Dollar General/Dollar Tree/Family Dollar Case Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

What's Next for Ukpound Shops?

February 3, 2015 February 3, 2015 What’s Next For UK Pound Shops? Major UK pound shop chains have seen revenues surge in the post-recession years. The economic slump and the Woolworths failure paved the way for this segment’s rapid expansion of stores. With further expansion expected, we think the segment is looking increasingly crowded. Some players are now eying international markets in their bid for growth. DEBORAH WEINSWIG Executive Director–Head Global Retail & Technology Fung Business Intelligence Centre [email protected] New york: 646.839.7017 Fung Business Intelligence Centre (FBIC) publication: UK POUND SHOPS 1 Copyright © 2015 The Fung Group, All rights reserved. February 3, 2015 What’s Next For UK Pound Shops? THE POUND SHOP BOOM Variety-store retailers have proliferated rapidly in the UK, mirroring the store-expansion boom of discount grocery chains (notably Aldi and Lidl), as the low-price, no-frills formula has found particular resonance in Britain’s era of sluggish economic growth. This retail segment encompasses chains like Poundland, 99p Stores and Poundworld, which sell all of their products at fixed price points. Similar to the dollar chains Dollar General and Family Dollar in the US, everything in the pound stores sells for £1 (or 99p) and the goods are bought cheaply in bulk. The group also includes chains with more flexible pricing schemes. Those include B&M Bargains, Home Bargains and Poundstretcher. For both types of stores, the offerings are heavy on beauty and personal care, household fast-moving consumer goods (FMCGs) and food and beverages (particularly confectionery). Other categories typically include do-it-yourself (DIY) and automotive accessories, pet products and seasonal goods. -

Equity Impacts of Dollar Store Vaccine Distribution

EQUITY IMPACTS OF DOLLAR STORE VACCINE DISTRIBUTION By Judith A. Chevalier, Jason L. Schwartz, Yihua Su, and Kevin R. Williams April 2021 COWLES FOUNDATION DISCUSSION PAPER NO. 2280 COWLES FOUNDATION FOR RESEARCH IN ECONOMICS YALE UNIVERSITY Box 208281 New Haven, Connecticut 06520-8281 http://cowles.yale.edu/ Equity Impacts of Dollar Store Vaccine Distribution * Judith A. Chevalier,Yale School of Management and NBER Jason L. Schwartz, Yale School of Public Health Yihua Su, Yale School of Public Health Kevin R. Williams, Yale School of Management and NBER April 2, 2021 Abstract We use geospatial data to examine the unprecedented national program currently underway in the United States to distribute and administer vaccines against COVID- 19. We quantify the impact of the proposed federal partnership with the company Dollar General to serve as vaccination sites and compare vaccine access with Dollar General to the current Federal Retail Pharmacy Partnership Program. Although dollar stores have been viewed with skepticism and controversy in the policy sector, we show that, relative to the locations of the current federal program, Dollar General stores are disproportionately likely to be located in Census tracts with high social vulnerability; using these stores as vaccination sites would greatly decrease the distance to vaccines for both low-income and minority households. We consider a hypothetical alternative partnership with Dollar Tree and show that adding these stores to the vaccination program would be similarly valuable, but impact different geographic areas than the Dollar General partnership. Adding Dollar General to the current pharmacy partners greatly surpasses the goal set by the Biden administration of having 90% of the popu- lation within 5 miles of a vaccine site. -

HD [email protected] Or by Writing to the Directors at the Following Address

THE HOME DEPOT PROXY STATEMENT AND NOTICE OF 2020 ANNUAL MEETING OF SHAREHOLDERS Thursday, May 21, 2020 at 9:00 a.m., Eastern Time COBB GALLERIA CENTRE, ATLANTA, GA Table of Contents INVESTOR FACTSHEET Strategy Our One Home Depot strategy aims to deliver shareholder value and grow our market share by providing best- in-class customer service through a seamless, interconnected shopping experience for our customers. We are continuously improving our online and in-store experience and providing enhanced training for our associates. In addition, to ensure we are the product authority in home improvement, we strive to provide unique and comprehensive product offerings, continued innovation, and exceptional convenience and value. To execute our strategy, we have committed approximately $11 billion over a multi-year period to investments in our stores, associates, interconnected and digital experience, pro customer experience, services business, supply chain, and product and innovation. Shareholder Return Principles Our first priority for our use of cash is investing in our business, as reflected by our One Home Depot strategy. Our use of the remainder of our cash is guided by our shareholder return principles: • Dividend Principle: Look to increase the dividend every year as we grow earnings • Return on Invested Capital Principle: Maintain a high return on invested capital, benchmarking all uses of excess liquidity against value created for shareholders through share repurchases • Share Repurchase Principle: After meeting the needs of the business, look to return excess cash to shareholders in the form of share repurchases Key Financial Performance Metrics Set forth below are key financial performance metrics for the indicated fiscal years. -

UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended July 31, 2015 Commission File Number: 001-11421 DOLLAR GENERAL CORPORATION (Exact name of Registrant as specified in its charter) TENNESSEE 61-0502302 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 100 MISSION RIDGE GOODLETTSVILLE, TN 37072 (Address of principal executive offices, zip code) Registrant’s telephone number, including area code: (615) 855-4000 Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes x No o Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. -

Annual Report Also Accompanies This Letter

ANNUAL MEETING ABOUT DOLLAR GENERAL Dollar General Corporation’s annual meeting of shareholders is scheduled for 9 a.m. Central Time on Dollar General Corporation has been delivering NET SALES (IN BILLIONS) Wednesday, May 27, 2020, at: value to shoppers for more than 80 years. Dollar $27.8 Goodlettsville City Hall Auditorium $25.6 General helps shoppers Save time. Save money. $23.5 105 South Main Street, Goodlettsville, TN 37072 ® $22.0 Every day! by o ering products that are frequently $20.4 used and replenished, such as food, snacks, health Shareholders of record as of March 19, 2020 are and beauty aids, cleaning supplies, basic apparel, entitled to vote at the meeting. housewares and seasonal items at everyday low prices in convenient neighborhood locations. NYSE: DG 2015 2016 2017 2018 2019 Dollar General operated 16,278 stores in 44 states The common stock of Dollar General Corporation is as of January 31, 2020. In addition to high-quality traded on the New York Stock Exchange under the private brands, Dollar General sells products ENDING STORE COUNT trading symbol “DG.” The number of shareholders of from America’s most-trusted manufacturers such 16,278 record as of March 19, 2020 was 2,617. 15,370 Visit www.dollargeneral.com as Clorox, Energizer, Procter & Gamble, Hanes, 14,534 to learn more about Dollar General Coca-Cola, Mars, Unilever, Nestle, Kimberly-Clark, 13,320 STOCK PERFORMANCE GRAPH 12,483 and shop online. Kellogg’s, General Mills, and PepsiCo. The graph below compares Dollar General Corporation’s cumulative total shareholder return on common stock STORES with the cumulative total returns of the S&P 500 index STORES IN 44 STATES DISTRIBUTION CENTER and the S&P Retailing index. -

Dollar General

NNN Dollar General the strongest dollar store chain High growth metro area REPRESENTATIVE PHOTO For more info on this opportunity please contact: very low unemployment RICK SANNER BOB SANNER [email protected] | (415) 274-2709 [email protected] | (415) 274-2717 rent increases CA BRE# 01792433 CA BRE# 00869657 JOHN ANDREINI CHRIS KOSTANECKI just opened [email protected] | (415) 274-2715 [email protected] | (415) 274-2701 118 Riley Ave, Ogden, KS 66517 CA BRE# 01440360 CA BRE# 01002010 In conjuction with KS Licensed Broker: Phil Bundy [email protected] | (316) 686-9292 Capital Pacific collaborates. Click here to meet the rest of our San Francisco team. NNN PROPERTY IN OGDEN, KANSAS Investment Highlights New 15-year primary term lease with four (4) five-year options with a 10% rental increase at the beginning of each option period. There is also a 3% rent increase at year 11. Ogden is a suburb of Manhattan, Kansas (home of Kansas State University), and is a part of the Manhattan MSA. The subject Representative Photos property is also quite close to one of the US Army’s largest bases, Ft. Riley. PRICE ............ $1,339,308 RENTABLE SF .........9,100 SF CAP RATE ............6.65% YEAR BUILT ..........2014 LEASE TYPE ..........NNN INVESTMENT GRADE CREDIT Dollar General’s credit is BBB- and the company’s credit rating has been raised four times since 2009. It has a better credit rating than both of its large competitors (See more information later in this offering) STRONG TENANT During fiscal 2014, Dollar -

Annual Report

Outside Back Cover Outside Front Cover 8.25”(W) x 10.875”(H) 8.25”(W) x 10.875”(H) ANNUAL REPORT WELCOME TO YOUR NEW COMMUNITY biglots.com 337376_Big Lots AR17_CVR.indd 1 4/13/18 2:49 PM Inside Front Cover Inside Back Cover 8.25”(W) x 10.875”(H) 8.25”(W) x 10.875”(H) About Our Company Headquartered in Columbus, Ohio, Big Lots, Inc. NOTICE OF ANNUAL MEETING (NYSE: BIG) is a community retailer operating more than The Annual Meeting of 1,400 BIG LOTS stores in 47 states, dedicated to friendly Shareholders will be held at service, trustworthy value, and affordable solutions in 9:00 a.m. EDT on Thursday, every season and category — furniture, food, decor, and May 31, 2018, at our corporate headquarters, 4900 East Dublin more. We exist to serve everyone like family, providing Granville Road, Columbus, a better shopping experience for our customers, valuing Ohio 43081. Whether or not and developing our associates, and creating growth you plan to attend, you are encouraged to vote as soon for our shareholders. Big Lots supports the communities as possible. In accordance it serves through the Big Lots Foundation, a charitable with the accompanying proxy organization focused on four areas of need: hunger, statement, shareholders who attend the meeting may housing, healthcare, and education. For more information withdraw their proxies and about the Company, visit www.biglots.com. vote in person if they so desire. Who is Big Lots? JENNIFER, OUR Transfer Agent & Registrar Investment Inquiries NYSE Trading Symbol We’re a Community Retailer. -

Family Dollar for Sale 414 Remi Trail (College Park Road) | Summerville, SC

Family Dollar for Sale 414 Remi Trail (College Park Road) | Summerville, SC Representative Photo Table of Contents FOR FURTHER INFORMATION 414 Remi Trail Hudson Rogers Summerville, SC office 843.203.1658 mobile 843.442.3978 Locator Map ..................................................................3 web [email protected] High Aerial .....................................................................4 Mid Aerial ......................................................................5 125-G Wappoo Creek Drive Site Aerial ......................................................................6 Charleston, SC 29412 Site Plan ........................................................................7 phone (843) 722.9925 fax (843) 722.9947 Elevations ......................................................................8 web twinriverscap.com Survey ............................................................................9 Property Information .................................................. 10 Charleston, SC ........................................................11,12 Tenant & Lease Information ...................................... 13 Financials .................................................................... 14 About Us ...................................................................... 15 Locator Map SUMMERVILLE, SC High Aerial STARBUCKS TRUE LOGOS. GENERATED BY CHI NGUYEN (CHISAGITTA) North Main St. VPD = 28,800 College Park Rd. SITE VPD = 11,700 Mid Aerial College Park Rd. VPD = 11,700 SITE Site Aerial SITE Site -

Dollar Stores Are Multiplying Rapidly

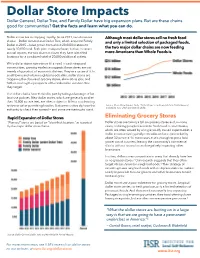

Dollar Store Impacts Dollar General, Dollar Tree, and Family Dollar have big expansion plans. But are these chains good for communities? Get the facts and learn what you can do. Dollar stores are multiplying rapidly. Since 2011, two dominant Although most dollar stores sell no fresh food chains — Dollar General and Dollar Tree, which acquired Family and only a limited selection of packaged foods, Dollar in 2015 — have grown from about 20,000 locations to nearly 30,000 total. Both plan to expand even further. In recent the two major dollar chains are now feeding annual reports, the two chains indicate they have identified more Americans than Whole Foods is. locations for a combined total of 20,000 additional outlets. While dollar stores sometimes fill a need in cash-strapped communities, growing evidence suggests these stores are not merely a byproduct of economic distress. They’re a cause of it. In small towns and urban neighborhoods alike, dollar stores are triggering the closure of grocery stores, eliminating jobs, and further eroding the prospects of the vulnerable communities they target. The dollar chains have thrived in part by taking advantage of lax land use policies. New dollar stores, which are generally smaller than 10,000 square feet, are often subject to little or no planning review or other permitting hurdles. But communities do have the Source: Chain Store Guide | Note: “Dollar Stores” combines data from Dollar General and Dollar Tree, which owns Family Dollar authority to check their spread — and some are starting to use it. Rapid Expansion of Dollar Stores Eliminating Grocery Stores “Planned” stores are based on “identified locations” as reported Dollar stores are taking a toll on grocery stores and, in many by the major dollar store chains. -

2021 CORPORATE SUSTAINABILITY REPORT Statements Contained Herein Asrepresenting the Company’S Asofanydate Views Subsequentto Thedate Ofthisreport

1 DOLLAR TREE I FAMILYD>LLM . CORPORATE 2021 SUSTAINABILITY REPORT TWO BRANDS, ENDLESS POSSIBILITIES Contents MISSION STATEMENT 2 CEO LETTER 3 WHO WE ARE 5 OUR ESG JOURNEY 9 COVID-19 RESPONSE 11 ENVIRONMENTAL STEWARDSHIP 16 SOCIAL IMPACT 25 PRODUCT SAFETY & SUPPLY CHAIN 36 GOVERNANCE & ETHICS 41 APPENDIX 50 Statements in this Corporate Sustainability Report and Dollar Tree, Inc.’s website regarding the company’s Environmental, Social, Governance (ESG) initiatives and future operating results, outlook, growth, plans, and business strategies, including statements regarding projected savings and anticipated improvements to the company’s business and ESG metrics as a result of its initiatives and programs, as well as any other statements that are not related to present facts or current conditions or that are not purely historical, constitute forward-looking statements. These forward-looking statements are based on the company’s historical performance and its plans, estimates, and expectations as of April 1, 2021. Forward- CORPORATE SUSTAINABILITY REPORT SUSTAINABILITYREPORT CORPORATE looking statements are not guarantees that the future results, plans, intentions, or expectations expressed or implied 2021 2021 by the company will be achieved. Matters subject to forward-looking statements involve known and unknown risks and uncertainties, including economic, legislative, regulatory, competitive, and other factors, which may cause actual financial or operating results, levels of activity, or the timing of events to be materially diferent than those expressed or implied by forward-looking statements. Important factors that could cause or contribute to such diferences include execution of the company’s plans and its success in realizing the benefits expected to result from its initiatives and programs, including its FAMILY DOLLAR FAMILY | sustainability initiatives, and the other factors set forth in Part I, “Item 1A. -

ECRM Ad Comparisons the LEADING PROVIDER of PROMOTIONAL DATA and BUSINESS INTELLIGENCE St

ECRM Ad Comparisons THE LEADING PROVIDER OF PROMOTIONAL DATA AND BUSINESS INTELLIGENCE St. Patrick’s Day Promotional Review 2013 versus 2014 Confidential and Proprietary to ECRM 1 METHODOLOGY Effective Ad Count Used in Study: Effective Ad Count gives partial credit to any product that shares an ad block with other products in order to provide more context in promotional analysis. For example: If 4 products are present in an ad block each will only receive a .25 count for that particular promotion. If 3 products are present each one receives .33 count. Time Periods: Current Year: 2/16/2014 - 3/22/2014 Prior Year: 2/17/2013 - 3/23/2013 Retailers Used in Representative Market Review: A & P, Albertson's - SoCal (SVU), Albertsons SOC, CVS, Dollar General, Family Dollar, Food Lion, Giant Eagle, Giant Food Landover, H.E.B., Jewel-Osco (NAI), Jewel-Osco (SVU), Kmart, Kroger CIN, Meijer, Rite Aid, Safeway Stores, Stater Bros, Super 1 Foods, Target Stores, Walgreens, Walmart-US, Winn Dixie. Representative Markets Used. Retailers Used in Promoted Price Study: Chicago Market Retailers: CVS, Dominick's Finer Foods, Food 4 Less, Meijer, Strack & Van Til, Target Stores, Ultra Foods. Media Type: Circular Promotions. Sampling Methodology: A typical basket of St. Patrick’s Day items was developed using the following categories: Beef, Cheese, Cheese Chunk/Block, Cordial, Deli Beef/Roast Beef, Deli Cheese, Dry Potatoes, Fingerling Potatoes, Fresh Cut Flowers, Grated Cheese, Imported Beer, Irish Whiskey, Other Vegetables, Petite Potatoes, Potato Chips, Red Potatoes, Russet Potatoes, Specialty Cheeses, White Potatoes, Yellow Potatoes and Bakery In-Store. The basket was used to identify pages containing St. -

RETAIL INVESTOR PRESENTATION Contents

SECOND QUARTER 2019 RETAIL INVESTOR PRESENTATION Contents Investment Thesis 4 Company Overview 5 Performance Track Record 10 Dependable Dividends 11 Portfolio Diversification 15 Asset Management & Real Estate Operations 22 Investment Strategy 25 Capital Structure and Scalability 28 Business Plan 32 Appendix 33 All data as of June 30, 2019 unless otherwise specified 2 Safe Harbor For Forward-Looking Statements Statements in this investor presentation that are not strictly historical are "forward-looking" statements. Forward-looking statements involve known and unknown risks, which may cause the company‘s actual future results to differ materially from expected results. These risks include, among others, general economic conditions, domestic and foreign real estate conditions, tenant financial health, the availability of capital to finance planned growth, continued volatility and uncertainty in the credit markets and broader financial markets, property acquisitions and the timing of these acquisitions, charges for property impairments, and the outcome of any legal proceedings to which the company is a party, as described in the company's filings with the Securities and Exchange Commission. Consequently, forward-looking statements should be regarded solely as reflections of the company's current operating plans and estimates. Actual operating results may differ materially from what is expressed or forecast in this investor presentation. The company undertakes no obligation to publicly release the results of any revisions to these forward-looking statements that may be made to reflect events or circumstances after the date these statements were made. 3 Investment Thesis Business model offers attractive total return with minimal cash flow volatility PROVEN TRACK RECORD OF RETURNS 16.4% Compound Average Annual Total Return Since ‘94 NYSE Listing 0.4 Beta vs.