Acquisition of the Defense Support Program Satellites

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Gallery of USAF Weapons Note: Inventory Numbers Are Total Active Inventory figures As of Sept

Gallery of USAF Weapons Note: Inventory numbers are total active inventory figures as of Sept. 30, 2014. By Aaron M. U. Church, Associate Editor I 2015 USAF Almanac BOMBER AIRCRAFT flight controls actuate trailing edge surfaces that combine aileron, elevator, and rudder functions. New EHF satcom and high-speed computer upgrade B-1 Lancer recently entered full production. Both are part of the Defensive Management Brief: A long-range bomber capable of penetrating enemy defenses and System-Modernization (DMS-M). Efforts are underway to develop a new VLF delivering the largest weapon load of any aircraft in the inventory. receiver for alternative comms. Weapons integration includes the improved COMMENTARY GBU-57 Massive Ordnance Penetrator and JASSM-ER and future weapons The B-1A was initially proposed as replacement for the B-52, and four pro- such as GBU-53 SDB II, GBU-56 Laser JDAM, JDAM-5000, and LRSO. Flex- totypes were developed and tested in 1970s before program cancellation in ible Strike Package mods will feed GPS data to the weapons bays to allow 1977. The program was revived in 1981 as B-1B. The vastly upgraded aircraft weapons to be guided before release, to thwart jamming. It also will move added 74,000 lb of usable payload, improved radar, and reduced radar cross stores management to a new integrated processor. Phase 2 will allow nuclear section, but cut maximum speed to Mach 1.2. The B-1B first saw combat in and conventional weapons to be carried simultaneously to increase flexibility. Iraq during Desert Fox in December 1998. -

Program Acquisition Cost by Weapon System Major Weapon Systems OVERVIEW

The estimated cost of this report or study for the Department of Defense is approximately $32,000 for the 2017 Fiscal Year. This includes $13,000 in expenses and $19,000 in DoD labor. Generated on 2017May03 RefID: E-7DE12B0 FY 2018 Program Acquisition Cost by Weapon System Major Weapon Systems OVERVIEW The combined capabilities and performance of United States (U.S.) weapon systems are unmatched throughout the world, ensuring that U.S. military forces have the advantage over any adversary. The Fiscal Year (FY) 2018 acquisition funding request for the Department of Defense (DoD) budget totals $208.6 billion, which includes base funding and Overseas Contingency Operations (OCO) funding; $125.2 billion for Procurement funded programs and $83.3 billion for Research, Development, Test, and Evaluation (RDT&E) funded programs. Of the $208.6 billion, $94.9 billion is for programs that have been designated as Major Defense Acquisition Programs (MDAPs). This book focuses on all funding for the key MDAP programs. To simplify the display of the various weapon systems, this book is organized by the following mission area categories: Mission Area Categories • Aircraft & Related Systems • Missiles and Munitions • Command, Control, Communications, • Mission Support Activities Computers, and Intelligence (C4I) Systems • RDT&E Science & Technology • Ground Systems • Shipbuilding and Maritime Systems • Missile Defense Programs • Space Based Systems FY 2018 Modernization – Total: $208.6 Billion ($ in Billions) Space Based Aircraft & Systems Related $9.8 -

IMTEC-89-53 Military Space Operations: Use of Mobile Ground

. -. ,(. ,. .“” ,Y .,, . -- II, ./, .I i /, . % . ,L. United States Gdneral Accounting Off& Report to the Honorable &.A0 John P. Murtha, Chairman, Subcommittee on Defense, Committee on Appropriations, House of Representatives July 1989 MILITARY SPACE ’ OPERATIONS Use of Mobile Ground Stations in Satellite Control GAO/IMTEC439-63 United States General Accounting Office GAO Washington, D.C. 20548 Information Management and Technology Division B-224148 July 3, 1989 The Honorable John P. Murtha Chairman, Subcommittee on Defense Committee on Appropriations House of Representatives Dear Mr. Chairman: In your January 9, 1989, letter and in subsequent discussions with your office, you asked us to determine (1) how mobile ground stations fit into the Air Force’s overall satellite control architecture, (2) how many sta- tions exist and are planned, (3) what they cost by program element and appropriation account, and (4) how much the Department of Defense budgeted in fiscal year 1990 for mobile ground stations. As agreed with your office, our review focused primarily on mobile ground stations used by the Air Force’s satellite programs and included mobile ground stations used for one Defense Communications Agency satellite program. The Air Force’s satellite control architecture establishes a requirement for mobile ground stations to provide command and control instructions to maintain the position of a satellite in orbit as well as to provide the capability to process information coming from satellites. This network of stations, when completed, is planned to supplement fixed stations and/or to totally command and control a satellite’s position in orbit or process information. As of May 1989, there were 39 existing mobile ground stations. -

National Reconnaissance Office Review and Redaction Guide

NRO Approved for Release 16 Dec 2010 —Tep-nm.T7ymqtmthitmemf- (u) National Reconnaissance Office Review and Redaction Guide For Automatic Declassification Of 25-Year-Old Information Version 1.0 2008 Edition Approved: Scott F. Large Director DECL ON: 25x1, 20590201 DRV FROM: NRO Classification Guide 6.0, 20 May 2005 NRO Approved for Release 16 Dec 2010 (U) Table of Contents (U) Preface (U) Background 1 (U) General Methodology 2 (U) File Series Exemptions 4 (U) Continued Exemption from Declassification 4 1. (U) Reveal Information that Involves the Application of Intelligence Sources and Methods (25X1) 6 1.1 (U) Document Administration 7 1.2 (U) About the National Reconnaissance Program (NRP) 10 1.2.1 (U) Fact of Satellite Reconnaissance 10 1.2.2 (U) National Reconnaissance Program Information 12 1.2.3 (U) Organizational Relationships 16 1.2.3.1. (U) SAF/SS 16 1.2.3.2. (U) SAF/SP (Program A) 18 1.2.3.3. (U) CIA (Program B) 18 1.2.3.4. (U) Navy (Program C) 19 1.2.3.5. (U) CIA/Air Force (Program D) 19 1.2.3.6. (U) Defense Recon Support Program (DRSP/DSRP) 19 1.3 (U) Satellite Imagery (IMINT) Systems 21 1.3.1 (U) Imagery System Information 21 1.3.2 (U) Non-Operational IMINT Systems 25 1.3.3 (U) Current and Future IMINT Operational Systems 32 1.3.4 (U) Meteorological Forecasting 33 1.3.5 (U) IMINT System Ground Operations 34 1.4 (U) Signals Intelligence (SIGINT) Systems 36 1.4.1 (U) Signals Intelligence System Information 36 1.4.2 (U) Non-Operational SIGINT Systems 38 1.4.3 (U) Current and Future SIGINT Operational Systems 40 1.4.4 (U) SIGINT -

Usafalmanac ■ Gallery of USAF Weapons

USAFAlmanac ■ Gallery of USAF Weapons By Susan H.H. Young The B-1B’s conventional capability is being significantly enhanced by the ongoing Conventional Mission Upgrade Program (CMUP). This gives the B-1B greater lethality and survivability through the integration of precision and standoff weapons and a robust ECM suite. CMUP will include GPS receivers, a MIL-STD-1760 weapon interface, secure radios, and improved computers to support precision weapons, initially the JDAM, followed by the Joint Standoff Weapon (JSOW) and the Joint Air to Surface Standoff Missile (JASSM). The Defensive System Upgrade Program will improve aircrew situational awareness and jamming capability. B-2 Spirit Brief: Stealthy, long-range, multirole bomber that can deliver conventional and nuclear munitions anywhere on the globe by flying through previously impenetrable defenses. Function: Long-range heavy bomber. Operator: ACC. First Flight: July 17, 1989. Delivered: Dec. 17, 1993–present. B-1B Lancer (Ted Carlson) IOC: April 1997, Whiteman AFB, Mo. Production: 21 planned. Inventory: 21. Unit Location: Whiteman AFB, Mo. Contractor: Northrop Grumman, with Boeing, LTV, and General Electric as principal subcontractors. Bombers Power Plant: four General Electric F118-GE-100 turbo fans, each 17,300 lb thrust. B-1 Lancer Accommodation: two, mission commander and pilot, Brief: A long-range multirole bomber capable of flying on zero/zero ejection seats. missions over intercontinental range without refueling, Dimensions: span 172 ft, length 69 ft, height 17 ft. then penetrating enemy defenses with a heavy load Weight: empty 150,000–160,000 lb, gross 350,000 lb. of ordnance. Ceiling: 50,000 ft. Function: Long-range conventional bomber. -

GAO-15-366, SPACE ACQUISITIONS: Space Based

United States Government Accountability Office Report to the Committee on Armed Services, U.S. Senate April 2015 SPACE ACQUISITIONS Space Based Infrared System Could Benefit from Technology Insertion Planning GAO-15-366 April 2015 SPACE ACQUISITIONS Space Based Infrared System Could Benefit from Technology Insertion Planning Highlights of GAO-15-366, a report to the Committee on Armed Services, U.S. Senate Why GAO Did This Study What GAO Found SBIRS is a key part of DOD’s missile The Air Force assessed options for replacing older technologies with newer warning and defense systems. To ones—called technology insertion—in the Space Based Infrared System (SBIRS) replace the first two satellites currently geosynchronous earth orbit (GEO) satellites 5 and 6. However, the assessment on orbit, the Air Force plans to build was limited in the number of options it could practically consider because of two more with the same design as timing and minimal early investment in technology planning. The Air Force previous satellites. The basic SBIRS assessed the feasibility and cost of inserting new digital infrared focal plane design is years old and some of its technology—used to provide surveillance, tracking, and targeting information for technology has become obsolete. To national missile defense and other missions—in place of the current analog focal address obsolescence issues in the plane, either with or without changing the related electronics. While technically next satellites, the program must feasible, neither option was deemed affordable or deliverable when needed. The replace old technologies with new ones, a process that may be referred Air Force estimated that inserting new focal plane technology would result in cost to as technology insertion or refresh. -

The Global Positioning System

The Global Positioning System Assessing National Policies Scott Pace • Gerald Frost • Irving Lachow David Frelinger • Donna Fossum Donald K. Wassem • Monica Pinto Prepared for the Executive Office of the President Office of Science and Technology Policy CRITICAL TECHNOLOGIES INSTITUTE R The research described in this report was supported by RAND’s Critical Technologies Institute. Library of Congress Cataloging in Publication Data The global positioning system : assessing national policies / Scott Pace ... [et al.]. p cm. “MR-614-OSTP.” “Critical Technologies Institute.” “Prepared for the Office of Science and Technology Policy.” Includes bibliographical references. ISBN 0-8330-2349-7 (alk. paper) 1. Global Positioning System. I. Pace, Scott. II. United States. Office of Science and Technology Policy. III. Critical Technologies Institute (RAND Corporation). IV. RAND (Firm) G109.5.G57 1995 623.89´3—dc20 95-51394 CIP © Copyright 1995 RAND All rights reserved. No part of this book may be reproduced in any form by any electronic or mechanical means (including photocopying, recording, or information storage and retrieval) without permission in writing from RAND. RAND is a nonprofit institution that helps improve public policy through research and analysis. RAND’s publications do not necessarily reflect the opinions or policies of its research sponsors. Cover Design: Peter Soriano Published 1995 by RAND 1700 Main Street, P.O. Box 2138, Santa Monica, CA 90407-2138 RAND URL: http://www.rand.org/ To order RAND documents or to obtain additional information, contact Distribution Services: Telephone: (310) 451-7002; Fax: (310) 451-6915; Internet: [email protected] PREFACE The Global Positioning System (GPS) is a constellation of orbiting satellites op- erated by the U.S. -

Acquisition of Space Systems, Volume 7: Past Problems and Future Challenges

YOOL KIM, ELLIOT AXELBAND, ABBY DOLL, MEL EISMAN, MYRON HURA, EDWARD G. KEATING, MARTIN C. LIBICKI, BRADLEY MARTIN, MICHAEL E. MCMAHON, JERRY M. SOLLINGER, ERIN YORK, MARK V. A RENA, IRV BLICKSTEIN, WILLIAM SHELTON ACQUISITION OF SPACE SYSTEMS PAST PROBLEMS AND FUTURE CHALLENGES VOLUME 7 C O R P O R A T I O N For more information on this publication, visit www.rand.org/t/MG1171z7 Library of Congress Control Number: 2015933393 ISBN: 978-0-8330-8895-6 Published by the RAND Corporation, Santa Monica, Calif. © Copyright 2015 RAND Corporation R® is a registered trademark. Cover image: United Launch Alliance Limited Print and Electronic Distribution Rights This document and trademark(s) contained herein are protected by law. This representation of RAND intellectual property is provided for noncommercial use only. Unauthorized posting of this publication online is prohibited. Permission is given to duplicate this document for personal use only, as long as it is unaltered and complete. Permission is required from RAND to reproduce, or reuse in another form, any of its research documents for commercial use. For information on reprint and linking permissions, please visit www.rand.org/pubs/permissions.html. The RAND Corporation is a research organization that develops solutions to public policy challenges to help make communities throughout the world safer and more secure, healthier and more prosperous. RAND is nonprofit, nonpartisan, and committed to the public interest. RAND’s publications do not necessarily reflect the opinions of its research clients and sponsors. Support RAND Make a tax-deductible charitable contribution at www.rand.org/giving/contribute www.rand.org Preface Space systems deliver critical capability to warfighters; thus, acquiring and deploying space systems in a timely and affordable manner is important to U.S. -

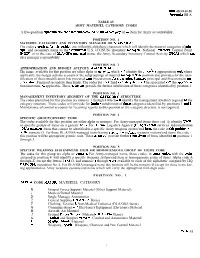

Item for Army Accountability, the Codes Presc@B@For @ P

DoD 41OO.38-M Appendix HI A TABLE 65 ARMY MATERIEL CATEGORY CODES A five-position alph~umeric code that indi~tes the finmci~ wtegory of ~ item for Army accountability, POSITION NO. 1 MATERIEL CATEGORY AND INVENTORY MANAGER OR NICP/SICA: The codes presc@b@for @ p.wition are, inflexible alphabetic characters which will identify the materiel categories of prin- cipal and secondary items to the Continen@ U.S. (CONUS) inventory mm~ers, National Invenbry Control Point (NICP), or in the case of DLA/GSA-managed items, the Army Secondary Inventory Control Activity (SICA) which exer- ekes manager responsibility. POSITION NO. 2 APPROPRIATION AND BUDGET ACTIVITY ACCOUNT& *. The codes available for this position are either alpha or numeric, which will identify the procu& appropriation ~d, where applicable, the budget activity account or the subgroupings of materiel m~ed. fiis position also providea for the iden- tification of those modification kits procured with Procurement Appropriation Financed principal and Procurement @- propriation Financed secondary item funds. The codes for stock fund second~y items wiU be associated with the aPpropna- 4 tion limitation, as applicable. These codes will provide for further subdivision of those categories identified by position 1. POSITION NO. 3 MANAGEMENT INVENTORY SEGMENT OF THE CATEGORY STRUCTURE The codes prescribed for this position are numeric 1 through 4 which will identif y the management inventory segment of the category structure. These codes will provide for further subdivision of those categories identified by positions 1 ~d 2. Maintenance of control accounts for recurring reports to this position of the category structure is not required. -

Gallery of USAF Weapons Note: Inventory Numbers Are Total Active Inventory Figures As of Sept

Gallery of USAF Weapons Note: Inventory numbers are total active inventory figures as of Sept. 30, 2015. By Aaron M. U. Church, Senior Editor ■ 2016 USAF Almanac BOMBER AIRCRAFT B-1 Lancer Brief: Long-range bomber capable of penetrating enemy defenses and de- livering the largest weapon load of any aircraft in the inventory. COMMENTARY The B-1A was initially proposed as replacement for the B-52, and four proto- types were developed and tested before program cancellation in 1977. The program was revived in 1981 as B-1B. The vastly upgraded aircraft added 74,000 lb of usable payload, improved radar, and reduced radar cross section, but cut maximum speed to Mach 1.2. The B-1B first saw combat in Iraq during Desert Fox in December 1998. Its three internal weapons bays accommodate a substantial payload of weapons, including a mix of different weapons in each bay. Lancer production totaled 100 aircraft. The bomber’s blended wing/ body configuration, variable-geometry design, and turbofan engines provide long range and loiter time. The B-1B has been upgraded with GPS, smart weapons, and mission systems. Offensive avionics include SAR for tracking, B-2A Spirit (SSgt. Jeremy M. Wilson) targeting, and engaging moving vehicles and terrain following. GPS-aided INS lets aircrews autonomously navigate without ground-based navigation aids Dimensions: Span 137 ft (spread forward) to 79 ft (swept aft), length 146 and precisely engage targets. Sniper pod was added in 2008. The ongoing ft, height 34 ft. integrated battle station modifications is the most comprehensive refresh in Weight: Max T-O 477,000 lb. -

Gallery of USAF Weapons Note: Inventory Numbers Are Total Active Inventory Figures As of Sept

Gallery of USAF Weapons Note: Inventory numbers are total active inventory figures as of Sept. 30, 2009. By Susan H. H. Young ■ 2010 USAF Almanac Bombers B-1 Lancer Brief: A long-range, air refuelable multirole bomber capable of flying intercontinental missions and penetrating enemy defenses with the largest payload of guided and unguided weapons in the Air Force inventory. Function: Long-range conventional bomber. Operator: ACC, AFMC. First Flight: Dec. 23, 1974 (B-1A); Oct. 18, 1984 (B-1B). Delivered: June 1985-May 1988. IOC: Oct. 1, 1986, Dyess AFB, Tex. (B-1B). Production: 104. Inventory: 66. Aircraft Location: Dyess AFB, Tex., Edwards AFB, Calif., Eglin AFB, Fla., Ellsworth AFB, S.D. Contractor: Boeing; AIL Systems; General Electric. Power Plant: four General Electric F101-GE-102 turbo- fans, each 30,780 lb thrust. Accommodation: four, pilot, copilot, and two systems officers (offensive and defensive), on zero/zero ACES II B-1B Lancer (Clive Bennett) ejection seats. Dimensions: span spread 137 ft, swept aft 79 ft, length 146 ft, height 34 ft. towed decoy complement its low radar cross section to First Flight: July 17, 1989. Weight: empty 192,000 lb, max operating weight form an integrated, robust onboard defense system that Delivered: Dec. 20, 1993-2002. 477,000 lb. supports penetration of hostile airspace. IOC: April 1997, Whiteman AFB, Mo. Ceiling: more than 30,000 ft. B-1A. USAF initially sought this new bomber as a replace- Production: 21. Performance: max speed at low level high subsonic, ment for the B-52, developing and testing four prototypes Inventory: 20. -

“Secret”, “Spy”, and “Classified” Terminology on Satellite Covers

ORBIT when the satellite details are unavailable. Often that generic information involves using the words “secret”, “spy”, or “classified” to describe the satellites being launched. This article, while not focusing on any particular series of military/reconnaissance satellites, explores the use of generic descriptive terminology as substitutes for actual details of many military satellite launches. The authors did an informal and limited survey of terminology found on their collection of satellite launch covers after noticing that certain key words or phrases are used often, while others are much less common. Covers with examples of the featured words will be shown after the survey results are introduced. As a disclaimer to this study, the results presented here are based on the authors’ collection of thousands of launch covers, which we feel is large enough to be fairly representative and informative. A Survey of “Secret”, “Spy”, and However, other cover collectors might find different terminology or statistics. If so, we invite them to share “Classified” Terminology on those results with us. Satellite Covers Terminology and key word statistics Don Hillger and Garry Toth For about 20 years, the authors have posted images of launch covers, not all of which we own, in online lists. Since many military and reconnaissance satellites are Some of the cover images were provided by other launched under a cloak of secrecy, it is left to cover collectors. Those lists can be found at the link provided at manufacturers to use generic descriptions on launch covers the end of this article. Since the authors collect mainly un- 11 ORBIT manned satellite launch covers, that collection includes 1962-04-17 [yyyy-mm-dd] launch/cancel date.