Crepe Paper Products from China

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Introduction to Process and Properties of Tissue Paper

Introduction to process and properties of tissue paper enrico galli, 2017 Enrico Galli self-presentation • I was born in Viareggio (Lucca county or “the so called tissue valley”) Tuscany - Italy • Graduated in Chemical Engineering at University of Pisa in 1979 • Process and project engineer and then technical manager in oil industry (oil refineries and spent lube oil re-refining) in GULF, API, AGIP in Italy • Technical manager in chemical and consumer products company (soap, detergents, derivate from fatty acids, sanitary gloves, tissue paper) in Italy. • Since 1984 in paper and tissue business: • Italy: Tissue (PM, PBD, CON), Newspaper (PM), Cardboard paper (PM, MM) • Estónia: Tissue (PM, CEO) • France: Tissue (PM) • Hungary: Tissue (CON) • Nigéria: Tissue (CON) • Romania: Tissue (PM, PBM, MM, CON), Writing paper (PBM) • Rússia: Tissue (PM) • Spain: Tissue (PBM) • UK: Tissue (PBM) • Cooperation with following main European Tissue Companies: Annunziata (now WEPA – Italy), GP (now Lucart – Italy), Horizon Tissue (Estonia), Imbalpaper (now Sofidel – Italy), Kartogroup (now WEPA – Italy, France, Spain), Montebianco (Romania), Pehartec (Romania), Perini (now Sofidel – Romania, UK), Siktyvkar Tissue Group (Russia), Vaida Papir (Hungary)… and now proudly NAVIGATOR in Portugal! • I have been supporting Sales and Marketing Teams for strategic planning as well as for products development in Baltic Countries, BENELUX, Denmark, Finland, France, Germany, Hungary, Ireland, Italy, Norway, Poland, Romania, Russia, Spain, Sweden, UK. • Since 1998 I have -

Pdf51da2bb9237.Pdf FAO, F

PEER-REVIEWED REVIEW ARTICLE bioresources.com Understanding the Effect of Machine Technology and Cellulosic Fibers on Tissue Properties – A Review Tiago de Assis,a Lee W. Reisinger,b Lokendra Pal,a Joel Pawlak,a Hasan Jameel,a and Ronalds W. Gonzalez a,* Hygiene tissue paper properties are a function of fiber type, chemical additives, and machine technology. This review presents a comprehensive and systematic discussion about the effects of the type of fiber and machine technology on tissue properties. Advanced technologies, such as through-air drying, produce tissue with high bulk, softness, and absorbency. Conventional technologies, where wet pressing is used to partially dewater the paper web, produces tissue with higher density, lower absorbency, and softness. Different fiber types coming from various pulping and recycling processes are used for tissue manufacturing. Softwoods are mainly used as a source of reinforcement, while hardwoods provide softness and a velvet type surface feel. Non- wood biomass may have properties similar to hardwoods and/or softwoods, depending on the species. Mechanical pulps having stiffer fibers result in bulkier papers. Chemical pulps have flexible fibers resulting in better bonding ability and softness. Virgin fibers are more flexible and produce stronger and softer tissue. Recycled fibers are stiffer with lower bonding ability, yielding products that are weaker and less soft. Mild mechanical refining is used to improve limitations found in recycled fibers and to develop properties in virgin fibers. -

Making Paper from Trees

Making Paper from Trees Forest Service U.S. Department of Agriculture FS-2 MAKING PAPER FROM TREES Paper has been a key factor in the progress of civilization, especially during the past 100 years. Paper is indispensable in our daily life for many purposes. It conveys a fantastic variety and volume of messages and information of all kinds via its use in printing and writing-personal and business letters, newspapers, pamphlets, posters, magazines, mail order catalogs, telephone directories, comic books, school books, novels, etc. It is difficult to imagine the modern world without paper. Paper is used to wrap packages. It is also used to make containers for shipping goods ranging from food and drugs to clothing and machinery. We use it as wrappers or containers for milk, ice cream, bread, butter, meat, fruits, cereals, vegetables, potato chips, and candy; to carry our food and department store purchases home in; for paper towels, cellophane, paper handkerchiefs and sanitary tissues; for our notebooks, coloring books, blotting paper, memo pads, holiday greeting and other “special occasion’’ cards, playing cards, library index cards; for the toy hats, crepe paper decorations, paper napkins, paper cups, plates, spoons, and forks for our parties. Paper is used in building our homes and schools-in the form of roofing paper, and as paperboard- heavy, compressed product made from wood pulp-which is used for walls and partitions, and in such products as furniture. Paper is also used in linerboard, “cardboard,” and similar containers. Wood pulp is the principal fibrous raw material from which paper is made, and over half of the wood cut in this country winds up in some form of paper products. -

4-10 Matting and Framing.Pdf

PRESERVATION LEAFLET CONSERVATION PROCEDURES 4.10 Matting and Framing for Works on Paper and Photographs NEDCC Staff NEDCC Andover, MA The importance of proper matting, mounting and framing Do not use any type of foam board such as Fom-cor®, is often overlooked as a key part of collections care and “archival” paper faced foam boards, Gator board, preventative conservation. Poor quality materials and expanded PVC boards such as Sintra® or Komatex®, any improper framing techniques are a common source of lignin containing paper-based mat boards, kraft (brown) damage to artwork and cultural heritage materials that paper, non-archival or self-adhesive tapes (i.e. document are in otherwise good condition. Staying informed about repair tapes), or ATG (adhesive transfer gum), all of which proper framing practices and choosing conservation-grade are used in the majority of frame shops. mounting, matting and framing can prevent many problems that in the future will be much more difficult to MATTING solve or even completely irreversible. As Benjamin Franklin said, “An ounce of prevention is worth a pound of The window mat is the standard mount for works on cure.” paper. The ideal window mat will be aesthetically pleasing while safely protecting the piece from exterior damage. Mats are an excellent storage method for works on paper CHOICE OF A FRAMER and can minimize the damage caused from handling in When choosing a framer it is important to find someone collections that are used for exhibition and study. Some well-informed about best conservation framing practices institutions simplify their framing and storage operations and experienced in implementing them. -

Pre-Feasibility Study for a Pulpwood Using Facility Siting in the State Of

Wisconsin Wood Marketing Team July 31, 2020 Pre-Feasibility Study for a Pulpwood-Using Facility Siting in the State of Wisconsin Project Director: Donald Peterson Funded by: State of Wisconsin U.S. Forest Service Wood Innovations Table of Contents Project Team ................................................................................................................................................. 5 Acknowledgements ....................................................................................................................................... 7 Foreword ....................................................................................................................................................... 8 Executive Summary ..................................................................................................................................... 10 Chapter 1: Introduction and Overview ....................................................................................................... 12 Scope ....................................................................................................................................................... 13 Assessment Process ................................................................................................................................ 14 Identify potential pulp and wood composite panel technologies ...................................................... 15 Define pulpwood availability ............................................................................................................. -

SECTION X Pulp of Wood Or of Other Fibrous Cellulosic Material; Recovered (Waste and Scrap) Paper Or Paperboard; Paper and Paperboard and Articles Thereof

Section X Chapter 47/1 SECTION X Pulp of wood or of other fibrous cellulosic material; recovered (waste and scrap) paper or paperboard; paper and paperboard and articles thereof Chapter 47 Pulp of wood or of other fibrous cellulosic material; recovered (waste and scrap) paper or paperboard NOTE— 1. For the purposes of heading 47.02, the expression “chemical wood pulp, dissolving grades” means chemical wood pulp having by weight an insoluble fraction of 92% or more for soda or sulphate wood pulp or of 88% or more for sulphite wood pulp after one hour in a caustic soda solution containing 18% sodium hydroxide (NaOH) at 20 °C, and for sulphite wood pulp an ash content that does not exceed 0.15% by weight. * * * Section X Chapter 47/2 Section X Chapter 47—continued Chapter 47/3 Pulp of wood or of other fibrous cellulosic material; recovered (waste and scrap) paper or paperboard—continued Statistical Key Rates of Duty Number Goods Normal *Preferential Code Unit Tariff Tariff 47.01 4701.00.00 Mechanical wood pulp Free Free 01D tne . Softwood 05G tne . Hardwood 47.02 4702.00.00 Chemical wood pulp, dissolving grades Free Free 01B tne . Softwood 05E tne . Hardwood 47.03 Chemical wood pulp, soda or sulphate, other than dissolving grades: – Unbleached: 4703.11.00 00L tne – – Coniferous Free Free 4703.19.00 – – Non-coniferous Free Free 01E tne . Softwood 05H tne . Hardwood – Semi-bleached or bleached: 4703.21.00 – – Coniferous Free Free 01B tne . Semi-bleached 09H tne . Bleached 4703.29.00 – – Non-coniferous Free Free 01J tne . -

Changes in Print Paper During the 19Th Century

Purdue University Purdue e-Pubs Charleston Library Conference Changes in Print Paper During the 19th Century AJ Valente Paper Antiquities, [email protected] Follow this and additional works at: https://docs.lib.purdue.edu/charleston An indexed, print copy of the Proceedings is also available for purchase at: http://www.thepress.purdue.edu/series/charleston. You may also be interested in the new series, Charleston Insights in Library, Archival, and Information Sciences. Find out more at: http://www.thepress.purdue.edu/series/charleston-insights-library-archival- and-information-sciences. AJ Valente, "Changes in Print Paper During the 19th Century" (2010). Proceedings of the Charleston Library Conference. http://dx.doi.org/10.5703/1288284314836 This document has been made available through Purdue e-Pubs, a service of the Purdue University Libraries. Please contact [email protected] for additional information. CHANGES IN PRINT PAPER DURING THE 19TH CENTURY AJ Valente, ([email protected]), President, Paper Antiquities When the first paper mill in America, the Rittenhouse Mill, was built, Western European nations and city-states had been making paper from linen rags for nearly five hundred years. In a poem written about the Rittenhouse Mill in 1696 by John Holme it is said, “Kind friend, when they old shift is rent, Let it to the paper mill be sent.” Today we look back and can’t remember a time when paper wasn’t made from wood-pulp. Seems that somewhere along the way everything changed, and in that respect the 19th Century holds a unique place in history. The basic kinds of paper made during the 1800s were rag, straw, manila, and wood pulp. -

Paper Towel Strength and Absorbency

Paper Towel Strength and Absorbency Summary Think about the last time you spilled a drink. How did you clean it up? Most likely you grabbed the nearest roll of paper towels. Why didn’t you use a roll of toilet paper or why didn’t you grab a wad of notebook or computer paper? What is it about a paper towel that makes it so useful to clean up spilled liquids? It has to do with how the paper towels are made. Paper towels are made from the same types of plant fibers that other types of paper are made from. The difference between paper towels and other types of paper comes when the paper fibers are mixed with a special type of resin to make them strong when they are wet. That’s why paper towels don’t tear as easily as notebook paper or tissue paper when they are wet. Once the sheets are made they have shapes pressed into them to make them look quilted. These shapes form air pockets to attract water. That is why paper towels are so absorbent. Different brands of paper towels have different methods for manufacturing their paper towels. In this activity you will get to test different brands of paper towels for their strength and absorbency. In this activity we will: 1. Observe what qualities about paper towels give them the best strength and ability to absorb water. 2. Test four different brands of paper towels to see which is the strongest and most absorbent. Materials - four or more different brands of paper towels - a jar of pennies - bowl of water - teaspoon - eye dropper or turkey baster - two assistants - record sheet and pencil (see below) Preparation 1. -

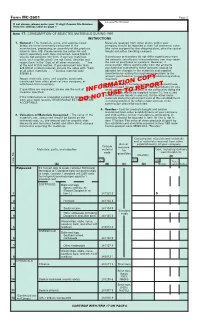

Form MC-2601 Page 5 Census File Number If Not Shown, Please Enter Your 11-Digit Census File Number from the Address Label on Page 1

Form MC-2601 Page 5 Census File Number If not shown, please enter your 11-digit Census File Number from the address label on page 1 Item 17. CONSUMPTION OF SELECTED MATERIALS DURING 1997 INSTRUCTIONS 1. General – The materials, parts, and supplies listed Materials received from other plants within your below are those commonly consumed in the company should be reported at their full economic value manufacture, processing, or assembly of the products (the value assigned by the shipping plant, plus the cost of listed in item 18B. Please review the entire list and freight and other handling charges). report separately each item consumed. Leave blank if you do not consume the item. If you use materials, If purchases or transfers do not differ significantly from parts, and supplies which are not listed, describe and the amounts actually put into production, you may report report them in the "Cost of all other materials . " line the cost of purchases or transfers. However, if at the end of this section. If you consumed less than consumption differs significantly from the amounts $25,000 of a listed material, include the value with "Cost purchased or transferred, these amounts should be of all other materials . ," Census material code adjusted for changes in the materials and supplies 970099 8. inventories by adding the beginning inventory to the amount purchased or transferred and subtracting ending Report materials, parts, and supplies purchased, inventory. transferred from other plants of your company, or withdrawn from inventory. 3. Contract Work – Include as materials consumed those you purchased for use by others making products for you If quantities are requested, please use the unit of under contract. -

Corrugated Cardboard Magazines

Most of us use a paper product every day. That's because paper products make up about 71 million tons (or 29 percent) of the municipal waste stream, according to the Environmental Protection Agency (EPA). The good news is that more and more Americans are recycling paper. In fact, upwards of 63 percent (45 million tons) is recycled annually. When you break that number down by population, roughly 334 pounds of paper is recycled for every person in the United States. Corrugated Cardboard Currently, about 70 percent of cardboard-boxes shipped commercially are recovered for recycling. Many of the boxes are themselves made of recycled materials or lumber industry byproducts like sawdust and wood chips. When recycled, cardboard is used to make chipboard like cereal boxes, paperboard, paper towels, tissues and printing or writing paper. It's also made into more corrugated cardboard. How It's Recycled: 1. The cardboard is re-pulped and the fibers are separated and bleached. This is a chemical process involving hydrogen peroxide, sodium silicate, and sodium hydroxide. 2. The fibers are screened and cleaned to eliminate contaminants. 3. The fibers are washed to remove leftover ink. 4. Fibers are pressed and rolled into paper. 5. he rolls of paper are then converted into boxes or made into new products. Magazines Magazines are made from paper that's been buffed and coated to achieve a glossy appearance. Next, the paper is covered with a white clay that makes color photographs look more brilliant. The shiny appearance does not contaminate the paper at all. About 45 percent of sub-content-3 are being recycled today. -

Portland Daily Press: January 21, 1897

PORTLAND DAILY PRESS. ■ THREE CENTS. THURSDAY MORNING. JANUARY 21 JUNE 28. 1862—VOL. S4. PORTLAND. MAINE. FSTiUt^HFI) "' 1897._PRICE — ——— .. I i /-v «■ nnmiAir anu ir csxen siok, siiupiy uy •» room. Mr. Cotter nsked him if certain earth, which he tegarded as erroneous ami brother a ivmsmi iiLLuiui!. WOTIOS3. spoke in the jury room. CENTURY sign be is recognized by any (SPECIAL iu particular of the idea that the income experiments were tried THREE FOURTHS BRIM’S FIGHT FOR LIFE. Mr. Hoar strenuously ohjeoted on and will be cared lor. Objections of the experiment station oould be Mason similar reasons as before apd was heard in fact counted as part of the inooine of the are sometimes raised in these days, at length on that citing owtain college, which he »aid was uct the case. point, have been made to NEW GOODS decisions in of bis objections. In the past, objections that are It will be late lu the session before the support la the or ia small lots, Lawyer French to the objections the order because of its eeorecy. piece State College tight Is on In earnest. The replied Before or of Mr. Hoar. He argued th3t the testi- The first is that there are un- The Yost-Tuckcr Case liable to shrink 6pot by damp, trustees will not Introduce any measure objection cn Petition a Blew mony wished to introduce *d- Anniversary Harmony Railroad Bills Pile In Commit- until after the oommittee has visited the For they ijos Seventy-Fifth those who bear tbo aegs. can be Up Bearing missable that it was im- worthy members, oollege and the oommittee will and Btated of probably possible for the to have tried ex- name of Masons that are not worthy Congress. -

Wood Pulp and Waste Paper

Wood Pulp and Waste Paper USITC Publication 3490 February 2002 OFFICE OF INDUSTRIES U.S. International Trade Commission Washington, DC 20436 UNITED STATES INTERNATIONAL TRADE COMMISSION COMMISSIONERS Stephen Koplan, Chairman Deanna Tanner Okun, Vice Chairman Lynn M. Bragg Marcia E. Miller Jennifer A. Hillman Director of Operations Robert A. Rogowsky Director of Industries Vern Simpson This report was prepared principally by Fred Forstall Animal and Forest Products Branch Agriculture and Forest Products Division Address all communications to Secretary to the Commission United States International Trade Commission Washington, DC 20436 www.usitc.gov ITC READER SATISFACTION SURVEY Industry and Trade Summary: Wood Pulp and Waste Paper The U.S. International Trade Commission (ITC) is interested in your voluntary comments (burden < 15 minutes) to help us assess the value and quality of our reports, and to assist us in improving future products. Please return survey by fax (202-205-2384) or by mail to the ITC. Your name and title (please print; responses below not for attribution): Please specify information in this report most useful to you/your organization: Was any information missing that you consider important? Yes (specify below) No If yes, please identify missing information and why it would be important or helpful to you: Please assess the value of this ITC report (answer below by circling all that apply): SA—Strongly Agree; A—Agree; N—No Opinion/Not Applicable; D—Disagree; SD—Strongly Disagree " Report presents new facts, information,