Games Workshop Group Initiation of Coverage

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

THE HORUS HERESY AGE of DARKNESS: ZONE MORTALIS Rules for Deadly Close-Quarter Battles in the Labyrinths and Vaults of the Far Future

THE HORUS HERESY AGE OF DARKNESS: ZONE MORTALIS RULES FOR Deadly CLOSE-Quarter Battles IN THE LABYRINTHS AND Vaults OF THE FAR FUTURE The Horus Heresy Age of Darkness: fighting in a collapsing hive city under mass The Two Modes of Play Zone Mortalis allows players to recreate artillery bombardment or on a burning The Zone Mortalis rules have two modes some of the most savage arenas of combat star vessel in the middle of a space battle of play. The first and simplest mode is to conceivable, the battlefields the Codex Tactica ought to be. It’s the kind of game where incorporate a designated area of Zone Imperialis refers to as ‘Zone Mortalis’— all sorts of odd situations are going to be Mortalis terrain in a regular game of The the fatal ground. Such zones – be they thrown up from time to time and sudden Horus Heresy: Age of Darkness. This makes the contested decks of a void warship, reversals will occur, so have fun with it – a proportion of the gaming table operate tangled mine works, lightless underhives, hyper-competitive players or those seeking under the basic Zone Mortalis rules and can the prison-vaults of sundered fortress- complete predictability in their games will be represent the internal space of a command citadels, labyrinthine industrial sewer better served elsewhere. bunker, trench network, generatorium or systems and sacred catacombs – all have a hidden lab, or perhaps even the sanctum confluence of factors in common such as Citadel’s Zone Mortalis terrain is perfect of one of the Primarchs, filled with secrets close confinement, limited access for attack for representing the narrow confines, twists and deadly defences. -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

MARCH 1St 2018

March 1st We love you, Archivist! MARCH 1st 2018 Attention PDF authors and publishers: Da Archive runs on your tolerance. If you want your product removed from this list, just tell us and it will not be included. This is a compilation of pdf share threads since 2015 and the rpg generals threads. Some things are from even earlier, like Lotsastuff’s collection. Thanks Lotsastuff, your pdf was inspirational. And all the Awesome Pioneer Dudes who built the foundations. Many of their names are still in the Big Collections A THOUSAND THANK YOUS to the Anon Brigade, who do all the digging, loading, and posting. Especially those elite commandos, the Nametag Legionaires, who selflessly achieve the improbable. - - - - - - - – - - - - - - - - – - - - - - - - - - - - - - - – - - - - - – The New Big Dog on the Block is Da Curated Archive. It probably has what you are looking for, so you might want to look there first. - - - - - - - – - - - - - - - - – - - - - - - - - - - - - - - – - - - - - – Don't think of this as a library index, think of it as Portobello Road in London, filled with bookstores and little street market booths and you have to talk to each shopkeeper. It has been cleaned up some, labeled poorly, and shuffled about a little to perhaps be more useful. There are links to ~16,000 pdfs. Don't be intimidated, some are duplicates. Go get a coffee and browse. Some links are encoded without a hyperlink to restrict spiderbot activity. You will have to complete the link. Sorry for the inconvenience. Others are encoded but have a working hyperlink underneath. Some are Spoonerisms or even written backwards, Enjoy! ss, @SS or $$ is Send Spaace, m3g@ is Megaa, <d0t> is a period or dot as in dot com, etc. -

Table of Contents

TABLE OF CONTENTS DISCLAIMER AND CREDITS ........................................................................................................................................... 2 INTRODUCTION FOR NEW PLAYERS ............................................................................................................................ 3 INTRODUCTION FOR OLD PLAYERS .............................................................................................................................. 4 BATTLE RULES .............................................................................................................................................................. 5 MOVEMENT PHASE .................................................................................................................................................. 9 TERRAIN ................................................................................................................................................................. 13 SHOOTING .............................................................................................................................................................. 17 MELEE .................................................................................................................................................................... 25 MORALE AND PSYCHOLOGY .................................................................................................................................. 29 VEHICLES ............................................................................................................................................................... -

Games Workshop Group Plc

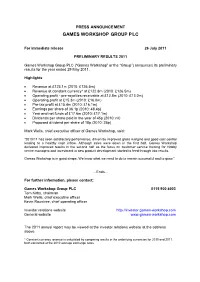

PRESS ANNOUNCEMENT GAMES WORKSHOP GROUP PLC For immediate release 26 July 2011 PRELIMINARY RESULTS 2011 Games Workshop Group PLC (“Games Workshop” or the “Group”) announces its preliminary results for the year ended 29 May 2011. Highlights • Revenue at £123.1m (2010: £126.5m) • Revenue at constant currency* at £122.8m (2010: £126.5m) • Operating profit - pre-royalties receivable at £12.8m (2010: £13.0m) • Operating profit at £15.3m (2010: £16.0m) • Pre-tax profit at £15.4m (2010: £16.1m) • Earnings per share of 36.1p (2010: 48.4p) • Year end net funds of £17.6m (2010: £17.1m) • Dividends per share paid in the year of 45p (2010: nil) • Proposed dividend per share of 18p (2010: 25p) Mark Wells, chief executive officer of Games Workshop, said: “2010/11 has seen satisfactory performance, driven by improved gross margins and good cost control leading to a healthy cash inflow. Although sales were down in the first half, Games Workshop delivered improved results in the second half as the focus on customer service training for Hobby centre managers and investment in new product development started to feed through into results. Games Workshop is in good shape. We know what we need to do to remain successful and to grow.” …Ends… For further information, please contact: Games Workshop Group PLC 0115 900 4003 Tom Kirby, chairman Mark Wells, chief executive officer Kevin Rountree, chief operating officer Investor relations website http://investor.games-workshop.com General website www.games-workshop.com The 2011 annual report may be viewed at the investor relations website at the address above. -

After Fantastika Programme

#afterfantastika Visit: www.fantastikajournal.com After Fantastika July 6/7th, Lancaster University, UK Schedule Friday 6th 8.45 – 9.30 Registration (Management School Lecture Theatre 11/12) 9.30 – 10.50 Panels 1A & 1B 11.00 – 12.20 Panels 2A, 2B & 2C 12.30 – 1.30 Lunch 1.30 – 2.45 Keynote – Caroline Edwards 3.00 – 4.20 Panels 3A & 3B 4.30 – 6.00 Panels 4A & 4B Saturday 7th 10.30 – 12.00 Panels 5A & 5B 12.00 – 1.00 Lunch 1.00 – 2.15 Keynote – Andrew Tate 2.30 – 3.45 Panels 6A, 6B & 6C 4.00 – 5.00 Roundtable 5.00 Closing Remarks Acknowledgements Thank you to everyone who has helped contribute to either the journal or conference since they began, we massively appreciate your continued support and enthusiasm. We would especially like to thank the Department of English and Creative Writing for their backing – in particular Andrew Tate, Brian Baker, Catherine Spooner and Sara Wasson for their assistance in promoting and supporting these events. A huge thank you to all of our volunteers, chairs, and helpers without which these conferences would not be able to run as smoothly as they always have. Lastly, the biggest thanks of all must go to Chuckie Palmer-Patel who, although sadly not attending the conference in-person, has undoubtedly been an integral part of bringing together such a vibrant and engaging community – while we are all very sad that she cannot be here physically, you can catch her digital presence in panel 6B – technology willing! Thank you Kerry Dodd and Chuckie Palmer-Patel Conference Organisers #afterfantastika Visit: www.fantastikajournal.com -

Warhammer 40K Roleplay Adventures Home : Adventures by A

Critical Hit - Warhammer 40,000 Roleplay Warhammer 40k Roleplay (W40kRP) takes characters into the realms of STORE the Warhammer 40,000 universe. You play a mutant hunter, pit fighter, mercenary, psyker - any of over 100 Warhammer 40k character types - skilled in the arts of battle and psionics, an adventurer in the perilous Warhammer 40k universe, opposed by Chaos, Orks, Tyranids, Warhammer 40k and a multitude of monstrous alien enemies. W40kRP provides an unmatched depth of background and atmosphere, with a fast, detailed Warhammer flexible game system, exciting combat and powerful psionics. Warhammer If you want to take part in the adventure then prepare yourself now. Forget the power of technology, science and common humanity. Forget the Warhammer Fantasy promise of progress and understanding, for there is no peace amongst the Roleplay stars, only an eternity of carnage and slaughter and the laughter of thirsting gods. But the universe is a big place and, whatever happens, you will not be missed. WFRP This website is completely unofficial and in no way endorsed by Games Workshop Limited. WHAT'S NEW BESTIARY Being a notification of updates to the web site, As permitted by the Administratum, a compendium Critical Hit, as and when said site is ameliorated. of the divers species that can be found in the 41st millennium including homo sapiens, aliens and RULES daemons and other warp abominations. The directives and regulations contained herein must be adhered to as laid down by the Adeptus ADVENTURES Terra. Divergence from said directives herein is For GMs only, a series of short encounters and permissible only through careful consideration of devious schemes for the amusement of player moral and social deviation. -

Consolidated Profit & Loss Account

PRESS ANNOUNCEMENT GAMES WORKSHOP GROUP PLC 14 January 2020 HALF-YEARLY REPORT Games Workshop Group PLC (‘Games Workshop’ or the ‘Group’) announces its half-yearly results for the six months to 1 December 2019. Highlights: Six months to Six months to 1 December 2019 2 December 2018 Revenue £148.4m £125.2m Revenue at constant currency* £145.6m £125.2m Operating profit pre-royalties receivable £48.5m £35.3m Royalties receivable £10.7m £5.5m Operating profit £59.2m £40.8m Operating profit at constant currency* £57.1m £40.8m Profit before taxation £58.6m £40.8m Cash generated from operations £60.4m £36.0m Basic earnings per share 145.9p 101.3p Dividend per share declared in the period 100p 65p Kevin Rountree, CEO of Games Workshop, said: “Our business and the Warhammer Hobby continue to be in great shape. We are pleased to once again report record sales and profit levels in the period. The global team have worked their socks off to deliver these great results. My thanks go out to them all. Sales for the month of December are in line with our expectations. We are also announcing that the Board has today declared a dividend of 45 pence per share, in line with the Company’s policy of distributing truly surplus cash.” …Ends… For further information, please contact: Games Workshop Group PLC 0115 900 4003 Kevin Rountree, CEO Rachel Tongue, Group Finance Director Investor relations website investor.games-workshop.com General website www.games-workshop.com *Constant currency revenue and operating profit are calculated by comparing results in the underlying currencies for 2018 and 2019, both converted at the average exchange rates for the six months ended 2 December 2018. -

Financial Highlights

FINANCIAL HIGHLIGHTS 2007 2006 Revenue £111.5m £115.2m Pre-exceptional operating profit £1.9m £4.2m Exceptional items - cost reduction programme £(4.0)m - Operating (loss)/profit £(2.1)m £4.2m Pre-tax (loss)/profit £(2.9)m £3.7m Year end net borrowings £10.2m £2.2m (Loss)/earnings per share (11.2)p 6.5p Dividend per share 4.95p 18.975p Contents 1 Financial highlights 2 Chairman's preamble 3 Business review 9 Financial review 11 Directors' report 16 Corporate governance 20 Remuneration report 23 Statement of directors' responsibilities 23 Company’s directors and advisers 24 Independent auditors' report 25 Income statement 25 Statements of recognised income and expense 26 Balance sheets 27 Cash flow statements 28 Notes to the financial statements 54 Five year summary and financial calendar 55 Notice of meeting 57 Appendix - Chairman's preambles from previous annual reports Games Workshop Group PLC 1 CHAIRMAN’S PREAMBLE To paraphrase Margaret Thatcher: 'The wisdom of hindsight, so useful to analysts and some shareholders, is sadly denied to practising businessmen.' Or least it is when we take our decisions. Like everyone else I wonder about the decisions I took and the things I said over the last few months and years. One can lose a great deal of sleep that way, but it is, of course, a futile exercise unless one is an historian. The real question is: did I do what I did and say what I said in good faith, with serious intent and with appropriate cognisance of the needs of all our stakeholders? Now, this is a good question and the answer for every one alive, never mind the few of us leading public companies, had better be yes. -

White Dwarf Editor

ISSUE 29 16th August 2014 Editor: Jes Bickham [email protected] Assistant Editor: Matt Keefe [email protected] Senior Staff Writer: Adam Troke [email protected] Staff Writer: Daniel Harden [email protected] Production Lead: Rebecca Ferguson [email protected] Digital Editor: Melissa Roberts [email protected] Lead Designer: Matthew Hutson [email protected] Designer: Kristian Shield [email protected] Designer: Ben Humber [email protected] Photo Editor: Glenn More [email protected] Photographer: Erik Niemz [email protected] Photographer: Martyn Lyon [email protected] Distribution Lead: Andy Keddie [email protected] Publisher: Paul Lyons [email protected] With the advent of the new Warhammer 40,000, the threat of Chaos Daemons is greater than ever. The Dark Powers press against the walls of reality without cease, and who will stand against their eternal predations? There are none so strong in this fight as the Grey Knights, the Imperium’s first and final line of defence against the terrors of the Warp. They stand ever-vigilant and ready to exterminate all the horrors that tempt humanity, and they return to tabletops everywhere this week with a brand-new Codex and the psychic might to smite all creatures spawned from the immaterium. Adam tests their mettle against his own Daemonic force in this issue’s Battle Report, with Andy Keddie fighting for the Emperor. It’s an epic affair and no mistake. The concluding chapter of Sanctus Reach also appears this week, in Hour of the Wolf. -

2007 Necromunda Scenario Competition Results

2007 NECROMUNDA SCENARIO COMPETITION RESULTS Thank you to all of you out there that submitted scenarios. After reviewing all the submitted scenarios I found that a lot of the entries were well thought out and definitely worth playing. We had five categories, so I split the submittals into their respective category and judged them all. So, without further ado, here are the Specialist Games 2007 Necromunda Scenario Competition winning scenarios… BEST ALL AROUND SCENARIO BEST LITTLE SCENARIO ‘To Catch a Curator’ by Ross Firth ‘The Escape Artist’ by Dave Parsons This one was a hard one. This winner was This scenario won this category because in short determined on the fact that the author read order it basically takes a skill that everyone hates, something in a Necromunda book and made an Escape Artist, and makes it a challenge. This awesome scenario out of it. This was the last scenario just adds that little extra flair needed scenario that I reviewed and re-formatted as well, of everyone once in a while when the monotony of all the luck, eh? I hope you will agree it is not over gang fight after gang fight after gang fight is or under powered and can fit in nicely with your selected. campaigns. ARBITRATOR GENERAL’S FAVORITE BEST TERRAIN SCENARIO ‘Dome Rush’ by Anthony Case ‘Good Well Hunting’ by Scott L Spears Anytime you have more than two players there This scenario won this category because it utilized a always seems to be someone laying out waiting, but lot of what Necromunda is and then went the further with this scenario the more players the merrier, and step. -

FTSE Russell Publications

2 FTSE Russell Publications 19 August 2021 FTSE 250 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Infrastructure 0.43 UNITED Bytes Technology Group 0.23 UNITED Edinburgh Investment Trust 0.25 UNITED KINGDOM KINGDOM KINGDOM 4imprint Group 0.18 UNITED C&C Group 0.23 UNITED Edinburgh Worldwide Inv Tst 0.35 UNITED KINGDOM KINGDOM KINGDOM 888 Holdings 0.25 UNITED Cairn Energy 0.17 UNITED Electrocomponents 1.18 UNITED KINGDOM KINGDOM KINGDOM Aberforth Smaller Companies Tst 0.33 UNITED Caledonia Investments 0.25 UNITED Elementis 0.21 UNITED KINGDOM KINGDOM KINGDOM Aggreko 0.51 UNITED Capita 0.15 UNITED Energean 0.21 UNITED KINGDOM KINGDOM KINGDOM Airtel Africa 0.19 UNITED Capital & Counties Properties 0.29 UNITED Essentra 0.23 UNITED KINGDOM KINGDOM KINGDOM AJ Bell 0.31 UNITED Carnival 0.54 UNITED Euromoney Institutional Investor 0.26 UNITED KINGDOM KINGDOM KINGDOM Alliance Trust 0.77 UNITED Centamin 0.27 UNITED European Opportunities Trust 0.19 UNITED KINGDOM KINGDOM KINGDOM Allianz Technology Trust 0.31 UNITED Centrica 0.74 UNITED F&C Investment Trust 1.1 UNITED KINGDOM KINGDOM KINGDOM AO World 0.18 UNITED Chemring Group 0.2 UNITED FDM Group Holdings 0.21 UNITED KINGDOM KINGDOM KINGDOM Apax Global Alpha 0.17 UNITED Chrysalis Investments 0.33 UNITED Ferrexpo 0.3 UNITED KINGDOM KINGDOM KINGDOM Ascential 0.4 UNITED Cineworld Group 0.19 UNITED Fidelity China Special Situations 0.35 UNITED KINGDOM KINGDOM KINGDOM Ashmore