Jakarta Property Market Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Daftar BU BBM Untuk Website Migas.Xlsx

STATUS BADAN USAHA NIAGA MIGAS UNTUK KEGIATAN NIAGA MINYAK BUMI/BBM/HASIL OLAHAN (PERIODE S.D OKTOBER 2020) A. BADAN USAHA NIAGA MIGAS, STATUS: PENGHENTIAN SEMENTARA/PEMBEKUAN No Nama Badan Usaha Alamat Badan Usaha Jenis Kegiatan Usaha 1 PT Hj Nurfadiah Jaya Angkasa Jl. Pulau Samosir no. 27 B Karang Mumus Samarinda Ilir Kalimantan Timur 75113 Niaga Umum BBM B. BADAN USAHA NIAGA MIGAS, STATUS: AKTIF, STATUS PELAPORAN : RUTIN No Nama Badan Usaha Alamat Badan Usaha Jenis Kegiatan Usaha 1 PT Agung Persada Mandiri Jl. Karang Anyar Raya 55 Blok A No.46, Kel. Karang Anyar, Sawah Besar, Jakarta Pusat Niaga Umum BBM 2 PT AKR Corporindo Tbk Wisma AKR Lantai 7 – 8 JL. Panjang Nomor 5 Kebon Jeruk, Jakarta Barat 11530 Niaga Umum BBM 3 PT Andifa Perkasa Energi Perum Jhonlin Indah C no 10 RT 013/003 Gunung Antasari Niaga Umum BBM 4 PT Aneka Petroindo Raya AKR Tower Lantai. 25 Jl. Panjang No. 5 RT. 011 RW 010. Kebon Jeruk, Kebon Jeruk, Jakarta Barat Niaga Umum BBM 5 PT Angkasa Tunggal Selaras Nugrahatama Sentra Arteri Mas Blok I Lt. 4 Jl. Sultan Iskandar Muda No. 10 Niaga Umum Hasil Olahan 6 PT Anigos Jaya Perkasa Jl. Lingkar Utara RT/RW 007/006, Kel. Perwira, Bekasi Utara, Bekasi Niaga Umum BBM 7 PT Anugrah Aldhi Persada Gd Graha BIP Lt 9 Jl Jend Gatot Subroto Kav 23, RT 002/002 Setiabudi, Jakarta Selatan Niaga Umum BBM 8 PT Apex Indopacific Rukan Crown Plaza Blok C-08 Jl. Prof.Dr.Soepomo SH No. 231 Jakarta Selatan Niaga Umum BBM 9 PT Arinda Ananda Arsindo Jl. -

Regional Kabupaten Tipe Outlet Nama Outlet BALI NUSRA KOTA

Regional Kabupaten Tipe Nama Outlet Outlet BALI NUSRA KOTA DENPASAR Erafone XIAOMI STORE TEUKU UMAR BALI BALI NUSRA KOTA DENPASAR Erafone MEGASTORE RUKO GATOT SUBROTO BALI BALI NUSRA KUPANG Erafone SES LIPPO PLAZA KUPANG BALI NUSRA KUPANG Erafone ERAFONE LIPPO PLAZA KUPANG BALI NUSRA KOTA MATARAM Erafone MEGASTORE RUKO MATARAM LOMBOK BALI NUSRA KOTA DENPASAR Erafone SES TRANS STUDIO MALL BALI BALI NUSRA KOTA DENPASAR Erafone ERAFONE MALL BALI GALERIA BALI NUSRA KOTA DENPASAR Erafone SES BEACHWALK BALI BALI NUSRA KOTA DENPASAR Erafone MEGASTORE 2 TEUKU UMAR BALI NUSRA KOTA DENPASAR Erafone MEGASTORE RUKO SINGARAJA BALI BALI NUSRA KOTA DENPASAR Erafone TELKOMSEL GRAPARI RENON BALI NUSRA KOTA MATARAM Erafone TELKOMSEL GRAPARI LOMBOK EPICENTRUM MALL BALI NUSRA KOTA MATARAM Erafone ERAFONE LOMBOK EPICENTRUM MALL CENTRAL JAKARTA BARAT Erafone ERAFONE 2 ITC ROXY MAS JABOTABEK CENTRAL JAKARTA BARAT Erafone ERAFONE 3 ITC ROXY MAS JABOTABEK CENTRAL JAKARTA BARAT Erafone ERAFONE 4 ITC ROXY MAS JABOTABEK CENTRAL JAKARTA BARAT Erafone ERAFONE CENTRAL PARK JABOTABEK CENTRAL JAKARTA BARAT Erafone ERAFONE DAAN MOGOT MALL JABOTABEK CENTRAL JAKARTA BARAT Erafone ERAFONE GREEN SEDAYU MALL JABOTABEK CENTRAL JAKARTA BARAT Erafone ERAFONE MAL CIPUTRA JAKARTA JABOTABEK CENTRAL JAKARTA BARAT Erafone ERAFONE MAL PURI INDAH JABOTABEK CENTRAL JAKARTA BARAT Erafone ERAFONE MAL TAMAN ANGGREK JABOTABEK CENTRAL JAKARTA BARAT Erafone ERAFONE PLAZA SLIPI JAYA JABOTABEK CENTRAL JAKARTA BARAT Erafone ERAFONE PX PAVILION ST MORITS JABOTABEK Internal Regional Kabupaten Tipe -

List Store Ibox

List Store iBox NO Store Name Addres 1 IBOX NEW KOTA KASABLANKA JL. Casablanca Raya Kav. 88, Jakarta Selatan, DKI 2 IBOX CILANDAK TOWN SQUARE Cilandak Town Square Ground Floor #065, Jl. T.B. 3 IBOX GANDARIA CITY Gandaria City 1st Floor #189, Jl. KH. M. Syafi'i Hadzami 4 IBOX KEMANG Lippo Mall Kemang 2nd Floor L2-27, Jl. Pangeran 5 IBOX PEJATEN VILLAGE Pejaten Village Lt. L2 – 08-09 Jl. Warung Jati Barat No. 6 IBOX RATU PLAZA 2 Ratu Plaza 1st Floor #8, Jl. Jendral Sudirman No. 9 7 IBOX MALL OF AMBASSADOR II Mal Ambasador 3rd Floor #18, Jl. Prof. Dr. Satrio Kav. FIRST FLOOR, UNIT NO. FL1 - 22 MARGO CITY, JL. 8 IBOX MARGO CITY MARGONDA RAYA NO. 358, DEPOK 16423 Ground Floor / 01 Jl. Juanda No. 99 Bakti Jaya Sukma 9 IBOX PESONA SQUARE DEPOK Jaya, Kota Depok, Jawa Barat 16418 10 IBOX FLAGSHIP SENAYAN CITY Senayan City 4th Floor #4-29 Jl. Asia Afrika Lot 19 Kode IBOX FLAGSHIP SUMMARECON Jl. Boulevard raya Gading Serpong Pakulonan Barat 11 MALL SERPONG Kelapa Dua Unit #GF211-212-215 IBOX BAYWALK MALL (GREEN Bay Walk Mall 4th Floor #36 Green Bay Pluit Jl. Pluit 12 BAY PLUIT) Karang Ayu, Penjaringan, Jakarta Utara 14450 Unit GF A3 001,002,016,017 Jl. Boulevard Artha Gading 13 IBOX MAL ARTHA GADING No.1, RT.18/RW.8, Klp. Gading Bar., Kec. Klp. Gading, Kota Jkt Utara, Daerah Khusus Ibukota Jakarta 14240 Mall of Indonesia Ground Floor #GF–A5 Jl. Raya 14 IBOX MALL OF INDONESIA NEW Boulevard Barat, Kelapa Gading, Jakarta Utara 14240 Jl. -

Feasibility Study Final Report on FY2014 JCM Large-Scale Project for Achievement of a Low-Carbon Society in Asia

Feasibility Study Final Report on FY2014 JCM Large-scale Project for Achievement of a Low-carbon society in Asia Feasibility Study on financing scheme development project for promoting energy efficiency equipment installation in Indonesia March, 6th, 2015 International Project Center Environment and Energy Research Division Table of Contents 1. Outline of the Study ........................................................................................................................ 1 1.1 Purpose of the Project .................................................................................................... 1 1.2 Subject of Project ........................................................................................................... 1 1.2.1 Study on an ESCO project in Indonesia ........................................................................... 1 1.2.2 Domestic progress briefing session ................................................................................. 3 1.2.3 Local workshops ........................................................................................................... 4 1.2.4 Presentations at a meeting designated by the Ministry of the Environment .......................... 4 1.3 Study system ................................................................................................................. 4 1.4 Implementation period ................................................................................................... 5 1.5 Deliverables ................................................................................................................. -

ALL BRANCHES of OPTIK SEIS

ALL BRANCHES of OPTIK SEIS : City Outlet Address & Location Telpphone PASAR BARU (EXPRESS) Jl. Pasar Baru No. 101 Telp. (021) 3812849, 3812429 PLAZA INDONESIA Lantai 3 No. E14 & E15, Jl. MH Thamrin Telp. (021) 31926924 GRAND INDONESIA SHOPPING TOWN (SIGNATURE) Lt. 2 East Mall Unit EM-2-39, Jl. MH. Thamrin No. 1 Telp. (021) 23580623 PLAZA ATRIUM Lantai Dasar Unit G.43-44, Jl. Senen Raya No.135 Telp. (021) 3862967 JAKARTA PUSAT GAJAH MADA PLAZA Lantai Dasar No. 47 - 49 Jl. Gajah Mada No. 19 - 26 Telp. (021) 6344648 SENAYAN CITY Second Floor No. 32 Jl. Asia Afrika Lot 19 Telp. ( 021) 72781258 PLAZA SENAYAN Lantai 2 No. 257C, 259C, 230B & 232B Jl. Asia Afrika No. 8 Telp. (021) 5725154, 5725121 CENTRAL DEPARTEMENT STORE Lantai Dasar East Mall, Jl. MH. Thamrin No. 1 GREEN PRAMUKA ( EXPRESS ) Ground Floor No.32-33, Jl.Jendral Ahmad Yani Kav 49 Jakarta Pusat (021) 29624938 MELAWAI RAYA No.65 (SIGNATURE) Jl. Melawai Raya No. 65, Kebayoran Baru Telp. (021) 7262206, 7262687 LIPPO MALL KEMANG SIGNATURE Upper Ground No. UG-30, Jl. Pangeran Antasari No.36, Kemang Jakarta 12150 Telp. (021) 29056893 PONDOK INDAH MALL 1 (SIGNATURE) Lantai 1 No. 101A, Jl. Metro Duta Pondok Indah Kav IV/TA Telp. (021) 7506790 PONDOK INDAH MALL 2 Lantai 1 No. 112, Jl. Kartika Utama V - TA Telp. (021) 75920500 LOTTE SHOPPING AVENUE Ciputra World 1, Lantai 1F No. 20A, Jl. Prof. DR. Satrio Kav. 3-5, Setiabudi, Jakarta 12940 Telp. (021) 29889470 TOWN SQUARE CILANDAK Level 2 (First Floor) No. 139, Jl. TB. Simatupang Kav. -

Bab I Pendahuluan

BAB I PENDAHULUAN 1.1 Gambaran Umum Objek Penelitian 1.1.1 Sejarah Singkat Perusahaan Hennes & Mauritz AB merupakan perusahaan multinasional yang bergerak dibidang fashion dan memproduksi busana sendiri. Perusahaan berdiri pada tahun 1947 yang bermarkas di Stockholm, Swedia. Sekarang perusahaan ini beroperasi di lebih dari 28 negara dan mempekerjakan 60.000 pekerja. Fashion brand ini pada awalnya hanyalah toko kecil di kawasan Västerås, Swedia. Awal mula bisnis ini yaitu berasal dari Pria yang berumur 30 tahun bernama Erling Persson, yang mulanya jalan-jalan di New York lalu tertarik untuk menjual pakaian wanita dan akhirnya pada 1947 dia membuka toko bernama Hennes yang memiliki arti perempuan. Kata ini diambil dari bahasa Swedia. Gambar 1.1 Store H&M ditahun 1947 Sumber : Dokumen H&M Sepuluh tahun kemudian Mauritz Widforss yang menjadikan nama Hennes menjadi Hennes & Mauritz. Berkat Mauritz kini fashion brand yang mulanya dikhususkan untuk wanita menjual pakaian juga untuk pria dan juga anak kecil. Ekspansi besar-besaran pun membuat mereka memiliki 42 gerai di beberapa wilayah. Lalu di tahun 1973 Hennes & Mauretz mulai menjual pakaian dalam, baik untuk wanita maupun pria. Kemudian di tahun berikutnya Hennes & Mauretz resmi rebranding menjadi H&M. 1.1.2 Lokasi H&M di Indonesia Menurut Detik Finance, hingga kini brand asal Swedia tersebut udah berekspansi hingga berbagai negara dan memiliki lebih dari 1.000 gerai termasuk salah satunya berada di Indonesia. H&M mulai memasuki Indonesia dengan membuka toko pertamanya di Gandaria City Mall, Jakarta Selatan. Toko seluas 2.400 meter persegi ini akan dibuka pada 5 Oktober 2013. Alasan untuk memilih Indonesia untuk mengembangkan bisnisnya karena menurut beliau, Indonesia memiliki pasar yang sangat menarik, penduduknya banyak lebih dari 200 juta orang, ini salah satu negara terbesar di dunia, dan ekonominya tumbuh, fashion tinggi, kami melihat banyak mode yang berbeda di sini dan kami menawarkan fashion untuk semua orang. -

+6285899961287 Pengaruh Kualitas Produk, Persepsi

PENGARUH KUALITAS PRODUK, PERSEPSI HARGA, DAN CITRA MEREK TERHADAP KEPUASAN PELANGGAN PRODUK UNIQLO DI MALL OF INDONESIA Salda Lavenia Email : [email protected] Dr. Ir. Abdullah Rakhman, M.M. Email : [email protected] Progam Studi Manajemen Institut Bisnis dan Informatika Kwik Kian Gie Abstract The object of this research is Uniqlo at Mall of Indonesia. The research method used is descriptive analysis and multiple regression analysis. Data collection began with a questionnaire of 170 people with Uniqlo customers at Mall of Indonesia as respondents, sampling is taking by nonprobability sampling with purposive sampling technique. The conclusion of this research is product quality, brand image and price perception have a positive influence on customer satisfaction. This study shows that respondents rated the product quality as good, brand image was good, price perception was appropriate, and customers were satisfied. The results of this study indicate that product quality, brand image and price perception have a positive effect on Uniqlo customer satisfaction at Mall of Indonesia. Keywords: Product Quality, Price Perception, Brand Image, Customer Satisfaction Abstrak Objek penelitian ini adalah Uniqlo di Mall Of Indonesia. Metode penelitian yang digunakan adalah analisis deskriptif dan analisis regresi berganda. Pengumpulan data dilakukan dengan menyebar kuesioner kepada 170 sampel pelanggan Uniqlo di Mall Of Indonesia sebagai respondennya. Pengambilan sampel dilakukan dengan cara nonprobability sampling dengan teknik purposive sampling. Kesimpulan dari penelitian ini adalah kualitas produk, citra merek dan persepsi harga memiliki pangaruh positif terhadap kepuasan pelanggan. Penelitian ini menunjukan bahwa responden menilai kualitas produk sudah baik, citra merek sudah baik, persepsi harga sudah sesuai, dan pelanggan puas. -

Politics and Urban Development Focus on Jakarta's Shopping Center Trajectory

POLITICS AND URBAN DEVELOPMENT FOCUS ON JAKARTA’S SHOPPING CENTER TRAJECTORY A Thesis Presented to the FaCulty of ArChiteCture and Planning COLUMBIA UNIVERSITY In Partial Fulfillment of the Requirements for the Degree Master of SCienCe in Urban Planning by Melinda Martinus May 2018 Advisor Hiba Bou Akar Reader Gavin Shatkin Abstract "City of consumerism" seems to be an appropriate moniker for Jakarta, the capital city of Indonesia. Over the past few years, Jakarta has transformed from an administrative town where both state and local public authorities exercise policy and development strategy — into an economic empire of the nation. Economic indicators pointed out that the economic development in the metropolitan region is massive; 6 percent economic growth, rising middle-class’ purchasing power, and increasing foreign property investment. Urban scholars have highlighted that this urban transformation is much influenced by modern world-class city aspiration driven by the private sectors who are able to display grandiose modern projects and influence the policy makers. One of the many phenomena that shows this urban revolution is the booming of shopping center development in the metropolitan region. Currently, Jakarta Metropolitan Region has 153 shopping centers, supplying more than 5 million square meter retail spaces to the 30 million metropolitan population. I argue that the enormous number of shopping center operated in the city comes as the result of the shifting urban development focus towards neoliberalism bounded to an intricate economic, political, and ideological system of the nation. Using urban historical framework and the mapping techniques, I seek to analyze the urban transformation through the shopping center perspective. -

Evolutionary Patterns in Indonesian Shopping Centers: the Case of Jakarta

EVOLUTIONARY PATTERNS IN INDONESIAN SHOPPING CENTERS: THE CASE OF JAKARTA Widiyani, PhD Candidate Urban Planning Group, Faculty of Architecture TU/e [email protected] Harry J.P. Timmermans Urban Planning Group, Faculty of Architecture TU/e [email protected] In the second term of 2006 Jakarta, the capital city of Indonesia experienced the largest retail growth in the Asian Pacific region. With more than 130 centers in 2010, the growth of Jakarta’s shopping centers is not only reflected in numbers but also in their physical size. In part, this evolution of shopping centers reflects the globalization of shopping centers development and major retailers. The location, composition and design of such centers strongly resemble other shopping centers in the Asian Pacific and the United States. At the same time, however, other centers seem more unique to Indonesia. In that sense, it is rather difficult to univocally assign these centers to the categories used in the classification suggested by International Council on Shopping Center Classifications (ICSC). The purpose of this paper is to describe and analyze the evolution of shopping centers in Jakarta using data from 1960-2010. To identify patterns of evolution hierarchical cluster analysis was employed. The first step is to measure similarity and dissimilarity between samples. The second step is to label and explain the clusters that had been found. The findings suggest three clusters of evolutionary patterns; classic shopping center, modern contemporary shopping center, and modern local shopping center. In addition to the city-level description of the evolution of shopping centers in Jakarta, a more detailed account will be given of each cluster. -

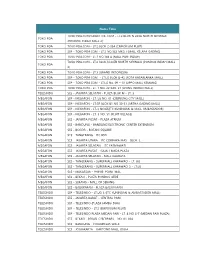

Nama Toko TOKO PDA TOKO PDA.COM/TABLET OK .COM

Nama Toko TOKO PDA.COM/TABLET OK .COM - LT.2 BLOK N 203A NORTH SKYWALK TOKO PDA (PONDOK INDAH MALL 2) TOKO PDA TOKO PDA.COM - LT.2 BLOK 2-35A (EMPORIUM PLUIT) TOKO PDA SEP - TOKO PDA.COM - LT.2 NO.362 MKG I (MALL KELAPA GADING) TOKO PDA TOKO PDA.COM - LT.1 NO.144 A (MALL PURI INDAH) TOKO PDA.COM - LT.2 BLOK N 207B NORTH SKYWALK (PONDOK INDAH MALL TOKO PDA 2) TOKO PDA TOKO PDA.COM - LT.3 (GRAND INDONESIA) TOKO PDA SEP - TOKO PDA.COM - LT.LG BLOK U-42 (KOTA KASABLANKA MALL) TOKO PDA SEP - TOKO PDA.COM - LT.LG No. 09 – 10 (LIPPO MALL KEMANG) TOKO PDA TOKO PDA.COM - LT. 1 NO. 22 KAV. 21 (LIVING WORLD MALL) TELESINDO SES - JAKARTA SELATAN - PLAZA BLOK M - LT. 3 MEGAFON SEP - MEGAFON - LT. LG NO. 01 (CIBINONG CITY MALL) MEGAFON SEP - MEGAFON - LT.GF BLOK B1 NO 30-31 (ARTHA GADING MALL) MEGAFON SEP - MEGAFON - LT-3_NO.65(ITC KUNINGAN & MALL AMBASSADOR) MEGAFON SEP - MEGAFON - LT. 3 NO. 51 (PLUIT VILLAGE) MEGAFON SES - JAKARTA PUSAT - PLAZA ATRIUM MEGAFON SES - BANDUNG - BANDUNG ELECTRONIC CENTER EXTENSION MEGAFON SES - BOGOR - BOTANI SQUARE MEGAFON SES - TANGERANG - ITC BSD MEGAFON SES - JAKARTA UTARA - ITC CEMPAKA MAS - BLOK. L MEGAFON SES - JAKARTA SELATAN - ITC FATMAWATI MEGAFON SES - JAKARTA PUSAT - GAJAH MADA PLAZA MEGAFON SES - JAKARTA SELATAN - MALL KALIBATA MEGAFON SES - TANGERANG - SUPERMALL KARAWACI - LT. UG MEGAFON SES - TANGERANG - SUPERMALL KARAWACI 2 - LT.LG MEGAFON SES - MAKASSAR - PHINISI POINT MAL MEGAFON SES - BEKASI - PLAZA PONDOK GEDE MEGAFON SES - SERANG - MALL OF SERANG MEGAFON SES - BALIKPAPAN - PLAZA BALIKPAPAN TELESINDO SEP - TELESINDO - LT.UG_3 (ITC KUNINGAN & AMBASSADOR MALL) TELESINDO SES - JAKARTA BARAT - CENTRAL PARK TELESINDO SEP - TELESINDO (PLAZA JAMBU DUA) TELESINDO SEP - TELESINDO - LT.2 (EMPORIUM PLUIT) TELESINDO SEP - TELESINDO PLAZA MEDAN FAIR - LT. -

Postcard from Jakarta

MUSIC EDUCATION IN INDONESIA F FOCUS FEATURE Postcard from Jakarta Piano teacher Melanie Spanswick was recently invited to serve as a ‘grand mentor’ at the Cantata Music School in Jakarta, working with both students and teachers. As she writes here, the visit was also an opportunity to learn about the broader music education landscape of Indonesia usic education around the world varies to work with both students and teachers, preparing E Melanie tremendously. The quality of tuition depends on students for a teatime concert, and this was followed by Spanswick Mfactors such as culture, finances and interest, a day of workshops for teachers which focused purely (centre) and as well as access to an educated workforce. I was invited on piano technique. Wherever I go to teach, particularly other teachers at to teach in Indonesia during October 2019, assuming in developing or emerging countries, certain musical Jakarta’s Cantata the role of ‘grand mentor’ at the Sekolah Musik Kantata elements frequently appear problematic. This may be due Music School (Cantata Music School) for Cantata Youth Musician (a to lack of student interest or practice, but, more often student performance programme). This school’s main hub than not, it’s sadly due to inadequate teaching. is situated in North Jakarta, but it has several Jakartan Becoming a piano teacher in Indonesia is no easy premises and a few satellites all around Indonesia. The feat. Teachers don’t always have access to the necessary central school in Kelapa Gading, housed in a large complex opportunities, and therefore they rely on acquiring Grade called the Mall of Indonesia, accommodates lessons for 8 or diploma exams from the major British examination over 600 students weekly, such is the interest and demand boards. -

Public Expose FY 2014

Public Expose Full Year 2014 PT Graha Layar Prima Tbk Section 1: Introduction to PT Graha Layar Prima Tbk Section 2: Indonesia’s movie theatre industry Section 3: Detailed company overview Section 4: GLP business plan Section 5: Financial overview Section 1: Introduction to PT Graha Layar Prima Tbk Section 2: Indonesia’s movie theatre industry Section 3: Detailed company overview Section 4: GLP business plan Section 5: Financial overview Company Overview – PT Graha Layar Prima Tbk (“GLP”) "Movies and Beyond" Robust Growth Embrace the concept of one-stop 12 locations with over 17,000 entertainment hub seats in 8 years . World-class theatres 3-year CAGR of 30%* for . Game center (X-rider) revenues since 2011 Trend Setter Impact Maker . Merchandise shops Differentiate with leading Provide customers with technology and trends different choices . 4DX Contributed to a recovery of . Sphere-X screen the cinema industry, post- . Velvet, Satin and Gold class monopoly era Vision Strong Values To be the first choice for Excellence unforgettable cinematic Mission Teamwork experiences Provide unforgettable Innovation entertainment experiences through a combination of exceptional products and services *Including Blitztheater (franchise) Group Structure PT Catur PT Layar IKT Holdings CJ CGV Co. PT Pangea Adi Kusuma Abadi Public Persada Limited Ltd Benua Jaya 48.24% 14.75% 14.75% 0.16% 0.05% 22.04% PT Graha Layar Prima Tbk 99.82% PT Graha Layar Mitra Organizational Structure BOARD OF COMMISSIONERS Audit Committee BOARD OF DIRECTORS President Director Corporate Internal Audit Unit Secretary Director of Public Director of Marketing Director of Business Director of Finance Relations & Human & Operations Development Resources Structural reporting line Coordination line We have a solid team of directors and commissioners to lead us Bratanata Perdana H.