Evidence of Differences in the Effectiveness of Safety-Net Management in European Union Countries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PREFERENCE SHARES, NOMINAL VALUE of E2.24 PER SHARE, in the CAPITAL OF

11JUL200716232030 3JUL200720235794 11JUL200603145894 Public Offer by RFS Holdings B.V. FOR ALL OF THE ISSUED AND OUTSTANDING (FORMERLY CONVERTIBLE) PREFERENCE SHARES, NOMINAL VALUE OF e2.24 PER SHARE, IN THE CAPITAL OF ABN AMRO Holding N.V. Offer Memorandum and Offer Memorandum for ABN AMRO ordinary shares (incorporated by reference in this Offer Memorandum) 20 July 2007 This Preference Shares Offer expires at 15:00 hours, Amsterdam time, on 5 October 2007, unless extended. OFFER MEMORANDUM dated 20 July 2007 11JUL200716232030 3JUL200720235794 11JUL200603145894 PREFERENCE SHARES OFFER BY RFS HOLDINGS B.V. FOR ALL THE ISSUED AND OUTSTANDING PREFERENCE SHARES, NOMINAL VALUE OF e2.24 PER SHARE, IN THE CAPITAL OF ABN AMRO HOLDING N.V. RFS Holdings B.V. (‘‘RFS Holdings’’), a company formed by an affiliate of Fortis N.V. and Fortis SA/NV (Fortis N.V. and Fortis SA/ NV together ‘‘Fortis’’), The Royal Bank of Scotland Group plc (‘‘RBS’’) and an affiliate of Banco Santander Central Hispano, S.A. (‘‘Santander’’), is offering to acquire all of the issued and outstanding (formerly convertible) preference shares, nominal value e2.24 per share (‘‘ABN AMRO Preference Shares’’), of ABN AMRO Holding N.V. (‘‘ABN AMRO’’) on the terms and conditions set out in this document (the ‘‘Preference Shares Offer’’). In the Preference Shares Offer, RFS Holdings is offering to purchase each ABN AMRO Preference Share validly tendered and not properly withdrawn for e27.65 in cash. Assuming 44,988 issued and outstanding ABN AMRO Preference Shares outstanding as at 31 December 2006, the total value of the consideration being offered by RFS Holdings for the ABN AMRO Preference Shares is e1,243,918.20. -

La Presente Versione Del Documento Sostituisce Le Versioni Precedenti

STRUTTURA CONTI DEI PARTECIPANTI A T2S Page 1 La presente versione del documento sostituisce le versioni precedenti/ The current version substitute the previous one NEGOZIATORE/ LIQUIDATORE/ CLIENT OF THE SETTLEMENT AGENT SETTLEMENT AGENT CONTO CODICE BIC/ DEFAULT CODICE REGOLAMENTO DI TIPO CODICE CED/ CODICE ABI/ DESCRIZIONE BREVE/ CODICE ABI/ DESCRIZIONE BREVE/ PARTY BIC BIC CODE SETTLEMENT CED/ PARENT BIC SAC T2S DEFAULT/DEFAULT NEGOZIAZIONE/ CED CODE ABI CODE SHORT DESCRIPTION ABI CODE SHORT DESCRIPTION (PARTY1) (PARTY2) AGENT CED CODE SETTLEMENT DEALING CAPACITY ACCOUNT NEFOSESSXXX 180 22548 NEONET SECURITIES AB Y 1105 3069 INTESA SANPAOLO MOTIITMMXXX BCITITM1T01 MOTIBCITITMMXXX6016200 Y B BACRIT22XXX 302 3032 CRED.EMILIANO Y 302 3032 CRED.EMILIANO MOTIITMMXXX BACRIT22XXX MOTIBACRIT22XXX0303200 Y P BACRIT22XXX 302 3032 CRED.EMILIANO Y 302 3032 CRED.EMILIANO MOTIITMMXXX BACRIT22XXX MOTIBACRIT22XXX6303200 Y T BARCIT4GXXX 303 3051 BARCLAYS BANK Y 515 3479 BPSS MOTIITMMXXX PARBITMM011 MOTIPARBITMMXXX6048200 Y B DEUTITMMXXX 308 3104 DEUTSCHE BANK Y 308 3104 DEUTSCHE BANK MOTIITMMXXX DEUTITMMXXX MOTIDEUTITMMXXX6310400 Y T DEUTITMMXXX 308 3104 DEUTSCHE BANK Y 308 3104 DEUTSCHE BANK MOTIITMMXXX DEUTITMMXXX MOTIDEUTITMMXXX0310400 Y P BLOPIT22XXX 315 3111 UBI BANCA Y 315 3111 UBI BANCA MOTIITMMXXX BLOPIT22XXX MOTIBLOPIT22XXX0311100 Y P BLOPIT22XXX 315 3111 UBI BANCA Y 315 3111 UBI BANCA MOTIITMMXXX BLOPIT22XXX MOTIBLOPIT22XXX6311100 Y T FIBKITMMXXX 317 3296 FIDEURAM S.p.A. Y 1105 3069 INTESA SANPAOLO MOTIITMMXXX BCITITM1T02 MOTIBCITITMMXXX6010500 Y T FIBKITMMXXX 317 3296 FIDEURAM S.p.A. Y 1105 3069 INTESA SANPAOLO MOTIITMMXXX BCITITM1T02 MOTIBCITITMMXXX6003800 Y P IBSPITNAXXX 339 1010 SANPAOLO B.NAPOLI Y 1105 3069 INTESA SANPAOLO MOTIITMMXXX BCITITM1T13 MOTIBCITITMMXXX6021800 Y B CITIITMXXXX 352 3566 CITIBANK N.A. Y 352 3566 CITIBANK N.A. -

BILANCIO-2004.Pdf

Banca Antoniana Popolare Veneta Società per Azioni Capitale sociale Sede legale: 35131 Padova – Piazzetta Filippo Turati, 2 Registro Imprese PD? – Cod. Fiscale e Partita I.V.A. 02691680280 864.791.313,00 interamente versato Aderente al Fondo Interbancario di Tutela dei Depositi Capogruppo del Gruppo Banca Antoniana Popolare Veneta Iscritto all’Albo dei Gruppi Bancari BOZZA DI STAMPA Convocazione Assemblea Ordinaria dei Soci I Signori Soci di Banca Antonveneta S.p.A. (la “Banca”) sono convocati in Assemblea Ordinaria in prima convocazio- ne per il giorno sabato 30 aprile 2005 alle ore 10,00 in Padova, presso Palasport San Lazzaro – Via San Marco n. 53 e, occorrendo, in seconda convocazione per il giorno sabato 14 maggio 2005, stessa ora e luogo, per deliberare sul seguente O R D I N E D E L G I O R N O 1) Relazioni del Consiglio di Amministrazione e del Collegio Sindacale sull’esercizio 2004; esame del bilancio al 31 di- cembre 2004; deliberazioni inerenti e conseguenti e conferimento di poteri; 2) Relazioni del Consiglio di Amministrazione e del Collegio Sindacale sul bilancio consolidato al 31 dicembre 2004 del “Gruppo Bancario Banca Antoniana Popolare Veneta”; 3) Nomina dei componenti il Consiglio di Amministrazione, previa determinazione del loro numero e della durata in carica; determinazione delle medaglie di presenza ai sensi dell’art. 20 dello Statuto sociale; 4) Nomina dei componenti il Collegio Sindacale ai sensi dell’art. 27 dello Statuto sociale; determinazione dei relati- vi compensi. Per partecipare all’Assemblea i Soci dovranno richiedere all’intermediario presso cui sono depositati i titoli le certifi- cazioni rilasciate ai sensi dell’art. -

Annual Report 2005

annual report 2005 ABN AMRO Holding N.V. AA_AR05_Omslag_E.indd 1 21-03-2006 15:34:23 AA_AR05_Omslag_E.indd 1 21-03-2006 15:34:23 Profile ABN AMRO • is a prominent international bank with European roots dating back to 1824 • has over 3,500 branches in almost 60 countries and territories, a staff of about 97,000 full-time equivalents worldwide and total assets of EUR 881 billion as of year-end 2005 • is listed on Euronext (Amsterdam, Brussels and Paris) and the New York Stock Exchange. Our business strategy is built on five elements: 1 Creating value for our clients by offering high-quality financial solutions that best meet their current needs and long-term goals 2 Focusing on: - consumer and commercial clients in our local markets in Europe, North America, Latin America and Asia and globally on: - selected multinational corporations and financial institutions - private clients 3 Leveraging our advantages in products and people to benefit all our clients 4 Sharing expertise and operational excellence across the Group 5 Creating ‘fuel for growth’ by allocating capital and talent according to the principles of Managing for Value, our value-based management model. We aim for sustainable growth to benefit all our stakeholders: our clients, our shareholders, our employees, and society at large. In pursuing this goal we are guided by our Corporate Values (integrity, teamwork, respect and professionalism) and Business Principles. Acting with integrity is at the heart of our organisation: by complying in each of the markets in which we operate with the relevant laws and regulations, the bank safeguards its reputation and its licence to operate. -

Informe Anual Banco Santander Chile

Informe Anual Banco Santander Chile Informe Anual Banco Santander Chile 3 índice de Contenidos 2009 I. Reconocimientos Obtenidos en 2009 4 II. Indicadores Financieros 6 III. Carta del Presidente 9 IV. Directorio y Gobierno Corporativo 13 V. Administración 20 VI. Entorno de los Negocios 22 1. Economía Internacional 23 2. Economía Chilena 25 3. Sistema Financiero 25 VII. Pilares de Nuestra Gestión 2009 28 1. Cercanía con los Clientes 29 2. Creando Valor para Nuestros Accionistas 31 3. Liquidez y Solvencia 33 4. Construyendo Juntos el Mejor Lugar para Trabajar 35 5. Compromiso con la Sociedad 37 6. Manejo Integral del Riesgo 39 VIII. Análisis de la Gestión y Resultados 2009 44 1. Áreas de Negocios 44 2. Manejo Activo del Balance 47 3. Análisis de los Resultados 49 3. Gestión Activa del Riesgo y las Recuperaciones 52 4. Aumento en la Vinculación y Transaccionalidad 54 5. Mejora Continua de la Eficiencia 55 IX. Informe Anual Comité de Directores y Auditoría 58 X. Grupo Santander en el Mundo 63 XI. Estados Financieros Consolidados 75 XII. Estados Financieros Resumidos de las Empresas Filiales 211 1. Santander Asset Management S.A. Administradora General de Fondos 212 2. Santander S.A. Agente de Valores 214 3. Santander Corredora de Seguros Limitada 216 4. Santander S.A. Corredores de Bolsa 218 5. Santander S.A. Sociedad Securitizadora 220 6. Santander Servicios de Recaudación y Pagos Limitada 222 XIII. Información General 224 3 Reconocimientos Obtenidos en 2009 Banco Santander fue reconocido con más de Las principales revistas de finanzas del mundo, 15 distinciones en el año 2009, por la labor Global Finance, Latin Finance y Euromoney nos desarrollada en las distintas áreas que le competen distinguieron como el Mejor Banco en Chile, y como entidad financiera líder en el país. -

Download Pdf File of RBS Group Annual Report 2007

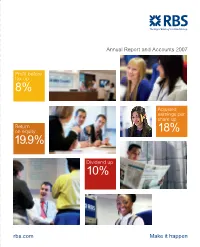

Annual Report and Accounts 2007 Profit before tax up 8% Adjusted earnings per share up Return on equity 18% 19.9% Dividend up 10% rbs.com Make it happen Highlights 2007 Contents Group operating profit up 9% 02 Measuring our success 04 Group profile to £10.3 billion 06 Divisional profile 08 Chairman’s statement 10 Group Chief Executive’s review Profit after tax up 19% to £7.7 billion Adjusted earnings per ordinary Divisional review share up 18% to 78.7p 13 Corporate Markets 15 Retail Markets 17 Ulster Bank 18 Citizens Total dividend up 10% to 33.2p 19 RBS Insurance 20 Manufacturing 21 ABN AMRO Tier 1 capital ratio 7.3% Total capital ratio 11.2% Corporate Responsibility 22 Combating crime 22 Building financial capability 23 Promoting financial inclusion 24 Customer service 24 Citizens in the community 25 Our employees 25 RBS and the environment Report and accounts 27 Business review 91 Governance 117 Financial statements 213 Additional information 235 Shareholder information RBS Group • Annual Report and Accounts 2007 01 Measuring our success Focus on growth and efficiency Income Adjusted cost:income ratio Group operating profit* (£m) (%) (£m) 07 31,115 07 43.9 07 10,282 06 28,002 06 42.1 06 9,414 05 25,569 05 42.4 05 8,251 04 22,515 pro forma 04 42.0 pro forma 04 7,108 pro forma The Group’s total income grew by 11% The Group’s cost:income ratio was 43.9%. Excluding ABN AMRO, Group operating profit increased by 9% to to £31,115 million in 2007. -

Investment Banking

PresentationPresentation toto FixedFixed IncomeIncome InvestorsInvestors June 2002 ContentsContents Mediobanca Section I Profile, shareholders and organisation chart Section II Wholesale - Corporate Banking Section III Wholesale - Investment Banking Section IV Retail financial services Section V Private Banking Section VI Research Section VII Capitalisation Section VIII Asset quality Section IX Cost efficiency, productivity and profitability Section X Treasury Section XI Business Plan 2002-2005 Section XII Transaction indicative highlights Appendices Appendix 1 Financial statements Appendix 2 Standard and Poor's ratings to italian financial institutions 2 ProfileProfile Mediobanca Profile, shareholders and organisation chart Section I p Mediobanca, founded in 1946, is the leading investment bank in Italy p Mediobanca’s central position in the Italian capital market is due to long-term close relationships with major Italian leading companies and with the international financial community p Business plan 2002-2005 focuses on enhancing wholesale banking business, developing private banking and private equity, adding international dimension to the bank’s structure p Core shareholders’ pact controls 46% of share capital. It was confirmed in 2001 until 2004 p Members of shareholders’ pact include key players in the Italian and European financial and business community p Market capitalisation as at 5th June 2002 was € 7.828bn p Mediobanca shares are constituents of Milan Stock Exchange “blue chip” index MIB 30 p Mediobanca enjoys excellent capitalisation: 19% Tier 1 at year end 2001, with no hybrid components p Regulated by Bank of Italy and Consob p Standard & Poors’ recently assigned AA- long term credit rating to Mediobanca with stable outlook, the best S&P rating to an Italian bank 3 ProfileProfile Mediobanca Profile, shareholders and organisation chart Section I MediobancaMediobanca GroupGroup Mediobanca S.p.A. -

ABN AMRO, 1990-Present

ABN AMRO History Department ABN AMRO, 1990-PRESENT The merger, 1990-1991 On 22 September 1991, the two largest general banks The South American operations of ABN AMRO’s subsidi- in the Netherlands, Algemene Bank Nederland (ABN) ary Hollandsche Bank-Unie were combined with those of and Amsterdam-Rotterdam Bank (Amro), merged. The Banco Real under the name Banco ABN AMRO Real. In resulting company adopted the name ABN AMRO. The the following years, more Brazilian take-overs followed, two principal motives for the merger were to concentrate and the country became the company’s third home market strengths and to scale up business internationally. after the Netherlands and the United States. Multiple take-overs occurred in Europe as well, such as that of the London stockbroking firm Hoare Govett (1992), the Swedish investment bank Alfred Berg (1995) and the centuries-old German private bank Delbrück & Co. (2002), which was merged with BethmannMaffei, an acquisition from 2004. In France Banque Odier Bungener Courvoisier, Banque Demachy and Banque du Phénix were acquired and merged with Banque de Neuflize, Schlumberger, Mallet to become Banque NSMD. After a long and controversial struggle regarding Banca Antonveneta, ABN AMRO acquired a majority stake in this Italian bank at the start of 2006. Barriers to growth An important reason for the creation of ABN AMRO was international strengthening and expansion. This goal was National and international expansion, 1990-2007 energetically pursued with many national and internati- In September 1990, the consumer credit activities in The onal acquisitions, but the company also divested itself Netherlands via intermediaries of the subsidiaries Finata, IDM and Mahuko were brought under a new subsidiary Interbank (sold in 2007). -

Annual Results 2008

Annual Results 2008 rbs.com Contents Page Forward-looking statements 3 Presentation of information 4 2008 Key points 5 Results summary – pro forma 7 Results summary – statutory 8 Chairman's review 9 Group Chief Executive's review 12 Pro forma results Summary consolidated income statement 16 Financial review 17 Description of business 20 Divisional performance 22 Global Markets Global Banking & Markets 23 Global Transaction Services 26 Regional Markets UK Retail & Commercial Banking 28 US Retail & Commercial Banking 35 Europe & Middle East Retail & Commercial Banking 38 Asia Retail & Commercial Banking 41 RBS Insurance 43 Group Manufacturing 45 Central items 46 Credit market exposures 47 Average balance sheet 48 Condensed consolidated balance sheet 50 Overview of condensed consolidated balance sheet 51 Notes 53 Analysis of income, expenses and impairment losses 57 Asset quality 58 Analysis of loans and advances to customers 58 Risk elements in lending 60 Regulatory ratios 61 Derivatives 63 Market risk 64 1 Contents (continued) Statutory results 65 Condensed consolidated income statement 66 Financial review 67 Condensed consolidated balance sheet 68 Overview of condensed consolidated balance sheet 69 Condensed consolidated statement of recognised income and expense 71 Condensed consolidated cash flow statement 72 Notes 73 Average balance sheet 85 Analysis of income, expenses and impairment losses 86 Asset quality 87 Analysis of loans and advances to customers 87 Risk elements in lending 89 Regulatory ratios 90 Derivatives 92 Market risk -

2007 Locandina.Pdf

invito Sotto l’Alto Patronato a palazzo 2007 del Presidente della Repubblica Con il Patrocinio del Ministero VI edizione per i Beni e le Attività Culturali Associazione Bancaria Italiana Associazione Bancaria Italiana - Commissione Regionale Abruzzo Banca Agricola Mantovana Banca Alpi Marittime una giornata Credito Cooperativo Carrù Banca Antonveneta Banca CR Firenze Banca Carige da non perdere Banca di Imola Banca di Piacenza Banca di Roma i palazzi delle banche aprono per voi Banca Etruria Banca Finnat Euramerica Banca Monte dei Paschi di Siena Banca Monte Parma Banca Popolare di Bergamo Banca Popolare di Milano Banca Popolare di Sondrio Banca Popolare di Vicenza Banca Popolare Sant’Angelo Banca Regionale Europea Banca Sella Nord Est Bovio Calderari Banca Toscana Banco di Sardegna Banco di Sicilia BNL - Gruppo BNP Paribas Capitalia Cariparma Cariprato Carisbo Carispaq Cassa dei Risparmi di Forlì e della Romagna Cassa di Risparmio di Ascoli Piceno Cassa di Risparmio di Asti Cassa di Risparmio di Cento Cassa di Risparmio di Cesena Cassa di Risparmio di Orvieto Cassa di Risparmio di Padova e Rovigo Cassa di Risparmio di Pistoia e Pescia Cassa di Risparmio di Ravenna Cassa di Risparmio di San Miniato Cassa di Risparmio di Venezia Credito Bergamasco Credito Emiliano Credito Valtellinese Deutsche Bank Dexia Crediop Friulcassa - Cassa di Risparmio Regionale sabato 6 ottobre 2007 dalle 10 alle 19 Intesa Sanpaolo MCC - Mediocredito Centrale ingresso gratuito Sanpaolo Banca dell’Adriatico Sanpaolo Banco di Napoli per informazioni UBI - Banco di Brescia UniCredit Banca o t t o n UniCredit Banca d’Impresa i • ritira il dépliant in banca v a i h UniCredit Gestione Crediti Banca c S telefona allo 06.6767990 dalle ore 10.00 alle ore 18.00 e • p UniCredit Private Banking p e s u i • [email protected] G o t o http://palazzi.abi.it f • e s e v a p i h c invito a palazzo c o r i t t è una manifestazione promossa dall’ABI - Associazione Bancaria Italiana e s s u realizzata con le banche aderenti al progetto m. -

ABN AMRO Holding N.V. Offer Memorandum Listing Particulars

11JUL200716232030 3JUL200720235794 11JUL200603145894 Public Offer by RFS Holdings B.V. FOR ALL THE ISSUED AND OUTSTANDING ORDINARY SHARES, NOMINAL VALUE OF e0.56 PER SHARE, IN THE CAPITAL OF ABN AMRO Holding N.V. Offer Memorandum and Listing Particulars 20 July 2007 This Offer expires at 15:00 hours, Amsterdam time, on 5 October 2007, unless extended. OFFER MEMORANDUM dated 20 July 2007 11JUL200716232030 3JUL200720235794 11JUL200603145894 PUBLIC OFFER BY RFS HOLDINGS B.V. FOR ALL THE ISSUED AND OUTSTANDING ORDINARY SHARES, NOMINAL VALUE OF e0.56 PER SHARE, IN THE CAPITAL OF ABN AMRO HOLDING N.V. RFS Holdings B.V. (‘‘RFS Holdings’’), a company formed by an affiliate of Fortis N.V. and Fortis SA/NV (Fortis N.V. and Fortis SA/NV together ‘‘Fortis’’), The Royal Bank of Scotland Group plc (‘‘RBS’’) and an affiliate of Banco Santander Central Hispano, S.A. (‘‘Santander’’), is offering to acquire all of the issued and outstanding ordinary shares, nominal value e0.56 per share (‘‘ABN AMRO Ordinary Shares’’), of ABN AMRO Holding N.V. (‘‘ABN AMRO’’), on the terms and conditions set out in this document (the ‘‘Offer’’). Under the terms of the Offer, holders of ABN AMRO Ordinary Shares will receive for each ABN AMRO Ordinary Share validly tendered and not properly withdrawn: • e35.60 in cash; and • 0.296 newly issued ordinary shares, nominal value £0.25 per share, of RBS (‘‘New RBS Ordinary Shares’’). For the purposes of the Dutch offer rules, the Offer extends to the ABN AMRO ADSs (as defined below), provided that, as further detailed below, the holders of ABN AMRO ADSs are referred to the U.S. -

Banco Santander Central Hispano, Sa

BANCO SANTANDER CENTRAL HISPANO, S.A. Acquisition of certain businesses of ABN AMRO Holding N.V. (“ABN AMRO”) for approximately €19.9 billion 29 May 2007 Summary Banco Santander Central Hispano, S.A. (“Santander ”), together with The Royal Bank of Scotland Group plc (“RBS ”) and Fortis N.V. and Fortis S.A./N.V. (“Fortis ”) (collectively, the “Banks ” and each a “Bank ”), has announced a proposed Offer (the “Offer ”) for all of the ABN AMRO ordinary shares. The Banks propose to offer €30.40 in cash plus 0.844 new RBS Shares for each ABN AMRO ordinary share, equating to €38.40 per ABN AMRO ordinary share 1. The total consideration payable to shareholders of ABN AMRO under the Offer would therefore be €71.1 billion 2. Further information relating to the proposed Offer is contained in the announcement made by the Banks today. Once the proposed Offer has been completed Santander will acquire the following core businesses from ABN AMRO (together the “ABN AMRO Businesses ”): • Business Unit Latin America (excluding wholesale clients outside Brazil) including, notably, the Banco Real (“Real ”) franchise in Brazil; • Banca Antonveneta (“Antonveneta ”) in Italy; and • Interbank and DMC Consumer Finance (“Interbank ”), a specialised consumer finance business in the Netherlands. It is expected that Santander will pay approximately €19.9 billion 2 or 27.9% of the total consideration payable under the proposed Offer. Of this amount, approximately €18.8 billion2 will be the share of consideration attributable to the ABN AMRO Businesses and the remainder will be the share of consideration attributable to Santander’s share of ABN AMRO’s shared assets.