Transportation Insurance on Contract Liability and Brokers Liability

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

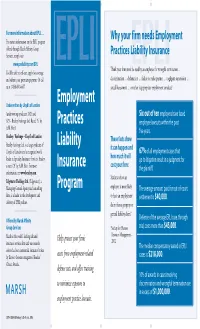

Employment Practices Liability Insurance Program EPLI

B5848_EPLI 2/14/06 2:49 PM Page 1 For more information about EPLI … Why your firm needs Employment For instant information on the EPLI program offered through Marsh Affinity Group Services, simply visit Practices Liability Insurance www.proliablity.com/EPLI Think your firm won’t be sued by an employee for wrongful termination … You’ll be able to self-rate, apply for coverage EPLI EPLI and submit your premium payment. Or call discrimination … defamation … failure to make partner … negligent supervision … us at 1-888-601-6667. sexual harassment … or other inappropriate employment conduct? Underwritten by Lloyd’s of London Employment (underwriting syndicates 2623 and Six out of ten employers have faced 623 – Beazley Furlonge Ltd. Rated “A” by Practices employee lawsuits within the past A.M. Best) five years. Beazley / Furlonge – Lloyd’s of London These facts show Beazley Furlonge Ltd. is a large syndicate of Liability it can happen and Lloyd’s of London and a recognized world 67% of all employment cases that leader in Specialty Insurance Services. Beazley how much it will go to litigation result in a judgment for is rated “A” by A.M. Best. For more Insurance cost your firm: the plaintiff. information, see www.beazley.com. Statistics show an Edgewater Holdings Ltd. (Edgewater), a Managing General Agency and consulting Program employer is more likely The average amount paid for out-of-court firm, is a leader in the development and to have an employment settlement is $40,000. delivery of EPLI policies. claim than a property or general liability claim.* Offered by Marsh Affinity Defense of the average EPLI case, through Group Services *Society for Human trial, costs more than $45,000. -

The Experience of the French Civil Code

NORTH CAROLINA JOURNAL OF INTERNATIONAL LAW Volume 20 Number 2 Article 3 Winter 1995 Codes as Straight-Jackets, Safeguards, and Alibis: The Experience of the French Civil Code Oliver Moreleau Follow this and additional works at: https://scholarship.law.unc.edu/ncilj Recommended Citation Oliver Moreleau, Codes as Straight-Jackets, Safeguards, and Alibis: The Experience of the French Civil Code, 20 N.C. J. INT'L L. 273 (1994). Available at: https://scholarship.law.unc.edu/ncilj/vol20/iss2/3 This Article is brought to you for free and open access by Carolina Law Scholarship Repository. It has been accepted for inclusion in North Carolina Journal of International Law by an authorized editor of Carolina Law Scholarship Repository. For more information, please contact [email protected]. Codes as Straight-Jackets, Safeguards, and Alibis: The Experience of the French Civil Code Cover Page Footnote International Law; Commercial Law; Law This article is available in North Carolina Journal of International Law: https://scholarship.law.unc.edu/ncilj/vol20/ iss2/3 Codes as Straight-Jackets, Safeguards, and Alibis: The Experience of the French Civil Code Olivier Moriteaut I. Introduction: The Civil Code as a Straight-Jacket? Since 1789, which marked the year of the French Revolution, France has known no fewer than thirteen constitutions.' This fact is scarcely evidence of political stability, although it is fair to say that the Constitution of 1958, of the Fifth Republic, has remained in force for over thirty-five years. On the other hand, the Civil Code (Code), which came into force in 1804, has remained substantially unchanged throughout this entire period. -

Use the Force? Understanding Force Majeure Clauses

Use the Force? Understanding Force Majeure Clauses J. Hunter Robinson† J. Christopher Selman†† Whitt Steineker††† Alexander G. Thrasher†††† Introduction It has been said that, sooner or later, everything old is new again.1 In the wake of the novel coronavirus pandemic (COVID-19) sweeping the globe in 2020, a heretofore largely overlooked and even less understood nineteenth century legal term has come to the forefront of American jurisprudence: force majeure. Force majeure has become a topic du jour in the COVID-19 world with individuals and companies around the world seeking to excuse non- † B.S. (2011), Auburn University; J.D. (2014), Emory University School of Law. Hunter Robinson is an associate at Bradley Arant Boult Cummings LLP. Hunter is a member of the firm’s litigation and banking and financial services practice groups and represents clients in commercial litigation matters across the country. †† B.S. (2007), Auburn University; J.D. (2012), University of South Carolina School of Law. Chris Selman is a partner at Bradley Arant Boult Cummings LLP. Chris is a members of the firm’s construction and government contracts practice group. He has extensive experience advising clients at every stage of a construction project, managing the resolution of construction disputes domestically and internationally, and drafting and negotiating contracts for a variety of contractor and owner clients. ††† B.A. (2003), University of Alabama; J.D. (2008), Georgetown University Law Center. Whitt Steineker is a partner at Bradley Arant Boult Cummings LLP. Whitt is a member of the firm’s litigation practice group, where he advises clients on a full range of services and routinely represents companies in complex commercial litigation. -

Interview With

entrevista a Nikos Antimissaris Consejero – Director General MAPFRE ASISTENCIA Madrid – España Contact center de MAPFRE ASISTENCIA en China Nikos Antimissaris, griego de nacimiento, cursó la Licenciatura en Administración de Empresas en la Universidad de Lieja (Bél- gica), vinculándose a España el último año de universidad, al es- tudiar entre 1992 y 1993 en la Universidad de Valladolid (España) dentro del programa europeo ERASMUS. Completó su formación académica con el MBA del Instituto de Empresa Business School, de Madrid (España). Además del griego, domina el inglés, el fran- cés y el español. Su carrera profesional se inició en 1994 en su país natal con MAPFRE ASISTENCIA, como Director General de la Unidad de Negocio de Grecia. En 2001 fue trasladado a los Servicios Cen- trales en Madrid para dirigir el negocio del área geográfica de Europa y Oriente Medio. En 2004 fue promocionado a Subdirec- tor General de la entidad y desde 2006 ostenta el cargo de Con- sejero Director General de MAPFRE ASISTENCIA. 40 / 67 / 2013 667_trebol_esp.indd7_trebol_esp.indd 4040 007/11/137/11/13 001:581:58 “MAPFRE ASISTENCIA aporta una solución integral a sus socios aseguradores que incluye, no sólo la suscripción del riesgo (por la vía del reaseguro), sino también toda la infraestructura operativa para la tramitación de los siniestros y la prestación de los servicios.” Nikos Antimissaris habla siempre en primera persona del plural porque siente que alcanzar en 2013 un volumen de ingresos de mil cien millones de euros es una labor de los seis mil empleados de MAPFRE ASISTENCIA desde los cuarenta y cinco países en que está presente. -

Is COVID-19 an Act of God And/Or Will COVID-19 Be a Defense Against Failure to Perform? Swata Gandhi

ALERT Corporate Practice MAY 2020 Is COVID-19 an Act of God and/or Will COVID-19 Be a Defense Against Failure to Perform? Swata Gandhi This is the second in a series of alerts on Force Majeure and Common Law Defenses against failure to perform contracts. In our first alert, we discussed the elements of a force majeure clause and looked at how various states have interpreted force majeure clauses. We focused on how most states take a narrow view of these provisions and they adhere to the plain meaning of the force majeure provisions. This alert takes a look at one event often listed in force majeure clauses – Acts of God. As discussed in our previous alert, some courts will excuse performance of a contract only if the event causing the breach is actually listed in the force majeure clause. Among the list of events that would most likely excuse a failure to perform under a contract due to COVID-19 would be if the force majeure provision listed pandemics, epidemic, health emergencies or government orders or regulations. While your contract may not list these events, most force majeure provisions do include an Act of God. In this alert we look at whether it is likely that courts will find that COVID-19 is an Act of God and if such consideration will actually be a defense against performance of a contract. In general, courts have found that an Act of God is a natural event that would not occur by the intervention of man, but proceeds from physical causes. -

Consumers Guide to Auto Insurance

CONSUMERS GUIDE TO AUTO INSURANCE PRESENTED TO YOU BY THE DEPARTMENT OF BUSINESS REGULATION INSURANCE DIVISION 1511 PONTIAC AVENUE, BLDG 69-2 CRANSTON, RI 02920 TELEPHONE 401-462-9520 www.dbr.ri.gov Elizabeth Kelleher Dwyer Superintendent of Insurance TABLE OF CONTENTS Introduction………………………………………………………………1 Underwriting and Rating………………………………………………...1 What is meant by underwriting and how is it accomplished…………..1 How are rates and premium charges determined in Rhode Island……1 What factors are considered in ratemaking……………………………. 2 What discounts are used in determining final premium cost…………..3 Rhode Island Automobile Insurance Plan…………………..…………..4 Regulation of Rates……………………………………………………….4 The Tort System…………………………………………………………..4 Liability Coverages………………………………………………………..5 Coverages Other Than Liability…………………………………………5 Physical Damage to the Automobile……………………………………..6 Other Optional Coverages………………………………………………..6 The No-Fault System……………….……………………………………..7 Smart Shopping……………………………………………………………7 Shop for True Comparison………………………………………………..8 Consumer Protection Available...…………………………………………8 What to Do if You are in an Automobile Accident………………………9 Your State Insurance Department………………………………….........9 Auto Insurance Buyer’s Worksheet…………………………………….10 Introduction Auto insurance is an expensive purchase for most Americans, and is especially expensive for Rhode Islanders. Yet consumers rarely comparison-shop for auto insurance as they might for other products and services. Auto insurance companies vary substantially both in price and service to policyholders, so it pays to shop around and compare different insurance companies. This guide to buying auto insurance was developed to help you become a more knowledgeable policyholder and to get the combination of price and service best suited to your needs. It provides information on how to shop for coverage and how insurance premiums are determined. You will also find an Auto Insurance Buyer’s Worksheet in the guide to help you compare premium prices among insurers. -

Tax Risk Insurance: Taking It Captive

taxnotes federal ■ Volume 171, Number 4 April 26, 2021 Tax Risk Insurance: Taking It Captive by Ken Brewer and Albert Liguori Reprinted from Tax Notes Federal, April 26, 2021, p. 549 For more Tax Notes content, please visit www.taxnotes.com. © 2021 Tax Analysts. All rights reserved. Analysts does not claim copyright in any public domain or third party content. TAX PRACTICE tax notes federal Tax Risk Insurance: Taking It Captive by Ken Brewer and Albert Liguori is to explore the U.S. tax implications of that meeting. Behold: captive tax risk insurance!3 In our experiences, the use of tax risk insurance has been most prevalent in the mergers and acquisitions context. But as we mentioned in our last article, we have seen it becoming more common in the context of large corporate groups seeking to manage their global tax risks, regardless of whether they are related to M&A.4 In either context, the use of tax risk insurance lends itself to captive arrangements, for the same reasons that have caused captive arrangements to be desirable for other types of insurance risks. Ken Brewer is a senior adviser and Captive Insurance and the U.S. Tax Implications international tax practitioner with Alvarez & Thereof Marsal Taxand LLC in Miami, and Albert Liguori is a managing director in the firm’s New As an alternative to traditional insurance York office. The authors send special thanks to protection, which is obtained from one or more of Brian Pedersen, managing director at Alvarez & the many underwriters offering that coverage to Marsal Taxand, for his contributions and the public, captive insurance is obtained from a review. -

Auto Insurance and How Those Terms Affect Your Coverage

Arkansas Insurance Department AUTOMOBILE INSURANCE Asa Hutchinson Allen Kerr Governor Commissioner A Message From The Commissioner The Arkansas Insurance Department takes very seriously its mission of “consumer protection.” We believe part of that mission is accomplished when consumers are equipped to make informed decisions. We believe informed decisions are made through the accumulation and evaluation of relevant information. This booklet is designed to provide basic information about automobile insurance. Its purpose is to help you understand terms used in the purchase of auto insurance and how those terms affect your coverage. If you have questions or need additional information, please contact our Consumer Services Division at: Phone: (501) 371-2640; 1-800-852-5494 Fax: (501) 371-2749 Email: [email protected] Web site: www.insurance.arkansas.gov Mission Statement The primary mission of the State Insurance Department shall be consumer protection through insurer insolvency and market conduct regulation, and fraud prosecution and deterrence. 1 Coverages Provided by Automobile Insurance The automobile insurance policy is comprised of several separate types of coverages: COLLISION, COMPREHENSIVE, LIABILITY, PERSONAL INJURY PROTECTION, UNINSURED MOTORIST, UNDERINSURED MOTORIST and other coverages. You are required by law to purchase liability protection only. All others are voluntary unless required by a lienholder. LIABILITY Under Legislation passed in 1987 and 1999, it is unlawful for any person to operate a motor vehicle within this state unless the vehicle is insured with the minimum amount of liability coverage: $25,000 for bodily injury or death of one person in any one accident; $50,000 for bodily injury or death of two or more persons in any one accident and $25,000 for damage to or destruction of the property of others. -

Force Majeure and Climate Change: What Is the New Normal?

Force majeure and Climate Change: What is the new normal? Jocelyn L. Knoll and Shannon L. Bjorklund1 INTRODUCTION ...........................................................................................................................2 I. THE SCIENCE OF CLIMATE CHANGE ..................................................................................4 II. FORCE MAJEURE: HISTORY AND DEVELOPMENT .........................................................8 III. FORCE MAJEURE IN CONTRACTS ...................................................................................11 A. Defining the Force Majeure Event. ..............................................................................12 B. Additional Contractual Requirements: External Causation, Unavoidability and Notice 15 C. Judicially-Imposed Requirements. ...............................................................................18 1. Foreseeability. .................................................................................................18 2. Ultimate (or external) causation.....................................................................21 D. The Effect of Successfully Invoking a Contractual Force Majeure Provision ............25 E. Force Majeure in the Absence of a Specific Contractual Provision. ...........................25 IV. FORCE MAJEURE PROVISIONS IN STANDARD FORM CONTRACTS AND MANDATORY PROVISIONS FOR GOVERNMENT CONTRACTS ......................................28 A. Standard Form Contracts .............................................................................................28 -

Consent Decree: United States Of

UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF GEORGIA ATLANTA DIVISION UNITED STATES OF AMERICA, ) ) Plaintiff, ) ) Civil Action No. 1:00-CV-3142 JTC v. ) ) CONSENT DECREE COLONIAL PIPELINE COMPANY, ) ) Defendant. ) ____________________________________) I. BACKGROUND A. Plaintiff, the United States of America (“United States”), through the Attorney General, at the request of the Administrator of the United States Environmental Protection Agency (“EPA”), filed a civil complaint (“Complaint”) against Defendant, Colonial Pipeline Company (“Colonial”), pursuant to the Clean Water Act (“CWA”), 33 U.S.C. §§ 1251 et seq., seeking injunctive relief and civil penalties for the discharge of oil into navigable waters of the United States or onto adjoining shorelines. B. The Parties agree that it is desirable to resolve the claims for civil penalties and injunctive relief asserted in the Complaint without further litigation. C. This Consent Decree is entered into between the United States and Colonial for the purpose of settlement and it does not constitute an admission or finding of any violation of federal or state law. This Decree may not be used in any civil proceeding of any type as evidence or proof of any fact or as evidence of the violation of any law, rule, regulation, or Court decision, except in a proceeding to enforce the provisions of this Decree. D. To resolve Colonial’s civil liability for the claims asserted in the Complaint, Colonial will pay a total civil penalty of $34 million to the United States, comply with the injunctive relief requirements in this Consent Decree, and satisfy all other terms of this Consent Decree. -

Force Majeure and Common Law Defenses | a National Survey | Shook, Hardy & Bacon

2020 — Force Majeure SHOOK SHB.COM and Common Law Defenses A National Survey APRIL 2020 — Force Majeure and Common Law Defenses A National Survey Contractual force majeure provisions allocate risk of nonperformance due to events beyond the parties’ control. The occurrence of a force majeure event is akin to an affirmative defense to one’s obligations. This survey identifies issues to consider in light of controlling state law. Then we summarize the relevant law of the 50 states and the District of Columbia. 2020 — Shook Force Majeure Amy Cho Thomas J. Partner Dammrich, II 312.704.7744 Partner Task Force [email protected] 312.704.7721 [email protected] Bill Martucci Lynn Murray Dave Schoenfeld Tom Sullivan Norma Bennett Partner Partner Partner Partner Of Counsel 202.639.5640 312.704.7766 312.704.7723 215.575.3130 713.546.5649 [email protected] [email protected] [email protected] [email protected] [email protected] SHOOK SHB.COM Melissa Sonali Jeanne Janchar Kali Backer Erin Bolden Nott Davis Gunawardhana Of Counsel Associate Associate Of Counsel Of Counsel 816.559.2170 303.285.5303 312.704.7716 617.531.1673 202.639.5643 [email protected] [email protected] [email protected] [email protected] [email protected] John Constance Bria Davis Erika Dirk Emily Pedersen Lischen Reeves Associate Associate Associate Associate Associate 816.559.2017 816.559.0397 312.704.7768 816.559.2662 816.559.2056 [email protected] [email protected] [email protected] [email protected] [email protected] Katelyn Romeo Jon Studer Ever Tápia Matt Williams Associate Associate Vergara Associate 215.575.3114 312.704.7736 Associate 415.544.1932 [email protected] [email protected] 816.559.2946 [email protected] [email protected] ATLANTA | BOSTON | CHICAGO | DENVER | HOUSTON | KANSAS CITY | LONDON | LOS ANGELES MIAMI | ORANGE COUNTY | PHILADELPHIA | SAN FRANCISCO | SEATTLE | TAMPA | WASHINGTON, D.C. -

Coronavirus Insurance Coverage and Claims Guidance

Coronavirus Insurance Coverage and Claims Guidance April 15, 2020 With the exposure of the coronavirus (COVID-19) increasing, organizations are evaluating the potential coverage which may be triggered from their insurance policies. Actual loss situations and a review of individual policy forms will be a crucial step to properly evaluate potential available coverage application. Insurance carriers have the ultimate authority in determining coverage for presented claims. Any suspected COVID-19 related losses should be reported per the policy guidelines. Policyholders should be aware that some policies may require specific time frames from notice of potential claim, such as 48 hours. This document provides factors that will be examined in the event losses related to COVID-19 occur. Coronavirus Insurance Coverage and 2 Lockton Companies Claims Guidance Workers’ compensation Each injured employee situation will be evaluated on its own individual merits. Workers’ compensation insurance covers employees who suffer injury or illness “arising out of or in the course of their employment.” Many factors will need to be considered if presented COVID-19-type claims are work related. These include but are not limited to: • The timing of when the loss occurs: were there reports of previously infected individuals made in this same time period? • The location(s) where the injured worker was present leading up the injury or exposure: was the injured worker within an area where exposure of the virus was present or carried a greater risk? • The activities the injured worker was engaged in leading up to when the loss or exposure took place: was the individual in contact with others or working remotely? • The specific nature of the loss: what further details can be uncovered to provide greater clarity around exposure to the virus as an occupational disease? In most jurisdictions, individuals seeking benefits under workers’ compensation will also need to meet the burden that the coronavirus illness arose out of, or was caused by, conditions “peculiar” to the work.