3,839Lake E Lower South Water St u b hotelMichigan rooms m E South Water St N Westshore Dr u l E Haddock Pl o C N r N Harbor Dr e Lake Shore L w t a e o k C r b v East Park N H e L a d o A S n 1,532,565 SF r E Lake S t N N Park Dr h a h S l s o r e y a SF New Developments a r t r i b e E Benton Pl v r G a i o D N Field Blvd c N W h e r t u N L A E Benton Pl e T 41 v I e S l N A N Stetson Ave N Beaubien Ct $124,000 R T Average INcome o g E Lower Randolph St E R andolph St a t c N Upper Columbus Dr S h St i E Upper Randol p h E Randolp h E Randolph St C N Cultural M Millenium Grant i Center c h 15,000 i Park Park g an Daily Park Visitors A v Date: 8/20/2015 e E Washington St N Columbus Dr Miles 0 0.025 0.05 0.075 0.1 2 Data contained herein was compiled from sources deemed to be reliable. -

Typologies and Evaluation of Outdoor Public Spaces at Street Level of Tall Buildings in Chicago

TYPOLOGIES AND EVALUATION OF OUTDOOR PUBLIC SPACES AT STREET LEVEL OF TALL BUILDINGS IN CHICAGO Abstract Authors Zahida Khan and Peng Du Outdoor public spaces are key to human interactions, promoting Illinois Institute of Technology public life in cities. The constant increase in world population has led Keywords to increased tall urban conditions making the study of outdoor public Public spaces, tall buildings, urban forms, rating system spaces around tall buildings very popular. This paper outlines typol- ogies for outdoor public spaces occurring at street level of tall build- ings in downtown Chicago, the birthplace of skyscrapers and an ideal case study for an American city. The study uses online data archives, Google Maps, and on-site surveys as research techniques for the analysis. The result depicts around 50% of all the tall buildings in Chicago foster public life at its street level through public spaces. The other key finding is the outline of seven typologies based on their position around the tall building. Further, a comparative analysis is conducted using one example of each typology based on three crite- ria adopted from ‘Project for Public Spaces,’ namely (1) Accessibility; (2) Design and Comfort, and (3) Users and Activities. Prometheus 04 Buildings, Cities, and Performance, II Introduction outdoor public spaces, including: (A) Accessibility, (B) Design & Comfort, (C) Users & Activities, (D) Environ- Outdoor public spaces at street level of tall buildings play mental Sustainability, and (E) Sociable. The scope of this a significant role in sustainable city development. The research is limited to the first three design criteria since rapid increase in world population and constant growth of the last two require a bigger timeframe and is addressed urbanization has led many scholars to support Koolhaas’ for future research. -

The Vertical City: Rent Gradients and Spatial Structure

The Vertical City: Rent Gradients and Spatial Structure Crocker H. Liu Robert A. Beck Professor of Hospitality Financial Management School of Hotel Administration Cornell University Phone: (607) 255-3739 [email protected] Stuart S. Rosenthal Maxwell Advisory Board Professor of Economics Department of Economics and Center for Policy Research Syracuse University Syracuse, New York, 13244-1020 Phone: (315) 443-3809 [email protected] William C. Strange RioCan Real Estate Investment Trust Professor of Real Estate and Urban Economics Rotman School of Management University of Toronto, Toronto Ontario M5S 3E6, Canada Phone: (416) 978-1949 [email protected] June 6, 2015 Version: February 8, 2016 PRELIMINARY: COMMENTS WELCOME We thank Laurent Gobillon and Anthony Yezer for helpful comments, as well as seminar participants at George Washington University and the Federal Reserve and attendees at presentations at the 2015 UEA/NARSC Conference in Portland and the AREUEA Annual Meetings in San Francisco. We also thank Daniel Peek and Joseph Shaw for valuable discussions on commercial buildings and leases. In addition, we thank several commercial real estate organizations for providing us with access to their offering memoranda. CompStak data were obtained with support from the Center for Real Estate and Finance at the School of Hotel Administration at Cornell and also from the Maxwell School at Syracuse University. Strange acknowledges financial support from the Social Sciences and Humanities Research Council of Canada and the Centre for Real Estate at the Rotman School of Management. Nuno Mota, Sherry Zhang, Jindong Pang, and Boqian Jiang provided excellent research assistance. Errors, of course, are the responsibility of the three authors. -

Executive Summary

EXECUTIVE SUMMARY hfflp.com 2 CONTACTS INVESTMENT SALES FINANCING HFF OFFICE SEAN P. FOGARTY STEPHEN SKOK ƐƔƏou|_!b;uvb7; -m-]bm] bu;1|ou -m-]bm] bu;1|ou "b|;ƑƔƏƏ ŐƒƐƑőƔƑѶŊƒѵƕƔ ŐƒƐƑőƔƑѶŊƒѵѶƐ _b1-]oķѵƏѵƏѵ v=o]-u|Š_Zrĺ1ol vvhohŠ_Zrĺ1ol ĹŐƒƐƑőƔƑѶŊƒѵƔƏ ĹŐƒƐƑőƔƑѶŊƒѵƔƐ MARTY F. O’CONNELL DANNY KAUFMAN -m-]bm] bu;1|ou -m-]bm] bu;1|ou ŐƒƐƑőƔƑѶŊƒѵƔƒ ŐƒƐƑőƔƑѶŊƒѵѶƓ lo1omm;ѴѴŠ_Zrĺ1ol 7h-=l-mŠ_Zrĺ1ol WICK B. KIRBY ";mbou bu;1|ou ŐƒƐƑőƖѶƏŊƒѵƐƐ hbu0Š_Zrĺ1ol KEVIN M. GIRARD bu;1|ou ŐƒƐƑőƔƑѶŊƒѵѶƖ h]bu-u7Š_Zrĺ1ol MATTHEW D. LAWTON ;1ঞ;-m-]bm] bu;1|ou ŐƒƐƑőƔƑѶŊƒѵƔѵ lѴ-|omŠ_Zrĺ1ol šƑƏƐѶoѴѴb7- ;mo]Ѵbo oѴ;uķĺĺķ !;-Ѵ v|-|;blb|;7Ő1oѴѴ;1ঞ;Ѵķľ Ŀőķ ";1ubঞ;vĺĺ-m7 ";1ubঞ;vblb|;7Ő1oѴѴ;1ঞ;Ѵķľ "Ŀő-u;om;70 ķm1ĺŐ+" Ĺ őĺ -m7b|v-LѴb-|;vor;u-|;o|o= ƑƔoL1;v-m7-u;-Ѵ;-7bm]ruob7;uo=1oll;u1b-Ѵu;-Ѵ;v|-|;-m71-rb|-Ѵl-uh;|vv;ub1;v|o|_;]Ѵo0-Ѵ1oll;u1b-Ѵu;-Ѵ;v|-|;bm7v|uĺ ķ|o];|_;ub|_b|v-LѴb-|;vķo@;uv1Ѵb;m|v-=ѴѴbm|;]u-|;71-rb|-Ѵl-uh;|vrѴ-oul bm1Ѵ7bm]7;0|rѴ-1;l;m|ķbm;v|l;m|-7bvouķ;tb|rѴ-1;l;m|ķ=m7vl-uh;ঞm]ķş-m71ourou-|;-7bvouķѴo-mv-Ѵ;v-m7Ѵo-mv;ub1bm]ĺ oulou;bm=oul-ঞomrѴ;-v;bvb|_Zrĺ1olou=oѴѴo om$b;uŠ ĺ _-v0;;m;m]-];70|_;om;uo=|_;ruor;u|Œruor;uঞ;vœ|ol-uh;|b|Œ|_;lœ=ouv-Ѵ;ĺm=oul-ঞom1om1;umbm]|_;ruor;u|Œruor;uঞ;vœ7;v1ub0;7_;u;bm_-v0;;mo0|-bm;7=uolvou1;vo|_;u|_-m ķ-m7m;b|_;u m;umou ķmou|_;buu;vr;1ঞ;;tb|_oѴ7;uvķoL1;uvķ;lrѴo;;v-m7-];m|vl-h;v-mu;ru;v;m|-ঞomvou-uu-mঞ;vķ;ru;vvoublrѴb;7ķ-v|o|_;-11u-1ou1olrѴ;|;m;vvo=v1_bm=oul-ঞomĺm-m7-ѴѴu;=;u;m1;|o -];ķvt-u;=oo|-];ķbm1ol;ķ;r;mv;v-m7-mo|_;uruor;u|vr;1bC1bm=oul-ঞom-u;-rruobl-|;ĺmorbmbomvķ-vvlrঞomvķou;vঞl-|;v1om|-bm;7_;u;bm-u;ruof;1ঞomvomѴ-m7v;7=oubѴѴv|u-ঞ;rurov;v-m7l-0; -

Building Owners & Managers Association of Chicago

BLS Contract Collection – Metadata Header This contract is provided by the Martin P. Catherwood Library, ILR School, Cornell University. The information provided is for noncommercial educational use only. Some variations from the original paper document may have occurred during the digitization process, and some appendices or tables may be absent. Subsequent changes, revisions, and corrections may apply to this document. For more information about the BLS Contract Collection, see http://digitalcommons.ilr.cornell.edu/blscontracts/ Or contact us: Catherwood Library, Ives Hall, Cornell University, Ithaca, NY 14853 607-254-5370 [email protected] Contract Database Metadata Elements (for a glossary of the elements see - http://digitalcommons.ilr.cornell.edu/blscontracts/2/) Title: Building Owners & Managers Association of Chicago (BOMA) and Service Employees International Union (SEIU), AFL-CIO Locals 1 & 25 (2003) K#: 7413 Employer Name: Building Owners & Managers Association of Chicago (BOMA) Location: IL Chicago Union: Service Employees International Union (SEIU), AFL-CIO Local: 1, 25 SIC: 6513 NAICS: 531110 Sector: P Number of Workers: 2000 Effective Date: 04/07/03 Expiration Date: 04/09/06 Number of Pages: 26 Other Years Available: N For additional research information and assistance, please visit the Research page of the Catherwood website - http://www.ilr.cornell.edu/library/research/ For additional information on the ILR School, http://www.ilr.cornell.edu/ 7413 2000 ee BOMA/CHICAGO - LOCAL 1 2003 JANITORS AGREEMENT April 7, 2003 through -

Chicagopedway

Pedway here 77 W. Wacker s su s su is on 2nd level 201 N. Clark 3 with sky wacker Leo Burnett Building 203 N. LaSalle bridges. Peek out on this bridge for a 200 N. Dearborn cool view of Marina Towers. interesting food court Renaissance Hotel Options include fresh roasted turkey, korean tacos, and 2 for 1 lake Richard J. Daley Center sushi after 2pm. starfruit cafe All natural frozen kefir yogurt. James R. Thompson Center lasalle clark state These three separate Pedways randolph dearborn do not directly connect. All are Block 37 accessible via street level. Macy’s City Hall/County Building Cook County Offices 120 N. LaSalle Three First National Plaza washington One N. Dearborn Abandoned Pedway: First National Bank Building, now Chase Tower called “Chase Tower,” once had Pedway here connecting with Contested section of Pedway: Three First National Plaza. madison If you enter the red or blue line CTA stations between Washington and Jackson (just south of Monroe), the underground platforms continue the entire length of 3 blocks. monroe The basement of Chase Tower has both a large cafeteria and an auditorium, which hosts NPR’s “Wait, Wait, Don’t Tell Me” history quiz show. TIPS ON NAVIGATING PEDWAY KEY Underground Pedway Passage - The access points, which are inside buildings or from the sidewalk, will Street Level or Above Passage 3 help you understand how to find the Underground structure That is passages. 1 Not Seen on Street Level Entrance to Building - If going inside a building, you usually w/ Pedway Access need to go underground. -

Chicago Brochure

WJE CHICAGO WJE Solutions for the Built World Founded in 1956, Wiss, Janney, Elstner Associates, Inc. (WJE), is an interdisciplinary engineering, architecture, and materials science firm specializing in delivering practical, innovative, and technically sound solutions across all areas of new and existing construction. WJE combines state-of-the- art laboratory and testing facilities, nationwide offices, and knowledge sharing systems to provide solutions for the built world. OUR SERVICES OUR APPROACH ◼ Engineering As materials, technologies, and structures change, our fundamental ◼ Architecture philosophy remains the same: developing better solutions based on an accurate diagnosis of each structure’s unique problem. ◼ Laboratory ◼ Field OUR PEOPLE ◼ Forensics With more than forty employees in Chicago and nearly 700 employees worldwide, WJE has the resources to respond to ◼ Design virtually any problem, with expertise in all aspects of construction technology. The firm’s engineers, architects, and materials scientists are supported by technicians who are experts in testing and instrumentation. WJE’s understanding of structural behavior and the performance of materials is enhanced by experience gained from more than 125,000 projects worldwide. OUR RESOURCES Our Janney Technical Center laboratory and testing facility is one of the nation’s largest privately owned construction-based testing laboratories; it enables WJE to provide reliable answers to questions about construction systems, components, and materials. No firm is more qualified to -

The Vertical City: the Price of Land and the Height of Buildings in Chicago 1870-2010

SERC DISCUSSION PAPER 180 The Vertical City: The Price of Land and the Height of Buildings in Chicago 1870-2010 Gabriel M. Ahlfeldt (SERC, LSE and CEPR) Daniel P. McMillen (University of Illinois at Urbana-Champaign) July 2015 This work is part of the research programme of the independent UK Spatial Economics Research Centre funded by a grant from the Economic and Social Research Council (ESRC), Department for Business, Innovation & Skills (BIS) and the Welsh Government. The support of the funders is acknowledged. The views expressed are those of the authors and do not represent the views of the funders. © G.M. Ahlfeldt and D.P. McMillen, submitted 2015 The Vertical City: The Price of Land and the Height of Buildings in Chicago 1870-2010 Gabriel M. Ahlfeldt* Daniel P. McMillen** July 2015 * SERC, London School of Economics and CEPR ** University of Illinois at Urbana-Champaign We thank the Lincoln Institute of Land Policy and especially Joan Youngman and Semida Munteanu for generous funding and support. We are also grateful to the Center for Metropolitan Studies, especially Dorothee Brantz, for hosting a team of researchers during the project work. We thank Christian Hilber and Paul Cheshire for comments and suggestions. Kristoffer Moeller and Sevrin Weights are acknowledged for their great contribution to designing and coordinating the compilation of the land price data set. Ted Pinchbeck is acknowledged for help with the skyscraper data set. Philip Boos, Aline Delatte, Nuria-Maria Hoyer Sepulvedra, Devika Kakkar, Rene Kreichauf, Maike Rackwitz, Lea Siebert, Stefan Tornack, Tzvetelina Tzvetkova provided excellent research assistance. Abstract We analyze the determinants of building heights in Chicago by combining a micro- geographic data set on tall buildings with a unique panel of land prices covering 140 years.