Ledgers and Prices: Early Mesopotamian Merchant Accounts

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Nabu 2015-2-Mep-Dc

ISSN 0989-5671 2015 N°2 (juin) NOTES BRÈVES 25) À propos d’ARET XII 344, des déesses dgú-ša-ra-tum et de la naissance du prince éblaïte* — Le texte administratif ARET XII 344 est malheureusement assez lacuneux, mais à notre avis quand même très intéressant. Les lignes du texte préservées sont les suivantes: r. I’:1’-5’: ‹x›[...] / šeš-[...] / in ⸢u₄⸣ / ḫúl / ⸢íl⸣-['à*-ag*-da*-mu*] v. II’:1’-11’: ...] K[ALAM.]KAL[AM(?)] / NI-šè-na-⸢a⸣ / ma-lik-tum / è / é / daš-dar / ap / íl-'à- ag-da-mu / i[n] / [...] / [...] r. III’:1’-9’: ⸢'à⸣-[...] / 1 gír mar-t[u] zú-aka / 1 buru₄-mušen 1 kù-sal / daš-dar / NAM-ra-luki / 1 zara₆-túg ú-ḫáb / 1 giš-šilig₅* 2 kù-sig₁₇ maš-maš-SÙ / 1 šíta zabar / dga-mi-iš r. IV’:1’-10’: ⸢x⸣[...] / 10 lá-3 an-dù[l] igi-DUB-SÙ šu-SÙ DU-SÙ kù:babbar / 10 lá-3 gú-a-tum zabar / dgú-ša-ra-tum / 5 kù-sig₁₇ / é / en / ni-zi-mu / 2 ma-na 55 kù-sig₁₇ / sikil r. V’:1’-6’: [x-]NE-[t]um / [x K]A-dù-gíd / [m]a-lik-tum / i[n-na-s]um / dga-mi-iš / 1 dib 2 giš- DU 2 ti-gi-na 2 geštu-lá 2 ba-ga-NE-su!(ZU) r. VI’:1’-6’: [...]⸢x⸣ / [m]a-[li]k-tum / [šu-ba₄-]ti / [x ki]n siki / [x-]li / [x-b]a-LUM. Tout d’abord, on remarquera qu’au début du texte on peut lire in ⸢u₄⸣ / ḫúl / ⸢íl⸣-['à*-ag*-da*- mu*], c’est-à-dire « dans le jour de la fête (en l’honneur) d’íl-'à-ag-da-mu ». -

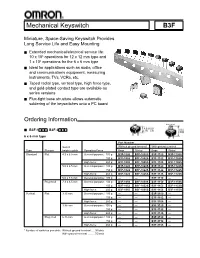

Mechanical Keyswitch B3F

Mechanical Keyswitch B3F Miniature, Space-Saving Keyswitch Provides Long Service Life and Easy Mounting ■ Extended mechanical/electrical service life: 10 x 106 operations for 12 x 12 mm type and 1 x 106 operations for the 6 x 6 mm type ■ Ideal for applications such as audio, office and communications equipment, measuring instruments, TVs, VCRs, etc. ■ Taped radial type, vertical type, high force type, and gold-plated contact type are available as series versions ■ Flux-tight base structure allows automatic soldering of the keyswitches onto a PC board Ordering Information Flat Projected ■ B3F-1■■■, B3F-3■■■ 6 x 6 mm type Part Number Switch Without ground terminal With ground terminal Type Plunger height x pitch Operating Force Bags Sticks* Bags Sticks* Standard Flat 4.3 x 6.5 mm General-purpose: 100 g B3F-1000 B3F-1000S B3F-1100 B3F-1100S 150 g B3F-1002 B3F-1002S B3F-1102 B3F-1102S High-force: 260 g B3F-1005 B3F-1005S B3F-1105 B3F-1105S 5.0 x 6.5 mm General-purpose: 100 g B3F-1020 B3F-1020S B3F-1120 B3F-1120S 150 g B3F-1022 B3F-1022S B3F-1122 B3F-1122S High-force: 260 g B3F-1025 B3F-1025S B3F-1125 B3F-1125S 5.0 x 7.5 mm General-purpose: 100 g — — B3F-1110 — Projected 7.3 x 6.5 mm General-purpose: 100 g B3F-1050 B3F-1050S B3F-1150 B3F-1150S 150 g B3F-1052 B3F-1052S B3F-1152 B3F-1152S High-force: 260 g B3F-1055 B3F-1055S B3F-1155 B3F-1155S Vertical Flat 3.15 mm General-purpose: 100 g — — B3F-3100 — 150 g — — B3F-3102 — High-force: 260 g — — B3F-3105 — 3.85 mm General-purpose: 100 g — — B3F-3120 — 150 g — — B3F-3122 — High-force: 260 g — — B3F-3125 — Projected 6.15 mm General-purpose: 100 g — — B3F-3150 — 150 g — — B3F-3152 — High-force: 260 g — — B3F-3155 — * Number of switches per stick: Without ground terminal ... -

Burn Your Way to Success Studies in the Mesopotamian Ritual And

Burn your way to success Studies in the Mesopotamian Ritual and Incantation Series Šurpu by Francis James Michael Simons A thesis submitted to the University of Birmingham for the degree of Doctor of Philosophy Department of Classics, Ancient History and Archaeology School of History and Cultures College of Arts and Law University of Birmingham March 2017 University of Birmingham Research Archive e-theses repository This unpublished thesis/dissertation is copyright of the author and/or third parties. The intellectual property rights of the author or third parties in respect of this work are as defined by The Copyright Designs and Patents Act 1988 or as modified by any successor legislation. Any use made of information contained in this thesis/dissertation must be in accordance with that legislation and must be properly acknowledged. Further distribution or reproduction in any format is prohibited without the permission of the copyright holder. Abstract The ritual and incantation series Šurpu ‘Burning’ is one of the most important sources for understanding religious and magical practice in the ancient Near East. The purpose of the ritual was to rid a sufferer of a divine curse which had been inflicted due to personal misconduct. The series is composed chiefly of the text of the incantations recited during the ceremony. These are supplemented by brief ritual instructions as well as a ritual tablet which details the ceremony in full. This thesis offers a comprehensive and radical reconstruction of the entire text, demonstrating the existence of a large, and previously unsuspected, lacuna in the published version. In addition, a single tablet, tablet IX, from the ten which comprise the series is fully edited, with partitur transliteration, eclectic and normalised text, translation, and a detailed line by line commentary. -

Herefore, Incentives Typically Offered and Used for Development Would Be Replaced with the EB-5 Investment

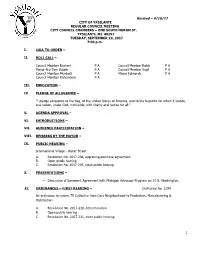

Revised – 9/18/17 CITY OF YPSILANTI REGULAR COUNCIL MEETING CITY COUNCIL CHAMBERS – ONE SOUTH HURON ST. YPSILANTI, MI 48197 TUESDAY, SEPTEMBER 19, 2017 7:00 p.m. I. CALL TO ORDER – II. ROLL CALL – Council Member Bashert P A Council Member Robb P A Mayor Pro-Tem Brown P A Council Member Vogt P A Council Member Murdock P A Mayor Edmonds P A Council Member Richardson P A III. INVOCATION – IV. PLEDGE OF ALLEGIANCE – “I pledge allegiance to the flag, of the United States of America, and to the Republic for which it stands, one nation, under God, indivisible, with liberty and justice for all.” V. AGENDA APPROVAL – VI. INTRODUCTIONS – VII. AUDIENCE PARTICIPATION – VIII. REMARKS BY THE MAYOR – IX. PUBLIC HEARING – International Village - Water Street A. Resolution No. 2017-208, approving purchase agreement. B. Open public hearing C. Resolution No. 2017-209, close public hearing X. PRESENTATIONS – Discussion of Easement Agreement with Michigan Advocacy Program on 15 N. Washington. XI. ORDINANCES – FIRST READING – Ordinance No. 1294 An ordinance to rezone 75 Catherine from Core Neighborhood to Production, Manufacturing & Distribution. A. Resolution No. 2017-210, determination B. Open public hearing C. Resolution No. 2017-211, close public hearing 1 XII. CONSENT AGENDA – Resolution No. 2017-212 1. Resolution No. 2017–213, approving minutes of August 22 and September 5, 2017. 2. Resolution No. 2017-214, approving the issuance of a blanket permit for window signs of any size for the month of October for businesses that participate with the Eastern Michigan University’s “Follow the Green & White Road” homecoming spirit project. -

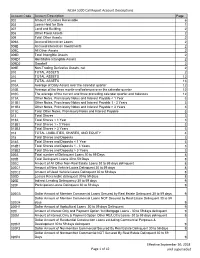

NCUA 5300 Call Report Account Descriptions Page 1 of 42 Effective

NCUA 5300 Call Report Account Descriptions Account Code Account Description Page 002 Amount of Leases Receivable 6 003 Loans Held for Sale 1 007 Land and Building 2 008 Other Fixed Assets 2 009 Total Other Assets 2 009A Accrued Interest on Loans 2 009B Accrued Interest on Investments 2 009C All Other Assets 2 009D Total Intangible Assets 2 009D1 Identifiable Intangible Assets 2 009D2 Goodwill 2 009E Non-Trading Derivative Assets, net 2 010 TOTAL ASSETS 2 010 TOTAL ASSETS 12 010 TOTAL ASSETS 13 010A Average of Daily Assets over the calendar quarter 12 010B Average of the three month-end balances over the calendar quarter 12 010C The average of the current and three preceding calendar quarter-end balances 12 011A Other Notes, Promissory Notes and Interest Payable < 1 Year 3 011B1 Other Notes, Promissory Notes and Interest Payable 1 - 3 Years 3 011B2 Other Notes, Promissory Notes and Interest Payable > 3 Years 3 011C Total Other Notes, Promissory Notes and Interest Payable 3 013 Total Shares 3 013A Total Shares < 1 Year 3 013B1 Total Shares 1 - 3 Years 3 013B2 Total Shares > 3 Years 3 014 TOTAL LIABILITIES, SHARES, AND EQUITY 4 018 Total Shares and Deposits 3 018A Total Shares and Deposits < 1 Year 3 018B1 Total Shares and Deposits 1 - 3 Years 3 018B2 Total Shares and Deposits > 3 Years 3 020A Total number of Delinquent Loans 30 to 59 Days 8 020B Total Delinquent Loans 30 to 59 Days 8 020C Amount of All Other Non-Real Estate Loans 30 to 59 days delinquent 8 020C1 Amount of New Vehicle Loans Delinquent 30 to 59 days 8 020C2 Amount of Used -

Electric Actuators Vsi-1000 Series

ELECTRIC ACTUATORS TM VSI-1000 SERIES DESCRIPTION VSI-1000 Series Electric Actuators are used on Kele KBV Series butterfly valves to provide two-position (with or without battery backup) or proportional control in a NEMA 4X housing. The VSI-1000 Series comes standard on 8" and larger non-spring return assemblies and on 5" and larger two- position spring return assemblies. They can be ordered on smaller valve assemblies as an option. Standard fea- tures include 2 SPDT fully adjustable auxiliary switches KBV-2-6-E2SO (two-position only), manual override crank, and an inter- assembly includes nal heater to prevent condensation in outdoor installa- VSI-BB1020 actuator tions. SPECIFICATIONS FEATURES Power 120 VAC standard •Lightweight, compact design Models 1005 to 1020 12/24 VDC optional • Two-position or modulating control Models 1005 to 1040 24 VAC optional • Two-position battery-backed models Torque range 347-17,359 in-lb • NEMA 4X watertight, corrosion-resistant housing Motor 120 VAC, 1 phase, 60 Hz; • Integral position indicator enclosed, non-ventilated, high • Space heater standard starting torque, reversible induc- • Two 1/2" conduit connections tion, Class E insulation • Detachable manual override crank Thermal overload Auto reset, embedded • Terminal strip wiring Travel limit switches Cam operated, adjustable SPDT • Worm gear drive, no electro-mechanical brake for open/close stop required • Mounting orientation in any direction Position indicator High-visibility graduated dial • 4-20 mA or 500Ω optional feedback signal Conduit connections -

Norman Identity and Historiography in the 11Th-12Th Centuries

Butler Journal of Undergraduate Research Volume 5 2019 The Comedia Normannorum: Norman Identity and Historiography in the 11th-12th Centuries Patrick Stroud Wabash College Follow this and additional works at: https://digitalcommons.butler.edu/bjur Recommended Citation Stroud, Patrick (2019) "The Comedia Normannorum: Norman Identity and Historiography in the 11th-12th Centuries," Butler Journal of Undergraduate Research: Vol. 5 , Article 10. Retrieved from: https://digitalcommons.butler.edu/bjur/vol5/iss1/10 This Article is brought to you for free and open access by the Undergraduate Scholarship at Digital Commons @ Butler University. It has been accepted for inclusion in Butler Journal of Undergraduate Research by an authorized editor of Digital Commons @ Butler University. For more information, please contact [email protected]. BUTLER JOURNAL OF UNDERGRADUATE RESEARCH, VOLUME 5 THE COMEDIA NORMANNORUM: NORMAN IDENTITY AND HISTORIOGRAPHY IN THE 11TH-12TH CENTURIES PATRICK STROUD, WABASH COLLEGE MENTOR: STEPHEN MORILLO Introduction—How Symbols and Ethnography Tie to Historical Myth Since the 1970s, historians have tried many different methodologies for exploring texts. Because multiple paradigms tempt the historian’s gaze, medieval texts can often befuddle readers in their hagiographies and chronologies. At the same time, these texts also give the historian a unique opportunity in the form of cultural insight. In his 1995 work Making History: The Normans and their Historians in Eleventh-Century Italy, Kenneth Baxter Wolf discusses a text’s role in medieval historiography. A professor of History at Pomona College, Wolf divides historical commentary on medieval primary sources into two ends of a spectrum. While one end worries itself on the accuracy and classical “truth” of a source, the other end, postmodern historiography, uses historical records “to tell us how the people who wrote them conceived of the events occurring in the world around them.”1 The historian treats a medieval text as a launching pad for cultural analysis. -

Lambert Walcot Kadmos 4 Dunnu

WARNING OF COPYRIGHT RESTRICTIONS1 The copyright law of the United States (Title 17, U.S. Code) governs the maKing of photocopies or other reproductions of the copyright materials. Under certain conditions specified in the law, library and archives are authorized to furnish a photocopy or reproduction. One of these specified conditions is that the photocopy or reproduction is not to be “used for any purpose other than in private study, scholarship, or research.” If a user maKes a reQuest for, or later uses, a photocopy or reproduction for purposes in excess of “fair use,” that user may be liable for copyright infringement. The Yale University Library reserves the right to refuse to accept a copying order, if, in its judgement fulfillment of the order would involve violation of copyright law. 137 C.F.R. §201.14 2018 KADMOS ZEITSCHRIFT FOR VOR- UND FRÜHGRIECHISCIIE EPIGRAPHIK IN VERBINDUNG MIT: EMMETT L. BENNETT-MADISON • WILLIAM C. BRICE-MANCHESTER PORPHYRIOS DIKAIOS-WALTHAM • KONSTANTINOS D. KTISTOPOULOS ATHENN. OLIVIER MASSON-PARIS • PIERO MERIGGI-PAVIA • FRITZ SCHACHE RMEYR-WIEN - JOHANNES SUNDWALL-HELSINGFORS HERAUSGEGEBEN VON ERNST GRUMACH BAND IV / HEFT 1 WA LTER DE G R U Y T E R & CO. / BERLIN LUNG - J. G. VERLAG 1TAhCOMP. ~ U CHHANDLUUNG -EORGG REIMER SK IKARL J.TRUBNER TTVE 1965 WILFRED G. LAMBERT and PETER WALCOT1 A NEW BABYLONIAN THEOGONY AND HESIOD A volume of cuneiform texts just published by the British Museum2 contains a short theogony, which is of interest to Classical scholars since it is closer to Hesiod's opening list of gods than any other cuneiform material of this category. -

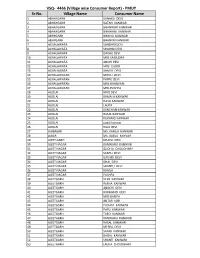

Sr No. Village Name Consumer Name VSQ- 4466 (Village Wise Consumer Report)

VSQ- 4466 (Village wise Consumer Report) - PMUY Sr No. Village Name Consumer Name 1 ABHAYGARH KANAKU DEVI 2 ABHAYGARH RATAN KANWAR 3 ABHAYGARH BHANWAR KANWAR 4 ABHAYGARH BHAWANI KANWAR 5 ABHYGARH BHIKHU KANWAR 6 ABHYGARH BHANVRI KANWAR 7 ACHALAWATA SUNDARI DEVI 8 ACHALAWATA SHOBHA DEVI 9 ACHALAWATA DAKHU DEVI 10 ACHALAWATA MRS SAMUDRA 11 ACHALAWATA ANOPI DEVI 12 ACHALAWATA MRS GUDDI 13 ACHALAWATA KAMLA DEVI 14 ACHALAWATAN MOOLI DEVI 15 ACHALAWATAN PAPPU DEVI 16 ACHALAWATAN MRS BHANVARI 17 ACHALAWATAN MRS PUSHPA 18 AGOLAI HIRO DEVI 19 AGOLAI KAMALA KANWAR 20 AGOLAI HAVA KANWAR 21 AGOLAI LALITA 22 AGOLAI KANCHAN KANWAR 23 AGOLAI RASAL KANWAR 24 AGOLAI RUKAMO KANWAR 25 AGOLAI guddi kanwar 26 AGOLAI RAJO DEVI 27 AJABASAR MS. KAMLA KANWAR 28 AJBAR MS. BABLU KANVAR 29 AJEET GARH DHAPU DEVI 30 AJEET NAGAR KANWARU KANWAR 31 AJEET NAGAR GUDIYA CHOUDHARY 32 AJEET NAGAR SANTU DEVI 33 AJEET NAGAR GAVARI DEVI 34 AJEET NAGAR DHAI DEVI 35 AJEET NAGAR SHANTU DEVI 36 AJEET NAGAR KAMLA . 37 AJEET NAGAR PUSHPA . 38 AJEETGARH VEER KANWAR 39 AJEETGARH REKHA KANWAR 40 AJEETGARH ANACHI DEVI 41 AJEETGARH RUKHAMO DEVI 42 AJEETGARH MRS BABITA 43 AJEETGARH ANTAR KOR 44 AJEETGARH PUSHPA KANWAR 45 AJEETGARH PAPU KANWAR 46 AJEETGARH TARO KANWAR 47 AJEETGARH KANWARU KANWAR 48 AJEETGARH RASAL KANWAR 49 AJEETGARH MEERA DEVI 50 AJEETGARH SAYAR KANWAR 51 AJEETGARH BADAL KANWAR 52 AJEETGARH SHANTI KANWAR 53 AJEETGARH LALITA CHOUDHARY Sr No. Village Name Consumer Name 54 AJEETGARH PEP KANWAR 55 AJEETGARH RASAL KANWAR 56 AJEETGARH JASU KANWAR 57 AJEETGARH LILA KANWAR 58 AJEETGARH KHAMMA DEVI 59 AJIT GADH SUGAN KANWAR 60 AJITGARH CHIMU DEVI 61 AJITGARH KANWARU KANWAR 62 AJJETGADH SOHNI DEVI 63 AKADEEYAWALA MAGEJ KANWAR 64 ALIDAS NAGAR PAPPU KANWAR 65 ALIDAS NAGAR PARVATI DEVI 66 ALIDAS NAGAR NAINU KANWAR 67 ALIDAS NAGAR MOHANI DEVI 68 ALIDAS NAGAR PISTA DEVI 69 ALIDAS NAGAR PRAKASH KANWAR 70 ALIDAS NAGAR NAKHTU DEVI 71 ALIDAS NAGAR DHAPU . -

Mesopotamian Culture

MESOPOTAMIAN CULTURE WORK DONE BY MANUEL D. N. 1ºA MESOPOTAMIAN GODS The Sumerians practiced a polytheistic religion , with anthropomorphic monotheistic and some gods representing forces or presences in the world , as he would later Greek civilization. In their beliefs state that the gods originally created humans so that they serve them servants , but when they were released too , because they thought they could become dominated by their large number . Many stories in Sumerian religion appear homologous to stories in other religions of the Middle East. For example , the biblical account of the creation of man , the culture of The Elamites , and the narrative of the flood and Noah's ark closely resembles the Assyrian stories. The Sumerian gods have distinctly similar representations in Akkadian , Canaanite religions and other cultures . Some of the stories and deities have their Greek parallels , such as the descent of Inanna to the underworld ( Irkalla ) resembles the story of Persephone. COSMOGONY Cosmogony Cosmology sumeria. The universe first appeared when Nammu , formless abyss was opened itself and in an act of self- procreation gave birth to An ( Anu ) ( sky god ) and Ki ( goddess of the Earth ), commonly referred to as Ninhursag . Binding of Anu (An) and Ki produced Enlil , Mr. Wind , who eventually became the leader of the gods. Then Enlil was banished from Dilmun (the home of the gods) because of the violation of Ninlil , of which he had a son , Sin ( moon god ) , also known as Nanna . No Ningal and gave birth to Inanna ( goddess of love and war ) and Utu or Shamash ( the sun god ) . -

A Comparison of the Role of Bārû and Mantis in Ancient Warfare

A Comparison of the Role of Bārû and Mantis in Ancient Warfare Krzysztof Ulanowski Divination played a huge role in both the Mesopotamian and Greek civiliza- tions. Diviners were consulted by their clients in all possible situations. The results of divination were especially important during times of war, when asso- ciated with the very life of the king along with thousands of others. Divination was a salient characteristic of Mesopotamian civilization; likewise, in Greek politics and warfare, a leader who ignored omens would incur the ominous anger impressions of those by whom he was followed.1 In this paper I will compare the role and responsibility of diviners in two different civilizations in relation to the affairs of war. What did the Assyrian bārû and the Greek mantis (μάντις) have in common and in what ways did they differ? Could they really decide the course of battles? Would it be possible to describe the skills of the bārû priest in the words of Euripides: “the best mantis is he who guesses well”?2 War When writing systems first appeared in the history of both Mesopotamian and Greek civilizations, the first written works not only had a codifying- mythological nature, but above all a military character. Weil’s essay, L’Iliade ou le poème de la force holds that “the true hero, the true subject at the centre of the Iliad is force”.3 Homer was the poet of war and the Iliad needs hardly be mentioned. In the case of Mesopotamian civilization, one could refer not only to The Gilgamesh Epic, but also to many other Sumerian, and therefore early texts which have war as a leading motif, such as The Victory of Eanatum 1 M.A. -

2020 Ambient Air Monitoring Network 5-Year Assessment

State of Hawaii 2020 Ambient Air Monitoring Network 5-Year Assessment Prepared by: State of Hawaii Department of Health Environmental Management Division Clean Air Branch July 1, 2020 Document No. CABMA-5YRA-2020-v01 Table of Contents List of Tables .......................................................................................................... iii List of Figures .......................................................................................................... iii Abbreviations and Definitions .................................................................................. iv I. Executive Summary ................................................................................................. 1 A. Purpose of Assessment .................................................................................... 1 B. Ambient Air Monitoring Networks ...................................................................... 1 C. Summary of 2015 Findings ............................................................................... 1 II. Introduction .............................................................................................................. 3 III. Current Air Monitoring in the State of Hawaii ........................................................... 4 IV. Climate, Population and Emission Source Characteristics ...................................... 7 A. Climate and Topography ................................................................................... 7 B. Population ......................................................................................................