Annual Report 2008

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

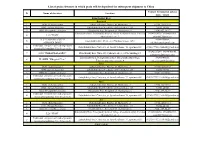

Catalogue of Exporters of Primorsky Krai № ITN/TIN Company Name Address OKVED Code Kind of Activity Country of Export 1 254308

Catalogue of exporters of Primorsky krai № ITN/TIN Company name Address OKVED Code Kind of activity Country of export 690002, Primorsky KRAI, 1 2543082433 KOR GROUP LLC CITY VLADIVOSTOK, PR-T OKVED:51.38 Wholesale of other food products Vietnam OSTRYAKOVA 5G, OF. 94 690001, PRIMORSKY KRAI, 2 2536266550 LLC "SEIKO" VLADIVOSTOK, STR. OKVED:51.7 Other ratailing China TUNGUS, 17, K.1 690003, PRIMORSKY KRAI, VLADIVOSTOK, 3 2531010610 LLC "FORTUNA" OKVED: 46.9 Wholesale trade in specialized stores China STREET UPPERPORTOVA, 38- 101 690003, Primorsky Krai, Vladivostok, Other activities auxiliary related to 4 2540172745 TEK ALVADIS LLC OKVED: 52.29 Panama Verkhneportovaya street, 38, office transportation 301 p-303 p 690088, PRIMORSKY KRAI, Wholesale trade of cars and light 5 2537074970 AVTOTRADING LLC Vladivostok, Zhigura, 46 OKVED: 45.11.1 USA motor vehicles 9KV JOINT-STOCK COMPANY 690091, Primorsky KRAI, Processing and preserving of fish and 6 2504001293 HOLDING COMPANY " Vladivostok, Pologaya Street, 53, OKVED:15.2 China seafood DALMOREPRODUKT " office 308 JOINT-STOCK COMPANY 692760, Primorsky Krai, Non-scheduled air freight 7 2502018358 OKVED:62.20.2 Moldova "AVIALIFT VLADIVOSTOK" CITYARTEM, MKR-N ORBIT, 4 transport 690039, PRIMORSKY KRAI JOINT-STOCK COMPANY 8 2543127290 VLADIVOSTOK, 16A-19 KIROV OKVED:27.42 Aluminum production Japan "ANKUVER" STR. 692760, EDGE OF PRIMORSKY Activities of catering establishments KRAI, for other types of catering JOINT-STOCK COMPANY CITYARTEM, STR. VLADIMIR 9 2502040579 "AEROMAR-ДВ" SAIBEL, 41 OKVED:56.29 China Production of bread and pastry, cakes 690014, Primorsky Krai, and pastries short-term storage JOINT-STOCK COMPANY VLADIVOSTOK, STR. PEOPLE 10 2504001550 "VLADHLEB" AVENUE 29 OKVED:10.71 China JOINT-STOCK COMPANY " MINING- METALLURGICAL 692446, PRIMORSKY KRAI COMPLEX DALNEGORSK AVENUE 50 Mining and processing of lead-zinc 11 2505008358 " DALPOLIMETALL " SUMMER OCTOBER 93 OKVED:07.29.5 ore Republic of Korea 692183, PRIMORSKY KRAI KRAI, KRASNOARMEYSKIY DISTRICT, JOINT-STOCK COMPANY " P. -

Conservation Investment Strategy for the Russian Far East AUTHORSHIP and ATTRIBUTION

SASHA LEAHOVCENCO PACIFIC ENVIRONMENT DAVID LAWSON, WWF ELAINE R. WILSON Conservation Investment Strategy Strategy Investment Conservation EXECUTIVE SUMMARY for the Russian Far East Far for the Russian Pacific Environment Pacific 2 Conservation Investment Strategy for the Russian Far East AUTHORSHIP AND ATTRIBUTION Executive Editors: Evan Sparling (Pacific Environment) Eugene Simonov (Pacific Environment, Rivers Without Boundaries) Project Coordinating Team: Eduard Zdor (Chukotka Association of Traditional Marine Mammal Hunters) Dmitry Lisitsyn (Sakhalin Environment Watch) Anatoly Lebedev (Bureau for Regional Outreach Campaigns) Sergey Shapkhaev (Buryat Regional Association for Baikal) Peer Review Group: Alan Holt (Margaret A. Cargill Foundation) David Gordon (Goldman Environmental Prize) Xanthippe Augerot (Pangaea Environmental LLC.) Peter Riggs (Pivot Point) Jack Tordoff (Critical Ecosystems Partnership Fund) Dmitry Lisitsyn (Sakhalin Environment Watch) Conservation Planning Expert: Nicole Portley (Sustainable Fisheries Partnership) Writing and Design: John Byrne Barry Additional Writing and Translating: Sonya Kleshik Special thanks to the following for their contributions to this assessment: Marina Rikhvanova (Baikal Environment Wave), Maksim Chakilev, Yuri Khokhlov, Anatoly Kochnev (Chukotka Branch of the Pacific Ocean Institute for Fisheries and Oceanography), Natalya Shevchenko (Chukotka Regional Department of the Environment (retired)), Oleg Goroshko (Daursky Biosphere Reserve), Elena Tvorogova (Foundation for Revival of Siberian -

Final Report ______January 01 –December 31, 2003

Phoenix Final Report ____________________________________________________________________________________ January 01 –December 31, 2003 FINAL REPORT January 01 – December 31, 2003 The Grantor: Save the Tiger Fund Project No: № 2002 – 0301 – 034 Project Name: “Operation Amba Siberian Tiger Protection – III” The Grantee: The Phoenix Fund Report Period: January 01 – December 31, 2003 Project Period: January 01 – December 31, 2003 The objective of this project is to conserve endangered wildlife in the Russian Far East and ensure long-term survival of the Siberian tiger and its prey species through anti-poaching activities of Inspection Tiger and non-governmental investigation teams, human-tiger conflict resolution and environmental education. To achieve effective results in anti-poaching activity Phoenix encourage the work of both governmental and public rangers. I. KHABAROVSKY AND SPECIAL EMERGENCY RESPONSE TEAMS OF INSPECTION TIGER This report will highlight the work and outputs of Khabarovsky anti-poaching team and Special Emergency Response team that cover the south of Khabarovsky region and the whole territory of Primorsky region. For the reported period, the Khabarovsky team has documented 47 cases of ecological violations; Special Emergency Response team has registered 25 conflict tiger cases. Tables 1 and 2 show the results of both teams. Conflict Tiger Cases The Special Emergency Response Team works on the territory of Primorsky region and south of Khabarovsky region. For the reported period, 25 conflict tiger cases have been registered and investigated by the Special Emergency Response team of Inspection Tiger, one of them transpired to be a “false alarm”. 1) On January 04, 2003 the Special Emergency Response team received information from gas filling station workers that in the vicinity of Terney village they had seen a tiger with a killed dog crossing Terney-Plastun route. -

China Russia

1 1 1 1 Acheng 3 Lesozavodsk 3 4 4 0 Didao Jixi 5 0 5 Shuangcheng Shangzhi Link? ou ? ? ? ? Hengshan ? 5 SEA OF 5 4 4 Yushu Wuchang OKHOTSK Dehui Mudanjiang Shulan Dalnegorsk Nongan Hailin Jiutai Jishu CHINA Kavalerovo Jilin Jiaohe Changchun RUSSIA Dunhua Uglekamensk HOKKAIDOO Panshi Huadian Tumen Partizansk Sapporo Hunchun Vladivostok Liaoyuan Chaoyang Longjing Yanji Nahodka Meihekou Helong Hunjiang Najin Badaojiang Tong Hua Hyesan Kanggye Aomori Kimchaek AOMORI ? ? 0 AKITA 0 4 DEMOCRATIC PEOPLE'S 4 REPUBLIC OF KOREA Akita Morioka IWATE SEA O F Pyongyang GULF OF KOREA JAPAN Nampo YAMAJGATAA PAN Yamagata MIYAGI Sendai Haeju Niigata Euijeongbu Chuncheon Bucheon Seoul NIIGATA Weonju Incheon Anyang ISIKAWA ChechonREPUBLIC OF HUKUSIMA Suweon KOREA TOTIGI Cheonan Chungju Toyama Cheongju Kanazawa GUNMA IBARAKI TOYAMA PACIFIC OCEAN Nagano Mito Andong Maebashi Daejeon Fukui NAGANO Kunsan Daegu Pohang HUKUI SAITAMA Taegu YAMANASI TOOKYOO YELLOW Ulsan Tottori GIFU Tokyo Matsue Gifu Kofu Chiba SEA TOTTORI Kawasaki KANAGAWA Kwangju Masan KYOOTO Yokohama Pusan SIMANE Nagoya KANAGAWA TIBA ? HYOOGO Kyoto SIGA SIZUOKA ? 5 Suncheon Chinhae 5 3 Otsu AITI 3 OKAYAMA Kobe Nara Shizuoka Yeosu HIROSIMA Okayama Tsu KAGAWA HYOOGO Hiroshima OOSAKA Osaka MIE YAMAGUTI OOSAKA Yamaguchi Takamatsu WAKAYAMA NARA JAPAN Tokushima Wakayama TOKUSIMA Matsuyama National Capital Fukuoka HUKUOKA WAKAYAMA Jeju EHIME Provincial Capital Cheju Oita Kochi SAGA KOOTI City, town EAST CHINA Saga OOITA Major Airport SEA NAGASAKI Kumamoto Roads Nagasaki KUMAMOTO Railroad Lake MIYAZAKI River, lake JAPAN KAGOSIMA Miyazaki International Boundary Provincial Boundary Kagoshima 0 12.5 25 50 75 100 Kilometers Miles 0 10 20 40 60 80 ? ? ? ? 0 5 0 5 3 3 4 4 1 1 1 1 The boundaries and names show n and t he designations us ed on this map do not imply of ficial endors ement or acceptance by the United N at ions. -

Research Journal of Pharmaceutical, Biological and Chemical Sciences

ISSN: 0975-8585 Research Journal of Pharmaceutical, Biological and Chemical Sciences Concentration of Gold from Ash and Slag Wastes of Energy Sector Enterprises of The Primorsky Territory. Evgeny Ivanovich Shamray1*, Andrey Vasilyevich Taskin2, Sergey Igorevich Ivannikov1, and Alexander Alekseevich Yudakov1. 1 Institute of chemistry FEB RAS, 690022, Russia, Vladivostok, Prosp. 100-letya Vladivostoka, 159. 2Far Eastern Federal University, 690091, Russia, Vladivostok, Sukhanova str., 8. ABSTRACT The study of a large array of ash waste from landfills of energy sector enterprises in Primorsky Territory was made. Data on the content of gold and silver in the ash and slug waste of some energy enterprises in Primorsky Territory was given. Group of samples with high content of gold and silver was found. Silver content was found within 0.5-29.7 g/t limits. Gold content was found within 0.004–0.45 g/t limits. The information on the chemical composition of the investigated slag samples was given. Based on these data, the method of separation of ash and slag waste in the individual mineral fractions was proposed. The possibility of gold concentration in the non-magnetic fraction of the slag cleared of silt, clay, black charcoal and magnetic minerals was shown. Keywords: technogenic deposits, wastes of energy enterprises, ash and slag waste (ASW), gold, silver, atomic and absorption analysis, neutron-activation analysis, X-ray fluorescence analysis. *Corresponding Author November – December 2016 RJPBCS 7(6) Page No. 156 ISSN: 0975-8585 INTRODUCTION Ash and slag waste (ASW) is formed during coal combustion process in energy producing enterprises. For example, in recent years, yearly inflow of ASW into the ash and slag disposal areas of Primorsky Territory is up to 3.0 million tons. -

List of Grain Elevators in Which Grain Will Be Deposited for Subsequent Shipment to China

List of grain elevators in which grain will be deposited for subsequent shipment to China Contact Infromation (phone № Name of elevators Location num. / email) Zabaykalsky Krai Rapeseed 1 ООО «Zabaykalagro» Zabaykalsku krai, Borzya, ul. Matrosova, 2 8-914-120-29-18 2 OOO «Zolotoy Kolosok» Zabaykalsky Krai, Nerchinsk, ul. Octyabrskaya, 128 30242-44948 3 OOO «Priargunskye prostory» Zabaykalsky Krai, Priargunsk ul. Urozhaynaya, 6 (924) 457-30-27 Zabaykalsky Krai, Priargunsky district, village Starotsuruhaytuy, Pertizan 89145160238, 89644638969, 4 LLS "PION" Shestakovich str., 3 [email protected] LLC "ZABAYKALSKYI 89144350888, 5 Zabaykalskyi krai, Chita city, Chkalova street, 149/1 AGROHOLDING" [email protected] Individual entrepreneur head of peasant 6 Zabaykalskyi krai, Chita city, st. Juravleva/home 74, apartment 88 89243877133, [email protected] farming Kalashnikov Uriy Sergeevich 89242727249, 89144700140, 7 OOO "ZABAYKALAGRO" Zabaykalsky krai, Chita city, Chkalova street, 147A, building 15 [email protected] Zabaykalsky krai, Priargunsky district, Staroturukhaitui village, 89245040356, 8 IP GKFH "Mungalov V.A." Tehnicheskaia street, house 4 [email protected] Corn 1 ООО «Zabaykalagro» Zabaykalsku krai, Borzya, ul. Matrosova, 2 8-914-120-29-18 2 OOO «Zolotoy Kolosok» Zabaykalsky Krai, Nerchinsk, ul. Octyabrskaya, 128 30242-44948 3 OOO «Priargunskye prostory» Zabaykalsky Krai, Priargunsk ul. Urozhaynaya, 6 (924) 457-30-27 Individual entrepreneur head of peasant 4 Zabaykalskyi krai, Chita city, st. Juravleva/home 74, apartment 88 89243877133, [email protected] farming Kalashnikov Uriy Sergeevich Rice 1 ООО «Zabaykalagro» Zabaykalsku krai, Borzya, ul. Matrosova, 2 8-914-120-29-18 2 OOO «Zolotoy Kolosok» Zabaykalsky Krai, Nerchinsk, ul. Octyabrskaya, 128 30242-44948 3 OOO «Priargunskye prostory» Zabaykalsky Krai, Priargunsk ul. -

Primorsky Krai 165,900 Sq

PRIMORSKY KHABAROVSK Trans- Siberian Railroad Russian Far East Amur River JAO Agzu Samarga Edinka POZHARSKY Svetlaya POZHARSKY Ulunga Verkhne Pereval Vostok Luchegorsk Krasny Yar Kuznetsovo Ignatevka Pozharskoe Maximovka Guberovo Glubinnoe CHINA Amgu !. Dalnerechensk Roshchino TERNEISKY Lazo Novopokrovka KRASNOARMEISKY Rakitnoe Velikaya Kema Tamga DALNERECHENSKY Malaya Kema Melnichnoe !. Lesozavodsk SKY LESOZAVOD Tury Rog Gornye Klyuchi Ternei Ariadnoe Kirovsky ¯ Novokachalinsk Lake lroad Dalny Kut KIROVSKY ORSKY KHANKA Rai Ilinka Plastun Khanka Gorny km DALNEG Cheremshany Dvoryanka berian PO ISKY Samarka Kamen-Rybolov Krasnorechensky 100 GRANICHNY Dalnegorsk !. Zharikovo Tr!.ans-SiSpassk-Dalny KY Koksharovka SPASSKY Kamenka KHOROLS AKOLEVS Khrustalny Pogranichny Khorol Y Yakovlevka EVSKY Rudny Rudnaya Pristan ! CH UGU CHERNIGOVSKY !Kavalerovo EROVSKY KY Lipovtsy ! Sibirtsevo Chuguevka KAVAL ! !. ANUCHINSKY Arsenev Yaroslavsky OKTYABRSKY Vesely Yar n MI Mikhailovka Pokrovka KHAILOVSKY Anuchino Olga a Mikhailovka Arkhipovka Nikolo-Lvovskoe !. OLGINSKY PARTI p USSURIISKY UssuriiskSHKO Terekhovka a ZANSKY TOVSKY Margaritovo NADEZHDINSKY Lazo J Sergeevka Uglovoe Artem ! !. ! Smolyaninovo ZOVSKY LA Valentin f Primorsky !. P! !. Bolshoi Kamen Partizansk o ! Russky Nakhodka Preobrazhenie ! . Popova ! a Kraskino KHASANSKY Poset Slavyanka e VLADIVOSTOK S Map 2.1 Zarubino Khasan Primorsky Krai 165,900 sq. km Newell, J. 2004. The Russian Far East: A Reference Guide for Conservation and Development. McKinleyville, CA: Daniel & Daniel. 466 pages By Newell and Zhou / Sources: Ministry of Natural Resources, 2002; ESRI, 2002. 110 Ⅲ THE RUSSIAN FAR EAST CHAPTER 2 Primorsky Krai PRIMORSKY Location Situated along the southeastern border of the rfe, Primorsky Krai, or Primorie, shares a common border with China in the west and Khabarovsk Krai in the north. To the east lies the Sea of Japan, which separates Primorsky from Japan by only 400 km. -

Amur Oblast TYNDINSKY 361,900 Sq

AMUR 196 Ⅲ THE RUSSIAN FAR EAST SAKHA Map 5.1 Ust-Nyukzha Amur Oblast TY NDINS KY 361,900 sq. km Lopcha Lapri Ust-Urkima Baikal-Amur Mainline Tynda CHITA !. ZEISKY Kirovsky Kirovsky Zeiskoe Zolotaya Gora Reservoir Takhtamygda Solovyovsk Urkan Urusha !Skovorodino KHABAROVSK Erofei Pavlovich Never SKOVO MAGDAGACHINSKY Tra ns-Siberian Railroad DIRO Taldan Mokhe NSKY Zeya .! Ignashino Ivanovka Dzhalinda Ovsyanka ! Pioner Magdagachi Beketovo Yasny Tolbuzino Yubileiny Tokur Ekimchan Tygda Inzhan Oktyabrskiy Lukachek Zlatoustovsk Koboldo Ushumun Stoiba Ivanovskoe Chernyaevo Sivaki Ogodzha Ust-Tygda Selemdzhinsk Kuznetsovo Byssa Fevralsk KY Kukhterin-Lug NS Mukhino Tu Novorossiika Norsk M DHI Chagoyan Maisky SELE Novovoskresenovka SKY N OV ! Shimanovsk Uglovoe MAZ SHIMA ANOV Novogeorgievka Y Novokievsky Uval SK EN SK Mazanovo Y SVOBODN Chernigovka !. Svobodny Margaritovka e CHINA Kostyukovka inlin SERYSHEVSKY ! Seryshevo Belogorsk ROMNENSKY rMa Bolshaya Sazanka !. Shiroky Log - Amu BELOGORSKY Pridorozhnoe BLAGOVESHCHENSKY Romny Baikal Pozdeevka Berezovka Novotroitskoe IVANOVSKY Ekaterinoslavka Y Cheugda Ivanovka Talakan BRSKY SKY P! O KTYA INSK EI BLAGOVESHCHENSK Tambovka ZavitinskIT BUR ! Bakhirevo ZAV T A M B OVSKY Muravyovka Raichikhinsk ! ! VKONSTANTINO SKY Poyarkovo Progress ARKHARINSKY Konstantinovka Arkhara ! Gribovka M LIKHAI O VSKY ¯ Kundur Innokentevka Leninskoe km A m Trans -Siberianad Railro u 100 r R i v JAO Russian Far East e r By Newell and Zhou / Sources: Ministry of Natural Resources, 2002; ESRI, 2002. Newell, J. 2004. The Russian Far East: A Reference Guide for Conservation and Development. McKinleyville, CA: Daniel & Daniel. 466 pages CHAPTER 5 Amur Oblast Location Amur Oblast, in the upper and middle Amur River basin, is 8,000 km east of Moscow by rail (or 6,500 km by air). -

Newell, J. 2004. the Russian Far East

Industrial pollution in the Komsomolsky, Solnechny, and Amursky regions, and in the city of Khabarovsk and its Table 3.1 suburbs, is excessive. Atmospheric pollution has been increas- Protected areas in Khabarovsk Krai ing for decades, with large quantities of methyl mercaptan in Amursk, formaldehyde, sulfur dioxide, phenols, lead, and Type and name Size (ha) Raion Established benzopyrene in Khabarovsk and Komsomolsk-on-Amur, and Zapovedniks dust prevalent in Solnechny, Urgal, Chegdomyn, Komso- molsk-on-Amur, and Khabarovsk. Dzhugdzhursky 860,000 Ayano-Maysky 1990 Between 1990 and 1999, industries in Komsomolsky and Bureinsky 359,000 Verkhne-Bureinsky 1987 Amursky Raions were the worst polluters of the Amur River. Botchinsky 267,400 Sovetsko-Gavansky 1994 High concentrations of heavy metals, copper (38–49 mpc), Bolonsky 103,600 Amursky, Nanaisky 1997 KHABAROVSK zinc (22 mpc), and chloroprene (2 mpc) were found. Indus- trial and agricultural facilities that treat 40 percent or less of Komsomolsky 61,200 Komsomolsky 1963 their wastewater (some treat none) create a water defi cit for Bolshekhekhtsirsky 44,900 Khabarovsky 1963 people and industry, despite the seeming abundance of water. The problem is exacerbated because of: Federal Zakazniks Ⅲ Pollution and low water levels in smaller rivers, particular- Badzhalsky 275,000 Solnechny 1973 ly near industrial centers (e.g., Solnechny and the Silinka River, where heavy metal levels exceed 130 mpc). Oldzhikhansky 159,700 Poliny Osipenko 1969 Ⅲ A loss of soil fertility. Tumninsky 143,100 Vaninsky 1967 Ⅲ Fires and logging, which impair the forests. Udylsky 100,400 Ulchsky 1988 Ⅲ Intensive development and quarrying of mineral resourc- Khekhtsirsky 56,000 Khabarovsky 1959 es, primarily construction materials. -

On Distribution of Lampyris Noctiluca (Linnaeus, 1767) (Coleoptera, Lampyridae) in the Amur Region

Ecologica Montenegrina 16: 111-113 (2018) This journal is available online at: www.biotaxa.org/em On distribution of Lampyris noctiluca (Linnaeus, 1767) (Coleoptera, Lampyridae) in the Amur region VITALY G. BEZBORODOV1* & EVGENY S. KOSHKIN2 1Amur Branch of Botanical Garden-Institute of the Far Eastern Branch of the Russian Academy of Sciences, 2-d km of Ignatevskoye road, Blagoveshchensk, 675000, Russia, 2Institute of Water and Ecology Problems of the Far Eastern Branch of the Russian Academy of Sciences, Dikopoltsev St. 56, Khabarovsk, 680000, Russia; State Nature Reserve «Bureinskii», Zelenaya Str. 3, Chegdomyn, Khabarovskii Krai, 682030, Russia. Corresponding author: Vitaly G. Bezborodov; e-mail: [email protected] Received: 7 February 2018│ Accepted by V. Pešić: 28 February 2018 │ Published online: 2 March 2018. Lampyris noctiluca (Linnaeus, 1767) (Coleoptera, Lampyridae) covers an extensive transpalaearctic range (Medvedev & Ryvkin 1992; Geisthardt & Sato 2007; Kazantsev 2010, 2011) with unclear boundaries of distribution on the periphery. The eastern sector of the range has been studied the least. Until recently, from the Amur region (within the borders of the Amurskaya oblast' and Khabarovskii krai of Russia) three points of collection of L. noctiluca were known. However, this which does not give a detailed idea of the range of the species in this region (Kazantsev 2010) (Fig. 1). Our research provided material from the basins of the Amur and Uda rivers, which significantly clarifies the northern boundary of distribution in the eastern sector of the range of Lampyris noctiluca. Lampyris noctiluca is also firstly recorded for the Heilongjiang province in China and the Evreiskaya avtonomnaya oblast' in Russia. -

Subject of the Russian Federation)

How to use the Atlas The Atlas has two map sections The Main Section shows the location of Russia’s intact forest landscapes. The Thematic Section shows their tree species composition in two different ways. The legend is placed at the beginning of each set of maps. If you are looking for an area near a town or village Go to the Index on page 153 and find the alphabetical list of settlements by English name. The Cyrillic name is also given along with the map page number and coordinates (latitude and longitude) where it can be found. Capitals of regions and districts (raiony) are listed along with many other settlements, but only in the vicinity of intact forest landscapes. The reader should not expect to see a city like Moscow listed. Villages that are insufficiently known or very small are not listed and appear on the map only as nameless dots. If you are looking for an administrative region Go to the Index on page 185 and find the list of administrative regions. The numbers refer to the map on the inside back cover. Having found the region on this map, the reader will know which index map to use to search further. If you are looking for the big picture Go to the overview map on page 35. This map shows all of Russia’s Intact Forest Landscapes, along with the borders and Roman numerals of the five index maps. If you are looking for a certain part of Russia Find the appropriate index map. These show the borders of the detailed maps for different parts of the country. -

BR IFIC N° 2693 Index/Indice

BR IFIC N° 2693 Index/Indice International Frequency Information Circular (Terrestrial Services) ITU - Radiocommunication Bureau Circular Internacional de Información sobre Frecuencias (Servicios Terrenales) UIT - Oficina de Radiocomunicaciones Circulaire Internationale d'Information sur les Fréquences (Services de Terre) UIT - Bureau des Radiocommunications Part 1 / Partie 1 / Parte 1 Date/Fecha 03.05.2011 Description of Columns Description des colonnes Descripción de columnas No. Sequential number Numéro séquenciel Número sequencial BR Id. BR identification number Numéro d'identification du BR Número de identificación de la BR Adm Notifying Administration Administration notificatrice Administración notificante 1A [MHz] Assigned frequency [MHz] Fréquence assignée [MHz] Frecuencia asignada [MHz] Name of the location of Nom de l'emplacement de Nombre del emplazamiento de 4A/5A transmitting / receiving station la station d'émission / réception estación transmisora / receptora 4B/5B Geographical area Zone géographique Zona geográfica 4C/5C Geographical coordinates Coordonnées géographiques Coordenadas geográficas 6A Class of station Classe de station Clase de estación Purpose of the notification: Objet de la notification: Propósito de la notificación: Intent ADD-addition MOD-modify ADD-ajouter MOD-modifier ADD-añadir MOD-modificar SUP-suppress W/D-withdraw SUP-supprimer W/D-retirer SUP-suprimir W/D-retirar No. BR Id Adm 1A [MHz] 4A/5A 4B/5B 4C/5C 6A Part Intent 1 111030913 ARG 6500.0000 EL SOMBRERO ARG 58W45'55'' 27S42'07'' FX 1 ADD 2 111030907