Consumers Guide to Auto Insurance

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

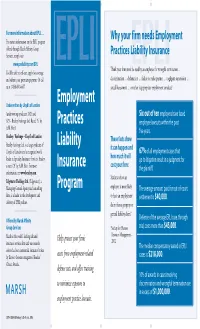

Employment Practices Liability Insurance Program EPLI

B5848_EPLI 2/14/06 2:49 PM Page 1 For more information about EPLI … Why your firm needs Employment For instant information on the EPLI program offered through Marsh Affinity Group Services, simply visit Practices Liability Insurance www.proliablity.com/EPLI Think your firm won’t be sued by an employee for wrongful termination … You’ll be able to self-rate, apply for coverage EPLI EPLI and submit your premium payment. Or call discrimination … defamation … failure to make partner … negligent supervision … us at 1-888-601-6667. sexual harassment … or other inappropriate employment conduct? Underwritten by Lloyd’s of London Employment (underwriting syndicates 2623 and Six out of ten employers have faced 623 – Beazley Furlonge Ltd. Rated “A” by Practices employee lawsuits within the past A.M. Best) five years. Beazley / Furlonge – Lloyd’s of London These facts show Beazley Furlonge Ltd. is a large syndicate of Liability it can happen and Lloyd’s of London and a recognized world 67% of all employment cases that leader in Specialty Insurance Services. Beazley how much it will go to litigation result in a judgment for is rated “A” by A.M. Best. For more Insurance cost your firm: the plaintiff. information, see www.beazley.com. Statistics show an Edgewater Holdings Ltd. (Edgewater), a Managing General Agency and consulting Program employer is more likely The average amount paid for out-of-court firm, is a leader in the development and to have an employment settlement is $40,000. delivery of EPLI policies. claim than a property or general liability claim.* Offered by Marsh Affinity Defense of the average EPLI case, through Group Services *Society for Human trial, costs more than $45,000. -

Maryland Casualty Producer State and General Sections Series 20-07 & 20-08 80 Scored Questions (Plus 10 Unscored)

Maryland Casualty Producer State and General Sections Series 20-07 & 20-08 80 scored questions (plus 10 unscored) Casualty Producer State Section Series 20-08 35 questions- 45-minute time limit 1.0 Insurance Regulation 1.1 Licensing 17% (5 items) Purpose Process (Insurance Article Annotated Code- Sec. 10-115; Sec.10-116; Sec. 10-104) Initial Licensure Qualifications Examination License fee & application Exemptions to Licensure Types of licensees Producers Business entity producers Nonresident producers Temporary Advisers Public insurance adjusters Limited Lines Producer Portable Electronics Insurance Limited Lines license Maintenance and duration (Insurance Article Annotated Code- Sec. 10-116; Sec. 10-117(b)(1)) Reinstatement and renewal Address change Reporting of actions Assumed names Continuing education requirements, exemptions and penalties Disciplinary actions Cease and desist order Hearings Probation, suspension, revocation, refusal to issue or renew Penalties and fines 1.2 State regulation 17% (5 items) Commissioner's general duties and powers (Insurance Article Annotated Code-Sec. 2-205 (a)(2)) State Specific Definitions (Insurance Article Annotated Code- Sec. 10-401; Sec. 27-209; Sec. 27-213; Sec. 10-201; Sec 10-126; Ref: COMAR Sec. 31.08.06.02) Company regulation Certificate of authority Solvency Rates Policy forms Examination of books and records Producer appointments Producer's Contract with Insurer versus Producer's Appointment with Insurer 1 Producer's Individual Appointment versus Business Entity Appointment Maintaining Record of Appointment Notice Termination of producer appointment Producer regulation (Insurance Article Annotated Code-Sec. 27-212(d)) Examination of Books and Records Insurance Information and Privacy Protection Fiduciary Responsibilities (COMAR- Sec. 31.03.03) Bail Bond (COMAR- Sec. -

Tax Risk Insurance: Taking It Captive

taxnotes federal ■ Volume 171, Number 4 April 26, 2021 Tax Risk Insurance: Taking It Captive by Ken Brewer and Albert Liguori Reprinted from Tax Notes Federal, April 26, 2021, p. 549 For more Tax Notes content, please visit www.taxnotes.com. © 2021 Tax Analysts. All rights reserved. Analysts does not claim copyright in any public domain or third party content. TAX PRACTICE tax notes federal Tax Risk Insurance: Taking It Captive by Ken Brewer and Albert Liguori is to explore the U.S. tax implications of that meeting. Behold: captive tax risk insurance!3 In our experiences, the use of tax risk insurance has been most prevalent in the mergers and acquisitions context. But as we mentioned in our last article, we have seen it becoming more common in the context of large corporate groups seeking to manage their global tax risks, regardless of whether they are related to M&A.4 In either context, the use of tax risk insurance lends itself to captive arrangements, for the same reasons that have caused captive arrangements to be desirable for other types of insurance risks. Ken Brewer is a senior adviser and Captive Insurance and the U.S. Tax Implications international tax practitioner with Alvarez & Thereof Marsal Taxand LLC in Miami, and Albert Liguori is a managing director in the firm’s New As an alternative to traditional insurance York office. The authors send special thanks to protection, which is obtained from one or more of Brian Pedersen, managing director at Alvarez & the many underwriters offering that coverage to Marsal Taxand, for his contributions and the public, captive insurance is obtained from a review. -

Auto Insurance and How Those Terms Affect Your Coverage

Arkansas Insurance Department AUTOMOBILE INSURANCE Asa Hutchinson Allen Kerr Governor Commissioner A Message From The Commissioner The Arkansas Insurance Department takes very seriously its mission of “consumer protection.” We believe part of that mission is accomplished when consumers are equipped to make informed decisions. We believe informed decisions are made through the accumulation and evaluation of relevant information. This booklet is designed to provide basic information about automobile insurance. Its purpose is to help you understand terms used in the purchase of auto insurance and how those terms affect your coverage. If you have questions or need additional information, please contact our Consumer Services Division at: Phone: (501) 371-2640; 1-800-852-5494 Fax: (501) 371-2749 Email: [email protected] Web site: www.insurance.arkansas.gov Mission Statement The primary mission of the State Insurance Department shall be consumer protection through insurer insolvency and market conduct regulation, and fraud prosecution and deterrence. 1 Coverages Provided by Automobile Insurance The automobile insurance policy is comprised of several separate types of coverages: COLLISION, COMPREHENSIVE, LIABILITY, PERSONAL INJURY PROTECTION, UNINSURED MOTORIST, UNDERINSURED MOTORIST and other coverages. You are required by law to purchase liability protection only. All others are voluntary unless required by a lienholder. LIABILITY Under Legislation passed in 1987 and 1999, it is unlawful for any person to operate a motor vehicle within this state unless the vehicle is insured with the minimum amount of liability coverage: $25,000 for bodily injury or death of one person in any one accident; $50,000 for bodily injury or death of two or more persons in any one accident and $25,000 for damage to or destruction of the property of others. -

A Maine Miracle 20 Years of Safer Workplaces and Better Workers’ Comp

MEMIC: A Maine Miracle 20 Years of Safer Workplaces and Better Workers’ Comp MEMIC: A Maine Miracle 20 Years of Safer Workplaces and Better Workers’ Comp Susan Dudley Gold Saco, Maine MEMIC: A Maine Miracle 20 Years of Safer Workplaces and Better Workers’ Comp Published by Custom Communications, Inc., 7 Pilgrim Lane, Saco, ME 04072 (207) 286-9295. E-mail: [email protected]. Website: www.desktoppub.com Copyright © 2013 by Maine Employers’ Mutual Insurance Company. This book is protected by copyright. No part of it may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means without the prior written consent of Maine Employers’ Mutual Insurance Company except for brief quotations in articles and reviews. All rights reserved. Printed in the United States of America. Library of Congress Control Number: 2012916342 ISBN-13: 978-1-892168-18-4 Design, Typography, and Setup: Custom Communications, Inc. Photo Credits: Front cover, title page: Michael Bourque, MEMIC; back cover, pp. 96, 131, 146, 149, 151: courtesy of Maine Employers’ Mutual Insurance Company, photographer Earl Dotter; pp. 12, 15, 16, 28, 42, 58: Library of Congress, Prints & Photographs Division; p. 21: © Corbis Corporation; pp. 35, 94: © Brian Peterson; p. 37 (headlines): © Portland Press Herald; p. 37 (image): © PhotoDisc; pp. 47, 71, 83, 125: © Don Johnson; pp. 115, 168: courtesy of Maine Employers’ Mutual Insurance Company, photographer Rene Minnis; p. 126: courtesy of Scott Hannigan; p. 134: © Best’s Review; p. 137: courtesy Maine Audio Visual Services; p. 142: Kevin Brusie; p. 157: courtesy Portland Pirates/Ron Morin; p. -

Attachment II

California Department of Insurance Eight-Hour Mandatory Long-Term Care Course Attachment II Tax Treatment of Long-Term Care Insurance & Expenses Introduction Federal and state tax codes have a purpose beyond raising revenue. Public policy is often served by providing economic relief to taxpayers or motivation for particular behavior. The 1996 Health Insurance Portability and Accountability Act (HIPAA – Public Law 104-191, 110 Stat. 1936, 2054 and 2063) is one of the most far-reaching laws passed by Congress in the latter part of the 20th century. The effects of HIPAA are so complex that federal and state governments as well as the insurance and health care industry continue to grapple with it. By including long-term care insurance in HIPAA, Congress attempted to fulfill a number of different public policy objectives including: (1) classifying long-term care costs as a medical expense thus providing taxpayers with some economic relief; (2) categorizing long-term care insurance as accident and health insurance thereby providing clarity as to the tax treatment of premiums and benefits; and (3) providing the general public an incentive to purchase private long-term care insurance. In addition, as Federal and State governments recognized that long-term care expenses were having a significant financial impact on state Medicaid (Medi-Cal) budgets, Congress was attempting to shift the financial burden of Medicaid to the private sector by providing general tax incentives to purchase long- term care insurance in anticipation of the huge number of baby boomers who may need care in the future. Note: The information provided in this treatise gives a broad description of the tax issues related to long-term care and long-term care insurance. -

Volume 19 Issue 2.Pdf

CONNECTICUT INSURANCE LAW JOURNAL Volume 19, Number 2 Spring 2013 University of Connecticut School of Law Hartford, Connecticut Connecticut Insurance Law Journal (ISSN 1081-9436) is published at least twice a year by the Connecticut Insurance Law Journal Association at the University of Connecticut School of Law. Periodicals postage paid at Hartford, Connecticut. Known office of publication: 55 Elizabeth Street, Hartford, Connecticut 06105-2209. Printing location: Western Newspaper Publishing Company, 537 East Ohio Street, Indianapolis, Indiana 46204. Please visit our website at http://www.insurancejournal.org or see the final page of this issue for subscription and back issue ordering information. Postmaster: Send address changes to Connecticut Insurance Law Journal, 55 Elizabeth Street, Hartford, Connecticut 06105-2209. The Journal welcomes the submission of articles and book reviews. Both text and notes should be double or triple-spaced. Submissions in electronic form are encouraged, and should be in Microsoft™ Word™ version 97 format or higher. Citations should conform to the most recent edition of A UNIFORM SYSTEM OF CITATION, published by the Harvard Law Review Association. It is the policy of the University of Connecticut to prohibit discrimination in education, employment, and in the provision of services on the basis of race, religion, sex, age, marital status, national origin, ancestry, sexual preference, status as a disabled veteran or veteran of the Vietnam Era, physical or mental disability, or record of such impairments, or mental retardation. University policy also prohibits discrimination in employment on the basis of a criminal record that is not related to the position being sought; and supports all state and federal civil rights statutes whether or not specifically cited within this statement. -

Coronavirus Insurance Coverage and Claims Guidance

Coronavirus Insurance Coverage and Claims Guidance April 15, 2020 With the exposure of the coronavirus (COVID-19) increasing, organizations are evaluating the potential coverage which may be triggered from their insurance policies. Actual loss situations and a review of individual policy forms will be a crucial step to properly evaluate potential available coverage application. Insurance carriers have the ultimate authority in determining coverage for presented claims. Any suspected COVID-19 related losses should be reported per the policy guidelines. Policyholders should be aware that some policies may require specific time frames from notice of potential claim, such as 48 hours. This document provides factors that will be examined in the event losses related to COVID-19 occur. Coronavirus Insurance Coverage and 2 Lockton Companies Claims Guidance Workers’ compensation Each injured employee situation will be evaluated on its own individual merits. Workers’ compensation insurance covers employees who suffer injury or illness “arising out of or in the course of their employment.” Many factors will need to be considered if presented COVID-19-type claims are work related. These include but are not limited to: • The timing of when the loss occurs: were there reports of previously infected individuals made in this same time period? • The location(s) where the injured worker was present leading up the injury or exposure: was the injured worker within an area where exposure of the virus was present or carried a greater risk? • The activities the injured worker was engaged in leading up to when the loss or exposure took place: was the individual in contact with others or working remotely? • The specific nature of the loss: what further details can be uncovered to provide greater clarity around exposure to the virus as an occupational disease? In most jurisdictions, individuals seeking benefits under workers’ compensation will also need to meet the burden that the coronavirus illness arose out of, or was caused by, conditions “peculiar” to the work. -

Captive Insurance Companies

Estate Planning – August 2011 CAPTIVE INSURANCE COMPANIES Possibilities and Pitfalls With Captive Insurance Companies Profitable family businesses can use captive insurance companies to manage business risk and shift wealth accumulated in a profitable captive from senior to junior generations thereby avoiding inclusion of those funds in the senior generation's estates. Author: KIMBERLY S. BUNTING, J. SCOT KIRKPATRICK, AND KAREN S. KURTZ, ATTORNEYS KIMBERLY S. BUNTING is a shareholder in Chamberlain, Hrdlicka, White, Williams & Martin LLP's Atlanta, Georgia, office. She practices in the areas of commercial and corporate law, and has significant experience with risk management and captive insurance companies. J. SCOT KIRKPATRICK is also a shareholder in Chamberlain, Hrdlicka's Atlanta office. His practice focuses principally on estate and income tax planning for high net worth individuals and their businesses. KAREN S. KURTZ is an associate in the Tax Section of Chamberlain Hrdlicka's Atlanta office, concentrating in estate and gift tax planning and litigation. A captive insurance company ("Captive") is an insurance company formed by a business owner to insure the risks of related or affiliated businesses. A Captive permits a business to manage its risks while potentially providing substantial benefits to that related business. The premiums received by the Captive are invested and thus not "lost" if not used to pay claims in the same sense that commercial insurance premiums are when paid to an unrelated insurer. This one benefit drives the use of Captives for the family business more than any other. Captives may issue property or casualty insurance coverage against a wide variety of possible liabilities. -

A Cure for the Plaintiff's Ills?

Indiana Law Journal Volume 51 Issue 1 Article 8 Fall 1975 A Cure for the Plaintiff's Ills? Andrew C. Mallor Applegate and Pratt Follow this and additional works at: https://www.repository.law.indiana.edu/ilj Part of the Insurance Law Commons, Medical Jurisprudence Commons, and the Torts Commons Recommended Citation Mallor, Andrew C. (1975) "A Cure for the Plaintiff's Ills?," Indiana Law Journal: Vol. 51 : Iss. 1 , Article 8. Available at: https://www.repository.law.indiana.edu/ilj/vol51/iss1/8 This Symposium is brought to you for free and open access by the Law School Journals at Digital Repository @ Maurer Law. It has been accepted for inclusion in Indiana Law Journal by an authorized editor of Digital Repository @ Maurer Law. For more information, please contact [email protected]. COMMENTARY A Cure for the Plaintiff's Ills? ANDREW C. MALLOR* In recent years negligence lawyers have been castigated as the villains of the malpractice problem.' In 1975, a full page newspaper advertisement was placed by the medical staff of a county hospital soliciting public support for legislation abolishing the contingency fee system, the legal doctrines of informed consent and res ipsa loquitur, and the availability of punitive damages in malpractice actions.2 Re- sponsibility for the malpractice crisis was placed on the plaintiffs' bar and the court system.' In truth, the malpractice problem cannot be resolved by narrowly focusing on the legal system. The malpractice problem is complex and far reaching, and easy solutions simply do not exist. This article will analyze the Indiana Medical Malpractice Act in- sofar as it affects the rights and interests of the plaintiff in a malprac- tice action. -

View This Comprehensive Glossary of Insurance Terms

Thomas Gregory Associates Insurance Agency, Inc. Chris Hawthorne 781-914-1038 Risk Reference Resource 1 Thomas Gregory Associates Insurance Agency, Inc. Chris Hawthorne 781-914-1038 Updated as of: August 21, 2007 -A- ARM – Associate in Risk Management ACRS- Accelerated Cost Recovery System; IRS table of depreciation ADR- See Alternative Dispute Resolution ALAE- See Allocated loss adjustment expense AP- Accounts Payable AR- Accounts Receivable A/T Cost- After Tax Cost Accident – An unplanned event, unexpected & undersigned, which occurs suddenly and at a definite place (occurrence). Act of God – An event arising out of natural causes with no human intervention which could not have been prevented with reasonable care or foresight. Examples are floods, lightning and earthquakes. Active Retention- Planned acceptance of losses by deductibles, deliberate non- insurance, and loss sensitive plans where some, but not all, risk is consciously retained rather than transferred. Actual Cash Value (ACV) – An amount equivalent to the replacement cost of lost or damaged property at the time of the loss, less depreciation. Actuary – A specialist trained in mathematics, statistics, and accounting who is responsible for rate, reserve & dividend calculations and other statistical studies. Additional Insured – A person other than the named insured who is protected under the terms of the contract. Usually additional insureds are added by endorsement or referred to in the wording of the definition of “insured” in the policy itself. Additional Living Expenses Insurance – A contract to reimburse the insured for increased living costs when loss of property forces an insured to maintain temporary residence elsewhere. Adhesion Contract- a contract (usually standardized) offering goods or services on a “take it” or “leave it” basis. -

Effective with UNDERWRITERS at LLOYD's, LONDON Insurance For

Effective with UNDERWRITERS AT LLOYD'S, LONDON Administered by Hiscox Inc. 520 Madison Avenue 32nd Floor, New York, NY 10022 (646) 452-2353 Insurance for General Liability DECLARATIONS This insurance has been placed with an insurer that is not licensed by the state of Michigan. In case of insolvency, payment of claims may not be guaranteed. Broker No.: US 0001488 RT Specialty of Illinois, LLC Policy No.: MPL1934916.18 500 W. Monroe St., 30th Floor Renewal of: MPL1934916.17 Chicago, IL 60661 1. Named Insured: Stateside APM Address: 6445 Citation Dr Ste F Clarkston, MI 48346-2996 2. Policy Period: Inception Date: 03/31/2018 Expiration Date: 03/31/2019 Inception date shown shall be at 12:01 A.M. (Standard Time) to Expiration date shown above at 12:01 A.M. (Standard Time) at the address of the Named Insured. 3. General terms and WCL P0001 CW (09/14) conditions wording: The General terms and conditions apply to this policy in conjunction with the specific wording detailed in each section below. 4. Endorsements: E6015.6 - Lloyd’s Syndicate (3624) Endorsement, E6016.1 - Service of Suit, E6017.2 - Nuclear Incident Exclusion Clause-Liability-Direct (Broad) Endorsement, E6018.2 - Applicable Law Endorsement, E6020.2 - War and Civil War Exclusion Endorsement, E6023.1 - Minimum Earned Premium Endorsement, and E9998.2 - TRIA Not Purchased Endorsement 5. Optional Extension Extended Reporting Period of 12/24/36 months at 75/150/225 percent of the annual premium. Period: 6. Notification of Hiscox Claims claims to: 520 Madison Avenue, 32nd floor New York, NY 10022 Fax: 212-922-9652 Email: [email protected] 7.