The Rise of Liu He: China's New Economic Czar

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hong Kong SAR

China Data Supplement November 2006 J People’s Republic of China J Hong Kong SAR J Macau SAR J Taiwan ISSN 0943-7533 China aktuell Data Supplement – PRC, Hong Kong SAR, Macau SAR, Taiwan 1 Contents The Main National Leadership of the PRC 2 LIU Jen-Kai The Main Provincial Leadership of the PRC 30 LIU Jen-Kai Data on Changes in PRC Main Leadership 37 LIU Jen-Kai PRC Agreements with Foreign Countries 47 LIU Jen-Kai PRC Laws and Regulations 50 LIU Jen-Kai Hong Kong SAR 54 Political, Social and Economic Data LIU Jen-Kai Macau SAR 61 Political, Social and Economic Data LIU Jen-Kai Taiwan 65 Political, Social and Economic Data LIU Jen-Kai ISSN 0943-7533 All information given here is derived from generally accessible sources. Publisher/Distributor: GIGA Institute of Asian Affairs Rothenbaumchaussee 32 20148 Hamburg Germany Phone: +49 (0 40) 42 88 74-0 Fax: +49 (040) 4107945 2 November 2006 The Main National Leadership of the PRC LIU Jen-Kai Abbreviations and Explanatory Notes CCP CC Chinese Communist Party Central Committee CCa Central Committee, alternate member CCm Central Committee, member CCSm Central Committee Secretariat, member PBa Politburo, alternate member PBm Politburo, member Cdr. Commander Chp. Chairperson CPPCC Chinese People’s Political Consultative Conference CYL Communist Youth League Dep. P.C. Deputy Political Commissar Dir. Director exec. executive f female Gen.Man. General Manager Gen.Sec. General Secretary Hon.Chp. Honorary Chairperson H.V.-Chp. Honorary Vice-Chairperson MPC Municipal People’s Congress NPC National People’s Congress PCC Political Consultative Conference PLA People’s Liberation Army Pol.Com. -

Journal of Current Chinese Affairs

3/2006 Data Supplement PR China Hong Kong SAR Macau SAR Taiwan CHINA aktuell Journal of Current Chinese Affairs Data Supplement People’s Republic of China, Hong Kong SAR, Macau SAR, Taiwan ISSN 0943-7533 All information given here is derived from generally accessible sources. Publisher/Distributor: Institute of Asian Affairs Rothenbaumchaussee 32 20148 Hamburg Germany Phone: (0 40) 42 88 74-0 Fax:(040)4107945 Contributors: Uwe Kotzel Dr. Liu Jen-Kai Christine Reinking Dr. Günter Schucher Dr. Margot Schüller Contents The Main National Leadership of the PRC LIU JEN-KAI 3 The Main Provincial Leadership of the PRC LIU JEN-KAI 22 Data on Changes in PRC Main Leadership LIU JEN-KAI 27 PRC Agreements with Foreign Countries LIU JEN-KAI 30 PRC Laws and Regulations LIU JEN-KAI 34 Hong Kong SAR Political Data LIU JEN-KAI 36 Macau SAR Political Data LIU JEN-KAI 39 Taiwan Political Data LIU JEN-KAI 41 Bibliography of Articles on the PRC, Hong Kong SAR, Macau SAR, and on Taiwan UWE KOTZEL / LIU JEN-KAI / CHRISTINE REINKING / GÜNTER SCHUCHER 43 CHINA aktuell Data Supplement - 3 - 3/2006 Dep.Dir.: CHINESE COMMUNIST Li Jianhua 03/07 PARTY Li Zhiyong 05/07 The Main National Ouyang Song 05/08 Shen Yueyue (f) CCa 03/01 Leadership of the Sun Xiaoqun 00/08 Wang Dongming 02/10 CCP CC General Secretary Zhang Bolin (exec.) 98/03 PRC Hu Jintao 02/11 Zhao Hongzhu (exec.) 00/10 Zhao Zongnai 00/10 Liu Jen-Kai POLITBURO Sec.-Gen.: Li Zhiyong 01/03 Standing Committee Members Propaganda (Publicity) Department Hu Jintao 92/10 Dir.: Liu Yunshan PBm CCSm 02/10 Huang Ju 02/11 -

Proquest Dissertations

The diffusion of the Internet in China Item Type text; Dissertation-Reproduction (electronic) Authors Foster, William Abbott Publisher The University of Arizona. Rights Copyright © is held by the author. Digital access to this material is made possible by the University Libraries, University of Arizona. Further transmission, reproduction or presentation (such as public display or performance) of protected items is prohibited except with permission of the author. Download date 04/10/2021 12:10:22 Link to Item http://hdl.handle.net/10150/289812 INFORMATION TO USERS This manuscript has been reproduced from the microfilm master. UMI films the text directly from the original or copy submitted. Thus, some thesis and dissertation copies are in typewriter face, while others may be from any type of computer printer. The quality of this reproduction is dependent upon the quality of the copy submitted. Broken or indistinct print, colored or poor quality Illustrations and photographs, print bleedthrough. substandard margins, and improper alignment can adversely affect reproduction. In the unlikely event that the author did not send UMI a complete manuscript and there are missing pages, these will be noted. Also, if unauthorized copyright material had to be removed, a note will indicate the deletion. Oversize materials (e.g., maps, drawings, charts) are reproduced by sectioning the original, beginning at the upper left-hand comer and continuing from left to right in equal sections with small overiaps. Photographs included in the original manuscript have been reproduced xerographically in this copy. Higher quality 6" x 9" black and white photographic prints are available for any photographs or illustrations appearing in this copy for an additional charge. -

Edited LOEBS Cites Plus List of Elements 1 30

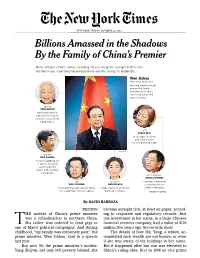

C MCYMK Y K Nxxx,2012-10-26,A,001,Bs-BK,E3Nxxx,2012-10-26,A,001,Bs-BK,E3 C M Y K Nxxx,2012-10-26,A,001,Bs-BK,E3 Late EditionLate Edition C M Y K Nxxx,2012-10-26,A,001,Bs-BK,E3 Today, morning fog and clouds, par- Today, morning fog and clouds, par- tial clearing,Late high 68. Edition Tonight, most- tial clearing, high 68. Tonight, most- ly cloudy,Today, morning mild, low fog 56.and Tomorrow, clouds, par- ly cloudy, mild, low 56. Tomorrow, periodictial clearing, clouds high and 68. sunshine, Tonight, most-high Late Edition periodic clouds and sunshine, high 66. lyWeather cloudy, mild,map lowis on 56. PageTomorrow, Today,B12.morning fog and clouds, par- 66. Weather map is ontial clearing,Page high B12. 68. Tonight, most- periodic clouds and sunshine,ly high cloudy, mild, low 56. Tomorrow, 66. Weather map is on Pageperiodic B12. clouds and sunshine, high 66. Weather map is on Page B12. VOL. CLXII . No. 55,936 © 2012 The New York Times NEW YORK, FRIDAY, OCTOBER 26, 2012 $2.50 VOL. CLXII . No. 55,936 © 2012 The New York Times NEW YORK, FRIDAY, OCTOBER 26, 2012 $2.50 VOL. CLXII . No. 55,936 © 2012 The New York Times NEW YORK, FRIDAY, OCTOBER 26, 2012 $2.50 VOL. CLXII . No. 55,936 © 2012 The New York Times NEW YORK, FRIDAY, OCTOBER 26, 2012 $2.50 POLITICAL MEMO POLITICALPOLITICAL MEMO MEMO 2 CHILDREN SLAIN Billions Amassed in the Shadows POLITICAL MEMO 2 CHILDREN2 CHILDREN SLAINObama SLAINBillions Campaign Endgame: Amassed in the Shadows 2 CHILDREN SLAIN Billions Amassed AmassedAT HOME IN CITY; in inBy the thethe ShadowsFamily Shadows of China’s Premier ObamaObama Campaign Campaign Endgame: Endgame: Grunt Work and Cold Math NANNY ARRESTED Obama Campaign Endgame:AT HOMEAT HOME IN CITY; IN CITY; Many relatives of Wen Jiabao, including his son, daughter, younger brother and AT HOME IN CITY; By JIMBy RUTENBERG the Family of brother-in-law,China’s have become extraordinarily Premier wealthy during his leadership. -

Oil Rises As US Imposes New Sanctions on Iran

NISHAT JV | Page 4 STAKE SALE | Page 10 Hyundai set to MUFG Q3 net assemble cars profi t rises 17% To advertise here in Pakistan to $2.62bn Call: Saturday, February 4, 2017 Jumada I 7, 1438 AH NONFARM PAYROLLS UP : Page 12 US job growth GULF TIMES accelerates in January, BUSINESS but wages lag A M Best affirms Oil rises as US imposes QIIC rating with ‘stable’ outlook By Santhosh V Perumal agency said while the com- Business Reporter pany benefits from moderate new sanctions on Iran underwriting leverage, capital requirements are largely Reuters A M Best, an international insur- driven by asset risk relating to New York/London ance rating agency, has aff irmed the company’s concentrated Qatar Islamic Insurance Com- portfolio, which is weighted pany’s financial strength rating towards domestic equities and il prices jumped yesterday after at ‘B++ (Good)’ and long-term real estate assets. the United States imposed sanc- issuer credit rating at “bbb+” The policyholders’ fund is Otions on some Iranian individuals with “stable” outlook. “suff iciently” capitalised on a and entities, days after the White House The ratings reflect the insurer’s standalone basis, supported by put Tehran “on notice” over a ballistic track record of excellent operat- QR110mn of retained surplus as missile test. ing performance, adequate com- on September 30, 2016. Front month US West Texas Intermedi- bined risk-adjusted capitalisation QIIC has a track record of strong ate crude futures climbed 24¢ to $53.78, (considering both shareholders’ operating and technical profit- after closing 34¢ down on Thursday, as of and policyholders’ funds), and ability, highlighted by a five-year 12:22pm ET (1722 GMT). -

Cleaning the Security Apparatus Before the Two Meetings

ASIA PROGRAMME CLEANING THE SECURITY APPARATUS BEFORE THE TWO MEETINGS BY ALEX PAYETTE PH.D, CEO CERCIUS GROUP ADJUNCT PROFESSOR, GLENDON COLLEGE MAY 2020 ASIA FOCUS #139 l’IRIS ASIA FOCUS #139 – ASIA PROGRAMME / May 2020 n April 19 2020, Sun Lijun 孙力军 was put under investigation. Sun is the mishu of Meng Jianzhu 孟建柱, Party secretary of the Central Political and Legal Affairs o Commission [zhengfa] from 2012 to 2017, and a close ally of Politburo member Han Zheng 韩正, who is also a full member of Jiang Zemin’s 江泽民 Shanghai Gang 上海帮 . His arrest, which happened only one day after 15 pro-democracy activists were arrested in Hong Kong1, almost coincided with his return from Wuhan – as part of the Covid-19 containment steering group 中央赴湖北指导组. To this effect, it is evident that Sun’s investigation and arrest have been in motion for quite a while now. With Sun out of play, the former public security “tsar” Zhou Yongkang 周永康 has effectively lost most of his tentacles on the public security system. That said, Sun’s arrest might not even be the most important news shaking up the public security apparatus ahead of the upcoming “Two Meetings” 两会. CUTTING THE ROOTS As it is customary with Cadres working for public security, State security and national Defence, Sun Lijun’s public profile is quite limited. Sun, who studied in Australia, majored in public health and urban management, a very interesting choice especially considering the current pandemic. Sun was primarily active in Shanghai, and held a number of notable posts in his career including: • Director of the Hong Kong affairs office of the Ministry of Public Security from 2016 until his arrest; • Deputy director of the infamous “610” unit 中央610办公室– also known as the Central Leading Group on Preventing and Dealing with Heretical Religions 中央防范 和处理邪教问题领导小组2; • Director of the No. -

2017 China Insurance Review

2017 Insurance Review FEBRUARY 2018 Thomas P. Fitzgerald Chairman Winston & Strawn LLP Foreword The continued growth of China’s insurance market means more opportunities for established and new insurance companies and insurance intermediaries looking to expand or create a foothold there. Winston & Strawn, a leading expert in cross-border M&A, contentious, and regulatory work, established offices in Hong Kong in 2008 and in Shanghai in 2009 in order to better serve our clients that operate in Asia. Our presence in Hong Kong and Mainland China has allowed us to broaden our services and extend the reach of our practices to include insurance expertise for the PRC. I hope that you find this booklet useful. Please feel free to reach out to our China team should you have any questions or require any additional information. You will find their contact details at the end of this booklet. Attorney advertising materials – © 2018 Winston & Strawn LLP 1. Introduction The overall outlook for China’s insurance industry has enjoyed robust growth in recent years. Total premium income, for example, China is healthy and rose 27.5% in 2016 to reach RMB 3.1 trillion (USD 490 billion), the strongest growth the industry has enjoyed statistics for 2017 show since 2008. As well, by the end of 2016, total insurance industry assets stood at RMB 15.12 trillion (USD 2.39 that overall insurance trillion), a 22.3% increase from the start of the year. Premium growth slowed in 2017 due in large part to premium income rose China Insurance Regulatory Commission (“CIRC”) reforms aimed at universal life insurance. -

China (Includes Tibet, Hong Kong, and Macau) 2017 Human Rights Report

CHINA (INCLUDES TIBET, HONG KONG, AND MACAU) 2017 HUMAN RIGHTS REPORT EXECUTIVE SUMMARY The People’s Republic of China (PRC) is an authoritarian state in which the Chinese Communist Party (CCP) is the paramount authority. CCP members hold almost all top government and security apparatus positions. Ultimate authority rests with the CCP Central Committee’s 25-member Political Bureau (Politburo) and its seven-member Standing Committee. Xi Jinping continued to hold the three most powerful positions as CCP general secretary, state president, and chairman of the Central Military Commission. At the 19th Communist Party Congress in October, the CCP reaffirmed Xi as the leader of China and the CCP for another five years. Civilian authorities maintained control of the military and internal security forces. The most significant human rights issues for which the government was responsible included: arbitrary or unlawful deprivation of life and executions without due process; extralegal measures such as forced disappearances, including extraterritorial ones; torture and coerced confessions of prisoners; arbitrary detention, including strict house arrest and administrative detention, and illegal detentions at unofficial holding facilities known as “black jails”; significant restrictions on freedom of speech, press, assembly, association, religion, and movement (for travel within the country and overseas), including detention and harassment of journalists, lawyers, writers, bloggers, dissidents, petitioners, and others as well as their family members; -

China Dream, Space Dream: China's Progress in Space Technologies and Implications for the United States

China Dream, Space Dream 中国梦,航天梦China’s Progress in Space Technologies and Implications for the United States A report prepared for the U.S.-China Economic and Security Review Commission Kevin Pollpeter Eric Anderson Jordan Wilson Fan Yang Acknowledgements: The authors would like to thank Dr. Patrick Besha and Dr. Scott Pace for reviewing a previous draft of this report. They would also like to thank Lynne Bush and Bret Silvis for their master editing skills. Of course, any errors or omissions are the fault of authors. Disclaimer: This research report was prepared at the request of the Commission to support its deliberations. Posting of the report to the Commission's website is intended to promote greater public understanding of the issues addressed by the Commission in its ongoing assessment of U.S.-China economic relations and their implications for U.S. security, as mandated by Public Law 106-398 and Public Law 108-7. However, it does not necessarily imply an endorsement by the Commission or any individual Commissioner of the views or conclusions expressed in this commissioned research report. CONTENTS Acronyms ......................................................................................................................................... i Executive Summary ....................................................................................................................... iii Introduction ................................................................................................................................... 1 -

Download/Manual/Statistical Report I 3Th.Of, Accessedon February 12,2004

University of Warwick institutional repository: http://go.warwick.ac.uk/wrap A Thesis Submitted for the Degree of PhD at the University of Warwick http://go.warwick.ac.uk/wrap/2442 This thesis is made available online and is protected by original copyright. Please scroll down to view the document itself. Please refer to the repository record for this item for information to help you to cite it. Our policy information is available from the repository home page. Globalization and Media Governance in the People's Republic of China (1992-2004) By Huaguo Zeng A Thesis Submitted in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy in International Studies University of Warwiclk Department of Politics and Inte Imational Studies July, 2006 CONTENTS Acknowledgments V .............................................................................. Abstract VI ........................................................................................... Abbreviations VII ................................................................................... List Tables Figures VII of and ...................................................................... Notes Text VIII and the ............................................................................... Declaration IX ........................................................................................ CHAPTER ONE INTRODUCTION 1. China's Media Politics 1980s 2 since the ..................................................... 2. Hypothesis, ResearchQuestions, Definitions -

Discord Or “Harmonious Society”?

Discord or “Harmonious Society”? China in 2030 by John P. Geis II, PhD, Colonel, USAF Scott E. Caine, Lieutenant Colonel, USAF Edwin F. Donaldson, Colonel, USAF Blaine D. Holt, Colonel, USAF Ralph A. Sandfry, PhD, Lieutenant Colonel, USAF February 2011 The Occasional Papers series was established by the Center for Strategy and Technology (CSAT) as a forum for research on topics that reflect long-term strategic thinking about technology and its implications for US national security. Copies of no. 68 in this series are available from the Center for Strategy and Technology, Air War College, 325 Chennault Circle, Maxwell AFB, AL 36112, or on the CSAT Web site at http://csat.au.af.mil/. The fax number is (334) 953-6158; phone (334) 953-6150. Occasional Paper No. 68 Center for Strategy and Technology Air University Maxwell Air Force Base, Alabama 36112 Muir S. Fairchild Research Information Center Cataloging Data Discord or “harmonious society”? : China in 2030 / John P. Geis II . [et al.]. p. ; cm.–(Occasional paper / Center for Strategy and Technology ; no. 68) Includes bibliographical references. ISBN 978-1-58566-209-8 1. National security—China—Forecasting. 2. China—History. 3. China—Politics and government. 4. China—Economic conditions. 5. United States. Air Force— Planning. 6. United States—Foreign relations—China. 7. China—Foreign rela- tions—United States. I. Geis, John P. II. Series: Occasional paper (Air University [U.S.]. Center for Strategy and Technology) ; no. 68. 320.951—dc22 Disclaimer The views expressed in this academic research paper are those of the authors and do not reflect the official policy or position of Air University, the US government, or the Department of Defense. -

Xi Jinping Combines Economics and Politics

The General Secretary’s Extended Reach: Xi Jinping Combines Economics and Politics Barry Naughton Xi Jinping has seized the initiative in economic policy, making himself the dominant actor in financial regulation and environmental policy, among other areas. These precedent-breaking economic policy roles provide Xi clear political benefits. They strengthen the central government’s power over local actors, and confirm Xi’s personal dominance of the political process. Quiet economic conditions continue to prevail in the run-up to the 19th Party Congress. However, dynamic economic policy-making has begun to have obvious and significant effects that extend far beyond the economic arenas to which they are initially targeted. A number of recent policy actions show Xi Jinping exercising an extraordinary degree of initiative. This reinforces the consensus view that the 19th Party Congress is likely to conclude with Xi Jinping’s power even greater than before. As economic policy, these actions are likely to display mixed outcomes. They serve to display Xi’s commitment to certain policy objectives, which in some cases makes implementation more effective. However, they also serve as an alternative to institutionalization, which is the only way to ensure the long-term effectiveness of such policies. Xi is going where no party secretary has gone before since Deng Xiaoping established a set of norms for policy-making under collective leadership. He is putting his stamp on everyday economic decision-making. Perhaps more tellingly, he is doing so in a way that extends central power and gives him personally direct instruments of pressure to reach into local governments.