Cpmg / Ka / Bg-Gpo/13/2003-2005

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cpmg / Ka / Bg-Gpo/13/2003-2005

The Karnataka Value Added Tax Act, 2003 Act 32 of 2004 Keyword(s): Assessment, Business, Capital Goods, To Cultivate Personally, Dealer, Export, Goods Vehicle, Import, Input Tax, Maximum Retail Price, Output Tax, Place of Business, Published, Registered Dealer, Return, Sale, State Representative, Taxable Sale, Tax Invoice, Tax Period, Taxable Turnover, Total Turnover, Works Contract Amendments appended; 5 of 2009, 32 of 2013, 54 of 2013, 5 of 2015 DISCLAIMER: This document is being furnished to you for your information by PRS Legislative Research (PRS). The contents of this document have been obtained from sources PRS believes to be reliable. These contents have not been independently verified, and PRS makes no representation or warranty as to the accuracy, completeness or correctness. In some cases the Principal Act and/or Amendment Act may not be available. Principal Acts may or may not include subsequent amendments. For authoritative text, please contact the relevant state department concerned or refer to the latest government publication or the gazette notification. Any person using this material should take their own professional and legal advice before acting on any information contained in this document. PRS or any persons connected with it do not accept any liability arising from the use of this document. PRS or any persons connected with it shall not be in any way responsible for any loss, damage, or distress to any person on account of any action taken or not taken on the basis of this document. 301 KARNATAKA ACT NO. 32 OF 2004 THE KARNATAKA VALUE ADDED TAX ACT, 2003 Arrangement of Sections Sections: Chapter I Introduction 1. -

Indian Dance Drama Tradition

Imperial Journal of Interdisciplinary Research (IJIR) Vol-3, Issue-4, 2017 (Special Issue), ISSN: 2454-1362, http://www.onlinejournal.in Proceedings of 5th International Conference on Recent Trends in Science Technology, Management and Society Indian Dance Drama Tradition Dr. Geetha B V Post-Doctoral research fellow, Women Studies Department, Kuvempu University, Shankarghatta, Shimoga. Abstract: In the cultures of the Indian subcontinent, for its large, elaborate make up and costumes. The drama and ritual have been integral parts of a elaborate costumes of Kathakalli become the most single whole from earliest recorded history. The recognized icon of Kerala. The themes of the first evidences of ritual dance drama performances Kathakali are religious in nature. The typically occur in the rock painting of Mirzapur, Bhimbetka, deal with the Mahabarat, the Ramayana and the and in other sites, which are various dated 20,000- ancient Scriptures known as the puranas. 5000 bce. The ancient remains of Mohenjo-Daro Kuchipudi dance drama traditions hails from and the Harappa (2500-2000 bce) are more Andhrapradesh. BhamaKalapam is the most definitive. Here archeological remains clearly popular Dance-Drama in Kuchipudi repertoire point to the prevalence of ritual performance ascribed to Siddhendra Yogi. The story revolves involving populace and patrons. The Mohenjo – round the quarrel between satyabhama and Daro seals, bronze fegurines, and images of priest Krishna. and broken torsos are all clear indications of dance In this paper I am dealing with Yakshagana dance as ritual. The aspects of vedic ritual tradition drama tradition. I would like to discuss this art closest to dance and drama was a rigorous system form’s present scenario. -

GST Notifications (Rate) / Compensation Cess, Updated As On

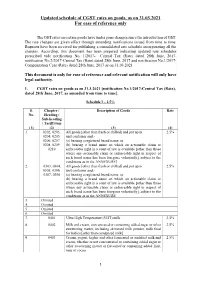

Updated schedule of CGST rates on goods, as on 31.03.2021 For ease of reference only The GST rates on certain goods have under gone changes since the introduction of GST. The rate changes are given effect through amending notifications issued from time to time. Requests have been received for publishing a consolidated rate schedule incorporating all the changes. According, this document has been prepared indicating updated rate schedules prescribed vide notification No. 1/2017- Central Tax (Rate) dated 28th June, 2017, notification No.2/2017-Central Tax (Rate) dated 28th June, 2017 and notification No.1/2017- Compensation Cess (Rate) dated 28th June, 2017 as on 31.03.2021 This document is only for ease of reference and relevant notification will only have legal authority. 1. CGST rates on goods as on 31.3.2021 [notification No.1/2017-Central Tax (Rate), dated 28th June, 2017, as amended from time to time]. Schedule I – 2.5% S. Chapter / Description of Goods Rate No. Heading / Sub-heading / Tariff item (1) (2) (3) (4) 1. 0202, 0203, All goods [other than fresh or chilled] and put up in 2.5% 0204, 0205, unit container and,- 0206, 0207, (a) bearing a registered brand name; or 0208, 0209, (b) bearing a brand name on which an actionable claim or 0210 enforceable right in a court of law is available [other than those where any actionable claim or enforceable right in respect of such brand name has been foregone voluntarily], subject to the conditions as in the ANNEXURE] 2. 0303, 0304, All goods [other than fresh or chilled] and put up in 2.5% 0305, 0306, unit container and,- 0307, 0308 (a) bearing a registered brand name; or (b) bearing a brand name on which an actionable claim or enforceable right in a court of law is available [other than those where any actionable claim or enforceable right in respect of such brand name has been foregone voluntarily], subject to the conditions as in the ANNEXURE 3. -

Library of Congress Medium of Performance Terms for Music

A clarinet (soprano) albogue anzhad USE clarinet BT double reed instrument USE imzad a-jaeng alghōzā Appalachian dulcimer USE ajaeng USE algōjā UF American dulcimer accordeon alg̲hozah Appalachian mountain dulcimer USE accordion USE algōjā dulcimer, American accordion algōjā dulcimer, Appalachian UF accordeon A pair of end-blown flutes played simultaneously, dulcimer, Kentucky garmon widespread in the Indian subcontinent. dulcimer, lap piano accordion UF alghōzā dulcimer, mountain BT free reed instrument alg̲hozah dulcimer, plucked NT button-key accordion algōzā Kentucky dulcimer lõõtspill bīnõn mountain dulcimer accordion band do nally lap dulcimer An ensemble consisting of two or more accordions, jorhi plucked dulcimer with or without percussion and other instruments. jorī BT plucked string instrument UF accordion orchestra ngoze zither BT instrumental ensemble pāvā Appalachian mountain dulcimer accordion orchestra pāwā USE Appalachian dulcimer USE accordion band satāra arame, viola da acoustic bass guitar BT duct flute USE viola d'arame UF bass guitar, acoustic algōzā arará folk bass guitar USE algōjā A drum constructed by the Arará people of Cuba. BT guitar alpenhorn BT drum acoustic guitar USE alphorn arched-top guitar USE guitar alphorn USE guitar acoustic guitar, electric UF alpenhorn archicembalo USE electric guitar alpine horn USE arcicembalo actor BT natural horn archiluth An actor in a non-singing role who is explicitly alpine horn USE archlute required for the performance of a musical USE alphorn composition that is not in a traditionally dramatic archiphone form. alto (singer) A microtonal electronic organ first built in 1970 in the Netherlands. BT performer USE alto voice adufo alto clarinet BT electronic organ An alto member of the clarinet family that is USE tambourine archlute associated with Western art music and is normally An extended-neck lute with two peg boxes that aenas pitched in E♭. -

Prabháta Sam'giita

Prabháta Sam'giita Songs of the New Dawn A brief introduction Renaissance Artists & Writers Association A New Dawn • Prabhata Samgiita – music of a new dawn • 5018 songs • From Indian classical to folk music • Written and composed by: – Shri Prabhata Rainjana Sarkar • Between 1982 and 1990 Variety of Themes • Devotional • Mystical love • Seasons • Ecology • Social consciousness • Marching songs • Stages, feelings & experiences in spiritual meditation • Krs'n'a •Shiva Languages Used • Most songs are in Bengali • Over 40 songs are composed in other languages, including: –English –Sanskrit (language for literary & spiritual uses) –Hindi (vocabulary borrows from Sanskrit, non-Persian & non-Arabic) –Urdu (similar to elementary Hindi, vocabulary borrows from Persian & Arabic) –Angika (spoken in in Bihar, Jharkhand & West Bengal) –Maithili (spoken in North-East Bihar & Nepal) Northern-Central India Some Genres of Prabhata Samgiita • Kiirtan songs • Tappa songs • Thumri songs • Gazal songs • Kawali songs • Baul songs • Jhumur songs Kiirtan Songs • Kiirtan is a special type of devotional song style • Centres around singing about the Supreme Entity (God) • Developed towards the end of the 12th century through Jayadeva’s composition of the Gita Govinda (around 1178 AD) • These are Sanskrit love poems saturated with madhura bhava (high state of devotional sentiment and Divine Love) Kiirtan Songs • During the 15th century Dwija Chandidas (1390 -1450) advocated Krishna kiirtans • These are songs in praise of Lord Krishna as the incarnation of the Supreme -

TRICHY 396 Metresmetres (758(758 Kc/S) Kc/S) Parkka Parkka Parkka Kambodikambodl 7.0 ACHUPRACHARAM a C H U PRA CH ARA M A.M

111gTHE INbIANItifttAN usTENRALISTENER SSATURDAY A T U R D A Y, JJUNE U N E 99 MADRAS TRICHY 396 metresmetres (758(758 kc/s) kc/s) Parkka parkkaparkka KambodiKambodl 7.0 ACHUPRACHARAMA C H U PRA CH ARA M a.m. TRANSMISSIONTRANSMISSION I Balagopala Bhairavi MADRAS 11 Talk in Tamil analysing Axix propagandapropaganda 7.45*7.45 * MUSICALMUSICAL PRELUDEPRELUDE t Evakai DeramanohanDevamanohari by RaoRao SahibSahib T.T. S.S. NATARAJA NATARAJA PILLAIPILLAI Biranavara Kalyani 211 metres (1,420 k c/3) PALGHAT RAMARAMA BHAGAVATARBHAGAVATAR Biranavara 211 metres (1,420 kc/s) Vin garvamgarvam Mohanam Valli manavala KapiRapt а.m.a.m. TRANSMISSIONTRANSMISSION II 7.15 T. S. CHANDRASEKHARANC H AN D RASEK H ARAN 7.50 NEWS IN TAMILTAM IL 7.30*7.30 * SWAGATAMSW A G A TA M Fluteflu te 8.0 T. A. N A G A SA M I 5.40 TIRUMOZIIITIRU M O ZH I VILAKKAMV IL A K K A M 8.0 T. A. NAGASAMI Exposition in TamilTamil byby H. H. AZHAKIYA AZHAKIYA MANA- MANA Dhyaname—Dhyaname-Dhanyasi-AdiDhanyasi—Adi BHAGAVATAR f 7.45 NEWS IN TAM IL BHAGAVATAR VALA NAIDU; DevotionalDevotional songssongs 7.45 NEWS IN TAMIL Dorakuna Bilahari 7.40 VIJAYALAKSHMIV IJA Y A L AK SH M I f Ini ennaenna Sahana 8.0 K U N N AK U D I V E N K A T R A M A 6.0 T. S.S. SESHADRISESH ADRI Parama kripa;kripa; Kalimayilada; Kanniparuva- 8.0 KUNNAKUDI VENKATRAMA Ennagamanasuku NilambariNilombori Todi thile IYER Edu paramukhamparamukham Todi IYER 8.15 NEWSNEWS IN IN ENGLISH Tarunam SuddhasaveriStiddhasaveri V. -

![THE GAZETTE of INDIA : EXTRAORDINARY [PART II—SEC. 3(I)] NOTIFICATION New Delhi, the 22Nd September, 2017 No.28/2017-Union](https://docslib.b-cdn.net/cover/2596/the-gazette-of-india-extraordinary-part-ii-sec-3-i-notification-new-delhi-the-22nd-september-2017-no-28-2017-union-2342596.webp)

THE GAZETTE of INDIA : EXTRAORDINARY [PART II—SEC. 3(I)] NOTIFICATION New Delhi, the 22Nd September, 2017 No.28/2017-Union

66 THE GAZETTE OF INDIA : EXTRAORDINARY [P ART II—SEC . 3(i)] 111. उडुकईi 112. चंडे 113. नागारा - केटलेG स कƙ जोड़ी 114. प बाई - दो बेलनाकार Gम कƙ इकाई 115. पैराित पु, हगी - sेम Gम दो िटϝस के साथ खेला 116. संबल 117. िटक डफ या िटक डफ - लाठी के साथ खेला जाने वाला टġड मĞ डेफ 118. तमक 119. ताशा - केटलेGम का Oकार 120. उƞम 121. जलातरंग िच पēा - पीतल के ƚजगल के साथ आग टĪग 122. चĞिगल - धातु िडक 123. इलाथलम 124. गेजर - Qास पोत 125. घटक और मटकाम (िमŝी के बरतन बतϕन Gम) 126. घुंघĐ 127. खारट या िच पला 128. मनजीरा या झंज या ताल 129. अखरोट - िमŝी के बतϕन 130. संकरजांग - िल थोफोन 131. थाली - धातु लेट 132. थाकुकाजामनाई 133. कंचारांग, कांच के एक Oकार 134. कथाततरंग, एक Oकार का जेलोफ़ोन [फा सं.354/117/2017-टीआरयू-भाग II] मोिहत ितवारी, अवर सिचव Ɨट पणी : Oधान अिधसूचना सं. 2/2017- संघ राϤ यϓेJ कर (दर), तारीख 28 जून, 2017, सा.का.िन. 711 (अ) तारीख 28 जून, 2018 ůारा भारत के राजपJ , असाधारण, भाग II, खंड 3, उपखंड (i) ůारा Oकािशत कƙ गई थी । NOTIFICATION New Delhi, the 22nd September, 2017 No.28/2017-Union Territory Tax (Rate) G.S.R.1196 (E).— In exercise of the powers conferred by sub-section (1) of section 8 of the Union Territory Goods and Services Tax Act, 2017 (14 of 2017), the Central Government, being satisfied that it is necessary in the public interest so to do, on the recommendations of the Council, hereby makes the following amendments in the notification of the Government of India in the Ministry of Finance (Department of Revenue), No.2/2017-Union territory Tax (Rate), dated the 28th June, 2017, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. -

The Arunachal Pradesh Gazette EXTRAORDINARY PUBLISHED by AUTHORITY

The Arunachal Pradesh Gazette EXTRAORDINARY PUBLISHED BY AUTHORITY No. 411, Vol. XXIV, Naharlagun, Wednesday, October 4, 2017 Asvina 12, 1939 (Saka) GOVERNMENT OF ARUNACHAL PRADESH DEPARTMENT OF TAX & EXCISE ITANAGAR ————— Notification No. 28/2017-State Tax (Rate) The 26th September, 2017 No. GST/24/2017.— In exercise of the powers conferred by sub-section (1) of Section 11 of the Arunachal Pradesh Goods and Services Tax Act, 2017 (7 of 2017), the State Government, on the recommendations of the Council, hereby makes the following amendments in the notification of the Government of Arunachal Pradesh, Department of Tax & Excise, No.2/2017-State Tax (Rate), dated the 28th June, 2017, published in the Extra ordinary Gazette of Arunachal Pradesh, vide number 192, Vol XXIV, dated the 30th June, 2017, namely:- In the said notification,- (B) in the Schedule,- (i) against serial number 27, in column (3), for the words “other than put up in unit containers and bearing a registered brand name”, the words, brackets and letters “other than those put up in unit container and,- (a) bearing a registered brand name; or (b) bearing a brand name on which an actionable claim or enforceable right in a court of law is available [other than those where any actionable claim or enforceable right in respect of such brand name has been foregone voluntarily, subject to the conditions as in the ANNEXURE I]”, shall be substituted ; (jj) against serial numbers 29 and 45, in column (3), for the words “other than put up in unit container and bearing a registered brand -

YAKSHAGANA SEMINAR Shri K

A view of .the Yakshauana Seminar in session. (Left to Right): Shri K.S. Karanth, Convener, Shri Baikadi Ven kata Krishna Rao, Secretary, Reception Committee, and Shri Sheshagiri Kini,President, Reception Committee YAKSHAGANA SEMINAR Shri K. s. Karanth's Report A seminar on Yakshagana-a dance drama-art-prevailing in the Malanad area of Karnataka . was organised at Brahmavar (South Kanara) from September 27 to 30, 1958, with the object of formulating a scheme for the revival and preservation of the best in the traditions of Yakshagana. A brief report of the same is as follows: Invitations were sent to various drama Brahmavar was chosen as the venue of the troupes and artistes, i.e., Bhagawaths, drummers Conference because of its historical importance and dancers. All veterans, including retired to the tradition of Yakshagana art as well as for artistes, were also approached. Enough publi the fact that it lay in a centrally situated area City was given through language papers and a around which many troupes flourished and reception committee was formed at Brahmavar many artistes practised their profession. with- Shri Sheshagiri Bhagawath, a veteran in the field, as the Chairman and Shri Rama Ganiga, Shri B. V. Achar of Brahmavar took up the a veteran dancer, as Vice-Chairman. All entire responsibility of playing the host to all artistes intending to participate in the seminar the delegates coming to the seminar. The were requested to intimate earlier about their other expenses were borne by the organiser. 9ualifications, such as professional experience Shri Achar's generosity made the organiser's In the field of dance, music, etc. -

Urgent Letter

April 27, 2020 The Honorable Nancy Pelosi The Honorable Kevin McCarthy Speaker of the House Republican Leader U.S. House of Representatives U.S. House of Representatives Washington, DC 20510 Washington, DC 20510 The Honorable Mitch McConnell The Honorable Chuck Schumer Majority Leader Democratic Leader U.S. Senate U.S. Senate Washington, DC 20510 Washington, DC 20510 Dear Speaker Pelosi, Leader McConnell, Leader Schumer & Leader McCarthy: On behalf of the American Hotel & Lodging Association (AHLA) and the undersigned hoteliers and hotel employees from all 50 states, we thank you for your steadfast leadership in guiding our nation through this unprecedented health and economic crisis. The economic impact of the COVID-19 health crisis on the hotel industry is estimated to be nine times greater than the September 11th terrorist attacks. According to Oxford Economics, nearly 4 million hotel employees have been furloughed and the industry is expected to lose nearly fifty percent of its total revenue in 2020 – which could exceed $112 Billion. From the beginning of this health and economic crisis, we have been focused on two main objectives: first, supporting and retaining hotel employees as demand has diminished; and second, saving the U.S. network of local hotels, the majority of which are small businesses. The hotel industry relies on a dedicated and talented hospitality workforce and is hopeful that we can restart the economy so that we can restore these critical jobs. However, if hotels across this country are insolvent and default on their loan obligations, then we will not be successful in retaining hotel employees. Hotel employees and local hotel owners have been negatively impacted by the COVID-19 pandemic through no fault of their own. -

Medium of Performance Thesaurus for Music

A clarinet (soprano) albogue tubes in a frame. USE clarinet BT double reed instrument UF kechruk a-jaeng alghōzā BT xylophone USE ajaeng USE algōjā anklung (rattle) accordeon alg̲hozah USE angklung (rattle) USE accordion USE algōjā antara accordion algōjā USE panpipes UF accordeon A pair of end-blown flutes played simultaneously, anzad garmon widespread in the Indian subcontinent. USE imzad piano accordion UF alghōzā anzhad BT free reed instrument alg̲hozah USE imzad NT button-key accordion algōzā Appalachian dulcimer lõõtspill bīnõn UF American dulcimer accordion band do nally Appalachian mountain dulcimer An ensemble consisting of two or more accordions, jorhi dulcimer, American with or without percussion and other instruments. jorī dulcimer, Appalachian UF accordion orchestra ngoze dulcimer, Kentucky BT instrumental ensemble pāvā dulcimer, lap accordion orchestra pāwā dulcimer, mountain USE accordion band satāra dulcimer, plucked acoustic bass guitar BT duct flute Kentucky dulcimer UF bass guitar, acoustic algōzā mountain dulcimer folk bass guitar USE algōjā lap dulcimer BT guitar Almglocke plucked dulcimer acoustic guitar USE cowbell BT plucked string instrument USE guitar alpenhorn zither acoustic guitar, electric USE alphorn Appalachian mountain dulcimer USE electric guitar alphorn USE Appalachian dulcimer actor UF alpenhorn arame, viola da An actor in a non-singing role who is explicitly alpine horn USE viola d'arame required for the performance of a musical BT natural horn composition that is not in a traditionally dramatic arará form. alpine horn A drum constructed by the Arará people of Cuba. BT performer USE alphorn BT drum adufo alto (singer) arched-top guitar USE tambourine USE alto voice USE guitar aenas alto clarinet archicembalo An alto member of the clarinet family that is USE arcicembalo USE launeddas associated with Western art music and is normally aeolian harp pitched in E♭. -

Classical Essence in Yakshagana

International Conference on Arts, Culture, Literature, Languages, Gender Studies/ Sexuality, Humanities and Philosophy for Sustainable Societal Development Classical Essence in Yakshagana Harshita Upadhya Student, Department of English Christ University, Bangalore Abstract—Yakshagana is one of the popular art forms in India. It is classical essence does it exist? What do Prasanga'sshow about a unique art which has been known as folk art and research Yakshagana. Janapada does not have literary script, What showcases the classical essence in Yakshagana. The usage of Hindu about Yakshagana? Is there Janapada stories used in Mythology, classical dance, musical impact, Natyashatra and Yakshagana? Or something else? In Music, Dance, Costumes Sanskrit basement likewise many other elements of Yakshagana is this showcases Classical or Folk form? unfolds the Classical essence. Ample of Shlokas and Prosody is dwelled in the literary works of Yakshagana and which cannot be Thesis statement: Yakshagana orients classical essence seen in Folk art. To support these ideas Lava Kusha Kalaga which employs Indian mythology, Classical Music and Prasanga is taken as my primary text. This Prasanga showcases classical dance components, Sanskrit impact and basement of many incidents which glorifies classical essence of Yakshagana. The cultural methodology is applied to design my research. The research Natyashstra in it. helps to know more about classical notion of Yakshagana and even My Primary Text is Lava-Kusha Kalaga Yakshagana reflects on classical genres. video which is performed by Mahila Yakshagana Balaga Gund (Women Yakshagana Team Gund) at Nandigadde Keywords: Prasanga, Yakshagana, Natya, Classical, Bhagawata Rangamandira on 06-09-2016. This Lava-Kusha Kalaga Prasanga is written by M.A Hegde Siddapur.