Tall Building and Land Values: Height and Construction Cost Elasticities in Chicago, 1870 - 2010

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rachel Michelin, AIA, LEED AP BD+C Vice President

1 | December 2019 Rachel Michelin, AIA, LEED AP BD+C Vice President Summary Rachel Michelin joined Thornton Tomasetti in 2005. She plays an essential role in building envelope improvement and renovation projects. She investigates building material and building envelope problems and designs repairs for masonry, concrete, stone, curtain walls, roofi ng and waterproofi ng. Rachel is a certifi ed Building Enclosure Commissioning Agent and has extensive experience in the forensic evaluation of building envelopes. Education Select Project Experience • M. Arch. (Structures Option), 2005, University of Illinois at Litigation Support Urbana-Champaign Individual Members/Unit Owners of the Hemingway House • B.S. Architectural Studies, 2003, University of Illinois at Condominium Assn. vs. Hemingway House Condominium Urbana-Champaign Association, regarding the necessity of proposed facade repairs. Continuing Education Facade Investigations and Restorations •University of Wisconsin, Commissioning Building Enclosure Assemblies and Systems 350 E. Cermak Road, Façade Repairs and Window Replacement, Chicago, IL. Professional services for façade Registrations repairs and window replacement at the historic R.R. Donnelly •Registered Architect in Illinois Building located at 350 East Cermak, which is a fully occupied data center and Landmarked building. The construction scope •NCARB Certifi cate Holder included brick masonry, limestone, and terra cotta façade repairs •LEED Accredited Professional, Building Design+Construction and window replacement throughout the -

Read More and Download The

Case Study: Vista Tower, Chicago A New View, and a New Gateway, for Chicago Abstract Upon completion, Vista Tower will become Chicago’s third tallest building, topping out the Lakeshore East development, where the Chicago River meets Lake Michigan. Juliane Wolf will participate in the Session 7C panel discussion High-Rise Occupying a highly visible site on a north- Design Drivers: Now to 2069, on Jeanne Gang Juliane Wolf south view corridor within the city’s grid, and in Wednesday, 30 October. Vista Tower is the subject of the off-site close proximity to the Loop, the river, and the program on Thursday, Authors city’s renowned lakefront park system, this 31 October. Jeanne Gang, Founding Principal and Partner Juliane Wolf, Design Principal and Partner mixed-use supertall building with a porous Studio Gang 1520 West Division Street base is simultaneously a distinctive landmark Chicago, IL 60642 USA at the scale of the city and a welcoming connector at the ground plane. Clad in a t: +1 773 384 1212 gradient of green-blue glass and supported by a reinforced concrete structure, the e: [email protected] studiogang.com tower is composed of an interconnected series of stacked, frustum-shaped volumes that move rhythmically in and out of plane and extend to various heights. The Jeanne Gang, architect and MacArthur Fellow, is the Founding Principal and Partner of Studio tower is lifted off the ground plane at the center, creating a key gateway for Gang, an architecture and urban design practice headquartered in Chicago with offices in New York, pedestrians accessing the Riverwalk from Lakeshore East Park. -

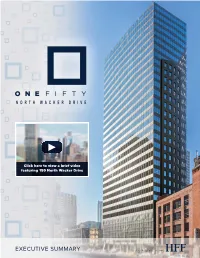

150 North Wacker Drive

Click here to view a brief video featuring 150 North Wacker Drive EXECUTIVE SUMMARY Holliday Fenoglio Fowler, L.P. (“HFF”) Holliday Fenoglio Fowler, L.P. (“HFF”) is pleased to present the sale of the 100% fee simple interest in 150 North Wacker Drive (the “Property”) located in the heart of Chicago’s Central Business District’s (“CBD”) most desirable submarket, the West Loop. The 31-story office tower is located one block east of Chicago’s Ogilvie Transportation Center on Wacker Drive – the home to many of Chicago’s most prestigious firms. The Property, consisting of 246,613 rentable square feet (“RSF”), is currently 91.9% leased and offers a significant mark to market opportunity in a best-in-class location on Wacker Drive. The Property is easily accessible via three major highways and the Chicago Transit Authority’s (“CTA”) transit and bus system, yet is still located in one of the most walkable areas of the city. Given the extensive common area renovations and recent leasing momentum, 150 North Wacker is a truly unique investment opportunity to acquire a rare asset with a premier Wacker Drive address and significant upside potential. KEY PROPERTY STATISTICS Location: 150 North Wacker Submarket: West Loop Total Rentable Area: 246,613 RSF Stories: 31 Percent Leased: 91.9% Weighted Average Lease Term: 4.0 Years Date Completed/Renovated: 1970/2002/2015 Average Floor Plates: 9,300 RSF Finished Ceiling Height: 8'9'' Slab to Slab Ceiling Height: 11'8'' Architect: Joel R. Hillman Parking: 134 Parking Stalls; Valet facilitates up to 160 Vehicles Transit Score: 100 Walk Score: 98 2 EXECUTIVE SUMMARY INVESTMENT HIGHLIGHTS NO. -

Les Numéros En Bleu Renvoient Aux Cartes

276 Index Les numéros en bleu renvoient aux cartes. 10 South LaSalle 98 American Writers Museum 68 35 East Wacker 88 Antiquités 170, 211 55 West Monroe Building 96 Aon Center 106 57th Street Beach 226 Apollo Theater 216 63rd Street Beach 226 Apple Michigan Avenue 134 75 East Wacker Drive 88 Aqua Tower 108 77 West Wacker Drive 88 Archbishop Quigley Preparatory Seminary 161 79 East Cedar Street 189 Architecture 44 120 North LaSalle 98 Archway Amoco Gas Station 197 150 North Riverside 87 Argent 264 181 West Madison Street 98 Arrivée 256 190 South LaSalle 98 Arthur Heurtley House 236 225 West Wacker Drive 87 Articles de voyage 145 300 North LaSalle Drive 156 Art Institute of Chicago 112 311 South Wacker Drive Building 83 Artisanat 78 321 North Clark 156 Art on theMART 159 A 325 North Wells 159 Art public 49 330 North Wabash 155 Arts and Science of the Ancient World: 333 North Michigan Avenue 68 Flight of Daedalus and Icarus 98 333 West Wacker Drive 87 Arts de la scène 40 360 CHICAGO 138 Astor Court 190 INDEX 360 North Michigan Avenue 68 Astor Street 189 400 Lake Shore Drive 158 AT&T Plaza 118 515 North State Building 160 Atwood Sphere 127 543-545 North Michigan Avenue 134 Auditorium Building 73 606, The 233 Auditorium Theatre 80 646 North Michigan Avenue 134 Autocar 258 730 North Michigan Avenue Building 137 Avion 256 860-880 North Lake Shore Drive 178 Axis Apartments & Lofts 179 875 North Michigan Avenue 138 900 North Michigan Shops 139 919 North Michigan Avenue 139 B 1211 North LaSalle Street 192 Baha’i House of Worship 247 1260 North Astor -

Traffic Impact Study Wolf Point Development Chicago, Illinois

Traffic Impact Study Wolf Point Development Chicago, Illinois Prepared for Hines Submitted by: Kenig, Lindgren, O’Hara, Aboona, Inc. November 8, 2012 Introduction This report summarizes the methodologies, results, and findings of a traffic impact study conducted by Kenig, Lindgren, O’Hara, Aboona, Inc. (KLOA, Inc.) for the proposed Wolf Point Development to be located in Chicago, Illinois. The site is bounded by the Apparel Mart building/Kinzie Street to the north, the Chicago River to the west and south, and Orleans Street to the east. Figure 1 shows the location of the site in relation to the area street system and Figure 2 shows an aerial view of the area. The development proposes three towers. • West Tower (Site A) - A residential tower providing approximately 500 residential units and 200 parking spaces for residents. • South Tower (Site B) - An approximate 1.8 million square-foot mixed-use tower with 1.2 million square feet of office space, approximately 600 residential units, and 400 parking spaces for the tower residents and employees. • East Tower (Site C) - An office tower with approximately 1.5 million square feet of space and 200 parking spaces for employees. The West (residential tower), South and East Towers will only have one full inbound and outbound access via the existing driveway (Wolf Point Plaza) off Orleans Street opposite South Mart Drive. The existing Kinzie Street private access drive located west of the site will be restricted to only service related traffic associated with the buildings adjacent to Wolf Point and truck traffic traveling to/from the West and South Towers of the Wolf Point Development. -

ACTIVE PLA PROJECTS • One Chicago Square

ACTIVE PLA PROJECTS • One Chicago Square (Chicago, State, Superior, Dearborn) (Power) 2019 • 3/Eleven Chicago 301-33 West Illinois, Chicago(Power) 2016 • 10-30 South Wacker (Lendlease) 2018 • 105 North May (Skender) 2018 • 110 North Wacker (Office Building) (Clark) 2017 • 178 West Randolph – Courtyard Marriott (Pepper) 2020 • 210 North Carpenter ((Leopardo) 2017 • 243 East Ontario (18 Story Hotel) (AECOM) 2017 • 311 West Monroe (15 Story Office Bldg.) (Leopardo) 2018 • 312 North Carpenter (LG Construction) 2016 • 320 South Canal (Clark Construction) 2019 • 333 North Green (19 Story Office Bldg. & Parking) (Power) 2018 • 345 North Morgan (11 Story Office Blg.) (Skender) 2020 • 403 North Wabash (17 Story – Condos) (McHugh) 2017 • 448 North LaSalle (13 Story office building) (Lendlease) 2019 • 633 West North Avenue (11 Story Apartment Bldg.) (Power) 2018 • 717 South Clark (31 Story Apartment Bldg.) (Lendlease) 2019 • 740 North Aberdeen (12 Story Apartment Bldg.) (McHugh) 2019 • 800 West Fulton Market (19 Story Office Bldg.) (Lendlease) 2019 • 840 South Canal (Data Center) (Clune Construction) 2018 • 845 West Madison (Lendlease) 2018 • 949 West Dakin (Apartment Development) (Leopardo) 2020 • 955 East 131st/Altgeld Gardens (Comm./Library Facility) (ALL Masonry) 2019 • 1000M (1000 South Michigan Avenue – Mixed Use High Rise) (McHugh) 2020 • 1100 West Fulton (5 Story Building/Renovation) (Skender) 2019 • 1200 South Indiana (McHugh) 2017 • 1313 West Morse (8 Story Mixed Use) (Pepper) 2017 • 1326 South Michigan (500 Unit Apt. Bld.) (Walsh) 2017 • 1375 West Fulton Office Building (Power) 2019 • 1515 West Webster (4 Story Shell & Core Office Bldg.)(Power) 2016 • 1550 North Clark (10 story condo) (Power) 2018 • 3501 South Pulaski (warehouse & distribution center/Hilco) 2018 • Advocate South Suburban Hospital Procedural Ctr. -

Summer Fun! New Tours, New Activities— Member Magazine · Summer 2019 Enjoy Everything the Cac Is Offering This Summer

SUMMER FUN! NEW TOURS, NEW ACTIVITIES— MEMBER MAGAZINE · SUMMER 2019 ENJOY EVERYTHING THE CAC IS OFFERING THIS SUMMER PAGE 4 WHAT’S NEW ON THE RIVERWALK? PAGE 8 STUDENT VOICES: HEAR FROM OUR TEENS PAGE 12 GENERAL WHAT A YEAR! INFORMATION August marks one year since we opened the Chicago Architecture Center. As we celebrate this momentous anniversary, we’ve CAC HOURS taken a look back to see how far we’ve come. By bringing tours, DAILY: exhibits, education and public programs under one roof, we have 9am (box office, tours & store); created something unique. Our vision has taken root and our 9:30am (exhibits) to 5pm hopes to create a hub for all things architecture where exciting CLOSED: ideas can be shared is coming true. Here are just a few highlights New Year’s Day, of our work as a thought leader in our first year! Thanksgiving and Christmas Hours are subject to change BUILT ENVIRONMENT EDUCATION SURVEY LANDSCAPE REPORT LOCATION In anticipation of a new mayor and In partnership with AIA Chicago 111 E. Wacker Drive city council, the CAC recently issued and the newly formed Chicago Chicago, Illinois 60601 a survey to more than 400 local Architecture Education Network, the design and civic leaders, asking them CAC recently produced and published CONTACT to identify key issues in the city’s the first report to ever document 312.922.TOUR (8687) built environment. The results of the Chicago’s K-12 architecture and design architecture.org survey will inform our conversations education landscape. Our hope is that with the new administration. -

Image and Perception of the Top Five American Tourist Cities As Represented by Snow Globes Caitlin Malloy

University of Arkansas, Fayetteville ScholarWorks@UARK Architecture Undergraduate Honors Theses Architecture 5-2017 Image and Perception of the Top Five American Tourist Cities as Represented by Snow Globes Caitlin Malloy Follow this and additional works at: http://scholarworks.uark.edu/archuht Part of the American Popular Culture Commons, Architectural History and Criticism Commons, Marketing Commons, Other Architecture Commons, and the Tourism and Travel Commons Recommended Citation Malloy, Caitlin, "Image and Perception of the Top Five American Tourist Cities as Represented by Snow Globes" (2017). Architecture Undergraduate Honors Theses. 19. http://scholarworks.uark.edu/archuht/19 This Thesis is brought to you for free and open access by the Architecture at ScholarWorks@UARK. It has been accepted for inclusion in Architecture Undergraduate Honors Theses by an authorized administrator of ScholarWorks@UARK. For more information, please contact [email protected], [email protected]. IMAGE AND PERCEPTION OF THE TOP FIVE AMERICAN TOURIST CITIES AS REPRESENTED BY SNOW GLOBES A thesis submitted in partial fulfillment of the requirements of the Honors Program of the Department of Architecture in the School of Architecture + Design Caitlin Lee Malloy May 2017 University of Arkansas at Fayetteville Professor Frank Jacobus Thesis Director Professor Windy Gay Doctor Ethel Goodstein-Murphree Committee Member Committee Member ACKNOWLEDGEMENTS I am so grateful for my time at the Fay Jones School of Architecture + Design – during the past five years, I have had the opportunity to work with the best faculty and have learned so much. My thesis committee in particular has been so supportive of my academic endeavors. My deepest appreciation for my committee chair, Frank Jacobus. -

John Hancock 600000 Visitors Aon Center Unlimited

Aon iconic Pathwayto Possible Chicago, IL Lakeshore east facts Lakeshore East N Cityfront Plaza Dr r D r e w E Hubbard St o L e r N Park Dr N Rush St N New St o e 13,210,000 SF v E Lower No A rth W ater St E North Water St office space n N Wabash Ave t a e S N McClurg Ct zi g E Kin i h N Lake Sh c i 41 r M E River Dr we Chicago River o N Columbus Dr 63,790 L N business population e v A n E Irv Kupcinet Brg E Low W er W l a acker D cker r e Dr ga i v e h L c Chicago i E W e ack M er c Se 8,063 rvi E Wacker Dr i ce Le r vel v E Wacker Dr e r residential units e p p S U n o N N s Breakwater Acc t e t S E Waterside Dr Dr N E Wacker Pl E South Water St N Field Dr s 3,839Lake E Lower South Water St u b hotelMichigan rooms m E South Water St N Westshore Dr u l E Haddock Pl o C N r N Harbor Dr e Lake Shore L w t a e o k C r b v East Park N H e L a d o A S n 1,532,565 SF r E Lake S t N N Park Dr h a h S l s o r e y a SF New Developments a r t r i b e E Benton Pl v r G a i o D N Field Blvd c N W h e r t u N L A E Benton Pl e T 41 v I e S l N A N Stetson Ave N Beaubien Ct $124,000 R T Average INcome o g E Lower Randolph St E R andolph St a t c N Upper Columbus Dr S h St i E Upper Randol p h E Randolp h E Randolph St C N Cultural M Millenium Grant i Center c h 15,000 i Park Park g an Daily Park Visitors A v Date: 8/20/2015 e E Washington St N Columbus Dr Miles 0 0.025 0.05 0.075 0.1 2 Data contained herein was compiled from sources deemed to be reliable. -

Downtown Chicago Multifamily Development Pipeline

CBRE Q1 2020 DOWNTOWN CHICAGO MULTIFAMILY DEVELOPMENT PIPELINE AS OF APRIL 2020 Q1 2020 DOWNTOWN CHICAGO MULTIFAMILY DEVELOPMENT PIPELINE # Project Name Submarket Developer/Equity Status Delivery Date Units 2021 RENTAL DELIVERIES 1 One Chicago Square River North JDL / Wanxiang U/C 20 21 795 2 AMLI 808 Old Town AMLI U/C 20 21 297 3 3300 N Clark* Lakeview Blitzlake Partners U/C 20 21 140 4 Pilsen Gateway Pilsen Cedar Street / Origin U/C 20 21 202 5 Parkline Loop Moceri / Rozak U/C 20 21 190 6 300 N Michigan Loop Magellan / Sterling Bay U/C 20 21 289 7 Cascade Lakeshore East Magellan / Lend Lease U/C 20 21 503 8 Old Town Park III (1100 N Wells St) Near North Onni U/C 20 21 456 9 Triangle Square* Bucktown Belgravia / Lennar U/C 20 21 300 Subtotal 2021 3,172 2020 RENTAL DELIVERIES 10 740 N Aberdeen River West Fifield U/C 2020 188 11 The Grand River North Onni U/C 2020 356 12 Aspire* South Loop Draper & Kramer Inc. U/C 2020 275 13 1900 West Lawrence* Ravenswood Springbank U/C 2020 59 14 Oak and Larrabee Near North Brinshore Development U/C 2020 104 15 2405 W Hutchinson* Lincoln Square KR Developments U/C 2020 48 16 Motif on Belden* Logan Square Inland U/C 2020 100 17 128 S Laflin West Loop Michigan Avenue RE Group U/C 2020 52 18 2701 W Armitage* Logan Square Eco Development U/C 2020 59 19 Edge on Broadway* Edgewater City Pads Leasing Q2 2020 105 20 Porte West Loop The John Buck Company / Lend Lease Leasing Q2 2020 586 21 Logan Apartments* (2500 N Milwaukee) Logan Square Fifield / Terraco Inc Leasing Q2 2020 220 22 Imprint South Loop CMK Leasing -

Typologies and Evaluation of Outdoor Public Spaces at Street Level of Tall Buildings in Chicago

TYPOLOGIES AND EVALUATION OF OUTDOOR PUBLIC SPACES AT STREET LEVEL OF TALL BUILDINGS IN CHICAGO Abstract Authors Zahida Khan and Peng Du Outdoor public spaces are key to human interactions, promoting Illinois Institute of Technology public life in cities. The constant increase in world population has led Keywords to increased tall urban conditions making the study of outdoor public Public spaces, tall buildings, urban forms, rating system spaces around tall buildings very popular. This paper outlines typol- ogies for outdoor public spaces occurring at street level of tall build- ings in downtown Chicago, the birthplace of skyscrapers and an ideal case study for an American city. The study uses online data archives, Google Maps, and on-site surveys as research techniques for the analysis. The result depicts around 50% of all the tall buildings in Chicago foster public life at its street level through public spaces. The other key finding is the outline of seven typologies based on their position around the tall building. Further, a comparative analysis is conducted using one example of each typology based on three crite- ria adopted from ‘Project for Public Spaces,’ namely (1) Accessibility; (2) Design and Comfort, and (3) Users and Activities. Prometheus 04 Buildings, Cities, and Performance, II Introduction outdoor public spaces, including: (A) Accessibility, (B) Design & Comfort, (C) Users & Activities, (D) Environ- Outdoor public spaces at street level of tall buildings play mental Sustainability, and (E) Sociable. The scope of this a significant role in sustainable city development. The research is limited to the first three design criteria since rapid increase in world population and constant growth of the last two require a bigger timeframe and is addressed urbanization has led many scholars to support Koolhaas’ for future research. -

Introduction 2019-2022 Doormen Agreement.Pub

FOR ABOMA MEMBER USE ONLY Issued November 2019 Apartment Building Owners and Managers Association of Illinois COLLECTIVE BARGAINING AGREEMENT BY AND BETWEEN APARTMENT BUILDING OWNERS AND MANAGERS ASSOCIATION OF ILLINOIS and SERVICE EMPLOYEES INTERNATIONAL UNION, LOCAL 1 PROPERTY SERVICE DIVISION for the period DECEMBER 1, 2019 THROUGH NOVEMBER 30, 2022 Covering Doorstaff, Receiving Room Employees and Others as defined in Article I INTRODUCTION This booklet is exclusively for the use of ABOMA Members and contains the following: • Pages 1 through 27 Full Collective Bargaining Agreement by and between ABOMA and SEIU Local 1, Property Service Division Covering Doorstaff Receiving Room Employees and Others as defined in Article I for the period of December 1, 2019 through November 30, 2022 • Page 24 Letter of Agreement – Drug and Alcohol Policies • Page 25 Letter of Agreement – Subcontracting • Page 26 and 27 Memorandum of Agreement relating to Sub contracting and sample of Contractor DSMOA SCHEDULE A Pages 1-3 (NIPF) The Buildings (Employers) identified in Schedule A of this Agreement shall contribute for all regular Employees to the SEIU National Industry Pension Fund (hereinafter referred to as the "NIPF") in order to provide retirement benefits for eligible Employees in accordance with the terms of the NIPF. SCHEDULE B Pages 1-3 (401K Pension Savings Plan) The Buildings (Employers) identified in Schedule B of this Agreement shall contribute for all regular employees to the SEIU Local 1 401(k) Savings Plan in order to provide retirement benefits for eligible Employees in accordance with the terms of the 401(k) Plan. SCHEDULE C Page 1 (DSMOA NIPF) The Buildings and sub-contractors (Employers) identified in Schedule C of this Agreement shall contribute for all regular Employees to the SEIU National Industry Pension Fund (hereinafter referred to as the "NIPF") in order to provide retirement benefits for eligible Employees in accordance with the terms of the NIPF.