Demand Rift Widens Will Goldstick Research Analyst | Downtown Chicago

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

THE BURNHAM BLOG Urban Planning Touches Every Part of Your Day to Day Life. Join the Conversation That Is Shaping the Region

THE BURNHAM BLOG Back in that time – Chicago 1948 Vision & Theme THE BURNHAM BLOG By Patrick T. Reardon on Wed., 10/28/2009 –9:66 am. Urban planning touches About the Logo If you’re at all a fan of Chicago history, I’m sure you every part of your day to know the frustration. day life. Join the Centennial Committee and Staff You read about Louis Jolliet and Father Jacques conversation that is shaping the region for Marquette arriving in this area in 1674, and you wonder Sponsors the next 100 years. how it looked, how the landscape rolled, where there were trees and where prairies --- the feel of the scene. Register or Login to comment Newsroom Or you look at the Plan of Chicago and ruminate about SUBSCRIBE VIA RSS News Coverage walking down the city’s sidewalks back in 1909 before Use our RSS any of that document’s proposals became reality. feed to track Press Releases new blog posts. Sure, there are photos, but they’re isolated shots --- a corner, a bridge, a building. But what would it have E-News & Social Media ABOUT THIS BLOG been like, for instance, to stroll with Daniel Burnham, the principal author of the Plan, from Michigan Avenue This blog is about The Burnham Blog to Wells Street along Randolph Street? history, planning and the future. It’s rooted in That’s why a quaint 10-minute video that popped up the recognition that we Get Involved recently on YouTube is so delightful. live in a world that is created by plans – and Contact Us by the failure to make plans. -

Rachel Michelin, AIA, LEED AP BD+C Vice President

1 | December 2019 Rachel Michelin, AIA, LEED AP BD+C Vice President Summary Rachel Michelin joined Thornton Tomasetti in 2005. She plays an essential role in building envelope improvement and renovation projects. She investigates building material and building envelope problems and designs repairs for masonry, concrete, stone, curtain walls, roofi ng and waterproofi ng. Rachel is a certifi ed Building Enclosure Commissioning Agent and has extensive experience in the forensic evaluation of building envelopes. Education Select Project Experience • M. Arch. (Structures Option), 2005, University of Illinois at Litigation Support Urbana-Champaign Individual Members/Unit Owners of the Hemingway House • B.S. Architectural Studies, 2003, University of Illinois at Condominium Assn. vs. Hemingway House Condominium Urbana-Champaign Association, regarding the necessity of proposed facade repairs. Continuing Education Facade Investigations and Restorations •University of Wisconsin, Commissioning Building Enclosure Assemblies and Systems 350 E. Cermak Road, Façade Repairs and Window Replacement, Chicago, IL. Professional services for façade Registrations repairs and window replacement at the historic R.R. Donnelly •Registered Architect in Illinois Building located at 350 East Cermak, which is a fully occupied data center and Landmarked building. The construction scope •NCARB Certifi cate Holder included brick masonry, limestone, and terra cotta façade repairs •LEED Accredited Professional, Building Design+Construction and window replacement throughout the -

333 North Michigan Buildi·N·G- 333 N

PRELIMINARY STAFF SUfv1MARY OF INFORMATION 333 North Michigan Buildi·n·g- 333 N. Michigan Avenue Submitted to the Conwnission on Chicago Landmarks in June 1986. Rec:ornmended to the City Council on April I, 1987. CITY OF CHICAGO Richard M. Daley, Mayor Department of Planning and Development J.F. Boyle, Jr., Commissioner 333 NORTH MICIDGAN BUILDING 333 N. Michigan Ave. (1928; Holabird & Roche/Holabird & Root) The 333 NORTH MICHIGAN BUILDING is one of the city's most outstanding Art Deco-style skyscrapers. It is one of four buildings surrounding the Michigan A venue Bridge that defines one of the city' s-and nation' s-finest urban spaces. The building's base is sheathed in polished granite, in shades of black and purple. Its upper stories, which are set back in dramatic fashion to correspond to the city's 1923 zoning ordinance, are clad in buff-colored limestone and dark terra cotta. The building's prominence is heightened by its unique site. Due to the jog of Michigan Avenue at the bridge, the building is visible the length of North Michigan Avenue, appearing to be located in the center of the street. ABOVE: The 333 North Michigan Building was one of the first skyscrapers to take advantage of the city's 1923 zoning ordinance, which encouraged the construction of buildings with setback towers. This photograph was taken from the cupola of the London Guarantee Building. COVER: A 1933 illustration, looking south on Michigan Avenue. At left: the 333 North Michigan Building; at right the Wrigley Building. 333 NORTH MICHIGAN BUILDING 333 North Michigan Avenue Architect: Holabird and Roche/Holabird and Root Date of Construction: 1928 0e- ~ 1QQ 2 00 Cft T Dramatically sited where Michigan Avenue crosses the Chicago River are four build ings that collectively illustrate the profound stylistic changes that occurred in American architecture during the decade of the 1920s. -

FOR IMMEDIATE RELEASE July 18, 2014 CONTACT

FOR IMMEDIATE RELEASE July 18, 2014 CONTACT: Mayor’s Press Office 312.744.3334 [email protected] MAYOR EMANUEL ANNOUNCES THE SECOND EXPANSION OF RETROFIT CHICAGO’S COMMERCIAL BUILDINGS INITIATIVE 16 additional facilities commit to 20 percent energy efficiency improvement within five years; current participants have achieved seven percent energy reduction to-date Marking another milestone in the City’s efforts to accelerate energy efficiency, Mayor Rahm Emanuel today announced the further expansion of Retrofit Chicago’s Commercial Buildings Initiative. The new building participants, including 11 higher education facilities, four commercial office buildings, and one cultural institution, have committed to at least 20 percent energy efficiency improvement within five years. This announcement expands the total program reach to 48 buildings and 37 million square feet, making Retrofit Chicago’s Commercial Buildings Initiative one of the largest private sector voluntary efficiency programs in the country. “Retrofit Chicago participants are leading a rising private sector energy movement that demonstrates how efficiency makes good business sense and good sense for our environment,” said Mayor Emanuel. “These buildings’ operational and capital improvements are saving money, reducing carbon emissions, creating 21st century jobs, and lowering the cost of doing business in Chicago.” To-date, current program participants have collectively achieved a seven percent reduction in total source energy use, with accompanying annual energy cost savings of $2.5 million and greenhouse gas emissions reductions equivalent to removing 5,800 cars from the road. Upon reaching the 20 percent improvement target, all 48 building participants have potential to save more than 150 million kilowatt-hours of electricity per year, while creating hundreds of local jobs in the growing clean energy economy. -

FOR IMMEDIATE RELEASE March 6, 2013 CONTACT

FOR IMMEDIATE RELEASE March 6, 2013 CONTACT: Mayor’s Press Office 312.744.3334 [email protected] MAYOR EMANUEL ANNOUNCES RETROFIT CHICAGO: COMMERCIAL BUILDINGS INITIATIVE DOUBLES IN SIZE Including new office, hotel, large residential, institutional properties; total program reach to over 28 million square feet Today Mayor Emanuel announced 18 new participants in Retrofit Chicago’s Commercial Buildings Initiative, bringing the program’s total reach to over 28 million square feet. This doubles the 14 million square feet represented by the program’s founding 14 participants. The Commercial Buildings Initiative was launched on June 5 by Mayor Emanuel and U.S. Secretary of Energy Dr. Steven Chu. “This expansion of Retrofit Chicago’s Commercial Buildings Initiative highlights the leadership of commercial building owners, managers, and tenants in making Chicago a center of building efficiency and a place where companies are maximizing their ability to compete,” said Mayor Emanuel. “These participants understand that in the modern economic environment, it is critical to operate at maximum efficiency. The commitments that have been made by these 32 organizations will create jobs and foster growth throughout Chicago’s economy, while improving our environment as well.” Energy efficiency and clean energy comprise one of seven focus areas outlined in Sustainable Chicago 2015, a three-year roadmap to drive sustainability through city operations, in residents’ day-to-day lives, and across our economy. The Commercial Buildings Initiative is one component of Retrofit Chicago – the City’s cross-sector effort to accelerate energy efficiency in buildings – which also includes energy efficiency efforts in municipal and residential buildings. -

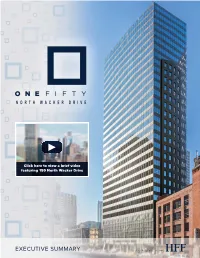

150 North Wacker Drive

Click here to view a brief video featuring 150 North Wacker Drive EXECUTIVE SUMMARY Holliday Fenoglio Fowler, L.P. (“HFF”) Holliday Fenoglio Fowler, L.P. (“HFF”) is pleased to present the sale of the 100% fee simple interest in 150 North Wacker Drive (the “Property”) located in the heart of Chicago’s Central Business District’s (“CBD”) most desirable submarket, the West Loop. The 31-story office tower is located one block east of Chicago’s Ogilvie Transportation Center on Wacker Drive – the home to many of Chicago’s most prestigious firms. The Property, consisting of 246,613 rentable square feet (“RSF”), is currently 91.9% leased and offers a significant mark to market opportunity in a best-in-class location on Wacker Drive. The Property is easily accessible via three major highways and the Chicago Transit Authority’s (“CTA”) transit and bus system, yet is still located in one of the most walkable areas of the city. Given the extensive common area renovations and recent leasing momentum, 150 North Wacker is a truly unique investment opportunity to acquire a rare asset with a premier Wacker Drive address and significant upside potential. KEY PROPERTY STATISTICS Location: 150 North Wacker Submarket: West Loop Total Rentable Area: 246,613 RSF Stories: 31 Percent Leased: 91.9% Weighted Average Lease Term: 4.0 Years Date Completed/Renovated: 1970/2002/2015 Average Floor Plates: 9,300 RSF Finished Ceiling Height: 8'9'' Slab to Slab Ceiling Height: 11'8'' Architect: Joel R. Hillman Parking: 134 Parking Stalls; Valet facilitates up to 160 Vehicles Transit Score: 100 Walk Score: 98 2 EXECUTIVE SUMMARY INVESTMENT HIGHLIGHTS NO. -

Les Numéros En Bleu Renvoient Aux Cartes

276 Index Les numéros en bleu renvoient aux cartes. 10 South LaSalle 98 American Writers Museum 68 35 East Wacker 88 Antiquités 170, 211 55 West Monroe Building 96 Aon Center 106 57th Street Beach 226 Apollo Theater 216 63rd Street Beach 226 Apple Michigan Avenue 134 75 East Wacker Drive 88 Aqua Tower 108 77 West Wacker Drive 88 Archbishop Quigley Preparatory Seminary 161 79 East Cedar Street 189 Architecture 44 120 North LaSalle 98 Archway Amoco Gas Station 197 150 North Riverside 87 Argent 264 181 West Madison Street 98 Arrivée 256 190 South LaSalle 98 Arthur Heurtley House 236 225 West Wacker Drive 87 Articles de voyage 145 300 North LaSalle Drive 156 Art Institute of Chicago 112 311 South Wacker Drive Building 83 Artisanat 78 321 North Clark 156 Art on theMART 159 A 325 North Wells 159 Art public 49 330 North Wabash 155 Arts and Science of the Ancient World: 333 North Michigan Avenue 68 Flight of Daedalus and Icarus 98 333 West Wacker Drive 87 Arts de la scène 40 360 CHICAGO 138 Astor Court 190 INDEX 360 North Michigan Avenue 68 Astor Street 189 400 Lake Shore Drive 158 AT&T Plaza 118 515 North State Building 160 Atwood Sphere 127 543-545 North Michigan Avenue 134 Auditorium Building 73 606, The 233 Auditorium Theatre 80 646 North Michigan Avenue 134 Autocar 258 730 North Michigan Avenue Building 137 Avion 256 860-880 North Lake Shore Drive 178 Axis Apartments & Lofts 179 875 North Michigan Avenue 138 900 North Michigan Shops 139 919 North Michigan Avenue 139 B 1211 North LaSalle Street 192 Baha’i House of Worship 247 1260 North Astor -

Architectural Footnotes the Chicago Tribune Tower

QUOTATION: What does history have in store for architecture today? Architectural Footnotes The Chicago Tribune Tower Cristina Garduño Freeman The University of Melbourne Vicki Leibowitz The University of Queensland Abstract One hundred and fifty material ‘quotations’ from significant buildings and places around the world (and indeed beyond it) are set into the Chicago Tribune Tower. The building, designed by Hood and Howells in 1922, was conceived as a materialisation of the power of the news corporation. The exterior is neo-gothic, while the interiors are commercially driven; and the base displays culturally significant material artefacts collected internationally. These material fragments are decontextualised from canonical sites and monuments and resituated within the tower’s architecture. Pieces-of-rock from places such as the Pyramids at Giza, the Sydney Opera House, Edinburgh Castle, the Forbidden City, the Berlin Wall, Antarctica, and even ‘The Moon’ form a haphazardly curated collection, exhibited as so-called architectural wonders, except in this case the cabinet of curiosities furnishing them is the façade of the Chicago Tribune Tower. This paper examines an instance of material quotation. In so doing, it draws upon the theoretical framework of Critical Heritage Studies which argues for an assessment of significance based on the decreased value of the material in favour of the social, cultural and performative aspects of heritage making. At the Tribune Tower, the collection of fragments is the result of Tribune editor and business mogul Robert McCormick’s fetishisation of spolia. The exhibition of these artefacts can be understood as an account of significant architectural chronology, yet their suture to the building’s façade leaves these quotations dangling without explanation and renders them an afterthought. -

Download Downtown Scranton Landmark Buildings and Historic

Downtown Scranton Landmark Buildings and Historic Districts Introduction Historic preservation in Scranton arose from a grass-roots movement in the late 1970's in response to serious threats to the late nineteenth/early 20th century fabric of the city, including the most significant and defining landmarks. Initial responses were in protest of demolition, but the main emphasis was on education and the development of a sense of pride in Scranton's unique architectural expression of its industrial boomtown history. The Architectural Heritage Association (AHA), founded in 1978, worked with the Pennsylvania Historic and Museum Association to create the Lackawanna Avenue Historic District, with the intent of seeing the then decaying commercial district retained and revived. In the 80s and 90s, redevelopment came to Scranton, but with the mixed blessings to the National Park Service, who intended to create the Steamtown Historic Site, and the Steamtown Mall developers, who intended to demolish most of Lackawanna Avenue. Local politicians and the press were strongly in favor of building the mall, even though it meant moving out active businesses, gaining control of the properties, and destroying historic structures. The architectural firm involved in the demolition of part of the Lackawanna Avenue Historic District to build the mall in 1992 failed to follow the process for altering nationally registered historic properties. That failure allowed the AHA to file a lawsuit. After several years, the court issued mitigation avenues: the 500 block of Lackawanna Avenue would not be demolished or included in the mall, the Oppenheim and Samters Buildings would be adaptively developed as office structures, the AHA would receive a cash settlement to assist in future preservation advocacy, and the City was to appoint a preservation specialist and establish, by ordinance, a Historical and Architectural Review Board (HARB). -

Image and Perception of the Top Five American Tourist Cities As Represented by Snow Globes Caitlin Malloy

University of Arkansas, Fayetteville ScholarWorks@UARK Architecture Undergraduate Honors Theses Architecture 5-2017 Image and Perception of the Top Five American Tourist Cities as Represented by Snow Globes Caitlin Malloy Follow this and additional works at: http://scholarworks.uark.edu/archuht Part of the American Popular Culture Commons, Architectural History and Criticism Commons, Marketing Commons, Other Architecture Commons, and the Tourism and Travel Commons Recommended Citation Malloy, Caitlin, "Image and Perception of the Top Five American Tourist Cities as Represented by Snow Globes" (2017). Architecture Undergraduate Honors Theses. 19. http://scholarworks.uark.edu/archuht/19 This Thesis is brought to you for free and open access by the Architecture at ScholarWorks@UARK. It has been accepted for inclusion in Architecture Undergraduate Honors Theses by an authorized administrator of ScholarWorks@UARK. For more information, please contact [email protected], [email protected]. IMAGE AND PERCEPTION OF THE TOP FIVE AMERICAN TOURIST CITIES AS REPRESENTED BY SNOW GLOBES A thesis submitted in partial fulfillment of the requirements of the Honors Program of the Department of Architecture in the School of Architecture + Design Caitlin Lee Malloy May 2017 University of Arkansas at Fayetteville Professor Frank Jacobus Thesis Director Professor Windy Gay Doctor Ethel Goodstein-Murphree Committee Member Committee Member ACKNOWLEDGEMENTS I am so grateful for my time at the Fay Jones School of Architecture + Design – during the past five years, I have had the opportunity to work with the best faculty and have learned so much. My thesis committee in particular has been so supportive of my academic endeavors. My deepest appreciation for my committee chair, Frank Jacobus. -

John Hancock 600000 Visitors Aon Center Unlimited

Aon iconic Pathwayto Possible Chicago, IL Lakeshore east facts Lakeshore East N Cityfront Plaza Dr r D r e w E Hubbard St o L e r N Park Dr N Rush St N New St o e 13,210,000 SF v E Lower No A rth W ater St E North Water St office space n N Wabash Ave t a e S N McClurg Ct zi g E Kin i h N Lake Sh c i 41 r M E River Dr we Chicago River o N Columbus Dr 63,790 L N business population e v A n E Irv Kupcinet Brg E Low W er W l a acker D cker r e Dr ga i v e h L c Chicago i E W e ack M er c Se 8,063 rvi E Wacker Dr i ce Le r vel v E Wacker Dr e r residential units e p p S U n o N N s Breakwater Acc t e t S E Waterside Dr Dr N E Wacker Pl E South Water St N Field Dr s 3,839Lake E Lower South Water St u b hotelMichigan rooms m E South Water St N Westshore Dr u l E Haddock Pl o C N r N Harbor Dr e Lake Shore L w t a e o k C r b v East Park N H e L a d o A S n 1,532,565 SF r E Lake S t N N Park Dr h a h S l s o r e y a SF New Developments a r t r i b e E Benton Pl v r G a i o D N Field Blvd c N W h e r t u N L A E Benton Pl e T 41 v I e S l N A N Stetson Ave N Beaubien Ct $124,000 R T Average INcome o g E Lower Randolph St E R andolph St a t c N Upper Columbus Dr S h St i E Upper Randol p h E Randolp h E Randolph St C N Cultural M Millenium Grant i Center c h 15,000 i Park Park g an Daily Park Visitors A v Date: 8/20/2015 e E Washington St N Columbus Dr Miles 0 0.025 0.05 0.075 0.1 2 Data contained herein was compiled from sources deemed to be reliable. -

Illinois Pollution Control Board

Electronic Filing - Received, Clerk's Office, June 25, 2008 BEFORE THE ILLINOIS POLLUTION CONTROL BOARD IN THE MATTER OF: ) ) WATER QUALITY STANDARDS AND ) EFFLUENT LIMITATIONS FOR THE ) R08-9 CHICAGO AREA WATERWAY SYSTEM ) (Rulemaking - Water)· AND THE LOWER DES PLAINES RIVER: ) PROPOSED AMENDMENTS TO 35 Ill. ) Adm. Code Parts 301, 302, 303 and 304. ) NOTICE OF FILING To: see attached Service List PLEASE TAKE NOTICE that on the 25 th Day ofJune, 2008, I filed with the Office of the Clerk ofthe Illinois Pollution Control Board the attached Response of Environmental Law and Policy Center, Friends ofthe Chicago River, Sierra Club (Illinois Chapter), Natural Resources Defense Council and Openlands to the Metropolitan Water Reclamation District of Greater Chicago's Motion To Stay, a copy ofwhich is hereby served upon you. By:!!t~~- Dated: June 25, 2008 Environmental Law and Policy Center 35 East Wacker Drive, Suite 1300 Chicago, IL 60601-2110 312-795-3747 Electronic Filing - Received, Clerk's Office, June 25, 2008 CERTIFICATE OF SERVICE I, Albert Ettinger, the undersigned attorney, hereby certify that I have served the attached Response to the Metropolitan Water Reclamation District of Greater Chicago's Motion To Stay, on all parties ofrecord (Service List attached), by depositing said documents in the United States Mail, postage prepaid, from 35 East Wacker Drive, Suite 1300, Chicago, Illinois before the hour of5:00 p.m., on this 25 th Day ofJune, 2008. ~~ Electronic Filing - Received, Clerk's Office, June 25, 2008 Service List Richard J. Kissel and Roy M. Harsch Bernard Sawyer and Thomas Granto Drinker, Biddle, Gardner, Carton Metropolitan Water Reclamation District 191 N.