Emerging Lessons from Half a Century of Fiscal Federalism in Switzerland

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rapport De La Municipalité Au Conseil Communal Sur Sa Gestion Pendant L’Année 2019

Rapport de la Municipalité au Conseil communal sur sa gestion pendant l’année 2019 Réf : 05/2020 Monsieur le Président, Mesdames, Messieurs les Conseillers, Conformément aux dispositions : de la Loi du 28 février 1956 (mise à jour le 1er janvier 2007) sur les communes, article 93c, du Règlement du 14 décembre 1979 (mis à jour le 1er juillet 2007) sur la comptabilité des communes, article 34, du Règlement du Conseil communal de Cossonay, du 19 novembre 2014, article 91, la Municipalité a l’honneur de vous soumettre le présent rapport sur sa gestion pendant l’année 2019. Les comptes, accompagnés de commentaires, font l’objet d’un document séparé (réf. 04/2020). Le Conseil communal a été présidé par M. Jacky Cretegny tout au long de l’année 2019. Au 31 décembre 2019, la composition du Conseil communal, ainsi que celle de ses commissions et délégations étaient les suivantes : Président : Jacky Cretegny Première Vice-Présidente : Florence Texier Claessens Deuxième Vice-Président : Oscar Lazzarotto Scrutateurs : Marie-Claire Leiser José Noriega Scrutateurs-suppléants : Jonathan Sidler Barbara Zippo Huissiers : Nathalie Martin et Pierre Mermoud (huissier suppléant) Secrétaire : Marianne Rufener Commission de gestion : Patrick Baudin Yves Corday Pascal Gindroz Diego Marin Etienne Martin Commission des finances : Renata Bosco Ehrbar Joachim Cretegny Philippe Zufferey Gaël Girardet Thomas Sigrist Délégués au Conseil intercommunal de l’Association intercommunale pour l’épuration des eaux (A.I.E.E.) : Joey Dias Nicolas Schlaeppi Patrick Bolay -

Events & Festivals May—October 2018

R E B T O C O S Y U A U T B R E E Y A E L P U S J M N T E M U J EVENTS & FESTIVALS MAY—OCTOBER 2018 R E B T O C O S Y U A U T B R E E Y A E L P U S J M N T E M U J Dream, sing, dance, and get carried away… Experience pure emotions with your family or friends thanks to the festivals and events in Vaud! The return of the warm season To discover many more stimulates our senses and makes events, connect to our us want to celebrate, enjoy Online Agenda which is also accessible with ourselves and share powerful and the app Vaud:Guide. beautiful moments. The events of the canton of Vaud, be they in the cities or the mountains, are ideal to experience intense moments. The festivals of music vaud-events.ch and living arts as well as sports competitions and the famous Wheat and Bread Festival of Echallens – a key event of the year 2018 – all offer unique moments Vaud:Guide that will make your heart beat to the rhythm of the canton of Vaud! Don’t miss our winter agenda available from November. regionduleman myvaud Photographs—David Schweizer, Camille Scherrer, Davide Gostoli, Anne-Laure Lechat, Alain Candellero, Gilbert Painblanc, www.alphafoto.com, Montreux Vevey Tourisme, François Melillo, Marie Pugin, 2013 FFJM – Lionel Flusin, Olivier Fatzer, Anthony Anex. Design—DidWeDo. J M U N A E Y J U L Y T A U U S T S P E M E B E R O C T OB E R R E B T O C O S Y U A U T B R E E Y A E L P U S J M N T E M U J TRADITIONAL FESTIVALS Midsummer festival and Désalpe What is more modern than 4—5 AUGUST MIDSUMMER IN being traditional? Customs TAVEYANNE and traditions are trendier Taveyanne www.villars-diablerets.ch than ever, and we are very pleased about that! Alphorn 18 AUGUST MIDSUMMER FESTIVAL players, makers of mountain St-Cergue cheese and well-groomed www.mi-ete-st-cergue.ch cows are admired and 22 SEPTEMBER photographed like real stars, 22nd VACHERIN MONT-D’OR FESTIVAL especially during one or the Les Charbonnières other of the many traditional www.myvalleedejoux.ch celebrations in Vaud. -

Cote : C XX 60 Intitulé : Chaux (La, Cossonay)

ARCHIVES CANTONALES VAUDOISES Section C : Parchemins et papiers Sous-section C XX : Communes vaudoises Cote : C XX 60 Intitulé : Chaux (La, Cossonay) INVENTAIRE Conditions de consultation : Libre Date de l'instrument de recherche (dernière mise à jour) : 22.01.2010 © Archives cantonales vaudoises Date d'extraction des données: 21.07.2017 [va] C XX 60 Chaux (La, Cossonay) 2 DESCRIPTION AU NIVEAU DU FONDS IDENTIFICATION Cote: C XX 60 Intitulé: Chaux (La, Cossonay) Dates: 1328 décembre 23 - 1795 juin 10 Date de constitution: 1916 - 1990 au moins. Niveau de description: Fonds Importance matérielle et support: 16 pièces Dimension: 0.05 CONTEXTE Nom du producteur d'archives: Archives cantonales vaudoises (collection) Histoire du producteur: - Historique de la conservation: - Modalités d’entrée: La collection de parchemins et de papiers concernant les communes vaudoises portant la cote générique C XX a été constituée par les ACV entre 1916 et environ 1990 (C XX 60 - La Chaux). Provenance des documents classés sous C XX: collection de Charles-Philippe Dumont achetée par les ACV en 1910, collections constituées par le Canton de Berne décrites notamment dans les inventaires blanc, vert et rouge, divers fonds d'archives de famille, etc. Certaines pièces ont été récupérées dans des reliures de registres, d'autres ont été collectées ça et là par les ACV. Date(s) d’entrée: 01.01.1798, 31.12.1990 CONTENU ET STRUCTURE Présentation du contenu: Collection de parchemins et de papiers concernant la commune de La Chaux (Cossonay). © Archives cantonales vaudoises -

2015 : Consultation D'horaire Réponses Aux Interventions (Version 1.5)

Direction générale de la mobilité et des routes Division management des transports Av. de l'Université 5 1014 Lausanne 141101 Consultation d'horaire 2014 - Réponses aux interventions_V1.5 DIRH – DGMR – MT / JN Lausanne, le 5 novembre 2014 Projet d’horaire 2015 : Consultation d'horaire Réponses aux interventions (version 1.5) SOUS RESERVE DE MODIFICATIONS Département des infrastructures et des ressources humaines Direction générale de la mobilité et des routes www.vd.ch/dgmr Tél. +41 21 316 73 73 / Fax : +41 21 316 73 76 Direction générale de la mobilité et des routes Division management des transports 141101 Consultation d'horaire 2014 - Réponses aux interventions_V1.5 Table des matières Préambule ................................................................................................................................................3 Transports ferroviaires ..............................................................................................................................4 CFF – Chemins de fer fédéraux ................................................................................................................................................................... 4 100 Lausanne – Sion – Brig ................................................................................................................................................................ 4 111 Vevey – Puidoux-Chexbres (Train des Vignes) ........................................................................................................................... -

Document ISOS Commune D'aubonne

Aubonne ® Commune d’Aubonne, district de Morges, canton de Vaud Ortsbilder Photo aérienne Bruno Pellandini 2008, © OFC, Berne Petite ville d’origine médiévale très bien préservée, située sur un coteau et dominée par un impressionnant château entouré par une couronne d’espaces libres. Longue allée menant à un remarquable point de vue. Petite ville/bourg £££ Qualités de situation £££ Qualités spatiales £££ Qualités historico-architecturales Carte Siegfried 1895 Carte nationale 2009 1 Aubonne Commune d’Aubonne, district de Morges, canton de Vaud 1 La Vieille Ville, à gauche Maison de Ville, 1801–04, au centre Hôtel de Ville, 18e–19e s. 2 3 2 Aubonne ® Commune d’Aubonne, district de Morges, canton de Vaud Ortsbilder 34 32 33 27 8 31 30 26 7 6 24 5 29 9 23 25 22 28 4 21 19 20 11 15 1 10 3 2 14 18 13 17 12 16 Base du plan: PB-MO 1:5000, Etabli sur la base des données cadastrales, Autorisation de l’Office de l’information sur le territoire - Vaud N° 05/2014 Emplacement des prises de vue 1: 10000 Photographies 2013 : 1–34 4 5 6 Extrémité supérieure de la Grande-Rue 3 Aubonne Commune d’Aubonne, district de Morges, canton de Vaud 7 Rue de Bourg-de-Four 8 9 Accès au niveau de la porte de Bougy, reconstr. 1759, par le « pont », att. 1729 10 Groupement du Chaffard 11 4 Aubonne ® Commune d’Aubonne, district de Morges, canton de Vaud Ortsbilder 13 Chapelle de Trévelin, 1861 12 Rue de Trévelin 14 15 Anc. fossés et maisons de la Vieille Ville 16 Allée de maronniers, att. -

10.735 Morges - Aclens - Cossonay-Ville État: 7

ANNÉE HORAIRE 2020 10.735 Morges - Aclens - Cossonay-Ville État: 7. Novembre 2019 Lundi–vendredi, sauf fêtes générales, sauf 21.9. 7301 7303 7305 7307 7309 7311 7313 7315 7317 Genève dép. 5 30 6 30 7 30 8 30 9 30 10 30 11 30 Lausanne dép. 5 51 5 58 6 51 6 58 7 51 8 58 9 58 10 58 11 58 Morges, gare 6 08 6 21 7 08 7 21 8 08 9 14 10 14 11 14 12 14 Lonay, parc 6 17 7 17 8 17 9 23 10 23 11 23 12 23 Bremblens, bas du village 6 20 6 32 7 20 7 32 8 20 9 26 10 26 11 26 12 26 Romanel-sur-Morges, poste 6 23 6 34 7 23 7 34 8 23 9 29 10 29 11 29 12 29 Aclens, collège 6 25 6 36 7 25 7 36 8 25 9 31 10 31 11 31 12 31 Romanel-sur-M., 6 40 7 40 Moulin-du-Choc Bussigny VD, gare sud 6 48 7 48 Gollion, village 6 28 7 28 8 28 9 34 10 34 11 34 12 34 Allens, village 6 30 7 30 8 30 9 36 10 36 11 36 12 36 Cossonay-Ville, centre 6 33 7 33 8 33 9 39 10 39 11 39 12 39 7319 7321 7323 7325 7327 7329 7331 7333 7335 Genève dép. 12 30 13 30 14 30 15 30 16 00 16 30 17 00 17 30 18 00 17 05 Lausanne dép. -

Région Morges – Aubonne

formation jeunessed’adultes enfance Morges – Aubonne Septembre 2021 Région Juin 2022 CHARTE La formation d’adultes vise à développer chez les participants: la capacité de dialogue entre personnes 1 confessant leur foi et personnes en recherche la faculté d’écouter d’autres avis, d’élargir et de 2 confronter positivement leurs points de vue la capacité de discerner les enjeux éthiques et 3 les valeurs en débat dans la société l’acquisition de connaissances bibliques 4 et théologiques la capacité à relier les connaissances reçues 5 à l’itinéraire personnel de vie Chacun peut librement et en sécurité: clarifier sa quête spirituelle et faire le point sur sa 6 foi et ses convictions se positionner par rapport à l’Eglise et à la 7 société et réfléchir aux implications de sa foi personnelle vivre s’il le souhaite un processus de 8 transformation dont le cheminement et l’issue lui appartiennent EERV 2021 – © OIC 1 Table des matières Editorial .....................................................................................................................3 Explorer la Bible La Bible pour les nuls................................................................................................4 Creuser un thème Sur les traces de Jésus..............................................................................................5 Approfondir ma spiritualité D’une page à l’Autre...............................................................................................6 Danser avec ses joies et ses peines !......................................................................7 -

C'est Parti, Ma Région !

Chigny Denges Echandens Echichens Lonay Lully Lussy-sur- Morges Préverenges Saint-Prex Tolochenaz Morges C’est parti, ma Région ! Compte-rendu de la 2ème Conférence régionale Région Morges Sommaire Editorial . 1 Echanges et discussions . 2 Exposition publique . 6 Exposition des enfants . 12 Tour en bus . 16 Tables rondes . 18 En images . 20 © Région Morges – Réalisation : DidWeDo – Photos : Stéphane Etter 1 Editorial 9h25, une trentaine de participants se rassemblent devant la salle de La Crosette . Ils sont venus découvrir à quoi ressemblera leur région d’ici quelques années . Parmi eux, de simples citoyens, mais aussi plusieurs élus désirant s’informer davantage . Quelques instants plus tard, le bus démarre et la visite commence . On traverse le village de Denges pour découvrir les premiers projets de plans de quartier . Les grues ne sont pas encore là mais un ancien hangar agricole a déjà été démoli pour laisser place à de nouveaux logements . Pour la suite, il faudra imaginer… On passe Préverenges, puis Morges . « C’est trop grand ! » s’ex- clame l’un des participants lorsque nous arrivons à proximité du chantier des Résidences du Lac, sur l’ancien site des Fonderies . « Et bien c’est le plus petit de nos projets… » lui répond l’urba- niste de la Ville . Il est vrai que les projets suivants sont d’une autre envergure : SudVillage, Prairie-Nord / Eglantine, Morges Gare-Sud, … de quoi accueillir plusieurs milliers d’habitants et d’emplois . Une heure plus tard, alors que la visite s’achève, l’un des partici- pants me confie qu’il habite à Denges depuis plus de … 60 ans ! Je me dis que le village a dû passablement changer depuis . -

Morges – Préverenges – St-Sulpice – Lausanne, 701 Bourdonnette

Morges – Préverenges – St-Sulpice – Lausanne, 701 Bourdonnette Morges,Morges, gare Morges,poste Morges,Casino Morges,temple Morges,Blancherie Morges,Parc de Préverenges,BiefVertou Préverenges, TaudazDenges, villageSt-Sulpice, Pierraz-MurSt-Sulpice, VenogeSt-Sulpice, Laviausud St-Sulpice, ChantresSt-Sulpice, centreSt-Sulpice, BochetSt-Sulpice, Parc Ecublens,Scientifique PâqueretEcublens, ChampagneEcublens, BlévallaireLausanne, allée de Dorigny Bourdonnette LUNDI – VENDREDI sauf fêtes générales et lundi du Jeûne (20 septembre) Morges, gare 5 10 5 25 5 40 5 55 6 10 6 25 6 40 6 50 7 00 7 10 8 50 9 00 9 10 9 25 15 25 15 40 15 55 Morges, temple 5 12 5 27 5 42 5 57 6 12 6 27 6 42 6 52 7 02 7 12 8 52 9 02 9 12 9 27 15 27 15 43 15 58 Morges, Parc de Vertou 5 13 5 28 5 43 5 58 6 14 6 29 6 44 6 54 7 04 7 14 8 54 9 04 9 14 9 29 15 29 15 45 16 00 Préverenges, village 5 16 5 31 5 46 6 01 6 17 6 32 6 47 6 57 7 08 7 18 8 58 9 07 9 17 9 32 15 32 15 48 16 03 Denges, Pierraz-Mur 5 18 5 33 5 48 6 03 6 19 6 34 6 49 6 59 7 10 7 20 9 00 9 09 9 19 9 34 15 34 15 50 16 05 St-Sulpice, Venoge sud 5 20 5 35 5 50 6 05 6 21 6 36 6 51 7 01 7 12 7 22 9 02 9 11 9 21 9 36 15 36 15 52 16 07 St-Sulpice, centre 5 23 5 38 5 53 6 08 6 24 6 39 6 54 7 04 7 15 7 25 9 05 9 14 9 24 9 39 15 39 15 56 16 11 St-Sulpice, Parc Scientifique 5 26 5 41 5 56 6 11 6 28 6 43 6 58 7 08 7 18 7 28 9 08 9 18 9 28 9 43 15 43 15 59 16 14 toutes les 10 minutes toutes les 15 minutes Ecublens, Blévallaire 5 28 5 43 5 58 6 13 6 31 6 46 7 01 7 11 7 22 7 32 9 12 9 21 9 31 9 46 15 46 16 03 16 18 Lausanne, -

Liste Des Communes Avec Leur Ancien District

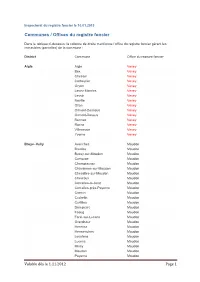

Inspectorat du registre foncier le 10.01.2013 Communes / Offices du registre foncier Dans le tableau ci-dessous, la colonne de droite mentionne l’office du registre foncier gérant les immeubles (parcelles) de la commune : District Commune Office du registre foncier Aigle Aigle Vevey Bex Vevey Chessel Vevey Corbeyrier Vevey Gryon Vevey Lavey-Morcles Vevey Leysin Vevey Noville Vevey Ollon Vevey Ormont-Dessous Vevey Ormont-Dessus Vevey Rennaz Vevey Roche Vevey Villeneuve Vevey Yvorne Vevey Broye–Vully Avenches Moudon Brenles Moudon Bussy-sur-Moudon Moudon Carrouge Moudon Champtauroz Moudon Chavannes-sur-Moudon Moudon Chesalles-sur-Moudon Moudon Chevroux Moudon Corcelles-le-Jorat Moudon Corcelles-près-Payerne Moudon Cremin Moudon Cudrefin Moudon Curtilles Moudon Dompierre Moudon Faoug Moudon Forel-sur-Lucens Moudon Grandcour Moudon Henniez Moudon Hermenches Moudon Lovatens Moudon Lucens Moudon Missy Moudon Moudon Moudon Payerne Moudon Valable dès le 1.11.2012 Page 1 Prévonloup Moudon Ropraz Moudon Rossenges Moudon Sarzens Moudon Syens Moudon Trey Moudon Treytorrens (Payerne) Moudon Valbroye Moudon Villars-le-Comte Moudon Villarzel Moudon Vucherens Moudon Vulliens Moudon Vully-les-Lacs Moudon Gros-de-Vaud Assens Yverdon Bercher Yverdon Bettens Yverdon Bioley-Orjulaz Yverdon Bottens Yverdon Boulens Yverdon Bournens Yverdon Boussens Yverdon Bretigny-sur-Morrens Yverdon Cugy Yverdon Daillens Yverdon Echallens Yverdon Essertines-sur-Yverdon Yverdon Etagnières Yverdon Fey Yverdon Froideville Yverdon Goumoëns Yverdon Jorat-Menthue Yverdon Lussery-Villars -

Questionnaire « Naturalisation » Questions Locales Morges

Questionnaire « naturalisation » Questions locales Morges GEOGRAPHIE QUESTION 1 Quelles sont les communes qui touchent la commune de Morges ? ☒ Préverenges, Lonay, Echichens, Chigny et Tolochenaz ☐ Préverenges, Echichens, St-Prex, Vufflens-le-Château et Denges ☐ Lonay, Tolochenaz, St-Sulpice, Echandens et Etoy ☐ Echichens, Chigny, Aubonne, Allaman et Rolle QUESTION 2 Quelles sont les deux rivières qui touchent le territoire morgien ? ☒ La Morges et le Bief ☐ La Venoge et le Boiron ☐ La Morges et la Versoix ☐ Le Bief et le Talent QUESTION 3 Combien de grands parcs publics compte la Ville de Morges au bord du lac ? ☒ 2 ☐ 5 ☐ 1 ☐ 3 QUESTION 4 Quels sont les noms des parcs publics de la Ville de Morges au bord du lac ? ☒ Parc de Vertou et Parc de l’Indépendance ☐ Parc de Vertou et Parc des Nations ☐ Parc de l’Indépendance et Parc du Temple ☐ Parc du Temple et Parc de Vidy QUESTION 5 Savez-vous ce qui est représenté sur le drapeau de la Ville de Morges ? ☒ Les deux rivières: La Morges et le Bief ☐ Le château ☐ Un coq ☐ Un poisson QUESTION 6 Quelle est l’altitude la plus basse ? ☒ 374 mètres ☐ 180 mètres ☐ 264 mètres ☐ 905 mètres QUESTION 7 Quelle est la surface de la Ville ? ☒ 3,83 km2 ☐ 3,50 km2 ☐ 2,86 km2 ☐ 8,32 km2 QUESTION 8 Qu’est-ce qui délimite le territoire communal au Nord ? ☒ Le vignoble ☐ Le Lac Léman ☐ Le collège de Marcelin ☐ Le Bief HISTOIRE QUESTION 1 Quelle est la date de la fondation de la Ville de Morges ? ☒ 1286 ☐ 1291 ☐ 1803 ☐ 1515 QUESTION 2 Quelle personnalité est liée à l'histoire de la Ville de Morges ? ☒ Ignace Paderewski -

INTERNATIONAL HEADQUARTERS a Flagship Activity of the Canton of Vaud 2 VAUD ECONOMIC PROMOTION / INTERNATIONAL HEADQUARTERS

INTERNATIONAL HEADQUARTERS A flagship activity of the canton of Vaud 2 VAUD ECONOMIC PROMOTION / INTERNATIONAL HEADQUARTERS AN ATTRACTIVE SETTING FOR BUSINESSES AT THE HEART OF EUROPE The canton of Vaud has many distinctive advantages: it is both a highly prosperous region and a center of global innovation while benefiting from a high concentration of academic institutes. Vaud is also located in the heart of Switzerland, a country that enjoys great economic stability and is marked by a strong work ethic. A major center of global innovation, the canton of Vaud Some young companies, following the example of the US benefits from many assets. In addition, the quality of life is startup Magic Leap, specialized in augmented reality, have excellent, which explains why many foreign companies chosen the central location of the canton of Vaud to expand decide to set up their headquarters there. Major companies into Europe, or even into the Asian market. with international reputations are present across all economic sectors: Nissan, Medtronic, Nestlé, Chiquita, Edwards Lifesciences, SC Johnson, Cisco, Honeywell, BOBST, Incyte, Becton Dickinson. Some of these companies were born in the canton, others have established themselves in the region to establish their global, EMEA region (Europe, Middle East and Africa) or European headquarters. “I would recommend the canton of Vaud without hesitation to any company that wishes to set up business in Europe for all the reasons that led Medtronic to do so: its location at the heart of the continent, its reputation for quality and precision, its highly skilled personnel, the proximity of FRANÇOIS MONORY Vice-president of operations advanced scientific research centers and international at the Medtronic Cardiac and organizations (UN, WHO).” Vascular Group AN IDEAL ENVIRONMENT FOR INVESTING Located in the heart of Europe, The canton of Vaud is the largest of the There are some 50,000 companies in Switzerland never ceases to amaze French-speaking cantons, but also the the canton, mainly operating in the with its diversity and prosperity.