What Is Fiduciary Liability Insurance and Why Do You Need It?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

How Many Fiduciary Duties Are There in Corporate Law?

DO NOT DELETE 10/24/2010 5:49 PM HOW MANY FIDUCIARY DUTIES ARE THERE IN CORPORATE LAW? JULIAN VELASCO* ABSTRACT Historically, there existed two main fiduciary duties in corporate law, care and loyalty, and only violations of the duty of loyalty were likely to lead to liability. In the 1980s and 1990s, the Delaware Supreme Court breathed life into the duty of care, created a number of intermediate standards of review, elevated the duty of good faith to equal standing with care and loyalty, and announced a unified test for review of breaches of fiduciary duty. The law, which once seemed so straightforward, suddenly became elaborate and complex. In 2006, in the case of Stone v. Ritter, the Delaware Supreme Court rejected the triadic formulation and declared that good faith was a component of the duty of loyalty. In this and other respects, Delaware seems to be returning to a bifurcated understanding of the law of fiduciary duties. I believe that this is a mistake. This area of law is inherently complex and much too important to be oversimplified. The current academic debate on the issue focuses on whether there should be two duties or three. In this Article, I argue that the question is misleading and irrelevant, but that if it must be asked, the best answer is that there are five duties—one for each paradigm of enforcement. In defending this claim, I explain the true nature of fiduciary duties and provide a robust framework for the discussion, implementation, and development of the law. * Associate Professor of Law, Notre Dame Law School; B.S. -

2013-2014 Sheathing Restitution's Dagger 899 Under the Securities

2013-2014 SHEATHING RESTITUTION’S DAGGER 899 UNDER THE SECURITIES ACT SHEATHING RESTITUTION’S DAGGER UNDER THE SECURITIES ACTS: WHY FEDERAL COURTS ARE POWERLESS TO ORDER DISGORGEMENT IN SEC ENFORCEMENT PROCEEDINGS FRANCESCO A. DELUCA* “Beneath the cloak of restitution lies the dagger to compel the conscious wrongdoer to disgorge his gains.”1 Table of Contents I. First Principles: A Primer on the SEC’s Disgorgement Remedy, Classic Disgorgement, and the Equity Jurisdiction of the Federal Courts ..................................... 903 A. “Disgorgement” in the Securities Context .................. 903 B. Classic Disgorgement .................................................. 904 C. The Equity Jurisdiction of the Federal Courts ............ 907 II. Disgorgement’s History Under the Securities Acts ........... 908 III. An Analysis of Cavanagh ................................................... 911 A. Analysis of Allegedly Analogous Equitable Remedies ..................................................................... 912 B. Analysis of Binding Precedents .................................. 920 C. Analysis of Persuasive Precedents .............................. 926 IV. The SEC’s Disgorgement Remedy Is Not an Equitable Remedy ............................................................................... 930 V. Implications ....................................................................... 931 VI. Conclusion ......................................................................... 933 * Boston University School of Law (J.D. 2014); Roger -

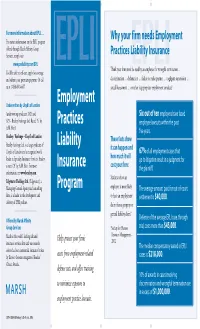

Employment Practices Liability Insurance Program EPLI

B5848_EPLI 2/14/06 2:49 PM Page 1 For more information about EPLI … Why your firm needs Employment For instant information on the EPLI program offered through Marsh Affinity Group Services, simply visit Practices Liability Insurance www.proliablity.com/EPLI Think your firm won’t be sued by an employee for wrongful termination … You’ll be able to self-rate, apply for coverage EPLI EPLI and submit your premium payment. Or call discrimination … defamation … failure to make partner … negligent supervision … us at 1-888-601-6667. sexual harassment … or other inappropriate employment conduct? Underwritten by Lloyd’s of London Employment (underwriting syndicates 2623 and Six out of ten employers have faced 623 – Beazley Furlonge Ltd. Rated “A” by Practices employee lawsuits within the past A.M. Best) five years. Beazley / Furlonge – Lloyd’s of London These facts show Beazley Furlonge Ltd. is a large syndicate of Liability it can happen and Lloyd’s of London and a recognized world 67% of all employment cases that leader in Specialty Insurance Services. Beazley how much it will go to litigation result in a judgment for is rated “A” by A.M. Best. For more Insurance cost your firm: the plaintiff. information, see www.beazley.com. Statistics show an Edgewater Holdings Ltd. (Edgewater), a Managing General Agency and consulting Program employer is more likely The average amount paid for out-of-court firm, is a leader in the development and to have an employment settlement is $40,000. delivery of EPLI policies. claim than a property or general liability claim.* Offered by Marsh Affinity Defense of the average EPLI case, through Group Services *Society for Human trial, costs more than $45,000. -

Fiduciary Law's “Holy Grail”

FIDUCIARY LAW’S “HOLY GRAIL”: RECONCILING THEORY AND PRACTICE IN FIDUCIARY JURISPRUDENCE LEONARD I. ROTMAN∗ INTRODUCTION ............................................................................................... 922 I. FIDUCIARY LAW’S “HOLY GRAIL” ...................................................... 925 A. Contextualizing Fiduciary Law ................................................... 934 B. Defining Fiduciary Law .............................................................. 936 II. CERTAINTY AND FIDUCIARY OBLIGATION .......................................... 945 III. ESTABLISHING FIDUCIARY FUNCTIONALITY ....................................... 950 A. “Spirit and Intent”: Equity, Fiduciary Law, and Lifnim Mishurat Hadin ............................................................................ 952 B. The Function of Fiduciary Law: Sipping from the Fiduciary “Holy Grail” .............................................................. 954 C. Meinhard v. Salmon .................................................................... 961 D. Hodgkinson v. Simms ................................................................. 965 CONCLUSION ................................................................................................... 969 Fiduciary law has experienced tremendous growth over the past few decades. However, its indiscriminate and generally unexplained use, particularly to justify results-oriented decision making, has created a confused and problematic jurisprudence. Fiduciary law was never intended to apply to the garden -

Consumers Guide to Auto Insurance

CONSUMERS GUIDE TO AUTO INSURANCE PRESENTED TO YOU BY THE DEPARTMENT OF BUSINESS REGULATION INSURANCE DIVISION 1511 PONTIAC AVENUE, BLDG 69-2 CRANSTON, RI 02920 TELEPHONE 401-462-9520 www.dbr.ri.gov Elizabeth Kelleher Dwyer Superintendent of Insurance TABLE OF CONTENTS Introduction………………………………………………………………1 Underwriting and Rating………………………………………………...1 What is meant by underwriting and how is it accomplished…………..1 How are rates and premium charges determined in Rhode Island……1 What factors are considered in ratemaking……………………………. 2 What discounts are used in determining final premium cost…………..3 Rhode Island Automobile Insurance Plan…………………..…………..4 Regulation of Rates……………………………………………………….4 The Tort System…………………………………………………………..4 Liability Coverages………………………………………………………..5 Coverages Other Than Liability…………………………………………5 Physical Damage to the Automobile……………………………………..6 Other Optional Coverages………………………………………………..6 The No-Fault System……………….……………………………………..7 Smart Shopping……………………………………………………………7 Shop for True Comparison………………………………………………..8 Consumer Protection Available...…………………………………………8 What to Do if You are in an Automobile Accident………………………9 Your State Insurance Department………………………………….........9 Auto Insurance Buyer’s Worksheet…………………………………….10 Introduction Auto insurance is an expensive purchase for most Americans, and is especially expensive for Rhode Islanders. Yet consumers rarely comparison-shop for auto insurance as they might for other products and services. Auto insurance companies vary substantially both in price and service to policyholders, so it pays to shop around and compare different insurance companies. This guide to buying auto insurance was developed to help you become a more knowledgeable policyholder and to get the combination of price and service best suited to your needs. It provides information on how to shop for coverage and how insurance premiums are determined. You will also find an Auto Insurance Buyer’s Worksheet in the guide to help you compare premium prices among insurers. -

A Comparative Analysis of Corporate Fiduciary Law: Why Delaware Should Look Beyond the United States in Formulating a Standard of Care

COMMENTS HENDRIK F. JORDAAN* A Comparative Analysis of Corporate Fiduciary Law: Why Delaware Should Look Beyond the United States in Formulating a Standard of Care Corporate internationalization has altered the corporate landscape irreversibly. Specifically, international trading in securities and cross-border corporate owner- ship, directorship, and management have increased substantially.' In 1995 multi- national companies invested a record $315 billion outside their own national Note: The American Bar Association grants permission to reproduce this article, or a part thereof, in any not-for-profit publication or handout provided such material acknowledges original publication in this issue of The InternationalLawyer and includes the title of the article and the name of the author. *Hendrik F. Jordaan is a J.D. Candidate (1997) at Southern Methodist University. He is editor-in- chief of Southern Methodist University School of Law Student Editorial Board for The International Lawyer. 1. See generally Richard M. Klapow, Foreign Investment Company Law in the United States: The Need for Change in a Global Securities Market, 14 BROOK. J. INT'L L. 411 (1988) (citing OECD REPORT, THE COMMITTEE ON FINANCIAL MARKETS INTERNATIONAL TRADE IN SERVICES: SECURITIES (Paris, 1987)); Caroline A.A. Greene, International Securities Law Enforcement: Recent Advances in Assistance and Cooperation, 27 VAND. J. TRANSNAT'L L. 635 (1994); Arthur R. Pinto, The Internationalizationof the Hostile Takeover Market: Its Implicationsfor Choice of Law in Corporate and Securities Law, 16 BROOK. J. INT'L L. 55 (1990). This trend to expand corporate activities internationally is driven by the benefits of risk diversification, the enhanced profitability that interna- tional investment frequently offers, and technological improvements and reductions in regulatory constraints. -

Tax Risk Insurance: Taking It Captive

taxnotes federal ■ Volume 171, Number 4 April 26, 2021 Tax Risk Insurance: Taking It Captive by Ken Brewer and Albert Liguori Reprinted from Tax Notes Federal, April 26, 2021, p. 549 For more Tax Notes content, please visit www.taxnotes.com. © 2021 Tax Analysts. All rights reserved. Analysts does not claim copyright in any public domain or third party content. TAX PRACTICE tax notes federal Tax Risk Insurance: Taking It Captive by Ken Brewer and Albert Liguori is to explore the U.S. tax implications of that meeting. Behold: captive tax risk insurance!3 In our experiences, the use of tax risk insurance has been most prevalent in the mergers and acquisitions context. But as we mentioned in our last article, we have seen it becoming more common in the context of large corporate groups seeking to manage their global tax risks, regardless of whether they are related to M&A.4 In either context, the use of tax risk insurance lends itself to captive arrangements, for the same reasons that have caused captive arrangements to be desirable for other types of insurance risks. Ken Brewer is a senior adviser and Captive Insurance and the U.S. Tax Implications international tax practitioner with Alvarez & Thereof Marsal Taxand LLC in Miami, and Albert Liguori is a managing director in the firm’s New As an alternative to traditional insurance York office. The authors send special thanks to protection, which is obtained from one or more of Brian Pedersen, managing director at Alvarez & the many underwriters offering that coverage to Marsal Taxand, for his contributions and the public, captive insurance is obtained from a review. -

Monitoring the Duty to Monitor

Corporate Governance WWW. NYLJ.COM MONDAY, NOVEMBER 28, 2011 Monitoring the Duty to Monitor statements. As a result, the stock prices of Chinese by an actual intent to do harm” or an “intentional BY LOUIS J. BEVILACQUA listed companies have collapsed. Do directors dereliction of duty, [and] a conscious disregard have a duty to monitor and react to trends that for one’s responsibilities.”9 Examples of conduct HE SIGNIFICANT LOSSES suffered by inves- raise obvious concerns that are industry “red amounting to bad faith include “where the fidu- tors during the recent financial crisis have flags,” but not specific to the individual company? ciary intentionally acts with a purpose other than again left many shareholders clamoring to T And if so, what is the appropriate penalty for the that of advancing the best interests of the corpo- find someone responsible. Where were the direc- board’s failure to act? “Sine poena nulla lex.” (“No ration, where the fiduciary acts with the intent tors who were supposed to be watching over the law without punishment.”).3 to violate applicable positive law, or where the company? What did they know? What should they fiduciary intentionally fails to act in the face of have known? Fiduciary Duties Generally a known duty to act, demonstrating a conscious Obviously, directors should not be liable for The duty to monitor arose out of the general disregard for his duties.”10 losses resulting from changes in general economic fiduciary duties of directors. Under Delaware law, Absent a conflict of interest, claims of breaches conditions, but what about the boards of mort- directors have fiduciary duties to the corporation of duty of care by a board are subject to the judicial gage companies and financial institutions that and its stockholders that include the duty of care review standard known as the “business judgment had a business model tied to market risk. -

Auto Insurance and How Those Terms Affect Your Coverage

Arkansas Insurance Department AUTOMOBILE INSURANCE Asa Hutchinson Allen Kerr Governor Commissioner A Message From The Commissioner The Arkansas Insurance Department takes very seriously its mission of “consumer protection.” We believe part of that mission is accomplished when consumers are equipped to make informed decisions. We believe informed decisions are made through the accumulation and evaluation of relevant information. This booklet is designed to provide basic information about automobile insurance. Its purpose is to help you understand terms used in the purchase of auto insurance and how those terms affect your coverage. If you have questions or need additional information, please contact our Consumer Services Division at: Phone: (501) 371-2640; 1-800-852-5494 Fax: (501) 371-2749 Email: [email protected] Web site: www.insurance.arkansas.gov Mission Statement The primary mission of the State Insurance Department shall be consumer protection through insurer insolvency and market conduct regulation, and fraud prosecution and deterrence. 1 Coverages Provided by Automobile Insurance The automobile insurance policy is comprised of several separate types of coverages: COLLISION, COMPREHENSIVE, LIABILITY, PERSONAL INJURY PROTECTION, UNINSURED MOTORIST, UNDERINSURED MOTORIST and other coverages. You are required by law to purchase liability protection only. All others are voluntary unless required by a lienholder. LIABILITY Under Legislation passed in 1987 and 1999, it is unlawful for any person to operate a motor vehicle within this state unless the vehicle is insured with the minimum amount of liability coverage: $25,000 for bodily injury or death of one person in any one accident; $50,000 for bodily injury or death of two or more persons in any one accident and $25,000 for damage to or destruction of the property of others. -

Fiduciary Responsibility Ian Lanoff

Fiduciary Responsibility Ian Lanoff www.groom.com November 7, 2005 Trust Law Evolution • Old English law recognized trusts • Family trusts have existed for centuries • Pension funds emerged in the 1900s • In 1974, ERISA codified trust law applicable to private pension plans 2 Public plans – not subject to ERISA • But ERISA is extremely influential • Public plan laws are modeled after ERISA: – Most impose duties of prudence and loyalty – Many have fiduciary conflict provisions – Many have party in interest rules • Public plans trustees look to ERISA for guidance • ERISA provides a model for best practices 3 Today's Roadmap 1. Who is a fiduciary? 2. The 4 primary fiduciary duties 3. Procedural prudence 4. ETIs 5. Fiduciary misconduct (i.e., conflicts) 6. Co-fiduciary liability 7. Party in interest violations 8. Prohibited transactions under the IRC 9. Plan expenses 10. What can internal auditors do? 4 Who is a fiduciary? 5 Why is it important to know if you are a fiduciary? • Fiduciaries must satisfy the "highest standard of conduct known to law" • Fiduciaries who violate those standards may become personally liable 6 Definition of fiduciary • ERISA has a “functional” definition: – You are a fiduciary if your job involves a “fiduciary function” (regardless of what is in your job description) – Even if your job does not involve a fiduciary function, you are a fiduciary if take on a fiduciary function (i.e., act outside your job) – Ministerial acts are not fiduciary functions • Applicable state law may be different 7 What is a fiduciary function? -

Fiduciary Duties and Potential Liabilities of Directors and Officers of Financially Distressed Corporations

LATHAM & WATKINS ATTORNEYS AT LAW 53rd AT THIRD, SUITE I000 885 THIRD AVENUE NEW YORK, NEW YORK I0022-4802 TELEPHONE (2I2) 906-I200 FAX (2I2) 75I-4864 Fiduciary Duties and Potential Liabilities of Directors and Officers of Financially Distressed Corporations This memorandum provides a general review of the duties and potential liabilities of directors and officers of financially distressed corporations.1 First, this memorandum discusses generally the fiduciary duties of directors in the context of financially healthy corporations and proceeds to describe how these duties shift in the context of financially distressed corporations. This memorandum then discusses briefly the duties and liabilities of non-director officers. Finally, the memorandum identifies certain statutory and other liabilities of both directors and officers that may be of particular relevance to officers and directors of financially distressed corporations. We have focused our discussion primarily on Delaware law because of the persuasiveness of Delaware court decisions in the area of corporate law. In our review, we have sought to identify the principal types of duties and liabilities that might be implicated when a corporation is facing financial difficulties. We have not attempted to conduct a comprehensive survey of every possible statutory or common law duty or liability that could conceivably exist. I. Summary A. Directors of solvent corporations have two basic “fiduciary” duties, the duty of care and the duty of loyalty, owed to the corporation itself and the shareholders. 1. Directors must act in good faith, with the care of a prudent person, and in the best interest of the corporation. 2. Directors must refrain from self-dealing, usurping corporate opportunities and receiving improper personal benefits. -

Coronavirus Insurance Coverage and Claims Guidance

Coronavirus Insurance Coverage and Claims Guidance April 15, 2020 With the exposure of the coronavirus (COVID-19) increasing, organizations are evaluating the potential coverage which may be triggered from their insurance policies. Actual loss situations and a review of individual policy forms will be a crucial step to properly evaluate potential available coverage application. Insurance carriers have the ultimate authority in determining coverage for presented claims. Any suspected COVID-19 related losses should be reported per the policy guidelines. Policyholders should be aware that some policies may require specific time frames from notice of potential claim, such as 48 hours. This document provides factors that will be examined in the event losses related to COVID-19 occur. Coronavirus Insurance Coverage and 2 Lockton Companies Claims Guidance Workers’ compensation Each injured employee situation will be evaluated on its own individual merits. Workers’ compensation insurance covers employees who suffer injury or illness “arising out of or in the course of their employment.” Many factors will need to be considered if presented COVID-19-type claims are work related. These include but are not limited to: • The timing of when the loss occurs: were there reports of previously infected individuals made in this same time period? • The location(s) where the injured worker was present leading up the injury or exposure: was the injured worker within an area where exposure of the virus was present or carried a greater risk? • The activities the injured worker was engaged in leading up to when the loss or exposure took place: was the individual in contact with others or working remotely? • The specific nature of the loss: what further details can be uncovered to provide greater clarity around exposure to the virus as an occupational disease? In most jurisdictions, individuals seeking benefits under workers’ compensation will also need to meet the burden that the coronavirus illness arose out of, or was caused by, conditions “peculiar” to the work.