Bilibili Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ipo Analysis

IPO ANALYSIS Zscaler Research on potential upcoming IPOs from Bilibili Spotify selected candidate companies. March 2018 VentureDeal Zscaler Files Terms For $110 Million IPO Quick Take Zscaler (ZS) intends to raise $110 million in a U.S. IPO, according to an amended S-1/A regulatory filing. The company has developed a suite of cloud security software offerings for the enterprise market. ZS management is proposing to price the IPO at a rich valuation and without demonstrating a path to profitability. My opinion is to AVOID the IPO at the current price. Perhaps institutional buyers will persuade management of their excessive valuation expectations. Alternatively, if the IPO fizzles, interested investors may be able to pick up a bargain post-IPO. Company Recap San Jose, California-based Zscaler was founded in 2007 to offer a range of internet and hybrid security capabilities to businesses of all sizes. Management is headed by co-founder and CEO Jay Chaudhry, who was previously Chief Strategy Officer at Secure Computing and founder & CEO of CipherTrust. The company has developed a robust partner network for both referrals & resellers and internet service providers. Investors have funded $148 million in several rounds and include TPG Capital (8.7% pre-IPO). CEO Chaudhry and affiliates own 54.3% of company stock pre-IPO. Technology Zscaler has created a suite of cloud security solutions in the following categories: Zscaler Internet Access • Secure Web Gateway • Cloud Firewall • Cloud Sandbox • Bandwidth Control • Data Loss Prevention Zscaler Private Access • For Amazon Web Services (AMZN) • For Microsoft Azure (MSFT) Zscaler Platform • Cloud Architecture • SSL Inspection • Data Privacy & Security • Zscaler App Below is a brief company promotional video: (Source:Zscaler) Market According to a December 2017 Gartnermarket research report, it forecasted that global security technology spending would reach $96 billion in 2018, representing an increase of 8% over 2017. -

AVG Android App Performance and Trend Report H1 2016

AndroidTM App Performance & Trend Report H1 2016 By AVG® Technologies Table of Contents Executive Summary .....................................................................................2-3 A Insights and Analysis ..................................................................................4-8 B Key Findings .....................................................................................................9 Top 50 Installed Apps .................................................................................... 9-10 World’s Greediest Mobile Apps .......................................................................11-12 Top Ten Battery Drainers ...............................................................................13-14 Top Ten Storage Hogs ..................................................................................15-16 Click Top Ten Data Trafc Hogs ..............................................................................17-18 here Mobile Gaming - What Gamers Should Know ........................................................ 19 C Addressing the Issues ...................................................................................20 Contact Information ...............................................................................21 D Appendices: App Resource Consumption Analysis ...................................22 United States ....................................................................................23-25 United Kingdom .................................................................................26-28 -

Prospectus Supplement and Plan to File a Final Prospectus Supplement with the SEC to Register the Sale of Shares Under the U.S

ai16158914263_Project S6 cover_ENG_03_20mm spine HR.pdf 1 16/3/2021 18:43:46 GLOBAL OFFERING Stock Code: 9626 (A company controlled through weighted voting rights and incorporated in the Cayman Islands with limited liability) Stock Code: 9626 Stock Joint Sponsors, Joint Global Coordinators, Joint Bookrunners, and Joint Lead Managers Joint Bookrunners and Joint Lead Managers Joint Lead Managers IMPORTANT If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. Bilibili Inc. (A company controlled through weighted voting rights and incorporated in the Cayman Islands with limited liability) GLOBAL OFFERING Number of Offer Shares under the Global Offering : 25,000,000 Offer Shares (subject to the Over-allotment Option) Number of Hong Kong Offer Shares : 750,000 Offer Shares (subject to adjustment) Number of International Offer Shares : 24,250,000 Offer Shares (subject to adjustment and the Over-allotment Option) Maximum Public Offer Price : HK$988.00 per Offer Share, plus brokerage of 1.0%, SFC transaction levy of 0.0027% and Hong Kong Stock Exchange trading fee of 0.005% (payable in full on application in Hong Kong dollars and subject to refund) Par Value : US$0.0001 per Share Stock Code : 9626 Joint Sponsors, Joint Global Coordinators, Joint Bookrunners, and Joint Lead Managers Joint Bookrunners and Joint Lead Managers Joint Lead Managers Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. -

System: Pipeline Performance Enhancement

Cross Cultural Analysis System Improvements Guandong Liu Yiyang Zeng Columbia University Columbia University [email protected] [email protected] 1 Introduction Cross-cultural analysis investigates the new task of determining which textual tags are preferred by different affinity groups for news and related videos. We use this knowledge to assign new group-specific tags to other videos of the same event that have arisen elsewhere. We map visual and multilingual textual features into a joint latent space using reliable visual cues, and determine tag relationships through deep canonical correlation analysis (DCCA). We are interested in any international events such as epidemics and transportation disasters and detect country-specific tags from different countries’ news coverage [1]. Our current pipeline is able to collect data, preprocess data, and analyze data. This semester, we investigated and improved system performances in different aspects to make it more reliable and flexible. This report consists of two parts: the first part gives a thorough overview to the whole pipeline and the second part talks about several bug fixes and performance improvements of the current system. 2 Pipeline User Manual This section gives a thorough overview to the whole pipeline and goes through each step with AlphaGo in Chinese and English task as an example. 2.1 Get Video Metadata The pipeline starts from getting video metadata from various sources. In our experiments, we got video metadata about AlphaGo from Chinese sources (Tencent, Iqiyi, Youku, BiliBili) and English source (YouTube). Note that to get video metadata from YouTube, one must first enable YouTube Data API and get own API credentials (key.txt is the API credentials). -

Reaching China's Video Crowd with the Power of Bilibili

www.nativex.com REACHING CHINA’S VIDEO CROWD WITH THE POWER OF BILIBILI. The YouTube of China 01 02 What is Bilibili? Key facts & stats 03 04 Fun facts about Bilibili The GenZ community hub: Bilibili user profiles & demographics 05 06 Promoting your apps Bilibili’s benefits or brands on Bilibili in a nutshell 07 08 Advertising on Bilibili: How we can help step-by-step guide 01 WHAT IS BILIBILI? What is Bilibili? Bilibili is one of China’s hottest emerging video platforms. Having almost tripled its audience in the last couple of years, Bilibili is now an entertainment power house that has expanded outside its ACG (anime, comics, games) roots to include support for e-commerce, technology, and lifestyle content. Bilibili’s focus on user generated content, along with innovative features like bullet comments, make it one of the most used video apps by China’s youth today. Thanks to its similar users, features, and functionality, some say that Bilibili is the YouTube of China. Bilibili is in a unique position on the Chinese market, as it’s backed by both Alibaba and Tencent (7.2% and 13.3% of shares, respectively), as well as Japanese giant Sony (4.98%). 01 02 KEY FACTS & STATS Key facts & stats Bilibili has shown incredible growth over the past few years. Let’s look at some of their most recent numbers from their Q1 2020 financial results: Mobile vs. Desktop user distribution: 172.4 million Total MAUs 88 % 12% (70% year-on-year growth) 156.4 million 50.8 million 13.4 million Mobile MAUs DAUs Monthly Paying Users (77% year-on-year growth) (69% year-on-year growth) (134% year-on-year growth) $327million Net Revenue 87minutes (69% year-on-year growth) average daily time spent on the app 02 03 FUN FACTS ABOUT BILIBILI 1. -

Bilibili (BILI): a Leader in ACG with Room to Grow

JAGUAR MEDIA SEPT 8TH, 2020 “CHINESE TECH DEMYSTIFIED” SERIES – EPISODE 5 Bilibili (BILI): A leader in ACG with room to grow Bilibili is often labeled as China’s version of YouTube, but that comparison is only half-accurate. Fundamentally, it is a video sharing and vlogging platform. But if we dig a little deeper, we will find that it caters almost exclusively to a dedicated under-30’s crowd while shunning older audiences, and the video content is overwhelmingly focused on animation, comics, and games (or ACG in short), fashion, pop culture, and music. No news, no politics, no academic discourse, no finance, none of that mundane stuff. Bilibili was founded in 2009 with the intention of being a worthy ACG competitor to AcFun (recall AcFun is the former parent company of DouYu). Bilibili’s founder Xu Yi was formerly a top user with a huge following on AcFun, but grew increasingly frustrated over time with community and website-related issues. And following a series of high-profile disagreements with AcFun management, he decided to sever ties and create Bilibili on the back of funding from now-CEO Chen Rui, a games/animation-loving billionaire investor who currently owns over 20% of the company. Before long, Bilibili saw significant traffic, enough to challenge AcFun’s. Due to this rivalry and history, Bilibili is commonly referred to by the Chinese internet community as “B Site” or “Station B”, while AcFun is nicknamed “A Site” or “Station A”. Fun fact: The word “Bilibili” doesn’t have any literal meaning. Rather, it is a playful reference to a main character from A Certain Scientific Railgun, a popular comic/animation series at the time, whereby “Bilibili” is the sound she makes when firing her weapon. -

Chinese Companies Listed on Major U.S. Stock Exchanges

Last updated: October 2, 2020 Chinese Companies Listed on Major U.S. Stock Exchanges This table includes Chinese companies listed on the NASDAQ, New York Stock Exchange, and NYSE American, the three largest U.S. exchanges.1 As of October 2, 2020, there were 217 Chinese companies listed on these U.S. exchanges with a total market capitalization of $2.2 trillion.2 3 Companies are arranged by the size of their market cap. There are 13 national- level Chinese state-owned enterprises (SOEs) listed on the three major U.S. exchanges. In the list below, SOEs are marked with an asterisk (*) next to the stock symbol.4 This list of Chinese companies was compiled using information from the New York Stock Exchange, NASDAQ, commercial investment databases, and the Public Company Accounting Oversight Board (PCAOB). 5 NASDAQ information is current as of February 25, 2019; NASDAQ no longer publicly provides a centralized listing identifying foreign-headquartered companies. For the purposes of this table, a company is considered “Chinese” if: (1) it has been identified as being from the People’s Republic of China (PRC) by the relevant stock exchange; or, (2) it lists a PRC address as its principal executive office in filings with U.S. Securities and Exchange Commission. Of the Chinese companies that list on the U.S. stock exchanges using offshore corporate entities, some are not transparent regarding the primary nationality or location of their headquarters, parent company or executive offices. In other words, some companies which rely on offshore registration may hide or not identify their primary Chinese corporate domicile in their listing information. -

Mobile Security 2015

Product Review: Mobile Security 2015 www.av-comparatives.org AV-Comparatives Mobile Security Review Language: English August 2015 Last revision: 17th September 2015 www.av-comparatives.org Product Review: Mobile Security 2015 www.av-comparatives.org Contents Overview ............................................................... 6 Products tested ...................................................... 8 Battery usage ......................................................... 9 Protection against Android malware ......................... 11 AVC UnDroid Analyser ............................................. 11 Test Set & Test Results ........................................... 12 Android Security .................................................... 14 AVG AntiVirus ........................................................ 16 AhnLab V3 Mobile Security ...................................... 19 Antiy AVL for Android ............................................. 22 Avast Mobile Security ............................................. 24 Avira Antivirus Security .......................................... 28 Baidu Mobile Guard ................................................ 31 Bitdefender Mobile Security and Antivirus ................. 34 CheetahMobile Clean Master .................................... 37 CheetahMobile CM Security Antivirus ........................ 40 ESET Mobile Security .............................................. 44 G Data Internet Security ......................................... 47 Kaspersky Internet Security .................................... -

Flywheel Models + Iqiyi (NASDAQ: IQ) an Investment Case Study by Hayden Capital Valuex Vail | June 27-29, 2018

Flywheel Models + iQiyi (NASDAQ: IQ) An Investment Case Study By Hayden Capital ValueX Vail | June 27-29, 2018 Hayden Capital 79 Madison Ave, 3rd Floor New York, NY. 10016 Office: (646) 883-8805 Mobile: (513) 304-3313 Email: [email protected] Disclaimer These materials shall not constitute an offer to sell or the solicitation of an offer to buy any interests in any fund or account managed by Hayden Capital LLC (“Hayden Capital”) or any of its affiliates. Such an offer to sell or solicitation of an offer to buy will only be made pursuant to definitive subscription documents between a fund and an investor. The fees and expenses charged in connection with the investment may be higher than the fees and expenses of other investment alternatives and may offset profits. No assurance can be given that the investment objective will be achieved or that an investor will receive a return of all or part of his or her investment. Investment results may vary substantially over any given time period. Reference and comparisons are made to the performance of other indices (together the “Comparative Indexes”) for informational purposes only. Hayden Capital’s investment program does not mirror any of the Comparative Indexes and the volatility of Hayden Capital’s investment strategy may be materially different than that of the Comparative Indexes. The securities or other instruments included in the Comparative Indexes are not necessarily included in Hayden Capital’s investment program and criteria for inclusion in the Comparative Indexes are different than those for investment by Hayden Capital. The performance of the Comparative Indexes was obtained from published sources believed to be reliable, but which are not warranted as to accuracy or completeness. -

Chinese Companies Listed on Major U.S. Stock Exchanges

Last updated: May 5, 2021 Chinese Companies Listed on Major U.S. Stock Exchanges This table includes Chinese companies listed on the NASDAQ, New York Stock Exchange, and NYSE American, the three largest U.S. exchanges. i As of May 5, 2021, there were 248 Chinese companies listed on these U.S. exchanges with a total market capitalization of $2.1 trillion. On October 2, 2020, when this table was last updated, there were 217 companies with a total market capitalization of $2.2 trillion. In the list below, newly added companies are marked with a section symbol (§) next to the stock symbol. ii Companies are arranged by the size of their market cap. There are eight national-level Chinese state-owned enterprises (SOEs) listed on the three major U.S. exchanges. In the list below, SOEs are marked with an asterisk (*) next to the stock symbol. iii Since this table was last updated in October 2020, 17 Chinese companies have delisted. Two companies currently trade over the counter: Kingold Jewelry (KGJI, $3 million market cap) and state-owned Guangshen Railway (GSHHY, $2,256 million market cap). The 17 delisted companies also include four companies targeted by the Executive Order 13959 (“Addressing the Threat from Securities Investments That Finance Communist Chinese Military Companies”), which prohibited investment in Communist Chinese Military Companies. These are: China Unicom, China Telecom, China Mobile, and CNOOC Limited. In addition, Semiconductor Manufacturing International Corporation (SMIC) stopped trading over the counter as a result of the order.1 The remaining U.S.-listed company subject to the order is Luokung Technology Corp. -

Key Trends in China's Online Video Industry

KEY TRENDS IN CHINA’S ONLINE VIDEO INDUSTRY April 2021 1 ONLINE VIDEO PENETRATION APPROACHES 94% OF INTERNET USERS TRACKING INTERNET & ONLINE VIDEO USER TRENDS Penetration of Internet Users 94% 89% 62% 1,200 989 1,007 927 942 1,000 880 873 900 829 802 725 800 709 617 624 549 600 501 499 Total users (mil.) 400 200 0 2018 2019 2020 Q1 2021 Internet Users Online Video Users Short Video Users Livestreaming Users Source: Company data, Media Partners Asia 2 SHORT VIDEO DRIVING CONSUMPTION SHARE OF VIDEO USER TIME SPENT 100% 9% 9% 22% 19% 20% 3% 3% 90% 24% 3% 3% 3% 3% 2% 80% 2% 3% 2% 3% 3% 8% 8% 4% 2% 5% 10% 9% 70% 13% 8% 9% 12% 4% 5% 60% 15% 66% Of 24% 12% 50% 23% 27% 27% Streaming Time 19% Spent On Top 3 40% 20% Short Video 30% 27% 28% 15% Platforms 20% 33% 34% % of Online Video Time Spent Time Video Online of % 26% 14% 10% 9% 15% 0% 1% 0% 2016 2017 2018 2019 2020 Q1 2021 Douyin Kuaishou WeChat Channel Video iQIYI Tencent Video Youku Mango TV Bilibili Others Source: Company data, Media Partners Asia 3 RATE INCREASES SUPPORT SVOD ARPUS, MORE UPSIDE ON AD ARPUS MONTHLY ARPU PER DAU (KEY DIGITAL COMPANIES) ADVERTISING REVENUE PER DAU (KEY VIDEO PLATFORMS) 35 70 30 60 Ad monetization per DAU for most video platforms Platforms such as Bilibili 25 50 is still fairly low, but and WeChat Channel Video upside may be limited due still significantly 40 20 to slowing industry undermonetized US$ US$ 65.1 growth 15 Recent rate hikes led 30 by iQIYI and Tencent Low monthly ARPU implies upside 21.6 10 Video on membership fees for most 20 Chinese platforms Average 5 10 20.4 7.5 12.3 11.8 10.9 10.7 4.9 6.8 3.8 2.9 2.8 2.5 0 1.0 0 Alibaba Tencent Baidu iQIYI Bilibili Kuaishou Weibo Douyin Youku Mango Kuaishou iQIYI Tencent Bilibili WeChat TV Video Channel Note: Video 1) Monthly ARPU reflects consumer spend, and excludes advertising. -

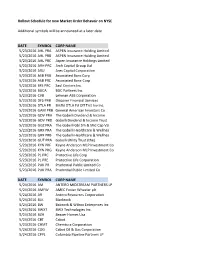

Rollout Schedule for New Market Order Behavoir on NYSE Additional

Rollout Schedule for new Market Order Behavoir on NYSE Additional symbols will be announced at a later date DATE SYMBOL CORP NAME 5/23/2016 AHL PRA ASPEN Insurance Holding Limited 5/23/2016 AHL PRB ASPEN Insurance Holding Limited 5/23/2016 AHL PRC Aspen Insurance Holdings Limited 5/23/2016 ARH PRC Arch Capital Group Ltd 5/23/2016 ARU Ares Capital Corporation 5/23/2016 ASB PRB Associated Banc Corp 5/23/2016 ASB PRC Associated Banc-Corp 5/23/2016 BFS PRC Saul Centers Inc. 5/23/2016 BGCA BGC Partners Inc. 5/23/2016 CVB Lehman ABS Corporation 5/23/2016 DFS PRB Discover Financial Services 5/23/2016 DTLA PR Brkfld DTLA Fd Off Trst Inv Inc. 5/23/2016 GAM PRB General American Investors Co 5/23/2016 GDV PRA The Gabelli Dividend & Income 5/23/2016 GDV PRD Gabelli Dividend & Income Trust 5/23/2016 GGZ PRA The Gabelli Gbl Sm & Mid Cap Val 5/23/2016 GRX PRA The Gabelli Healthcare & Wellnes 5/23/2016 GRX PRB The Gabelli Healthcare & Wellnes 5/23/2016 GUT PRA Gabelli Utility Trust (the) 5/23/2016 KYN PRF Kayne Anderson MLP Investment Co 5/23/2016 KYN PRG Kayne Anderson MLP Investment Co 5/23/2016 PL PRC Protective Life Corp 5/23/2016 PL PRE Protective Life Corporation 5/23/2016 PUK PR Prudential Public Limited Co 5/23/2016 PUK PRA Prudrntial Public Limited Co DATE SYMBOL CORP NAME 5/24/2016 AM ANTERO MIDSTREAM PARTNERS LP 5/24/2016 AMFW AMEC Foster Wheeler plc 5/24/2016 AR Antero Resources Corporation 5/24/2016 BLK Blackrock 5/24/2016 BW Babcock & Wilcox Enterprises Inc 5/24/2016 BWXT BWX Technologies Inc.