Revision of Uniform Disclaimer of Property Interests Acts

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Uniform Probate Code Article Ii Intestacy, Wills, and Donative Transfers

UNIFORM PROBATE CODE ARTICLE II INTESTACY, WILLS, AND DONATIVE TRANSFERS [Sections to be Revised in Bold] Table of Sections PART 1 INTESTATE SUCCESSION § 2-101. Intestate Estate. § 2-102. Share of Spouse. § 2-102A. Share of Spouse. § 2-103. Share of Heirs Other Than Surviving Spouse. § 2-104. Requirement That Heir Survive Decedent for 120 Hours. § 2-105. No Taker. § 2-106. Representation. § 2-107. Kindred of Half Blood. § 2-108. Afterborn Heirs. § 2-109. Advancements. § 2-110. Debts to Decedent. § 2-111. Alienage. § 2-112. Dower and Curtesy Abolished. § 2-113. Individuals Related to Decedent Through Two Lines. § 2-114. Parent and Child Relationship. § 2-101. Intestate Estate. (a) Any part of a decedent’s estate not effectively disposed of by will passes by intestate succession to the decedent’s heirs as prescribed in this Code, except as modified by the decedent’s will. (b) A decedent by will may expressly exclude or limit the right of an individual or class to succeed to property of the decedent passing by intestate succession. If that individual or a member of that class survives the decedent, the share of the decedent’s intestate estate to which that individual or class would have succeeded passes as if that individual or each member of that class had disclaimed his [or her] intestate share. § 2-102. Share of Spouse. The intestate share of a decedent’s surviving spouse is: (1) the entire intestate estate if: (i) no descendant or parent of the decedent survives the decedent; or (ii) all of the decedent’s surviving descendants are also -

Testamentary Trusts

TESTAMENTARY TRUSTS Trusts that are created pursuant to the terms of a probated Last Will and Testament are commonly referred to as “testamentary trusts.” 1. Applicable Law. The applicable law for these Trusts is the Kansas Probate Code (not the Kansas Trust Code). The authority of the probate court as to testamentary trusts is set forth at K.S.A. 59-103(7), as follows: to supervise the administration of trusts and powers created by wills admitted to probate, and trusts and powers created by written instruments other than by wills in favor of persons subject to conservatorship; to appoint and remove trustees for such trusts, to make all necessary orders relating to such trust estates, to direct and control the official acts of such trustees, and to settle their accounts. K.S.A. 59-103(a) Docket Fee for Trusteeship $69.50 [Rev. Ch. 80, Sec. 17, 2017 Sess. Laws] 2. Obtaining Appointment of Testamentary Trustee. Based upon the statutory grant of Court authority under K.S.A. 59-103(7), it appears necessary for a nominated testamentary trustee to be formally appointed by the Court. As a practical matter, the judicial grant of Letters of Trusteeship may be necessary to obtain delivery of the trust’s share of probate assets, to deal with banks and financial institutions (such as to open accounts), or to later sell assets. It is also appropriate to establish the formal commencement of the new fiduciary relationship and the Trustee’s formal acceptance of the obligation as fiduciary for the newly established testamentary trust. -

Answering Your Legal Questions About Revocable Living Trusts Who May Create, Manage, and Benefit from a Revocable Living Trust?

Answering your legal questions about revocable living trusts Who may create, manage, and benefit from a revocable living trust? If you were to die or become disabled, you’d want your This pamphlet, which dependents to be financially secure. And you’d want some- is based on Wisconsin one to manage or distribute your assets just as you would yourself, if you could. The only way to assure these out- law, is issued to inform comes is to do estate planning. and not to advise. No A revocable living trust is one of several estate-plan- person should ever ning tools. You can read about others in the State Bar of apply or interpret any Wisconsin’s pamphlet, “Wills/Estate Planning: Answering Your Legal Questions.” law without the aid Should a revocable living trust be part of your estate of a trained expert plan? No simple guidelines exist to answer that question. who knows the facts, People with various levels of wealth and in different cir- because the facts may cumstances may, or may not, find a revocable living trust useful. change the application Your legal or financial adviser can help you of the law. Last revised: decide whether this option is right for you. This pam- 10/2013 phlet answers several questions to provide you basic information. Who can be the trustee? What is a revocable living trust? Any competent adult may be a trustee. Usually, you name yourself, or you and your spouse, as the trustee because A trust is a written document that names someone to you want full control of the property while you’re alive. -

Wills--Deceased Residuary Legatee's Share Held Not to Pass by Way Of

St. John's Law Review Volume 38 Number 1 Volume 38, December 1963, Number Article 11 1 Wills--Deceased Residuary Legatee's Share Held Not to Pass by Way of Intestacy Where It Is Clearly Manifested That Surviving Residuary Legatees Should Share in the Residuum (In re Dammann's Estate, 12 N.Y.2d 500 (1963)) St. John's Law Review Follow this and additional works at: https://scholarship.law.stjohns.edu/lawreview This Recent Development in New York Law is brought to you for free and open access by the Journals at St. John's Law Scholarship Repository. It has been accepted for inclusion in St. John's Law Review by an authorized editor of St. John's Law Scholarship Repository. For more information, please contact [email protected]. ST. JOHN'S LAW REVIEW [ VOL. 38 argument against such an extension was rejected. 52 Likewise, the presence of a compensation fund for prisoners was held not necessarily to preclude prisoner suits under the FTCA.53 The Court found the compensation scheme to be non-comprehensive.5 4 The government's contention that variations in state laws might hamper uniform administration of federal prisons, as it was feared they would with the military, was rejected. Admitting that prisoner recoveries might be prejudiced to some extent by variations in state law, the Court regarded no recovery at all as a more serious prejudice to the prisoner's rights.55 In this connection, it is interesting to consider the desirability of spreading tort liability in the governmental area.5" The impact of the principal case is, in some respects, clear. -

Probate and Property (35:01)

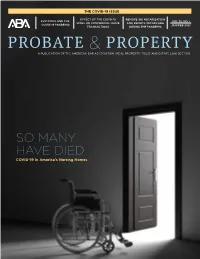

THE COVID-19 ISSUE EFFECT OF THE COVID-19 REMOTE INK NOTARIZATION EVICTIONS AND THE VOL 35, NO 1 VIRUS ON COMMERCIAL LEASE AND REMOTE WITNESSING COVID-19 PANDEMIC JAN/FEB 2021 TRANSACTIONS DURING THE PANDEMIC A PUBLICATION OF THE AMERICAN BAR ASSOCIATION | REAL PROPERTY, TRUST AND ESTATE LAW SECTION SO MANY HAVE DIED COVID-19 in America’s Nursing Homes The Section is excited to announce the RPTE Book Club. The RPTE Book Club is a lecture and Q&A Series with the authors. Each series will be a different book title within the legal field. THE COLOR OF LAW A Forgotten History of How Our Government Segregated America Join RPTE along with author Richard Rothstein as he discusses how segregation in America is the byproduct of explicit government policies at the local, state, and federal levels along with a Q&A session. Wednesday, February 24, 2021 12-1 PM CT The first 100 registrants will receive a copy of the book with their registration fee. Register at ambar.org/rptebookclub PROFESSORS’ CORNER PROFESSORS’ CORNER A monthly webinar featuring a panel of professors addressing recent cases or issues of relevance to A monthlypractitioners webinar and featuring scholars ofa panel real estate of professors or trusts addressing and estates. recent FREE cases for RPTE or issues Section of relevance members to! practitioners and scholars of real estate or trusts and estates. FREE for RPTE Section members! Register for each webinar at http://ambar.org/ProfessorsCornerRegister for each webinar at http://ambar.org/ProfessorsCorner WILLS IN THE 21ST CENTURY: TOWARDS THE SECURE ACT: RETIREMENT PLANNING SENSIBLE APPLICATION OF FORMALITIES AND MONETARY EXPECTATIONS THE LEGACIES OF RACIAL RESTRICTIVE MOORE ON POWELL AND I.R.C. -

Dependent Disclaimers Katheleen R

University of Oklahoma College of Law From the SelectedWorks of Katheleen R. Guzman Fall 2016 Dependent Disclaimers Katheleen R. Guzman Available at: https://works.bepress.com/katheleen_guzman/11/ guzman, katheleen 12/4/2017 For Educational Use Only DEPENDENT DISCLAIMERS, 42 ACTEC L.J. 159 42 ACTEC L.J. 159 ACTEC Law Journal Fall, 2016 Katheleen R. Guzmana1 Copyright © 2016 by The American College of Trust and Estate Counsel. All Rights Reserved.; Katheleen R. Guzman *159 DEPENDENT DISCLAIMERS I. INTRODUCTION Intent, delivery, and acceptance.1 The first two can be pressed at a donor’s choice; with the last one, the donee can brake. In this regard, inter vivos gift theory reflects symmetrical propositions: just as no one can be forced to make a gift, none can be forced to accept one. The same holds true for estates. Under the twin theories of renunciation and disclaimer,2 would-be takers may refuse to accept a devise or inheritance,3 simultaneously rejecting a right to acquire and exercising a right to avoid. Such refusal again reflects evenness of form, for in the very act of disclaiming inheres the enrichment of someone else. It might initially seem odd that one would reject another’s largesse or the status of being deemed heir. But ownership carries both value and cost, and acquisition is personal choice. Refusal will sometimes occur. *160 Where the rejecter is also the would-be owner, the disclaimer is both clean and direct, and is a relative commonplace within estates law to attain tax efficiency or avoid a creditor’s claim. -

Ademption by Extinction: Smiting Lord Thurlow's Ghost

ADEMPTION BY EXTINCTION: SMITING LORD THURLOW'S GHOST John C. Paulus* INTRODUCTION Testator (T)properly executes a will giving his farm, Blackacre, to his daughter (D), and the rest of his property to his son (S). T lives with D on Blackacre. Three years later T sells Blackacre and buys Whiteacre. T and D live together on Whiteacre until T's death four years later. From numerous utterances and acts it is very evident that T wants D to have Whiteacre for her own after his death. Will Whiteacre go to D or S? In most (maybe all) of the states, the answer would be, "S." The identity rule enunciated by Lord Thurlow in 1786 is followed.' As indicated by its application to T, D, and S, the dominating philosophy can bring forth some unsatisfactory results. Lord Thurlow's opinion calls for the application of a simple test in determining whether or not a specific devise adeems: If the asset identified as the exclusive subject of the devise is not held by the testator at his death, the devise fails.' Ademption by extinction, as this problem area is uniformly called, is reduced to a matter of identifying, if possible, the devised item in the estate.' The most often quoted statement by Lord Thurlow is: "And I do * Professor of Law, Willamette University. Visiting Professor of Law, Texas Tech University 1970-71. 1. Ashburner v. Macguire, 29 Eng. Rep. 62 (Ch. 1786). This hypothetical is similar to the facts in Ashburner in that the testator sells the devised asset (Blackacre). Three years later in Stanley v. -

Coming to Terms with the Uniform Probate Code's Reformation of Wills

University of Colorado Law School Colorado Law Scholarly Commons Articles Colorado Law Faculty Scholarship 2012 Coming to Terms with the Uniform Probate Code's Reformation of Wills Wayne M. Gazur University of Colorado Law School Follow this and additional works at: https://scholar.law.colorado.edu/articles Part of the Estates and Trusts Commons, and the Evidence Commons Citation Information Wayne M. Gazur, Coming to Terms with the Uniform Probate Code's Reformation of Wills, 64 S.C. L. REV 403 (2012), available at https://scholar.law.colorado.edu/articles/740. Copyright Statement Copyright protected. Use of materials from this collection beyond the exceptions provided for in the Fair Use and Educational Use clauses of the U.S. Copyright Law may violate federal law. Permission to publish or reproduce is required. This Article is brought to you for free and open access by the Colorado Law Faculty Scholarship at Colorado Law Scholarly Commons. It has been accepted for inclusion in Articles by an authorized administrator of Colorado Law Scholarly Commons. For more information, please contact [email protected]. +(,121/,1( Citation: 64 S. C. L. Rev. 403 2012-2013 Provided by: William A. Wise Law Library Content downloaded/printed from HeinOnline Tue Feb 28 11:04:51 2017 -- Your use of this HeinOnline PDF indicates your acceptance of HeinOnline's Terms and Conditions of the license agreement available at http://heinonline.org/HOL/License -- The search text of this PDF is generated from uncorrected OCR text. -- To obtain permission to use this article beyond the scope of your HeinOnline license, please use: Copyright Information COMING TO TERMS WITH THE UNIFORM PROBATE CODE'S REFORMATION OF WILLS Wayne M. -

Attorney and Client - Unauthorized Practice - Practice of Law by Corporations John T

Marquette Law Review Volume 21 Article 5 Issue 1 December 1936 Attorney and Client - Unauthorized Practice - Practice of Law by Corporations John T. McCarrier Follow this and additional works at: http://scholarship.law.marquette.edu/mulr Part of the Law Commons Repository Citation John T. McCarrier, Attorney and Client - Unauthorized Practice - Practice of Law by Corporations, 21 Marq. L. Rev. 55 (1936). Available at: http://scholarship.law.marquette.edu/mulr/vol21/iss1/5 This Article is brought to you for free and open access by the Journals at Marquette Law Scholarly Commons. It has been accepted for inclusion in Marquette Law Review by an authorized administrator of Marquette Law Scholarly Commons. For more information, please contact [email protected]. 1936] RECENT DECISIONS in the end would retain the amount received by them and the residuary legatee would not be relieved in the slightest. The result would be effected only if costs consumed the corpus of the residuary legatee's portion or if such legatee was bankrupt. The banking commission seems to have been fully satisfied on this score and hence its resolve to bring the action only against the residuary legatee is perfectly intel- ligible. Just why the court should not be satisfied with this arrange- ment which would do complete justice between the parties and save expense and trouble is difficult to understand in view of the two other cases above mentioned in which the liability was enforced against dis- tributees. In all three cases all that really happened was that property of the deceased stockholder came to the legatee subject to a lien for the superadded liability. -

26. Uniform Disclaimer of Property Interests Act

CHAPTER 8.1 26. UNIFORM DISCLAIMER OF PROPERTY INTERESTS ACT. Drafting note: Existing Chapter 8.1 has been relocated to proposed Subtitle V due to its applicability to both probate and nonprobate transfers. Existing Chapter 8.1 is based on the Uniform Disclaimer of Property Interests Act promulgated by the National Conference of Commissioners on Uniform State Laws in 1999 as both a stand-alone act and a part of the Uniform Probate Code. Virginia enacted the Act in 2003. There is little variation between the language of the Act as promulgated and as adopted in Virginia. § 64.1-196.1 64.2-2600. Definitions. In As used in this chapter: "Disclaimant" means the person to whom a disclaimed interest or power would have passed had the disclaimer not been made. "Disclaimed interest" means the interest that would have passed to the disclaimant had the disclaimer not been made. "Disclaimer" means the refusal to accept an interest in or power over property. "Fiduciary" means a personal representative, trustee, agent acting under a power of attorney, or other person authorized to act as a fiduciary with respect to the property of another person. "Jointly held property" means property held in the name of two of more persons under an arrangement in which all holders have concurrent interests and under which the last surviving holder is entitled to the whole of the property and includes, without limitation, property held as tenants by the entirety. "Person" means an individual, corporation, business trust, estate, trust, partnership, limited liability company, association, joint venture, government, governmental subdivision, agency or instrumentality, public corporation, or any other legal or commercial entity. -

California Law Revision Commission

STATE OF CALIFORNIA CALIFORNIA LAW REVISION COMMISSION STAFF REPORT California Uniform Prudent Investor Act March 1998 California Law Revision Commission 4000 Middlefield Road, Room D-1 Palo Alto, CA 94303-4739 NOTE This is a special edition of the Uniform Prudent Investor Act setting out the origi- nal explanatory text from the Commission’s recommendation and the final statutory text with official Commission Comments. Staff Report on California Uniform Prudent Investor Act UNIFORM PRUDENT INVESTOR ACT * A new Uniform Prudent Investor Act was approved by the National Conference of Commissioners on Uniform State Laws in the summer of 1994.1 The new act seeks to modernize investment practices of fiduciaries, focusing on trustees of pri- vate trusts. The primary objectives of the UPIA are stated in its Prefatory Note: (1) The standard of prudence is applied to any investment as part of the total portfolio, rather than to individual investments. In the trust setting the term “portfolio” embraces all the trust’s assets.… (2) The tradeoff in all investing between risk and return is identified as the fiduciary’s central consideration.… (3) All categoric restrictions on types of investments have been abrogated; the trustee can invest in anything that plays an appropriate role in achieving the risk/return objectives of the trust and that meets the other requirements of prudent investing.… (4) The long familiar requirement that fiduciaries diversify their investments has been integrated into the definition of prudent investing.… (5) The much criticized former rule of trust law forbidding the trustee to dele- gate investment and management functions has been reversed. -

Uniform Trust Code

D R A F T FOR DISCUSSION ONLY UNIFORM TRUST CODE NATIONAL CONFERENCE OF COMMISSIONERS ON UNIFORM STATE LAWS MARCH 10, 2000 INTERIM DRAFT UNIFORM TRUST CODE WITHOUT PREFATORY NOTE AND COMMENTS Copyright © 2000 By NATIONAL CONFERENCE OF COMMISSIONERS ON UNIFORM STATE LAWS The ideas and conclusions set forth in this draft, including the proposed statutory language and any comments or reporter’s notes, have not been passed upon by the National Conference of Commissioners on Uniform State Laws or the Drafting Committee. They do not necessarily reflect the views of the Conference and its Commissioners and the Drafting Committee and its Members and Reporters. Proposed statutory language may not be used to ascertain the intent or meaning of any promulgated final statutory proposal. UNIFORM TRUST CODE TABLE OF CONTENTS ARTICLE 1 GENERAL PROVISIONS AND DEFINITIONS SECTION 101. SHORT TITLE. ............................................................ 1 SECTION 102. SCOPE. ................................................................... 1 SECTION 103. DEFINITIONS. ............................................................. 1 SECTION 104. DEFAULT AND MANDATORY RULES. ...................................... 4 SECTION 105. QUALIFIED BENEFICIARIES. ............................................... 5 SECTION 106. NOTICE. .................................................................. 5 SECTION 107. COMMON LAW OF TRUSTS. ................................................ 6 SECTION 108. CHOICE OF LAW. .........................................................