Annual Results 2008

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PREFERENCE SHARES, NOMINAL VALUE of E2.24 PER SHARE, in the CAPITAL OF

11JUL200716232030 3JUL200720235794 11JUL200603145894 Public Offer by RFS Holdings B.V. FOR ALL OF THE ISSUED AND OUTSTANDING (FORMERLY CONVERTIBLE) PREFERENCE SHARES, NOMINAL VALUE OF e2.24 PER SHARE, IN THE CAPITAL OF ABN AMRO Holding N.V. Offer Memorandum and Offer Memorandum for ABN AMRO ordinary shares (incorporated by reference in this Offer Memorandum) 20 July 2007 This Preference Shares Offer expires at 15:00 hours, Amsterdam time, on 5 October 2007, unless extended. OFFER MEMORANDUM dated 20 July 2007 11JUL200716232030 3JUL200720235794 11JUL200603145894 PREFERENCE SHARES OFFER BY RFS HOLDINGS B.V. FOR ALL THE ISSUED AND OUTSTANDING PREFERENCE SHARES, NOMINAL VALUE OF e2.24 PER SHARE, IN THE CAPITAL OF ABN AMRO HOLDING N.V. RFS Holdings B.V. (‘‘RFS Holdings’’), a company formed by an affiliate of Fortis N.V. and Fortis SA/NV (Fortis N.V. and Fortis SA/ NV together ‘‘Fortis’’), The Royal Bank of Scotland Group plc (‘‘RBS’’) and an affiliate of Banco Santander Central Hispano, S.A. (‘‘Santander’’), is offering to acquire all of the issued and outstanding (formerly convertible) preference shares, nominal value e2.24 per share (‘‘ABN AMRO Preference Shares’’), of ABN AMRO Holding N.V. (‘‘ABN AMRO’’) on the terms and conditions set out in this document (the ‘‘Preference Shares Offer’’). In the Preference Shares Offer, RFS Holdings is offering to purchase each ABN AMRO Preference Share validly tendered and not properly withdrawn for e27.65 in cash. Assuming 44,988 issued and outstanding ABN AMRO Preference Shares outstanding as at 31 December 2006, the total value of the consideration being offered by RFS Holdings for the ABN AMRO Preference Shares is e1,243,918.20. -

La Presente Versione Del Documento Sostituisce Le Versioni Precedenti

STRUTTURA CONTI DEI PARTECIPANTI A T2S Page 1 La presente versione del documento sostituisce le versioni precedenti/ The current version substitute the previous one NEGOZIATORE/ LIQUIDATORE/ CLIENT OF THE SETTLEMENT AGENT SETTLEMENT AGENT CONTO CODICE BIC/ DEFAULT CODICE REGOLAMENTO DI TIPO CODICE CED/ CODICE ABI/ DESCRIZIONE BREVE/ CODICE ABI/ DESCRIZIONE BREVE/ PARTY BIC BIC CODE SETTLEMENT CED/ PARENT BIC SAC T2S DEFAULT/DEFAULT NEGOZIAZIONE/ CED CODE ABI CODE SHORT DESCRIPTION ABI CODE SHORT DESCRIPTION (PARTY1) (PARTY2) AGENT CED CODE SETTLEMENT DEALING CAPACITY ACCOUNT NEFOSESSXXX 180 22548 NEONET SECURITIES AB Y 1105 3069 INTESA SANPAOLO MOTIITMMXXX BCITITM1T01 MOTIBCITITMMXXX6016200 Y B BACRIT22XXX 302 3032 CRED.EMILIANO Y 302 3032 CRED.EMILIANO MOTIITMMXXX BACRIT22XXX MOTIBACRIT22XXX0303200 Y P BACRIT22XXX 302 3032 CRED.EMILIANO Y 302 3032 CRED.EMILIANO MOTIITMMXXX BACRIT22XXX MOTIBACRIT22XXX6303200 Y T BARCIT4GXXX 303 3051 BARCLAYS BANK Y 515 3479 BPSS MOTIITMMXXX PARBITMM011 MOTIPARBITMMXXX6048200 Y B DEUTITMMXXX 308 3104 DEUTSCHE BANK Y 308 3104 DEUTSCHE BANK MOTIITMMXXX DEUTITMMXXX MOTIDEUTITMMXXX6310400 Y T DEUTITMMXXX 308 3104 DEUTSCHE BANK Y 308 3104 DEUTSCHE BANK MOTIITMMXXX DEUTITMMXXX MOTIDEUTITMMXXX0310400 Y P BLOPIT22XXX 315 3111 UBI BANCA Y 315 3111 UBI BANCA MOTIITMMXXX BLOPIT22XXX MOTIBLOPIT22XXX0311100 Y P BLOPIT22XXX 315 3111 UBI BANCA Y 315 3111 UBI BANCA MOTIITMMXXX BLOPIT22XXX MOTIBLOPIT22XXX6311100 Y T FIBKITMMXXX 317 3296 FIDEURAM S.p.A. Y 1105 3069 INTESA SANPAOLO MOTIITMMXXX BCITITM1T02 MOTIBCITITMMXXX6010500 Y T FIBKITMMXXX 317 3296 FIDEURAM S.p.A. Y 1105 3069 INTESA SANPAOLO MOTIITMMXXX BCITITM1T02 MOTIBCITITMMXXX6003800 Y P IBSPITNAXXX 339 1010 SANPAOLO B.NAPOLI Y 1105 3069 INTESA SANPAOLO MOTIITMMXXX BCITITM1T13 MOTIBCITITMMXXX6021800 Y B CITIITMXXXX 352 3566 CITIBANK N.A. Y 352 3566 CITIBANK N.A. -

Informe Anual Banco Santander Chile

Informe Anual Banco Santander Chile Informe Anual Banco Santander Chile 3 índice de Contenidos 2009 I. Reconocimientos Obtenidos en 2009 4 II. Indicadores Financieros 6 III. Carta del Presidente 9 IV. Directorio y Gobierno Corporativo 13 V. Administración 20 VI. Entorno de los Negocios 22 1. Economía Internacional 23 2. Economía Chilena 25 3. Sistema Financiero 25 VII. Pilares de Nuestra Gestión 2009 28 1. Cercanía con los Clientes 29 2. Creando Valor para Nuestros Accionistas 31 3. Liquidez y Solvencia 33 4. Construyendo Juntos el Mejor Lugar para Trabajar 35 5. Compromiso con la Sociedad 37 6. Manejo Integral del Riesgo 39 VIII. Análisis de la Gestión y Resultados 2009 44 1. Áreas de Negocios 44 2. Manejo Activo del Balance 47 3. Análisis de los Resultados 49 3. Gestión Activa del Riesgo y las Recuperaciones 52 4. Aumento en la Vinculación y Transaccionalidad 54 5. Mejora Continua de la Eficiencia 55 IX. Informe Anual Comité de Directores y Auditoría 58 X. Grupo Santander en el Mundo 63 XI. Estados Financieros Consolidados 75 XII. Estados Financieros Resumidos de las Empresas Filiales 211 1. Santander Asset Management S.A. Administradora General de Fondos 212 2. Santander S.A. Agente de Valores 214 3. Santander Corredora de Seguros Limitada 216 4. Santander S.A. Corredores de Bolsa 218 5. Santander S.A. Sociedad Securitizadora 220 6. Santander Servicios de Recaudación y Pagos Limitada 222 XIII. Información General 224 3 Reconocimientos Obtenidos en 2009 Banco Santander fue reconocido con más de Las principales revistas de finanzas del mundo, 15 distinciones en el año 2009, por la labor Global Finance, Latin Finance y Euromoney nos desarrollada en las distintas áreas que le competen distinguieron como el Mejor Banco en Chile, y como entidad financiera líder en el país. -

Download Pdf File of RBS Group Annual Report 2007

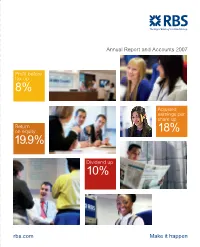

Annual Report and Accounts 2007 Profit before tax up 8% Adjusted earnings per share up Return on equity 18% 19.9% Dividend up 10% rbs.com Make it happen Highlights 2007 Contents Group operating profit up 9% 02 Measuring our success 04 Group profile to £10.3 billion 06 Divisional profile 08 Chairman’s statement 10 Group Chief Executive’s review Profit after tax up 19% to £7.7 billion Adjusted earnings per ordinary Divisional review share up 18% to 78.7p 13 Corporate Markets 15 Retail Markets 17 Ulster Bank 18 Citizens Total dividend up 10% to 33.2p 19 RBS Insurance 20 Manufacturing 21 ABN AMRO Tier 1 capital ratio 7.3% Total capital ratio 11.2% Corporate Responsibility 22 Combating crime 22 Building financial capability 23 Promoting financial inclusion 24 Customer service 24 Citizens in the community 25 Our employees 25 RBS and the environment Report and accounts 27 Business review 91 Governance 117 Financial statements 213 Additional information 235 Shareholder information RBS Group • Annual Report and Accounts 2007 01 Measuring our success Focus on growth and efficiency Income Adjusted cost:income ratio Group operating profit* (£m) (%) (£m) 07 31,115 07 43.9 07 10,282 06 28,002 06 42.1 06 9,414 05 25,569 05 42.4 05 8,251 04 22,515 pro forma 04 42.0 pro forma 04 7,108 pro forma The Group’s total income grew by 11% The Group’s cost:income ratio was 43.9%. Excluding ABN AMRO, Group operating profit increased by 9% to to £31,115 million in 2007. -

Investment Banking

PresentationPresentation toto FixedFixed IncomeIncome InvestorsInvestors June 2002 ContentsContents Mediobanca Section I Profile, shareholders and organisation chart Section II Wholesale - Corporate Banking Section III Wholesale - Investment Banking Section IV Retail financial services Section V Private Banking Section VI Research Section VII Capitalisation Section VIII Asset quality Section IX Cost efficiency, productivity and profitability Section X Treasury Section XI Business Plan 2002-2005 Section XII Transaction indicative highlights Appendices Appendix 1 Financial statements Appendix 2 Standard and Poor's ratings to italian financial institutions 2 ProfileProfile Mediobanca Profile, shareholders and organisation chart Section I p Mediobanca, founded in 1946, is the leading investment bank in Italy p Mediobanca’s central position in the Italian capital market is due to long-term close relationships with major Italian leading companies and with the international financial community p Business plan 2002-2005 focuses on enhancing wholesale banking business, developing private banking and private equity, adding international dimension to the bank’s structure p Core shareholders’ pact controls 46% of share capital. It was confirmed in 2001 until 2004 p Members of shareholders’ pact include key players in the Italian and European financial and business community p Market capitalisation as at 5th June 2002 was € 7.828bn p Mediobanca shares are constituents of Milan Stock Exchange “blue chip” index MIB 30 p Mediobanca enjoys excellent capitalisation: 19% Tier 1 at year end 2001, with no hybrid components p Regulated by Bank of Italy and Consob p Standard & Poors’ recently assigned AA- long term credit rating to Mediobanca with stable outlook, the best S&P rating to an Italian bank 3 ProfileProfile Mediobanca Profile, shareholders and organisation chart Section I MediobancaMediobanca GroupGroup Mediobanca S.p.A. -

ABN AMRO Holding N.V. Offer Memorandum Listing Particulars

11JUL200716232030 3JUL200720235794 11JUL200603145894 Public Offer by RFS Holdings B.V. FOR ALL THE ISSUED AND OUTSTANDING ORDINARY SHARES, NOMINAL VALUE OF e0.56 PER SHARE, IN THE CAPITAL OF ABN AMRO Holding N.V. Offer Memorandum and Listing Particulars 20 July 2007 This Offer expires at 15:00 hours, Amsterdam time, on 5 October 2007, unless extended. OFFER MEMORANDUM dated 20 July 2007 11JUL200716232030 3JUL200720235794 11JUL200603145894 PUBLIC OFFER BY RFS HOLDINGS B.V. FOR ALL THE ISSUED AND OUTSTANDING ORDINARY SHARES, NOMINAL VALUE OF e0.56 PER SHARE, IN THE CAPITAL OF ABN AMRO HOLDING N.V. RFS Holdings B.V. (‘‘RFS Holdings’’), a company formed by an affiliate of Fortis N.V. and Fortis SA/NV (Fortis N.V. and Fortis SA/NV together ‘‘Fortis’’), The Royal Bank of Scotland Group plc (‘‘RBS’’) and an affiliate of Banco Santander Central Hispano, S.A. (‘‘Santander’’), is offering to acquire all of the issued and outstanding ordinary shares, nominal value e0.56 per share (‘‘ABN AMRO Ordinary Shares’’), of ABN AMRO Holding N.V. (‘‘ABN AMRO’’), on the terms and conditions set out in this document (the ‘‘Offer’’). Under the terms of the Offer, holders of ABN AMRO Ordinary Shares will receive for each ABN AMRO Ordinary Share validly tendered and not properly withdrawn: • e35.60 in cash; and • 0.296 newly issued ordinary shares, nominal value £0.25 per share, of RBS (‘‘New RBS Ordinary Shares’’). For the purposes of the Dutch offer rules, the Offer extends to the ABN AMRO ADSs (as defined below), provided that, as further detailed below, the holders of ABN AMRO ADSs are referred to the U.S. -

Libro De Entidades (1 MB )

REGISTROS DE ENTIDADES 2021 SITUACION A 23 DE SEPTIEMBRE DE 2021 BANCO DE ESPAÑA INDICE Página CREDITO OFICIAL ORDENADO ALFABETICAMENTE ...................................................................................................... 7 ORDENADO POR CODIGO B.E. ......................................................................................................... 9 BANCOS ORDENADO ALFABETICAMENTE .................................................................................................... 13 ORDENADO POR CODIGO B.E. ....................................................................................................... 15 CAJAS DE AHORROS ORDENADO ALFABETICAMENTE .................................................................................................... 25 ORDENADO POR CODIGO B.E. ....................................................................................................... 27 COOPERATIVAS DE CREDITO ORDENADO ALFABETICAMENTE .................................................................................................... 31 ORDENADO POR CODIGO B.E. ....................................................................................................... 33 ESTABLECIMIENTOS FINANCIEROS DE CREDITO ORDENADO ALFABETICAMENTE .................................................................................................... 45 ORDENADO POR CODIGO B.E. ....................................................................................................... 47 ESTABLECIMIENTOS FINANCIEROS DE CREDITO ENTIDADES DE PAGO -

Crecimiento Inorganico Del Banco Santander En Las Dos Ultimas Decadas

FACULTAD DE CIENCIAS ECONOMICAS Y EMPRESARIALES CRECIMIENTO INORGANICO DEL BANCO SANTANDER EN LAS DOS ULTIMAS DECADAS Clave:201114853 Coordinador de TFG: Raquel Redondo Palomo Madrid Junio 2015 2 INORGANICO DEL BANCO SANTANDER DECADAS INORGANICO DOS EN DEL BANCO ULTIMAS LAS CRECIMIENTO 3 INDICE 1. Resumen. .................................................................................................................. 5 1.1 Abstract ......................................................................................................................... 6 2. Introducción. ............................................................................................................ 7 2.1 Motivación del trabajo. ....................................................................................................... 7 2.2 Objetivos. ............................................................................................................................ 8 2.3 Metodología. ....................................................................................................................... 9 3. Marco teórico. ........................................................................................................ 10 3.1 Efectos de la globalización en el crecimiento. ................................................................. 10 3.1.1 La globalización y causas principales: ....................................................................... 10 3.1.2 Ventajas e inconvenientes del proceso de globalización. ....................................... -

Informe Anual Banco Santander Chile

2008 Informe Anual Banco Santander Chile WorldReginfo - 1e572dcc-6c4d-4900-b053-c0f0d189e72b WorldReginfo - 1e572dcc-6c4d-4900-b053-c0f0d189e72b Informe Anual Banco Santander Chile 2008 WorldReginfo - 1e572dcc-6c4d-4900-b053-c0f0d189e72b WorldReginfo - 1e572dcc-6c4d-4900-b053-c0f0d189e72b Índice de Contenidos Reconocimientos Obtenidos en 2008 5 Indicadores Financieros 7 Carta del Presidente 10 Directorio 12 Transparencia y Gobierno Corporativo 16 Administración 20 Carta del Gerente General 22 Entorno de los Negocios 24 • Economía Internacional 24 • Economía Chilena 26 • Sistema Financiero 28 Análisis de la Gestión 29 • Crecimiento Selectivo del Negocio 31 • Aumento en Vinculación y Fomento al Uso de Nuestros Productos 35 • Gestión Activa del Riesgo 36 • Mejora Continua de la Eficiencia 37 Áreas de Negocio 40 Manejo Integral del Riesgo 42 Gestión Estratégica 2008 50 • Clientes 50 • Empleados 54 • Sociedad 56 • Accionistas 59 Informe Anual Comité de Directores y Auditoría 62 Grupo Santander en el Mundo 69 Estados Financieros Consolidados 85 Estados Financieros Resumidos de las Empresas Filiales 133 • Santander Asset Management S.A. Administradora General de Fondos 134 • Santander S.A. Agente de Valores 136 • Santander Corredora de Seguros Limitada 138 • Santander S.A. Corredores de Bolsa 140 • Santander S.A. Sociedad Securitizadora 142 • Santander Servicios de Recaudación y Pagos Limitada 144 Información General 147 WorldReginfo - 1e572dcc-6c4d-4900-b053-c0f0d189e72b Memoria Financiera 6 7 WorldReginfo - 1e572dcc-6c4d-4900-b053-c0f0d189e72b Reconocimientos Obtenidos en 2008 1 1er lugar en Ranking de 2 Entre las Mejores Empresas para 3 Premio a la Memoria con Mejor Responsabilidad Social Chile 2008, Trabajar en Chile, según ranking Contenido Financiero, Revista Fundación Prohumana, Revista de Great Place to Work y Revista Gestión y PricewaterhouseCoopers. -

Santander US Debt, S.A. Unipersonal Banco Santander, S.A

LISTING PROSPECTUS Santander US Debt, S.A. Unipersonal (incorporated with limited liability in the Kingdom of Spain) guaranteed by Banco Santander, S.A. (incorporated with limited liability in the Kingdom of Spain) US$1,500,000,000 FLOATING LIBOR SENIOR NOTES DUE 2011 Santander US Debt, S.A. Unipersonal (the “Issuer”) issued on October 23, 2009 US$1,500,000,000 Floating LIBOR Senior Notes due October 21, 2011 (the “Notes”), which bear interest at the then-applicable U.S. dollar three-month LIBOR rate plus 0.40% per year. Interest on the Notes is payable on each January 21, April 21, July 21 and October 21 of each year, beginning on January 21, 2010 through and including the Maturity Date or any earlier date of redemption. The Notes will mature on October 21, 2011 (the “Maturity Date”). The Notes were issued in registered book-entry form through The Depository Trust Company (“DTC”) in denominations of U.S.$100,000 and integral multiples thereof. The Notes are unsecured and will rank equally in right of payment with the Issuer’s other unsecured unsubordinated indebtedness. The guarantees of the Notes (the “Guarantees”) as to the payment of principal and interest will be direct, unsecured and unsubordinated obligations of the Issuer’s parent, Banco Santander, S.A. (the “Guarantor”), ranking equally in right of payment with the Guarantor’s other unsecured unsubordinated indebtedness. For a more detailed description of the Notes and the Guarantees, see “Description of the Notes and Guarantees” beginning on page 69. Investing in the Notes involves risks. See “Risk Factors” beginning on page 14. -

Clearstream Banking Luxemburg

Clearstream Banking Luxemburg Participant Name BIC Code* Participant Code (CHINA) SOUTHERN SECS-SH/SN n.a. CN030 (ING) BARING SECURITIES HK-SH/SN n.a. CN205 1ST BK GREENWICH/U102 n.a. F7249 1ST CAP BK MONTERY/L101 n.a. F7133 1ST CENTENNIAL/T108 n.a. F9445 1ST CENTURY BANK/L101 n.a. F6878 1ST ENTPRSE BK LA/1030 n.a. F7223 1ST PAC BK CA SD/1020 n.a. F7234 2S BANCA n.a. C3307 6980271103 n.a. H0487 6980321592 n.a. H1074 6980413561 n.a. H0953 6980764740 n.a. H0962 6980767923 n.a. H0730 6981200105 n.a. H0486 6981903737 n.a. H0961 6981916176 n.a. H0768 6982000078 n.a. H0811 6984400093 n.a. H1078 6984400503 n.a. H0770 6984400668 n.a. H0564 698MFS n.a. H1462 A S NOMINEES n.a. H0800 1 A, ER SEC BANK/T108 n.a. F8783 A.B.ASESORES BURSATILES DEUDA n.a. E4012 A.C. NOMINEES LTD n.a. H0016 A.T. EQUITIES SPAIN n.a. E3670 AAHGSBL n.a. H0567 AAIC (FORMERLY DESCAP) n.a. F9548 AANVLDNBRNCHEURHUB/ABN AMRO EQUI.UK n.a. H1794 ABACO CASA DE BOLSA S.A. DE C.V. n.a. M5017 ABAX BANK n.a. C0061 ABBACUS n.a. C6288 ABBEY NATIONAL n.a. C2535 ABBEY NATIONAL n.a. C0072 ABBEY NATIONAL TREASURY SERV. PLC n.a. S0341 ABDELMALEK RAUL EMILIO n.a. A0626 ABERDEEN UTM LTD n.a. H0775 ABN AMRO n.a. F0792 ABN AMRO ASIA LTD.SEOUL BRANCH n.a. KR196 ABN AMRO ASIA LTD-SH/SN n.a. CN240 ABN AMRO ASIA SEC (S) PTE LTD n.a. -

'An Assessment of Asset and Liquidity Quality As Indicators of Performance Within the European Banking Sector'

‘An assessment of asset and liquidity quality as indicators of performance within the European banking sector’ Eva J. Gleeson MSc in Management National College of Ireland, IFSC Submitted to the National College of Ireland, September 2015 1 Submission of Thesis and Dissertation National College of Ireland Research Students Declaration Form (Thesis/Author Declaration Form) Name: Eva J. Gleeson Student Number: x13117114 Degree for which thesis is submitted: MSC Management Material submitted for award (a) I declare that the work has been composed by myself. (b) I declare that all verbatim extracts contained in the thesis have been distinguished by quotation marks and the sources of information specifically acknowledged. (c) My thesis will be included in electronic format in the College Institutional Repository TRAP (thesis reports and projects). (d) Either *I declare that no material contained in the thesis has been used in any other submission for an academic award Or *I declare that the following material contained in the thesis formed part of a submission for the award of MSC Management (State the award and the awarding body and list the material below) Signature of research student: Eva J. Gleeson Date:31//08/2015 2 Submission of Thesis to Norma Smurfit Library, National College of Ireland Student name: ______________________________ Student number: __________ ___ __ School: ___________________________________ Course: __________ ______________ Degree to be awarded: __________________________________ _____________ _ __ Title of Thesis: __________________________________________________________ ___ _______________________________________________________________________ __ _______________________________________________________________________ __ One hard bound copy of your thesis will be lodged in the Norma Smurfit Library and will be available for consultation. The electronic copy will be accessible in TRAP (http://trap.ncirl.ie/), the National College of Ireland’s Institutional Repository.