China's State LNG Buyers Mull Force Majeure

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sven Olson, Leistritz, USA, Explains Why Multiphase Twin-Screw Subsea Pumps Are an Efficient Technology for Boosting Ageing, Low Energy Reservoirs and Long Tie-Backs

win-screw multiphase pumps have now been in and late life assets. These assets, referred to as brownfields, service for over 20 years, primarily in offshore topside have increased the emphasis on utilising existing structures T and onshore applications, with installations all over and facilities more efficiently to create acceptable financial the world. The primary objectives, such as reducing facility returns despite low oil prices. Investments in large offshore costs, boosting low pressure wells, reducing flaring and production facilities at current (and foreseeable) oil venting, and acting as a flow assurance tool, have all been prices do not seem to be the way the market will go. Most met. Operators have seen their production costs – especially existing process facilities are oversized and could benefit for mature reservoirs – drop and at the same time improved from more production. With excess available process revenue streams from increased production and higher total capacity, many operators are well equipped to go after recovery rate. The twin-screw technology with its special reservoir life extension and longer tieback projects. An features and advantages is attracting more and more interest often-used example is the present low recovery rate in the from the market. Gulf of Mexico, which often sees operators leave 60% of recoverable hydrocarbons still in place at abandonment. The Increased recovery from mature assets rate for the North Sea is much better, with some operators Changes in deepwater oil and production strategies in recent now striving to leave no more than 20 - 30% of hydrocarbons years have driven operators away from massive billion in place at the end of production. -

BLÜCHER Marine References

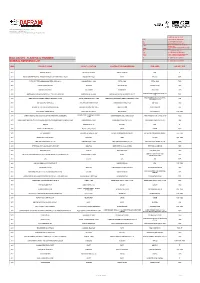

BLÜCHER Marine References Country Project Shipyard Owner Vessel Type Hull no. Year Argentina Frigate Naval Shipyard Frigate Frigate Refitting 2005 Australia Australian Customs and Austal Ships Australian Customs and Border Cape Class Patrol Boat 361 2013 Border Protection Service Protection Service Australia Australian Customs and Austal Ships Australian Customs and Border Cape Class Patrol Boat 362 2013 Border Protection Service Protection Service Australia Australian Customs and Austal Ships Australian Customs and Border Cape Class Patrol Boat 363 2013 Border Protection Service Protection Service Australia Australian Customs and Austal Ships Australian Customs and Border Cape Class Patrol Boat 364 2013 Border Protection Service Protection Service Australia Australian Customs and Austal Ships Australian Customs and Border Cape Class Patrol Boat 365 2014 Border Protection Service Protection Service Australia Australian Customs and Austal Ships Australian Customs and Border Cape Class Patrol Boat 366 2014 Border Protection Service Protection Service Australia Australian Customs and Austal Ships Australian Customs and Border Cape Class Patrol Boat 367 2014 Border Protection Service Protection Service Australia Australian Customs and Austal Ships Australian Customs and Border Cape Class Patrol Boat 368 2014 Border Protection Service Protection Service Australia Australian Defence Civmec/ASC Australian Defence OPV OPV1 2019 Australia Australian Defence - ASC Shipyard Australian Defence Air Warfare Destroyer 2012 AWD Australia Australian Defence - LHD BAE Systems Australian Defence Landing Helicpoter 2012 Dock Australia Dick Smith Tenix Dick Smith Ocean Research Ulysses Blue 2005 Vessel Australia Esso West Tuna Esso Platform 1996 Australia HMAS Arunta BAE Systems Australian Defence ANZAC Frigate ANZAC 2019 Australia Jean de la Valette - Virtu Austal Ships Virtu Ferries High Speed Ferry 248 2010 Ferries Australia RNZN Tenix RNZN Ocean Research 42826 2006 Vessel Australia Taylor Bros. -

Rosetti Marino, Italy

CASE STUDY ROSETTI MARINO, ITALY Key Facts ROSETTI MARINO SAVES TIME AND MONEY BY Company: Rosetti Marino AUTOMATING ISOMETRIC PRODUCTION Website: www.rosetti.it Intergraph Spoolgen® Produces Spool Drawings for the Workshop More Quickly and Efficiently Country: Italy Products Used: Rosetti Marino provides solutions and services to some of the biggest players PDS® in the oil and gas industry. With its strong engineering and project management Intergraph Spoolgen® capabilities and state-of-the-art fabrication facilities, Rosetti designs, procures, and constructs a wide range of fixed offshore platforms, process plants, and ships. Key Benefits: Focusing on process packages, pressure vessels, and shipbuilding to meet the • Simple to use demand of both mature and emerging markets, the company operates out of Rosetti • Eliminates errors and rework Marino’s original location in Ravenna, one of Italy’s leading commercial ports on the through data consistency north Adriatic Sea. Support offices are based in Croatia, Portugal, Kazakhstan, and • Automatically generates drawings Russia. and reports THE CHALLENGE • Saves tremendous amount of time • Provides rapid return on investment Rosetti Marino is comprised of its main fabrication yards in Ravenna, Italy, and two engineering subsidiaries: Fores Engineering, which manufactures and integrates process control and automation systems, and Basis Engineering, which provides multidisciplinary engineering services for the oil, gas, and petrochemical industries. When a new contract arrives, Basis Engineering uses PDS®, the market-leading 3D plant design system, to design how the project should be constructed. The system produces piping isometric drawings, which are then sent to the Rosetti fabrication yard. “We used to manually rework the engineering isometrics to add fabrication information such as weld numbers and line information,” said Claudio Antonellini, Rosetti’s engineering manager. -

Saipem13ing.Qxd 8-04-2014 10:20 AM Pagina I

001-064BilSaipem13Ing.qxd 8-04-2014 10:20 AM Pagina I Annual Report 2013 WorldReginfo - ff4b09bc-fd13-477b-a0ea-c961b0701766 Mission Pursuing satisfaction of our Clients in the energy industry, we tackle each challenge with safe, reliable and innovative solutions. Our competent, multi-local teams provide sustainable development for our Company and for the communities in which we operate. Our core values Commitment to health and safety, openness, flexibility, integration, innovation, quality, competitiveness, teamwork, humility, internationalisation, responsibility and integrity. Countries in which Saipem operates EUROPE Austria, Belgium, Croatia, Cyprus, Denmark, France, Greece, Italy, Luxembourg, Malta, Netherlands, Norway, Poland, Portugal, Romania, Spain, Sweden, Switzerland, Turkey, United Kingdom AMERICAS Bolivia, Brazil, Canada, Chile, Colombia, Dominican Republic, Ecuador, Mexico, Peru, Suriname, United States, Venezuela CIS Azerbaijan, Kazakhstan, Russia, Turkmenistan, Ukraine AFRICA Algeria, Angola, Cameroon, Congo, Egypt, Gabon, Ghana, Libya, Mauritania, Morocco, Mozambique, Nigeria, South Africa, Togo, Uganda MIDDLE EAST Iraq, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Yemen FAR EAST AND OCEANIA Australia, China, India, Indonesia, Japan, Malaysia, Myanmar, Pakistan, Papua New Guinea, Singapore, Thailand, Vietnam WorldReginfo - ff4b09bc-fd13-477b-a0ea-c961b0701766 Annual Report 2013 WorldReginfo - ff4b09bc-fd13-477b-a0ea-c961b0701766 Disclaimer By their nature, forward-looking statements are subject to risk and -

UK Energy Services Overview

UK energy services overview Incorporating the 10th annual UK oilfield services industry review March 2021 Contents Overview UK energy services industry — oilfield services sector | UK energy services overview March 2021 Key themes Challenging market but the Focus on survival and getting Energy transition is more Digital transformation is 1 recovery cycle has begun 2 fit for the future 3 prevalent than ever 4 accelerating Globally, the adoption of digitalisation, big data In 2020, oilfield services companies had to deal The restructuring of the industry is unfolding The pandemic has accelerated the allocation of and automation has increased pace in 2020 with the impact of both a global pandemic and and 2021 will continue to see significant capital towards sustainable companies and the and this trend is set to continue. The benefits a sharp oil price decline, at a time when many cost reduction measures and rationalisation energy transition of oilfield services companies. of digital are not only bringing internal benefits were still dealing with liquidity and balance of capacity, through asset retirements, Environmental, social and governance (ESG) through the reduction of operating costs sheet issues and struggling to deploy their bankruptcies and consolidation. Challenging themes are increasingly at the forefront for but also offering new revenue opportunities assets in oversupply markets. Faced with a market conditions, debt and equity investors shareholders and investors. This is shaping the through bringing digital solutions to customers sharp decrease in their customer capex spend have forced greater capital discipline on investment strategies of the oil and gas majors and digitalising the energy transition. While (c.30%), a significant part of their focus has operators and contractors. -

Fascicolo Bilancio Consolidato 06 2019 Con

Half-year consolidated financial statements as at 30 June 2019 1/64 Consolidated financial statements as at 30 June 2019 - Rosetti Marino S.p.A. C O N T E N T S Page Board of Directors' report on operations accompanying the consolidated financial statements as at 30/06/2019: 3 Half-year consolidated financial statements as at 30 June 2019: - Balance sheet 19 - Income statement 21 - Cash flow statement 22 - Explanatory notes • Presentation and content of the consolidated financial statements 23 • Consolidation principles 24 • Scope of consolidation 26 • Reconciliation of the parent company's shareholders' equity and profit/loss and corresponding consolidated figures 28 • Valuation principles 29 • Comments on main asset items • Comments on main liability items 46 • Comments on main income statement items 55 • Other information 60 - Annexes: • Statement of changes in shareholders' equity 62 • Statement of changes in tangible fixed assets 63 • Statement of temporary differences that resulted in the recognition of deferred tax assets and liabilities 64 2/64 Consolidated financial statements as at 30 June 2019 - Rosetti Marino S.p.A. BOARD OF DIRECTORS' REPORT ON OPERATIONS ACCOMPANYING THE CONSOLIDATED FINANCIAL STATEMENTS AS AT 30 JUNE 2019 3/64 Consolidated financial statements as at 30 June 2019 - Rosetti Marino S.p.A. Dear Shareholders, The consolidated financial statements of the Group for the first half of 2019, which we hereby submit for your approval, closed with a net profit of Euro 2,147 thousand, after recognising Euro 2,825 thousand in depreciation and amortisation, Euro 755 thousand for write-downs of current assets and provisions for risks of Euro 6,572 thousand. -

Members' Directory 2019-2020

Directory Sponsor MEMBERS’ DIRECTORY RenewableUK 2019-2020 Members’ Directory 2019-2020 Members’ Directory Micro Grid Renewables Generation Solar Electricity Trading Transmission Distribution Demand-Side Centralised Power Response Generation Smart Storage Cities Wind Smart Homes User Demand EVs 25 EUR million Sales in more than Established 6 manufacturing State of the art average annual investments facilities (last 3 years) 50 countries 1950 plants in 3 countries Who we are Tracing its industrial roots back to 1950, Cablel® Hellenic Cables has evolved into a leading European provider of reliable and competitive cable solutions. With 6 manufacturing plants across 3 countries, Cablel® Hellenic Cables covers a wide range of cable products and solutions, from Land and Submarine Power cables to Fiber Optics, Telecommunication cables and Magnet Wires. Cablel® Hellenic Cables offers a wide range of integrated solutions, including design, manufacturing, planning, project management and installation. In-house R&D and testing facilities guarantee continuous product development and innovation. As the world’s need for sustainable and reliable flow of energy and information continues to increase, we remain focused on our mission to provide top-quality products and services meeting the highest technical and sustainability standards set by our customers. HEAD OFFICE: 33, Amaroussiou - Halandriou Str., 151 25 Maroussi, Athens, GREECE Tel.: +30 210 6787 416, +30 210 6787 900, Fax: +30 210 6787 406 [email protected] www.cablel.com 09-13-2019_KX_CABLEL_168x240mm_FINAL.indd -

Shipowner Orderbook Monitor

ShipOwner Orderbook Monitor Volume 19, No.1 January-2012 Licensed to HSBC Bank plc. Distribution is restricted; please remember acknowledge the source. http://www.clarksons.net 26/01/2012 08:13:21 67853 Orderbooks by Owner Country Major European Shipyards Rank Country No. m. cgt 1 China P.R. 789 15.5 7 26 2 Greece 552 14.7 SELECTED SHIPYARDS 3 Japan 379 8.8 1. Daewoo Mangalia, Rom. 14. Ferus Smit, Neths. 2. Santierul Naval, Romania 15. Brod. 3 Maj, Croatia 4 Germany 433 8.8 3. Meyer Werft, Germany 16. Sedef Gemi End., Turkey 4. Brod. Uljanik, Croatia 17. Brodosplit, Croatia 5 South Korea 201 4.8 5. STX Europe, France 18. Rousse Shipyard, Bulg. 6. Brod. Trogir, Croatia 19. Flensburger S.B, Ger. 19 21 7. STX Finnyards, Finland 20. Besiktas Shipyard, Tur. 6 United States 194 4.7 22 8. Schps. Bodewes, Neths. 21. P+S Werften, Germany 12 9. Celiktekne, Turkey 22. Damen S’yards, Neths. 8 3 7 Norway 288 4.6 11 10. Volgograd S.Y., Russia 23. UM Deniz Shipyard, Tur. 14 11. IHC Dredgers, Neths. 24. Bulyard, Varna, Bulgaria 8 Singapore 299 4.5 12. Peters Kampen, Neths. 25. Anadolu Shipyard, Tur. 13. Marmara Tersaneri, Tur. 26. Nevsky S.B., Russia 9 Taiwan 141 4.1 10 10 Denmark 142 3.7 5 11 Hong Kong 169 3.4 2 15 12 Israel 85 2.9 4 1 6 18 13 Turkey 170 2.8 17 24 13 14 Brazil 112 2.6 25 9 20 23 15 Italy 103 2.2 16 16 India 133 1.8 Other 1,706 25.1 GLOBAL TOTAL 5,896 115.0 Orderbook by Owner Major Far Eastern Shipyards Rank Company No. -

Bilancio 1993 Rosetti

Consolidated financial statements as at 30 June 2020 - Rosetti Marino S.p.A. Half-year consolidated financial statements as at 30/06/2020 1/65 Consolidated financial statements as at 30 June 2020 - Rosetti Marino S.p.A. C O N T E N T S Page Board of Directors' report on operations accompanying the consolidated financial statements as at 30/06/2020: 3 Half-year consolidated financial statements as at 30 June 2020: - Balance sheet 18 - Income statement 20 - Cash flow statement 21 - Explanatory notes Presentation and content of the consolidated financial statements 22 Consolidation principles 23 Scope of consolidation 24 Reconciliation of the shareholders' equity and profit (loss) for the period of the Parent Company and the corresponding consolidated figures 27 Valuation principles 27 Comments on main asset items 35 Comments on main liability items 44 Comments on main income statement items 56 Other information 62 - Annexes: Statement of changes in shareholders' equity 63 Statement of changes in tangible fixed assets 64 Statement of temporary differences that resulted in the recognition of deferred tax assets and liabilities 65 2/65 Consolidated financial statements as at 30 June 2020 - Rosetti Marino S.p.A. BOARD OF DIRECTORS' REPORT ON OPERATIONS ACCOMPANYING THE CONSOLIDATED FINANCIAL STATEMENTS AS AT 30 JUNE 2020 3/65 Consolidated financial statements as at 30 June 2020 - Rosetti Marino S.p.A. Dear Shareholders, The consolidated financial statements of the Group for the first half of 2020 which we hereby submit for your approval closed with a net loss of Euro 17,058 thousand, after recognising Euro 3,406 thousand in depreciation and amortisation and Euro 23 thousand of write-downs of current assets. -

INTERIM FINANCIAL REPORT AS of JUNE 30, 2020 001-078Saipemsem20ing.Qxd 3-08-2020 16:55 Pagina II

001-078SaipemSem20Ing.qxd 3-08-2020 16:55 Pagina I INTERIM FINANCIAL REPORT AS OF JUNE 30, 2020 001-078SaipemSem20Ing.qxd 3-08-2020 16:55 Pagina II Mission Our mission is to implement challenging, safe and innovative projects, leveraging on the competence of our people and on the solidity, multiculturalism and integrity of our organisational model. With the ability to face and overcome the challenges posed by the evolution of the global scenarios, we must seize the opportunities to create economic and social value for all our stakeholders. OUR VALUES Innovation; health, safety and environment; multiculturalism; passion; integrity. Disclaimer By their nature, forward-looking statements are subject to risk and uncertainty since they are dependent upon circumstances which should or are considered likely to occur in the future and are outside of the Group’s control. These include, but are not limited to: exchange and interest rate fluctuations, commodity price volatility, credit and liquidity risks, HSE risks, the levels of capital expenditure in the oil and gas industry and other sectors, political instability in areas where the Group operates, actions by competitors, success of commercial transactions, risks associated with the execution of projects (including ongoing investment projects), the recent Coronavirus outbreak (including its impact across our business, worldwide operations and supply chain); in addition to changes in stakeholders’ expectations and other changes affecting business conditions. Actual results could therefore differ materially from the forward-looking statements. The financial reports contain in-depth analyses of some of the aforementioned risks. Forward-looking statements are to be considered in the context of the date of their release. -

Company Profile

COMPANY PROFILE 27 April 2018 COMPANY PROFILE Rosetti Marino is the operating parent company of a leading group whose core business is designing and building off-shore oil and gas platforms under EPC (engineering, procurement and construction) contracts (79,4% of total consolidated 2017 revenue), designing and building service and work vessels (1,5% of the total) and building COMPANY INFORMATION processing plants (19,1% of the total). The company has two construction yards in the Share cap. €4,000,000 Port of Ravenna while the third is located a few km away from the city of Aktau, on Registered office: the Kazakh shore of the Caspian Sea. Its main clients include major oil companies and Via Trieste, 230 the leading international contractors active in the industry, in addition to Europe's 48122 Ravenna (RA) main builders of service vessels. Italy B oard of Directors Top Management Auditors Tel. +39 0544 878.111 Stefano Silvestroni Fabio Iarocci Gian Luigi Facchini Fax. +39 0544 878.188 Chairman Energy Operations Manager Chairman of the Board of Auditors www.rosetti.it Oscar Guerra Luca Barchiesi Renzo Galeotti CEO – Chief Executive Off. CFO – Chief Financial Off. Standing Auditor SHAREHOLDERS Medardo Ranieri Ermanno Bellettini Massimo Luigi Roberto Invernizzi Vice Chairman Corporate System Dept. Standing Auditor Luca Barchiesi Stefano Silvestroni Vice Chairman and General and Legal Affairs Dept. Supervisory Board Managing Director Stefano Cappelli Legislative Decree 231/01 Ermanno Bellettini Commercial & Development Dept.Francesco Pellei Luca Gentili Cesario Mondelli Chairman Giorgio Zuffa Shipbuilding Director Adolfo Mancanelli Investor Relations Procurement & Logistics Dept. Alfonso Levote 2017 CONSOLIDATED FINANCIAL STATEMENTS Income Statement Balance Sheet €/000 31/12/17 €/000 31/12/17 Total revenue (GIP) 189,509 Intangible assets 1,893 Prop., plant and equip. -

General Reference List Ball Valves

62010 URBISAGLIA (MC) - SS 78 Km 6 - ITALY www.dafram.it - [email protected] Tel. +39.(0)733.51191 - Fax. +39.(0)733.50196 tel. +39.(0)733.51191 LEGENDA: VALVE TYPE FSE FSE: FLOATING SIDE-ENTRY FT FT: FLOATING TOP-ENTRY FW FW: FLOATING WELDED BODY FDBB: FLOATING MODULAR DB&B, FDBB DOUBLE BALL TSEB: TRUNNION SIDE-ENTRY BOLTED TSEB BODY TT TT: TRUNNION TOP-ENTRY TW TW: TRUNNION WELDED BODY TDBB: TRUNNION MODULAR DOUBLE TDBB BLOCK & BLEED, DOUBLE BALL BALL VALVES - FLOATING & TRUNNION 3F 3F: THREE WAYS FLOATING GENERAL REFERENCE LIST 3T 3T: THREE WAYS TRUNNION YEAR PROJECT NAME PLANT LOCATION CONTRACTOR ENGINEERING END USER VALVE TYPE 2011 HARWEEL PHASE 3 SULTANATE OF OMAN WORLEY PARSONS PDO TT 2011 RAS SHUKIER FIRE FIGHTING, PROPANE STORAGE & UTILITIES FOR NGL PLANT RAS SHUKIER - Egypt ENPPI EBGDCO TSEB 2011 PP PROJECT PETROCHINA NINGXIA PETROCHEMICAL CO. NINGXIA REGION - CHINA PETROCHINA PETROCHINA TSEB 2011 ENG P22 HARALD BY-PASS DENMARK MAERSK OIL DK MAERSK OIL DK TSEB 2011 KHANNUR LNG VESSEL LNG CARRIER HAMWORTHY GOLAR LNG TSEB INNER MONGOLIA DONGHUA ENERGY CO 2011 INNER MONGOLIA DONGHUA ENERGY CO. LTD COAL SLURRY SDV INNER MONGOLIA - CHINA INNER MONGOLIA DONGHUA ENERGY CO LTD TSEB LTD INNER MONGOLIA TALENT CHEMICAL 2011 INNER MONGOLIA TALENT CHEMICAL FERTILIZER CO. LTD JUNGAR - INNER MONGOLIA - CHINA INNER MONGOLIA TALENT CHEMICAL FERTILIZER CO. LTD FSE FERTILIZER CO. LTD 2011 GDF SUEZ CAPE ANN VESSEL CAPE ANN LNG CARGO CARRIER SAMSUNG HEAVY INDUSTRIES GDF SUEZ TSEB 2011 EKOFISK 2/4L - HOT WATER SERVICE PACKAGE EKOFISK PLATFORM - NORTH SEA AKER SOLUTIONS CONOCO PHILLIPS FSE 2011 FSPO ATHENA CARMEN VESSEL NORTH SEA - UK SECTOR BW OFFSHORE ITACHA ENERGY FSE - TSEB QINYUAN COUNTY - CHANGZHI - SHANXI - 2011 SHANXI TONGZHOU COKE GROUP 100.000 TONS/A METHANOL ENGINEERING SHANXI TONGZHOU CIAL COKING GROUP SHANXI TONGZHOU CIAL COKING GROUP TSEB CHINA 2011 ANHUI LIUGUO CHEMICAL CO LTD.