Development of Life Cycle Cost Model of Passenger Car By

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Automotive-200103-1Q20 Strategy (Kenanga)

Sector Update 03 January 2020 Automotive NEUTRAL National Marques Overtaking on the Fast Lane ↔ By Wan Mustaqim Bin Wan Ab Aziz l [email protected] We maintain our NEUTRAL rating on the AUTOMOTIVE sector. The MIER consumer sentiment index scored 84.0 points (-9.0ppt QoQ, -23.5ppt YoY) in 3QCY19 which is below the optimistic threshold (>100pts) due to normalisation of consumer confidence post-tax holiday and weak macroeconomic outlook. Reflecting this, we are seeing car sales trending in favour of value-for-money national marques, as evident from their 11MCY19 TIV market share of 57%. Non-national marques on the other hand, are focusing on higher-margin lower-volume models (catering to higher purchasing power consumers). Notable developments in Automotive industry in 2019/2020 include: (i) national marques surpassing non-national marques in terms of market share, (ii) Proton has surpassed Honda as no.2 trailing behind Perodua, (iii) increasing number of new model launches, (iv) better incentives under National Automotive Policy 2020 (tentatively on 1QCY20), and (v) another OPR rate cut by 25bps (to 2.75%) in 2020, which should have minimal positive impact on vehicles loans. No changes to our 2019 TIV target of 600,000 units (+0.2%), and we introduce 2020 TIV target of 612,000 units (+2%) matching MAA’s target factoring the extra boost from national marques (Proton and Perodua). Our sector top-pick is BAUTO (OP; TP: RM2.65) for its defensible niche SUV market and attractive, steady dividend yield of 7.3%. National marques affirming leading market position . As of 11MCY19, the national marques (57%) continued to stay above non-national marques (43%) in terms of market share, marking a year not seen since 2013, owing to the outstanding sales from Perodua, especially after the introduction of its all-new Perodua Myvi and supported by the all-new Perodua Aruz (27,389 units delivered). -

Dealership Staff Can Help Reduce the Number of Problems Owners Experience with Their New Vehicle

Dealership Staff Can Help Reduce The Number of Problems Owners Experience With Their New Vehicle Honda Receives Two Model-Level Awards For Initial Quality, Perodua and Toyota Each Get One KUALA LUMPUR: 27 November 2015 — The salesperson plays a critical role in reducing the number of problems owners experience with their new vehicle, according to the J.D. Power Asia Pacific 2015 Malaysia Initial Quality StudySM (IQS) released today. Automakers continue to add features, specifically entertainment and connectivity technology, to their vehicle. By explaining at the time of delivery all of the features of the vehicle and how they work, the salesperson can make sure the owner is comfortable with the technology thus significantly reducing the number of problems the owner experienced with their vehicle. The study finds that when the salesperson provides a comprehensive explanation of the vehicle and its features, owners report an average of 79 problems per 100 vehicles (PP100). In contrast, owners who indicate their salesperson provided no explanation, or only a partial explanation, report an average of 163 PP100. “With all of the new content automakers are putting in their vehicles, it is absolutely critical for salespeople to provide comprehensive explanation of vehicle, including a test drive, to make sure the customer fully understands how to operate all of the technology and its benefits,” said Rajaswaran Tharmalingam, country head, Malaysia, J.D. Power. “The technology may work exactly as it’s designed, but if the customer doesn’t know how to use it or had difficulties using it, they deem it a problem. The salesperson can greatly reduce those problems simply spending time with the customer during the delivery process going through the vehicle and its accessories.” Tharmalingam noted that given the importance of the test drive, only 59 percent of customers in Malaysia took one during their shopping process. -

Approval Car Price Issued As of 31St January 2020

APPROVAL CAR PRICE ISSUED AS OF 31ST JANUARY 2020 DATE SHOWROOM PASSENGER MOTOR VEHICLES BRAND PASSENGER MOTOR VEHICLES MODEL /TYPE DATE ISSUED PRICE (SRP) EFFECTIVE EXPIRY ALFA ROMEO ALFA ROMEO GIULIA 620 QV V6 (G.H.K MOTORS SDN BHD) ALFA ROMEO GIULIA 620 QV V6 2.9L AUTO SEDAN PETROL 27-May-19 21-Apr-19 20-Apr-20 $139,973.00 ALFA ROMEO GIULIA 620 GME ALFA ROMEO GIULIA 620 GME 2.0L AUTO SEDAN PETROL 27-May-19 21-Apr-19 20-Apr-20 $63,353.00 ALFA ROMEO STELVIO ALFA ROMEO STELVIO 2.0L 8-SPEED AUTOMATIC TRANSMISSION AWD SUV 7-Jan-20 1-Dec-19 30-Nov-20 $75,262.00 PETROL (SOLID PAINT) ALFA ROMEO STELVIO 2.0L 8-SPEED AUTOMATIC TRANSMISSION AWD SUV 7-Jan-20 1-Dec-19 30-Nov-20 $77,538.00 PETROL (SPECIAL PAINT) ALFA ROMEO VELOCE 620 2.0L GME 2000 ALFA ROMEO GIULIA VELOCE 620 2.0L AUTO GME 2000 SEDAN PETROL 27-Jul-19 3-Jun-19 2-Jun-20 $69,666.00 AUDI AUDI A3 TFSI S-TRONIC (T. C. Y. MOTORS SDN BHD) AUDI A3 1.2L TFSI S-TRONIC AUTO SEDAN PETROL 26-Dec-19 31-Dec-19 30-Dec-20 $43,631.00 AUDI A3 TFSI S-TRONIC SPORTBACK AUDI A3 1.2L TFSI S-TRONIC AUTO SPORTBACK PETROL 7-Sep-19 11-Sep-19 10-Sep-20 $46,803.00 AUDI A4 TFSI S-TRONIC BLACK EDITION AUDI A4 2.0L TFSI S-TRONIC AUTO SEDAN PETROL - BLACK EDITION 19-Jun-19 3-Jun-19 2-Jun-20 $55,068.00 AUDI A4 TFSI QUATTRO S-TRONIC AUDI A4 2.0L TFSI QUATTRO S-TRONIC AUTO AWD SEDAN PETROL 19-Jun-19 3-Jun-19 2-Jun-20 $67,560.00 AUDI A4 TFSI ULTRA QUATTRO S-TRONIC AUDI A4 2.0L TFSI ULTRA QUATTRO AWD S-TRONIC AUTO SEDAN PETROL 25-Feb-19 11-Feb-19 10-Feb-20 $68,676.00 AUDI A5 TFSI QUATTRO S-TRONIC COUPE AUDI A5 2.0L TFSI -

Toyota Gear Shift/Select Cable

INDEX PAGES TOYOTA 1 ~ 53 NISSAN 54 ~ 91 MAZDA 92 ~ 104 HINO 105 ~ 115 ISUZU 116 ~ 137 MITSUBISHI 138 ~ 160 PROTON 161 ~ 164 DAIHATSU 165 ~ 172 SUZUKI 173 ~ 180 HONDA 181 ~ 193 SUBARU 194 ~ 195 HYUNDAI 196 ~ 199 DAEWOO & KIA & SSANGYONG 200 ~ 203 AMERICAN & EUROPEAN VEHICLES 204 ~ 212 MOTORCYCLES 213 ~ 215 KUBOTA,TRACTOR & FORK LIFT 216 ~ 218 OTHERS 219 ~ 221 CABLES FOR SOUTH AFRICA MAKET 222 ~ 229 ADDITIONAL ITEMS 230 TOYOTA OEM NUMBER ICI NUMBER MODEL TOYOTA ACCELERATOR CABLE 35520-12050 CATY123 AE 8# 35520-12072 CATY145 KE70 ATM 81.08- 35520-12110 CATY124 TE 7# 35520-12200 CATY158 35520-12201 CATY158 35520-12240 CATY126 HILUX LN85/106 88-92, AE101, AE92, AT171 35520-12300 CATY148 AE100,101,110 4FC 91.08- 35520-12310 CATY151 COROLLA AE101 4A-FE 91.06-93.05 35520-12370 CATY122 35520-12390 CATY150 COROLLA AE101 4A-FE 93.05- , AE102,111 1991-1995 RHD 35520-12391 CATY150 COROLLA AE101 4A-FE 93.05- , AE102,111 1991-1995 RHD 35520-16090 CATY147 EE101,92.05-95.05,EP82 3F .92.01- 35520-20070 CATY141 CRESSIDA 35520-28011 CATY133 35520-30030 CATY146 MS112,122,132,133 8MX73 84.08- 35520-33010 CATY217 CAMRY SXV10# 2.2L 5S-FE DOHC 16V MPFI 4CYL 4SP AUTO, VCV10, MCV10 ATM 1992-2001 35520-33050 CATY234 AVALON XL,XLS (MCX10) 1996-1999/CAMRY CE,LE,XLE (MCV20) 1997-2001/SOLARA MCV20 1999-2003/LEXUS ES300 (MCV20) 1996-2001 47616-26040 CATY192 62-CATY002 CATY002 HILUX LN50 62-CATY004 CATY004 HILUX 62-CATY026 CATY026 HILUX HIACE Y SERIES LN80/85/106/130 LHD 92-94 3L 78120-35013 CATY156 78120-90506 CATY159 DYNA RB10 '77-79 78150-06020 CATY220 TOYOTA CAMRY -

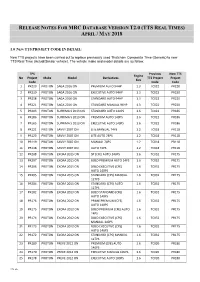

Release Notes for Mrc Database Version T2.0 (Tts Real Times) April / May 2018

RELEASE NOTES FOR MRC DATABASE VERSION T2.0 (TTS REAL TIMES) APRIL / MAY 2018 1.0 NEW TTS PROJECT CODE IN DETAIL: New TTS projects have been carried out to replace previously used Thatcham Composite Time (Generic) to new TTS Real Time (Actual/Similar vehicle). The vehicle make and model details are as follow: TPS Previous New TTS Engine No Project Make Model Derivatives TTS Project Project Size Code Code Code 1 PR220 PROTON SAGA 2016 ON PREMIUM AUTO 94HP 1.3 TC022 PR220 2 PR219 PROTON SAGA 2016 ON EXECUTIVE AUTO 94HP 1.3 TC022 PR220 3 PR218 PROTON SAGA 2016 ON STANDARD AUTO 94HP 1.3 TC022 PR220 4 PR221 PROTON SAGA 2016 ON STANDARD MANUAL 94HP 1.3 TC022 PR220 5 PR203 PROTON SUPRIMA S 2013 ON STANDARD AUTO 140PS 1.6 TC022 PR186 6 PR186 PROTON SUPRIMA S 2013 ON PREMIUM AUTO 140PS 1.6 TC022 PR186 7 PR165 PROTON SUPRIMA S 2013 ON EXECUTIVE AUTO 140PS 1.6 TC022 PR186 8 PR121 PROTON SAVVY 2007 ON LITE MANUAL 74PS 1.2 TC018 PR118 9 PR120 PROTON SAVVY 2007 ON LITE AUTO 74PS 1.2 TC018 PR118 10 PR119 PROTON SAVVY 2007 ON MANUAL 74PS 1.2 TC018 PR118 11 PR118 PROTON SAVVY 2007 ON AUTO 74PS 1.2 TC018 PR118 12 PR208 PROTON EXORA 2015 ON SP (CFE) AUTO 140PS 1.6 TC032 PR175 13 PR207 PROTON EXORA 2015 ON BOLD PREMIUM AUTO 14PS 1.6 TC032 PR175 14 PR206 PROTON EXORA 2015 ON BOLD EXECUTIVE (CFE) 1.6 TC032 PR175 AUTO 140PS 15 PR205 PROTON EXORA 2015 ON STANDARD (CPS) MANUAL 1.6 TC032 PR175 127PS 16 PR204 PROTON EXORA 2015 ON STANDARD (CPS) AUTO 1.6 TC032 PR175 127PS 17 PR182 PROTON EXORA 2013 ON BOLD STANDARD (CFE) 1.6 TC032 PR175 AUTO 140PS 18 PR176 PROTON -

Automotive-191003-4Q19 Strategy

Sector Update 03 October 2019 Automotive NEUTRAL National Marques Racing Ahead ↔ By Wan Mustaqim Bin Wan Ab Aziz l [email protected] We maintain our NEUTRAL rating on the AUTOMOTIVE sector. The MIER consumer sentiment inde x scored 93.0 pts (+7.4pts QoQ, -39.9pts YoY) in 2Q19 which is below the optimistic threshold (>100pts) due to muted growth post the zero-rated tax holiday. Reflecting this, we are seeing car sales trending in favour of value-for-money national marques. Non-national marques on the other hand, are focusing on higher-margin lower-volume models (catering to higher-purchasing power consumers). Notable developments in Automotive industry in 2019 include: (i) National Marques surpassing Non-National marques’ market share, (ii) Proton is expected to surpass Honda as no.2 trailing behind Perodua in total industry market share TIV powered by the all-new Proton X70, and supported by all-new and face-lifted models, (iii) increasing number of new model launches, and (iv) introduction of the third national car under National Automotive Policy 2019 by year-end. No changes to our 2019 TIV target of 600,000 units matching MAA’s target factoring the extra boost from national marques (Proton and Perodua). Our sector top-pick is BAUTO (OP; TP: RM2.75) which offers a steady dividend yield of 7.2%. National marques affirming leading market position . As of 8M19, the national marques (56%) continued to stay above non-national marques (44%) in terms of market share, marking a year not seen since 2013, attributed to the outstanding sales from Perodua, especially after the introduction of its all-new Perodua Myvi and supported by the all-new Perodua Aruz (25k bookings, 20.3k delivered). -

PROCLAMATION of SALE MOTOR VEHICLES for Sale by Public Auction on Monday 4Th November 2019 @ 2.30 P.M Venue : Unit Nos

PROCLAMATION OF SALE MOTOR VEHICLES For Sale By Public Auction On Monday 4th November 2019 @ 2.30 p.m Venue : Unit Nos. B-0-6 & B-0-7, Ground Floor, Block B Megan Avenue II, No 12, Jln Yap Kwan Seng, Kuala Lumpur www.ngchanmau.com/auto "Prospect bidders may submit bids for the Auto e-Bidding via www.ngchanmau.com/auto. *Please register at least one (1) working day before auction day for registration & verification purposes". To get a digital copy of auction listings by Car Make / Model, please SMS or Whatsapp to 012-5310600. LEGAL OWNER : PUBLIC BANK BERHAD (6463-H) / PUBLIC ISLAMIC BANK BERHAD (14328-V) REGISTRATION YEAR OF KEY RESERVE PRICE LOT NO MAKE & MODEL REMARKS NO MAKE (YES / NO) (RM) STORE YARD : INTER PACIFIC AUTO AUCTION SDN. BHD. PANDAN SAFARI SHOPPING COMPLEX, CAR PARK (LEVEL 3) , NO. 1, JALAN PERDANA 6/10A, PANDAN PERDANA, 55300 KUALA LUMPUR (TELEPHONE NO : 03-9274 7612 / 9274 7613) VIEWING DATES: 31st October 2019, 1st & 2nd November 2019 (10.00AM - 3.00PM) & 4th November 2019 (10.00AM - 12.00PM) P101 PMN7720 NISSAN ALMERA 1.5 2016 YES 20,000 P102 WB8814L TOYOTA CAMRY 2.5 HYBRID 2015 NO 72,000 Unable to determine engine P103 BMU1800 MAZDA 6 2.0 2014/15 NO 53,000 number. Unable to determine engine P104 WA3299T FORD FIESTA SPORT 1.0 2014 NO 25,000 number. P105 PLF8070 HONDA ACCORD 2.4 2011/12 NO 26,000 P106 VBB8871 NISSAN TEANA 200 2017 NO 55,000 P107 CBU6650 NAZA CITRA 2.0 2006 NO 2,500 P108 WYG7208 PEUGEOT 208 1.6 2013 YES Engine number differ. -

Welfare Effects of Trade Barriers on Malaysian Car Industry: an Alternative Approach

WELFARE EFFECTS OF TRADE BARRIERS ON MALAYSIAN CAR INDUSTRY: AN ALTERNATIVE APPROACH Wai Kun C Lau (1718460) A Dissertation Submitted In Fulfilment Of The Requirements For The Degree of DOCTOR OF PHILOSOPHY FACULTY OF BUSINESS & LAW SWINBURNE UNIVERSITY OF TECHNOLOGY April 2020 i Abstract Malaysian car industry has been heavily protected by tariff and non-tariff tools since it was founded in 1983. Despite excessive tariffs imposed on foreign cars, the demand for foreign cars increases after the Asian financial crisis 1997 while the demand for domestic cars declines. Partial equilibrium framework is applied in this research because the car industry’s contribution to GDP is very small and the focus of this research is specifically on the car industry. Since cars are durable and differentiated, changes due to technological advancement may influence car demand. This research applies Discrete Choice model to account for car characteristics in addition to socio-economic factors for analysis of car demand in Malaysia. Logistic regression analysis results show factors that influence car demand are: horsepower, fuel consumption, and car size that is measured by number of passengers. Results suggest that non-tariff barriers and government incentives given to the civil servants have significant influence on Proton cars’ demand, and foreign car makers that have been operating in Malaysia before the founding of Proton enjoy their reputation from their historical experience and performance. While it is often believed that European cars have ostentatious value in Malaysia, the results show otherwise. Price elasticity of demand for major car makes is estimated based on the average horsepower, car size and fuel consumption. -

LH & RH) Chrome Inner Door Handle (4Pcs/Set

85 (ADVANCE) Air-Cond Panel Switch PROTON EXORA Fog Lamp Panel Switch PROTON EXORA Door Mirror (LH & RH) Led Door Mirror (LH & RH) TOYOTA FORTUNER / HILUX PROTON PERSONA ELEGANCE * 7 wire Upgrade PERSONA “OLD” & GEN.2 Safety Belt (Rear) Security Alarm System Auto Adjustable with Motor System TOYOTA * LH. RH, Center Fog Lamp (LH & RH) Car Audio PROTON PREVE PROTON PREVE with GPS Chrome Inner Door Handle (4pcs/set) Chrome Fog Lamp Rim (LH & RH) PROTON PERSONA / EXORA PROTON EXORA © Copyright 2006 YAC AUTO (M) Sdn. Bhd. All Rights Reserved. 86 Fog Lamp (LH & RH) Fog Lamp (LH & RH) M.TRITON '09 / PROTON INSPIRA PROTON EXORA “campaign ” Chrome Front Garnish PROTON EXORA FL 'BOLD' Reverse Sensor (Colour) PROTON EXORA “campaign ” Air Scoop (w/out Paint) TOYOTA HILUX Aluminium Loading Sill PROTON EXORA/PERODUA MYVI/PERODUA ALZA YC1990 Lower Tie Frame Bar (Beaks Bar) PROTON - WIRA/WAJA/GEN.2/PERSONA PROTON - SATRIA/SATRIA NEO Blue | Gold | Red | Silver Polishing 15” Wheel Cover Door Handle Cover (4pcs/set) Silver | Titanium PEROUDA MYVI '2011 IS200 YC2947 © Copyright 2006 YAC AUTO (M) Sdn. Bhd. All Rights Reserved. 87 Head Lamp Lid Cover (2pcs/set) Head Lamp Lid Cover (2pcs/set) PERODUA MYVI '2011 PROTON EXORA Chrome | Black | Silver | White | Grey | Yellow | Chrome | Black | Silver | White | Elegance Brown | Purple | Orange | Carbon Fiber Carbon Fiber YC2987 YC3787 Tail Lamp Cover (2pcs/set) Ultra Car Seat Mat PERODUA MYVI '2011 Chrome | Black | Silver | White | Grey | Yellow | Purple | Orange | Carbon Fiber YC2997 Aluminium Loading Si (LH & RH) PROTON EXORA YC1990 Emergency Led Lid with Magnet * 36cm x 31.5cm © Copyright 2006 YAC AUTO (M) Sdn. -

Sustainable Product Innovation Implementation: a Case at Perodua Sdn Bhd

SUSTAINABLE PRODUCT INNOVATION IMPLEMENTATION: A CASE AT PERODUA SDN BHD Nurfazliyana Jamaludin1 Noor Hidayah Abu2 School of Technology Management & Logistics, College of Business, Universiti Utara Malaysia, 06010 Sintok, Kedah [email protected], [email protected] ABSTRACT Innovation is very important in business, either for large firms and Small and Medium Enterprises (SME) especially in new products development process. Hence, many companies in Malaysia are directly involved with innovation process, especially the automobile industry. Perodua Sdn Bhd already operates for 26 years which has launched various vehicle models starting from Perodua Kancil and latest Perodua Aruz. Perodua makes innovation as the basis for product development. However, based on Malaysia Sales Satisfaction Index 2018, Perodua at the bottom ranks among 10 automotive companies based on that article. Based on customer feedback, at the early stage of operation several weaknesses have been identified in relation to product innovation produced such as design features, relationships with suppliers and safety aspects. Consequently, Perodua has taken drastic steps to improve innovation while enhancing customer satisfaction. In view of that, the main purpose of this study was to explore the innovation activity and sustainable product innovation implementation at Perodua Sdn Bhd. In this study, qualitative method based on interview was implement with Service Manager who has 10 year experience at Putrajaya Presint 14. The results of the study revealed that design, performance, features, safety serviceability and quality tool and technique that have strong relationship to achieve sustainable product innovation implementation. This paper is able to be a guideline especially for automotive company in order to achieve kaizen in their business operation and for the future researcher for the reference. -

Car Prices Down with New Sst, Tiv Up

Issue #4/2018 (November) FINAL COUNTDOWN CAR PRICES TO KLIMS 18 DOWN WITH NEW SST, TIV UP Vehicle prices from some major players have gone down, instead of going up as widely expected following the reintroduction of the Sales and Services Tax (SST) HE new government’s pared to the same period last year. decision to zero rate Passenger vehicles (PV) also the GST for three gained 6.1% (or 23,265 units) in months (June-Sep- the fi rst nine months of this year tember 2018) expect- (Full statistics on pg.3) edly spurred new vehicle sales up Vehicle prices from some Tas buyers took advantage of the major players have gone down, situation. This was refl ected in instead of going up as widely the Total Industry Volume (TIV) expected following the reintro- YTD September 2018 hitting an duction of the Sales and Services impressive gain of 6.9% compared Tax (SST). In line with the govern- to the same period last year. ment’s initiative, the new tax YB Tuan Muhammad Bakhtiar, Deputy Minister of Tourism, Arts Commercial vehicle (CV) sales structure has allowed the indus- and Culture Malaysia, MAA President and representatives of the gained the most with a hefty 24.1% try to be more competitive with grand lucky draw prizes at the launching of the KLIMS ’18 A & P or 10,680 units increase com- prices especially CKD models. • Campaign. KLIMS’18 HYPES UP AS MALAYSIA’S TOURISM EVENT, CLOCKS UP ADVERTISING AND PROMOTION MILEAGE AND LAUNCH CAR PRIZES FOR VISITORS AA is revving up the Kuala Lumpur Interna- tional Motor Show 2018 M(KLIMS’18) with an Advertising and Promotion Campaign launch on 11 October 2018 at Aloft Kuala Lumpur. -

New Car Assessment Program for South East Asia Region

Safer cars for ASEAN region New Car Assessment Program for South East Asia Region A A I S u m m i t 25 November 2013 Grand Inna Kuta, Bali Malaysian Institute of Road Safety Research (MIROS) Safer cars for ASEAN region Established on 3rd January 2007, MIROS functions as a one-stop centre for the generation and dissemination of road safety information through the print media and a concerted training programme. MIROS carries out studies and evaluates current procedures on road safety to generate information that will form the core of its evidence-based intervention programmes to enhance road safety. [email protected] 2 General inquiries: General Functions Safer cars for ASEAN region • Conduct high impact research that will be translated into road safety policies. • Develop national objectives, policies, and priorities for the orderly development and administration of road safety research. • Enhance and increase knowledge based on new developments in issues related to road safety. • Serve as an audit and accreditation agency in curriculum design and standards on road safety. • Propose evidenced based cost-effective interventions/ programmes. • Serve as a repository of knowledge and linkage on road safety. • Serve as a centre providing consultation and advice on road safety issues. [email protected] 3 General inquiries: General Safer cars for ASEAN region [email protected] 4 General inquiries: General UN Decade of Action for Road Safety – May 11 2011 Safer cars for ASEAN region The Decade was approved by the Moscow Ministerial in 2009 and UN General Assembly in 2010. It was launched by a global relay of events on 11th May.