IBEF Presentataion

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sustainable Development Report 2017

I II X Sustainability The essence of our existence. Organisation Profile GRI-102, SDG-8, 9 Ambuja Cements Limited (ACL), started in 1986, is India’s leading Cement Company. Ambuja Cement is the premier cement brand in India for Ordinary Portland Cement (OPC), and low carbon products such as Pozzolana Portland Cement (PPC) and Pozzolana Composite Cement (PCC) having significant footprints across the Western, Eastern and Northern markets of India. Our customers range from Individual House Builders (IHBs) to governments to global construction firms. The total cement production for 2017 was 22.98 MT against the annual capacity of 29.65 million tonnes per annum (MTPA). Our employee strength stood at 5,328. In line with the 2030 SDG targets, Ambuja aims to achieve higher level of economic productivity through diversification, technological upgradation and innovation, with a focus on value-added products and services with sustainable human capital deployment. Nature of Company Ownership Ambuja Cements Limited (ACL) is a public limited company listed on the Bombay Stock Exchange Limited and National Stock Exchange of India Limited. The GDRs issued by the Company are listed on the Luxembourg Stock Exchange. LafargeHolcim Limited, Switzerland, is the majority shareholder. For the detailed shareholding pattern, please see the Annual Report on our website: www.ambujacement.com . Integrated Cement Plants Bulk Cement Terminals 1. Ambujanagar, Taluka Kodinar, District Gir 1. Muldwarka, District Gir Somnath, Gujarat; Somnath, Gujarat; 2. Panvel, District Raigad, Maharashtra; 2. Darlaghat, District Solan, Himachal Pradesh; 3. Kochi, Kerala; 3. Maratha Cement Works, District Chandrapur, 4. Surat, Gujarat; Maharashtra; 5. Mangalore, Karnataka. 4. -

Successful Auctions So Far

Successful Auctions so far: S State Name of the Block Mineral Date of ML / Area Reserves (in Final Preferred Bidder No auction CL (in MT) Bid (in Ha) %) 1 Andhra Gudipadu block Limestone 08.06.2016 ML 40.82 26.66 8.12 Penna Cements Pradesh 2 Andhra Erragudi-Hussainapuram Limestone 26.09.2017 ML 131.57 9.03 10.6 Sree Jayajothi Pradesh –Yanakandla Cements Pvt Ltd 3 Andhra Nandavaram–Venkatapuram Limestone 26.09.2017 ML 24.739 1.66 10.7 Sree Jayajothi Pradesh Cements Pvt Ltd 4 Andhra Chigargunta – Bisanatham Gold 27.07.2018 ML 262.01 2.22 38.25 NMDC Limited Pradesh 5 Andhra Chintalayapalle- Limestone 28.11.2018 ML 417.51 92.24 13.4 Adani Cementation Pradesh Abdullapuram-Korumanipalli Ltd (CAK) 6 Andhra Gorlagutta Limestone 27.05.2021 ML 181.03 61.14 7.25 M/s. Sree Jayajothi Pradesh Cements Private Limited 7 Chhattisgarh Karhi-Chandi Limestone 18.02.2016 ML 242.13 155 58.95 Shree Cement 8 Chhattisgarh Kesla Limestone 19.02.2016 ML 108 67 10.15 Century Cement 9 Chhattisgarh Baghmara Gold 26.02.2016 CL 474.3 2.7 12.55 Vedanta Ltd 10 Chhattisgarh Kesla II Limestone 01.05.2017 ML 357.07 215 96.15 Dalmia (bharat) cement 11 Chhattisgarh Guma Limestone block, Palari Limestone 12.03.2018 ML 249.03 124 138.25 Ultratech Cement 12 Chhattisgarh Mohra (Block A), Limestone 08.09.2020 ML 127.05 56.847 5.45 State Govt to inform Balodabazar, Balodabazar- Bhatapara 13 Chhattisgarh Parsabhadar, Balodabazar, Limestone 08.09.2020 ML 28.461 9.614 34.15 State Govt to inform Balodabazar-Bhatapara 14 Gujarat Mudhvay Sub- block B Limestone 25.05.2017 ML 233.5 301.5 -

Ambuja Cements ( AMBCEM)

Ambuja Cements ( AMBCEM) CMP: | 407 Target: | 490 (20%) Target Period: 12 months BUY July 26, 2021 Beats estimates with strong margins… About the stock: Ambuja Cement (a Holcim group company) is a large cement player with capacity of over 29.7 MT spread across North-Central (40%), West (~35%) and East (~25%) India. It has a large marketing set-up, pan-India presence and strong operational linkages with ACC. Particulars The upcoming new capacity at Rajasthan will enhance its cement capacity by Particular Amount 1.8 MT to 31.5 MT and clinker capacity by 3.0 MT Market cap | 80816 crore Debt (CY20) | 72 crore Result Update Result In the long run, the company plans to reach over ~50 MT capacity through Cash & Invest (CY20) | 686 crore significant de-bottlenecking and setting up of satellite grinding units EV | 80202 crore 52 week H/L | 410 / 196 Equity capital | 397.1 crore Q1FY22 Results: Ambuja Cement reported 149 bps QoQ expansion in margins Face value | 2 leading to better profitability despite cost pressure. Shareholding pattern Clocked revenue of | 3,371 crore, down 6.9% QoQ led by sales volumes de- (in %) Sep-20 Dec-20 Mar-21 Jun-21 growth of 11.3% to 6.4 MT. On a YoY basis, revenues were up 53.2% Promoter 63.3 63.3 63.3 63.3 EBITDA/t was up 10.8% QoQ to | 1,495/t (vs. last quarter EBITDA/t of FII 16.8 18.1 17.8 17.7 | 1,349/t). EBITDA margin was at 28.5%, up 149 bps QoQ, 112 bps YoY DII 13.3 11.5 12.4 12.5 Others 6.6 7.1 6.6 6.5 Reported PAT was at | 723.1 crore, up 59.5% YoY, 8.8% QoQ vs. -

Uti Nifty Next 50 Index Fund

C MYK Index Fund UTI NIFTY NEXT 50 INDEX FUND Investment Objective Portfolio as on October 31, 2020 The investment objective of the scheme is to provide returns that, before expenses, closely correspond to the total returns of the securities as represented by the underlying index, subject to Equity % of NAV tracking error. Adani Green Energy Ltd. 4.41 However there is no guarantee or assurance that the investment objective of the scheme will be Avenue Supermarts Ltd. 4.39 achieved. Tata Consumer Products Ltd. 3.89 Dabur India Ltd. 3.81 Snapshot ICICI Lombard General Insurance Co Ltd. 3.55 Fund Manager - (Managing the scheme since July-2018) Info-Edge (India) Ltd. 3.54 Mr. Sharwan Kumar Goyal, CFA, MMS Godrej Consumer Products Ltd. 3.31 Pidlite Industries Ltd. 3.15 Market Capitalisation (%) Date of inception/allotment: Lupin Ltd. 2.87 28th June, 2018 Large Mid Small Aurobindo Pharma Ltd. 2.86 Fund size monthly average: ` 669.54 Crore Colgate Palmolive India Ltd. 2.66 Closing AUM: ` 680.21 Crore Fund 96 4 0 Bandhan Bank Ltd. 2.58 No. of Unit Holders : 51,072 Ambuja Cements Ltd. 2.51 Minimum Investment Amount : ` 5000/- Marico Ltd. 2.42 Subsequent minimum investment under a folio is Havells India Ltd. 2.40 Rs.1,000/- and in multiples of Rs. 1/- thereafter with no upper limit. Biocon Ltd. 2.36 Petronet Lng Ltd. 2.28 NAV (Regular) per unit as on October 31, 2020 Bharti Infratel Ltd. 2.08 Growth Option: ` 9.75 ICICI Prudential Life Insurance Company Ltd. 2.06 High/Low NAV in the month : Growth option ` 9.80, ` 9.60 Berger Paints India Ltd. -

Inner 9 Flexicap Fund

Modera erate tely Mod High to e H w at ig o er h L d o M V e r y w H Tata Flexi Cap Fund o i L g (An open ended dynamic equity scheme investing across large cap, mid cap, small cap stocks.) h Riskometer Investors understand that their principal As on 31st July 2021 PORTFOLIO will be at Very High Risk INVESTMENT STYLE Company name No. of Market Value % of Company name No. of Market Value % of Primarily focuses on investing in equity and equity related Shares Rs. Lakhs Assets Shares Rs. Lakhs Assets instruments of well researched companies across market Equity & Equity Related Total 185889.49 93.44 Leisure Services capitalization. Auto Jubilant Foodworks Ltd. 115000 4341.42 2.18 INVESTMENT OBJECTIVE Eicher Motors Ltd. 102000 2580.86 1.30 Easy Trip Planners Ltd. 500000 2045.50 1.03 The investment objective of the Scheme is to generate capital Auto Ancillaries Pesticides appreciation over medium to long term. However, there is no MRF Ltd. 4750 3795.60 1.91 Astec Lifesciences Ltd. 173000 2401.59 1.21 assurance or guarantee that the investment objective of the Scheme will be achieved. The scheme does not assure or guarantee any Banks Bayer Cropscience Ltd. 34921 2017.88 1.01 returns. ICICI Bank Ltd. 2200000 15015.00 7.55 Petroleum Products DATE OF ALLOTMENT HDFC Bank Ltd. 560000 7988.12 4.02 Reliance Industries Ltd. 565000 11499.45 5.78 September 06,2018 Axis Bank Ltd. 761500 5398.27 2.71 Pharmaceuticals Kotak Mahindra Bank Ltd. 225000 3723.30 1.87 Dr Reddys Laboratories Ltd. -

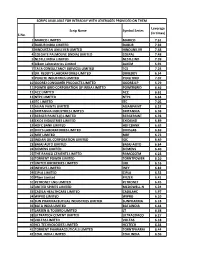

S.No. Scrip Name Symbol Series Leverage (In Times) 1 MARICO

SCRIPS AVAILABLE FOR INTRADAY WITH LEVERAGES PROVIDED ON THEM Leverage Scrip Name Symbol Series (in times) S.No. 1 MARICO LIMITED MARICO 7.61 2 DABUR INDIA LIMITED DABUR 7.92 3 HINDUSTAN UNILEVER LIMITED HINDUNILVR 7.48 4 COLGATE PALMOLIVE (INDIA) LIMITED COLPAL 7.48 5 NESTLE INDIA LIMITED NESTLEIND 7.39 6 Alkem Laboratories Limited ALKEM 6.91 7 TATA CONSULTANCY SERVICES LIMITED TCS 7.24 8 DR. REDDY'S LABORATORIES LIMITED DRREDDY 6.54 9 PIDILITE INDUSTRIES LIMITED PIDILITIND 7.07 10 GODREJ CONSUMER PRODUCTS LIMITED GODREJCP 5.79 11 POWER GRID CORPORATION OF INDIA LIMITED POWERGRID 6.46 12 ACC LIMITED ACC 6.61 13 NTPC LIMITED NTPC 6.64 14 ITC LIMITED ITC 7.05 15 ASIAN PAINTS LIMITED ASIANPAINT 6.52 16 BRITANNIA INDUSTRIES LIMITED BRITANNIA 6.98 17 BERGER PAINTS (I) LIMITED BERGEPAINT 6.78 18 EXIDE INDUSTRIES LIMITED EXIDEIND 6.89 19 HDFC BANK LIMITED HDFCBANK 6.63 20 DIVI'S LABORATORIES LIMITED DIVISLAB 6.69 21 MRF LIMITED MRF 6.73 22 INDIAN OIL CORPORATION LIMITED IOC 6.49 23 BAJAJ AUTO LIMITED BAJAJ-AUTO 6.64 24 SIEMENS LIMITED SIEMENS 6.40 25 THE RAMCO CEMENTS LIMITED RAMCOCEM 6.23 26 TORRENT POWER LIMITED TORNTPOWER 6.10 27 UNITED BREWERIES LIMITED UBL 6.16 28 INFOSYS LIMITED INFY 6.82 29 CIPLA LIMITED CIPLA 6.52 30 Pfizer Limited PFIZER 6.41 31 PETRONET LNG LIMITED PETRONET 6.45 32 UNITED SPIRITS LIMITED MCDOWELL-N 6.24 33 CADILA HEALTHCARE LIMITED CADILAHC 5.97 34 WIPRO LIMITED WIPRO 6.10 35 SUN PHARMACEUTICAL INDUSTRIES LIMITED SUNPHARMA 6.18 36 BATA INDIA LIMITED BATAINDIA 6.44 37 LARSEN & TOUBRO LIMITED LT 6.38 38 ULTRATECH CEMENT -

Loan Against Securities – Approved Single Scrip

Loan against securities – Approved single scrip Security ISIN Code Scrip Name Type Margin INE769A01020 AARTI INDUSTRIES Single Scrip 50 INE012A01025 ACC LIMITED Single Scrip 50 INE079A01024 AMBUJA CEMENTS LTD Single Scrip 50 INE437A01024 APOLLO HOSPITALS ENTERPRISE LTD Single Scrip 50 INE208A01029 ASHOK LEYLAND LTD Single Scrip 50 INE021A01026 ASIAN PAINTS LTD Single Scrip 50 INE406A01037 AUROBINDO PHARMA LTD Single Scrip 50 INE192R01011 AVENUE SUPERMARTS Single Scrip 50 INE917I01010 BAJAJ AUTO LTD Single Scrip 50 INE296A01024 BAJAJ FINANCE LTD Single Scrip 50 INE028A01039 BANK OF BARODA Single Scrip 50 INE084A01016 BANK OF INDIA Single Scrip 50 INE463A01038 BERGER PAINTS INDIA LTD Single Scrip 50 INE029A01011 BHARAT PETROLEUM CORPORATION LTD Single Scrip 50 INE323A01026 BOSCH LTD Single Scrip 50 INE216A01030 BRITANNIA INDUSTRIES LIMITED Single Scrip 50 INE010B01027 CADILA HEALTHCARE LTD Single Scrip 50 INE476A01014 CANARA BANK Single Scrip 50 INE172A01027 CASTROL INDIA LTD Single Scrip 50 INE059A01026 CIPLA LTD Single Scrip 50 INE522F01014 COAL INDIA LTD Single Scrip 50 INE259A01022 COLGATE-PALMOLIVE (INDIA) LTD Single Scrip 50 INE016A01026 DABUR INDIA LTD Single Scrip 50 INE361B01024 DIVIS LABORATORIES LTD Single Scrip 50 INE089A01023 DRREDDYS LABORATORIES LTD Single Scrip 50 INE066A01021 EICHER MOTORS LIMITED Single Scrip 50 INE302A01020 EXIDE INDUSTRIES LTD Single Scrip 50 INE129A01019 GAIL (INDIA) LTD Single Scrip 50 INE176B01034 HAVELLS INDIA LTD Single Scrip 50 INE860A01027 HCL TECHNOLOGIES LTD Single Scrip 50 INE040A01034 HDFC -

Momentum Pick

Momentum Picks Open Recommendations New recommendations Gladiator Stocks Date Scrip I-Direct Code Action Initiation Range Target Stoploss Duration 1-Oct-21 Nifty Nifty Sell 17520-17545 17482/17430 17583.00 Intraday Scrip Action 1-Oct-21 ONGC ONGC Buy 142.50-143.00 144.25/145.70 141.20 Intraday Hindalco Buy PICK MOMENTUM 1-Oct-21 UPL UPL Sell 707.00-708.00 700.60/693.80 714.60 Intraday Bata India Buy 30-Sep-21 Trent TRENT Buy 1010-1025 1125 948.00 30 Days HDFC Buy 30-Sep-21 Dhampur Sugar DHASUG Buy 290-294 312 282.00 07 Days Duration: 3 Months Click here to know more… Open recommendations Date Scrip I-Direct Code Action Initiation Range Target Stoploss Duration 29-Sep-21 SJVN SJVLIM Buy 28.3-29 31.50 27.00 14 Days 29-Sep-21 National Aluminium NATALU Buy 92-94 101.00 86.50 07 Days Intraday recommendations are for current month futures. Positional recommendations are in cash segment Retail Equity Research Retail – October 1, 2021 For Instant stock ideas: SUBSCRIBE to mobile notification on ICICIdirect Mobile app… Research Analysts Securities ICICI Dharmesh Shah Nitin Kunte, CMT Ninad Tamhanekar, CMT [email protected] [email protected] [email protected] Pabitro Mukherjee Vinayak Parmar [email protected] [email protected] NSE (Nifty): 17618 Technical Outlook NSE Nifty Daily Candlestick Chart Domestic Indices Day that was… Open High Low Close Indices Close 1 Day Chg % Chg Equity benchmarks concluded the monthly expiry session on a subdued note tracking mixed global cues. -

Annexure 1B 18416

Annexure 1 B List of taxpayers allotted to State having turnover of more than or equal to 1.5 Crore Sl.No Taxpayers Name GSTIN 1 BROTHERS OF ST.GABRIEL EDUCATION SOCIETY 36AAAAB0175C1ZE 2 BALAJI BEEDI PRODUCERS PRODUCTIVE INDUSTRIAL COOPERATIVE SOCIETY LIMITED 36AAAAB7475M1ZC 3 CENTRAL POWER RESEARCH INSTITUTE 36AAAAC0268P1ZK 4 CO OPERATIVE ELECTRIC SUPPLY SOCIETY LTD 36AAAAC0346G1Z8 5 CENTRE FOR MATERIALS FOR ELECTRONIC TECHNOLOGY 36AAAAC0801E1ZK 6 CYBER SPAZIO OWNERS WELFARE ASSOCIATION 36AAAAC5706G1Z2 7 DHANALAXMI DHANYA VITHANA RAITHU PARASPARA SAHAKARA PARIMITHA SANGHAM 36AAAAD2220N1ZZ 8 DSRB ASSOCIATES 36AAAAD7272Q1Z7 9 D S R EDUCATIONAL SOCIETY 36AAAAD7497D1ZN 10 DIRECTOR SAINIK WELFARE 36AAAAD9115E1Z2 11 GIRIJAN PRIMARY COOPE MARKETING SOCIETY LIMITED ADILABAD 36AAAAG4299E1ZO 12 GIRIJAN PRIMARY CO OP MARKETING SOCIETY LTD UTNOOR 36AAAAG4426D1Z5 13 GIRIJANA PRIMARY CO-OPERATIVE MARKETING SOCIETY LIMITED VENKATAPURAM 36AAAAG5461E1ZY 14 GANGA HITECH CITY 2 SOCIETY 36AAAAG6290R1Z2 15 GSK - VISHWA (JV) 36AAAAG8669E1ZI 16 HASSAN CO OPERATIVE MILK PRODUCERS SOCIETIES UNION LTD 36AAAAH0229B1ZF 17 HCC SEW MEIL JOINT VENTURE 36AAAAH3286Q1Z5 18 INDIAN FARMERS FERTILISER COOPERATIVE LIMITED 36AAAAI0050M1ZW 19 INDU FORTUNE FIELDS GARDENIA APARTMENT OWNERS ASSOCIATION 36AAAAI4338L1ZJ 20 INDUR INTIDEEPAM MUTUAL AIDED CO-OP THRIFT/CREDIT SOC FEDERATION LIMITED 36AAAAI5080P1ZA 21 INSURANCE INFORMATION BUREAU OF INDIA 36AAAAI6771M1Z8 22 INSTITUTE OF DEFENCE SCIENTISTS AND TECHNOLOGISTS 36AAAAI7233A1Z6 23 KARNATAKA CO-OPERATIVE MILK PRODUCER\S FEDERATION -

NSE Symbol NSE 6 Month Avg Total Market

Average Market Cap of 200 listed companies on BSE & NSE for the six months ended 30 June 2021 BSE 6 month Avg NSE 6 month Avg Average of BSE and NSE 6 Total Market Cap Total Market Cap month Avg Total Market Cap S.No. Company Name ISIN BSE SYMBOL (Rs. In Crs.) NSE Symbol (Rs. In Crs.) (Rs. in Crs.) 1 Reliance Industries Ltd INE002A01018 RELIANCE 1338017.01 RELIANCE 1355067.509 1346542.26 Tata Consultancy Services 2 Ltd. INE467B01029 TCS 1169783.56 TCS 1173068.166 1171425.86 3 HDFC Bank Ltd. INE040A01034 HDFCBANK 819037.95 HDFCBANK 818713.671 818875.81 4 Infosys Ltd INE009A01021 INFY 579784.19 INFY 579697.3885 579740.79 5 Hindustan Unilever Ltd., INE030A01027 HINDUNILVR 549336.78 HINDUNILVR 549358.908 549347.84 Housing Development 6 Finance Corp.Lt INE001A01036 HDFC 462288.58 HDFC 461373.1089 461830.84 7 ICICI Bank Ltd. INE090A01021 ICICIBANK 416645.51 ICICIBANK 416389.0234 416517.27 8 Kotak Mahindra Bank Ltd. INE237A01028 KOTAKBANK 361640.52 KOTAKBANK 361438.6361 361539.58 9 State Bank Of India, INE062A01020 SBIN 329767.32 SBIN 329789.268 329778.29 10 Bajaj Finance Limited INE296A01024 BAJFINANCE 324996.53 BAJFINANCE 324843.5005 324920.02 11 Bharti Airtel Ltd. INE397D01024 BHARTIARTL 299981.36 BHARTIARTL 299955.7729 299968.57 12 HCL Technologies Ltd INE860A01027 HCLTECH 261400.46 HCLTECH 261392.0109 261396.24 13 Wipro Ltd., INE075A01022 WIPRO 258617.45 WIPRO 261102.3994 259859.92 14 ITC Ltd INE154A01025 ITC 259423.16 ITC 259396.0648 259409.61 15 Asian Paints Ltd. INE021A01026 ASIANPAINT 253487.28 ASIANPAINT 253454.4536 253470.87 16 AXIS Bank Ltd. -

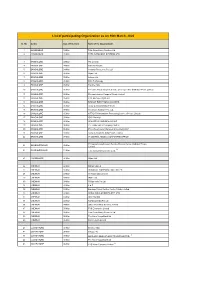

List of Participating Organization As on 16Th March, 2020

List of participating Organization as on 16th March, 2020 Sl. No Centre Date of Interview Name of the Organizations 1 AHMEDABAD 04-Mar Tata Consultancy Services Ltd. 2 AHMEDABAD 05-Mar TATA AUTOCOMP SYSTEMS LTD 3 BANGALORE 04-Mar ITC Limited 4 BANGALORE 04-Mar Bank Of Baroda 5 BANGALORE 04-Mar Vedanta Resources Pvt Ltd 6 BANGALORE 05-Mar Wipro Ltd. 7 BANGALORE 05-Mar Infosys Ltd. 8 BANGALORE 05-Mar DXC Technology 9 BANGALORE 05-Mar Deloitte India 10 BANGALORE 05-Mar PricewaterhouseCoopers Service Delivery Center (Kolkata) Private Limited 11 BANGALORE 05-Mar Pricewaterhouse Coopers Private Limited 12 BANGALORE 05-Mar Tata Advanced Systems 13 BANGALORE 05-Mar BHARAT ELECTRONICS LIMITED 14 BANGALORE 05-Mar Avery Dennison(India) Pvt Ltd 15 BANGALORE 05-Mar Accenture Solutions Pvt. Ltd. 16 BANGALORE 05-Mar NTT DATA Information Processing Services Private Limited 17 BANGALORE 05-Mar ICICI Bank ltd 18 BANGALORE 05-Mar WALKER CHANDIOK & CO LLP 19 BANGALORE 06-Mar The Indian Hotels Company Limited 20 BANGALORE 06-Mar Price Waterhouse Chartered Accountants LLP 21 BANGALORE 07-Mar Consero Solutions India Private Limited, 22 BANGALORE 07-Mar ITI LIMITED, REGD & CORPORATE OFFICE PricewaterhouseCoopers Service Delivery Center (Kolkata) Private 23 BHUBANESHWAR 30-Mar Limited 24 BHUBANESHWAR 31-Mar Tata Consultancy Services Ltd. * 25 CHANDIGARH 30-Mar Wipro Ltd. 26 CHENNAI 02-Mar ONGC Limited 27 CHENNAI 02-Mar INDIAN OIL CORPORATION LIMITED 28 CHENNAI 03-Mar Air Asia(India) Limited 29 CHENNAI 03-Mar Wipro Ltd. 30 CHENNAI 03-Mar Philips India Pvt Ltd 31 CHENNAI 03-Mar L & T 32 CHENNAI 03-Mar Barclays Global Service Centre Private Limited 33 CHENNAI 03-Mar SHELL INDIA MARKETS PVT. -

Inner 25 Resources & Energy Fund

Modera erate tely Mod High to H w te ig o ra h L de o M V e r y w H Tata Resources & Energy Fund o i L g (An open ended equity scheme investing in Resources and Energy Sector) h Riskometer Investors understand that their principal As on 30th April 2021 PORTFOLIO will be at Very High Risk INVESTMENT STYLE Company name No. of Market Value % of Company name No. of Market Value % of Primarily focuses on investment in at least 80% of its net Shares Rs. Lakhs Assets Shares Rs. Lakhs Assets assets in equity/equity related instruments of the companies in the Resources & Energy sectors in India. Equity & Equity Related Total 8050.68 99.20 Vedanta Ltd. 170000 437.33 5.39 Cement National Aluminium Co. Ltd. 510000 329.72 4.06 INVESTMENT OBJECTIVE Ultratech Cement Ltd. 7500 470.92 5.80 Pesticides The investment objective of the scheme is to provide long term capital appreciation by investing atleast 80% Grasim Industries Ltd. 28500 399.50 4.92 Upl Ltd. 35000 212.42 2.62 of it’s net assets in equity/equity related instruments of the companies in the Resources& Energy sectors in Ambuja Cements Ltd. 75000 231.79 2.86 Bayer Cropscience Ltd. 3000 160.41 1.98 India.However, there is no assurance or guarantee that ACC Ltd. 12000 225.93 2.78 Pi Industries Ltd. 3800 95.44 1.18 the investment objective of the Scheme will be achieved.The Scheme does not assure or guarantee any Heidelberg Cement India Ltd.