Entertainment and Media Outlook: 2013 – 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SADC Today 15.1 English:Layout 1

SADC TODAY Vol. 15 No 1 December 2012 Energy Sector Plan targets surplus, sets priorities by Joseph Ngwawi THE SADC region has suffered a shortage of The Plan identifies “hard” infrastructure electricity since 2007 as demand exceeds sup- projects that include the planned increase in ply, and the expectation is that this energy gap electricity generation and transmission; refiner- will be addressed by 2014. However, the imple- ies, storage facilities and pipelines for petro- mentation of projects can lag behind their leum and gas; and transport facilities for coal POLICY 3 planned dates due to a lack of funding and distribution and exports. other constraints. The plan for the energy sector has identified ENERGY 4 SADC is now taking longer term measures 73 power generation projects to increase gen- AFRICAN UNION 5 to address the energy deficit and ensure self- eration from the current 56,000 megawatts sufficiency in energy generation and an end to (MW) and ensure that the projected demand of YEAR IN REVIEW 6 electricity shortages, through an ambitious En- 96,000 MW is surpassed by 2027. ergy Sector Plan that calls for the region to in- Prioritisation of the various projects was de- PEACE & SECURITY 7 crease power generation by more than 70 termined using a formula under which projects percent and invest at least US$170 billion over were rated according to their ability to impact ENERGY 8-9 the next 15 years. on the regional energy deficit. ENVIRONMENT 10 The Energy Sector Plan is part of the SADC Seven generation projects that scored above Regional Infrastructure Development Master 50 percent and with capacity greater than CLIMATE CHANGE 11 Plan approved by the 32nd Summit of SADC 1,000MW each were ranked as top priority. -

Jacaranda Fm in Essence

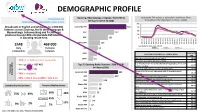

DEMOGRAPHIC PROFILE Gauteng, Mpumalanga, Limpopo, North West Jacaranda FM enjoys a consistent audience flow JACARANDA FM Afrikaans LSM 8-10 (000) throughout the day (Mon to Sun) – (000) PERFORMANCE HIGHLIGHTS (Part 1 of 2) 200 Broadcasts in English and Afrikaans to 1 004 000 Jacaranda FM 366 150 listeners across Gauteng, North West, Limpopo & 100 Mpumalanga. Johannesburg and Pretoria are 947 247 pivotal areas and 84% of Jacaranda FM listeners 50 in Gauteng reside here. RSG 185 0 Metro FM 109 0100-0200 0200-0300 0300-0400 0400-0500 0500-0600 0600-0700 0700-0800 0800-0900 0900-1000 1000-1100 1100-1200 1200-1300 1300-1400 1600-1700 1700-1800 1800-1900 1900-2000 2100-2200 2300-2400 0000-0100 1400-1500 1500-1600 2000-2100 2200-2300 1h48 469 000 Ave Qhr by hr, Mon – Sun, ADULTS Daily Exclusive 702 88 M-F SAT SUN Listenership Listeners Jacaranda 5FM 80 LIFESTYLE STATEMENTS - AGREE WITH FM OFM 44 I am very conscious about my health 48.8% • 47% of individuals listen exclusively I consider my diet to be very healthy 43.4% It is important for me to include lots of vegetables, fruit and • Average HHI of R27 482 Top 10 Gauteng Radio Stations : SEM 8-10 & 63.4% salad in my diet Afrikaans (000) • Average age of 41 You can judge a person by the car they drive 44.0% Jacaranda FM 297 My car should be well equipped with all possible safety Exclusive 52.5% • 70% is employed features Listenership 947 257 My car should express my personality 48.8% • 63% in LSM 8-10 and 60% in SEM 9-10 Comfort is the most important thing in a car 51.6% RSG 138 I love to buy new gadgets and appliances 46.9% Metro FM 95 I do extensive research before purchasing an electronic Listenership by location Listenership by device 44.4% item. -

Employment Equity Act (55/1998): 2019 Employment Equity Public Register in Terms of Section 41 43528 PUBLIC REGISTER NOTICE

STAATSKOERANT, 17 JULIE 2020 No. 43528 31 Employment and Labour, Department of/ Indiensneming en Arbeid, Departement van DEPARTMENT OF EMPLOYMENT AND LABOUR NO. 779 17 JULY 2020 779 Employment Equity Act (55/1998): 2019 Employment Equity Public Register in terms of Section 41 43528 PUBLIC REGISTER NOTICE EMPLOYMENT EQUITY ACT, 1998 (ACT NO. 55 OF 1998) I, Thembelani Thulas Nxesi, Minister of Employment and Labour, publish in the attached Schedule hereto, the register maintained in terms of Section 41 of the Employment Equity Act, 1998 (Act No. 55 of 1998) of designated employers that have submitted employment equity reports in terms of Section 21, of the Employment Equity Act, Act No. 55 of 1998 as amended. MR.lWNXESI, MP MINISTER OF EMPLOYMENT AND LABOUR ')..,6j oZ> do:2,"eJ 1/ ---------------------------------------------------------------------------------------------------- ISAZISO SEREJISTA YOLUNTU UMTHETHO WOKULUNGELELANISA INGQESHO, (UMTHETHO YINOMBOLO YAMA-55 KA-1998) Mna, Thembelani Thulas Nxesi, uMphathiswa wezengqesho kanye nezabasebenzi, ndipapasha kule Shedyuli iqhakamshelwe apha, irejista egcina ngokwemiqathango yeCandelo 41 lomThetho wokuLungelelanisa iNgqesho, ka- 1998 (umThetho oyiNombolo yama-55 ka-1998) izikhundla zabaqeshi abangenise iingxelo zokuLungelelanisa iNgqesho ngokwemigaqo yeCandelo 21, lo mThetho wokulungelelanisa iNgqesho, umThetho oyiNombolo yama-55 ka- 1998. -6'';7MR.TW NXESI, MP UMPHATHISWA WEZENGQESHO KANYE NEZABASEBENZI 26/tJ :20;:J,()1/ This gazette is also available free online at www.gpwonline.co.za 32 No. 43528 GOVERNMENT GAZETTE, 17 JULY 2020 List of designated employers who reported for the 1 September 2019 reporting cycle Description of terms: No: This represents sequential numbering of designated employers & bears no relation to an employer. (The list consists of 5969 large employers & 21158 small employers). -

November 2014

FREE November 2014 OFFICIAL PROGRAMME www.worldrugby.bm GOLF TouRNAMENt REFEREEs LIAIsON Michael Jenkins Derek Bevan mbe • John Weale GROuNds RuCK & ROLL FRONt stREEt Cameron Madeiros • Chris Finsness Ronan Kane • Jenny Kane Tristan Loescher Michael Kane Trevor Madeiros (National Sports Centre) tEAM LIAIsONs Committees GRAPHICs Chief - Pat McHugh Carole Havercroft Argentina - Corbus Vermaak PREsIdENt LEGAL & FINANCIAL Canada - Jack Rhind Classic Lions - Simon Carruthers John Kane, mbe Kim White • Steve Woodward • Ken O’Neill France - Marc Morabito VICE PREsIdENt MEdICAL FACILItIEs Italy - Guido Brambilla Kim White Dr. Annabel Carter • Dr. Angela Marini New Zealand - Brett Henshilwood ACCOMMOdAtION Shelley Fortnum (Massage Therapists) South Africa - Gareth Tavares Hilda Matcham (Classic Lions) Maureen Ryan (Physiotherapists) United States - Craig Smith Sue Gorbutt (Canada) MEMbERs tENt TouRNAMENt REFEREE AdMINIstRAtION Alex O'Neill • Rick Evans Derek Bevan mbe Julie Butler Alan Gorbutt • Vicki Johnston HONORARy MEMbERs CLAssIC CLub Harry Patchett • Phil Taylor C V “Jim” Woolridge CBE Martine Purssell • Peter Kyle MERCHANdIsE (Former Minister of Tourism) CLAssIC GAs & WEbsItE Valerie Cheape • Debbie DeSilva Mike Roberts (Wales & the Lions) Neil Redburn Allan Martin (Wales & the Lions) OVERsEAs COMMENtARy & INtERVIEWs Willie John McBride (Ireland & the Lions) Argentina - Rodolfo Ventura JPR Williams (Wales & the Lions) Hugh Cahill (Irish Television) British Isles - Alan Martin Michael Jenkins • Harry Patchett Rodolfo Ventura (Argentina) -

Analysing Rugby Game Attendance at Selected Smaller Unions in South Africa

Analysing rugby game attendance at selected smaller unions in South Africa by PAUL HEYNS 12527521 B.Com (Hons), NGOS Mini-dissertation submitted in partial fulfilment of the requirements for the degree Master of Business Administration at the Potchefstroom Business School of the North-West University Supervisor: Prof. R.A. Lotriet November 2012 Potchefstroom ABSTRACT Rugby union is being viewed and played by millions of people across the world. It is one of the fastest growing sport codes internationally and with more countries emerging and playing international and national games, the supporter attendance is crucial to the game. The rugby industry is mostly formal, with an international body controlling the sport globally and a governing body in each country to regulate the sport in terms of rules and regulations. These bodies must adhere to the international body’s vision and mission to grow the sport and to steer it in the correct direction. This study focuses on rugby game attendance of selected smaller unions in South Africa. Valuable information was gathered describing the socio- economic profile and various preferences and habits of supporters attending rugby games. This information forms the basis for future studies to honour the people that support their unions when playing rugby nationally or internationally. The research was conducted through interviews with influential administrators within the rugby environment and questionnaires that were distributed among supporters that attended a Leopard and Puma game. The main conclusions during the study were the failure to attract supporters to the Leopards and the Pumas local matches. The supporters list various reasons for poor supporter attendances namely: a lack of marketing, no entertainment, the quality of the teams that are competing, and the time-slots in which the matches take place. -

In This Issue

2016/2017 ISSUE 3 Message from Border Cricket CEO Spring is upon us and the cricketers are working hard at training attendance and contributions at such meetings. and adding to the noise levels down the corridor which was The Border Team under the guidance of Coach Frank Plaatjes and somewhat quieter during the winter period. I take this opportunity captain Martin Walters are ready for a bumper season. We have to welcome you to the start of the 2016/17 season. confidence that their results will improve from last season and we can again compete in the finals of the one-day competition, as we The team prepared well for the Africa T20 Cup. We were all geared are well known for our performances in the limited up for a great competition, however the weather Gods were not on over competition. our side. We will work to ensure that the lucky draw will soon be a distant memory. Our Border team performed exceptionally well Our Women’s team performed so well last season and we have and we look forward their campaigns this season. The rain factor every confidence yet again that they will bring back the silverware however is uncontrollable and we hope that it will not hamper too and set new milestones. many of our cricket matches this season. We are busy updating our website and will soon have all our Off the field we received an unqualified audit during this season updated programmes, fixtures and courses for the season. with a profit of R 3.1 million, our revenue jumping to R38 million. -

STATE of the NEWSROOM SOUTH AFRICA2 013 Disruptions and Transitions

STATE OF THE NEWSROOM SOUTH AFRICA2 013 Disruptions and Transitions Glenda Daniels Lead Researcher and Project Co-ordinator: Dr Glenda Daniels For Wits Journalism: Prof Anton Harber and Prof Franz Krüger Wits Journalism student researchers: Kagiso Ledikwa, Taurai Maduna, Ebrahim Moolla, Mackson Muyambo and Camilla Bath Copy editor: Gill Moodie/Grubstreet Design and Layout: Hothouse South Africa Proof reader: Ruth Becker Photography: TJ Lemon, Pheladi Sethusa, Madelene Cronje, Liesl Frankson Special thanks: to Dr Julie Reid, Kelly Hawkins (both from Unisa), Joe Thloloe and Dr Johan Retief for information on the Press Council and Ombudsman rulings, to Jenny Tennant from Big Media for reading and commenting, and to Dinesh Balliah for general help. Publisher: Wits Journalism, University of the Witwatersrand Electronic copies can be accessed at: journalism.co.za/newsroom2013 CONTENTS PREFACE iii EXECUTIVE SUMMARY v 01 THE MEDIA LANDSCAPE 1 The Print Media Circulation Cutting Costs Ownership New Developments Transformation Community Media and Independent Publishing The Broadcast Landscape Television Audience Figures The Move to Digital Terrestrial Television (DTT) Radio The Internet, Paywalls, Apps and Mobis 02 THE LEGAL, POLITICAL AND REGULATORY LANDSCAPE 15 The Protection of State Information Bill/Secrecy Bill Amendments and Outstanding Problems Other Laws Impacting on Journalism From Self-regulation to Independent Co-regulation Freedom of Expression 03 RACE AND GENDER TRANSFORMATION 22 A Look Back in Time Employment Equity Policies Race and -

Centurion Lifestyle Centre Shopper Profile

Shopper profile Contents RETAIL The value of the data 1 Mall demographic profile 2 Shopper media consumption 4 Sample size: 909 Weighted to SA shopper: 339 000 The value of the data The following data has been collected and verified by Ask Afrika Group, the copyright license holder for Target Group Index (TGI). Ask Afrika Group is the largest independent South African market research company with fieldwork capabilities in 95% of Sub-Saharan Africa. They are backed by the power of TGI Research, the only SA population database with psychographics that cover over 600 lifestyle and attitude statements. TGI is South Africa’s broadest consumer/shopper profiling tool in sampling 24 000 nationally representative respondents aged 15+, living in communities 8 000+. Insights are tailor-suited for malls, which link demographic, psychographic, brand and media insights. TGI supports strategic and informed decision making. Page 1 Mall demographic profile RETAIL SA shopper SA shopper vs Centurion Lifestyle Centre shopper Age Race Gender LSM 3.4% 61.1% 65+ Black 7.1% 73.1% 50.7% 21.5% 31.1% 49.8% 45-64 White 23.2% 10.6% 28.4% 1.6% 35-44 Coloured 22.5% 12.2% 49.3% 6.3% 33.5% Indian/ 6.2% 50.2% 3.9% 25-34 2.3% 25.6% 29.1% Asian 4.2% 11.7% 9% 14.6% 36.4% 13.6% 14.1% 12.6% 23.7% 10.2% 15.9% 4 5 6 7 8 9 10 13.2% 15-24 18% Most important media used* 0.6% 20.6% 3.7% 2.3% 5.2% 3.6% 7.9% 14.4% 42.8% 2% 16% 4.4% 3.3% 6% 5.4% 6% 9.2% 48.4% Cinema In-store Outdoor Internet Internet Magazines Newspapers Radio TV (Billboards and posters) (Desktop) (Mobile) *Based on those that have visited a mall in the past three months/*2018C TGI Data. -

C:\Users\Patricia\Documents\ACFN Shell Hearings\ACFN Report Text.11

1. Introduction and Terms of Reference I was invited by Chief Allan Adam of the Athabasca Chipewyan First Nation to work on its behalf as it prepared for the hearings for Shell’s proposed Jackpine Mine Expansion and new Pierre River Mine (letter 18 Nov. 2010). Sean Nixon, with Woodward & Company LLP, then provided me with terms of reference to follow in writing an expert report (e-mail letter 21 Dec. 2010): 1. Provide an ethnographic description of the people who now form Athabasca Chipewyan First Nation, including an analysis of how traditional band structures differ from those created by virtue of the Indian Act . 2. Describe how ACFN passed on their culture and cultural practices to future generations (e.g., what were their oral history traditions?). 3. Provide a description of ACFN traditional territory or traditional lands, including: a. whether there was a pre-contact (and/or pre-Treaty) concept of ACFN territory, b. the extent to which ACFN moved around within their territory (including: the amount of space required to carry out their traditional activities; the need to be respectful of others’ rights; and the depletion of resources), c. “axes” of ACFN territory (if this concept is relevant to ACFN), d. whether there was any amalgamation of groups (e.g., was there any overlap between local groups and bands through marriage and family connections?), e. whether there was any effect of the formation of a separate First Nation at Fort MacKay on ACFN membership and on its relation to the “southern territories” (i.e., the southern portions of ACFN traditional territory or traditional lands)? 4. -

947 Station Profile the Station

947 STATION PROFILE THE STATION If Joburg is South Africa’s heart, then 947 is its racing pulse. We keep listeners connected to the city, engaged with the boldest personalities and moving to the biggest hits – all day and all night. Wake up with a smile with Nick Explicit, then sit down for breakfast with Anele and the Club on 947. Your workday is a breeze with non-stop beats and the city’s hottest happenings courtesy of Msizi James and Ayanda MVP. Then at the end of another glorious Joburg day, head home with 947 Drive with Thando and stay entertained into the night with Zweli and Chrizz Beatz. 947 is all about having fun in Joburg. We give you a lift when you need it and a laugh when you least expect it. Our social sites are flaming hot with presenter-generated content, videos, competitions and more. Our passion is changing lives in Joburg by amplifying the generosity of its people. If you love Joburg, 947 loves you! Tune into 94.7 FM every day and never miss a beat. Visit 947 online at www.947.co.za Twitter: #947Joburg Facebook: @947Joburg Download the 947 App (iOS & Android) HEADSPACE According to our AudioScope Wave 1 research, 947 listeners: Varied levels of wealth Creative trendsetters These listeners are spread across The 947 listener is more likely the wealth spectrum-with the to be described as being a majority of them considering creative intellectual who is themselves to be middle class- more likely to set trends upper middle class Responsible for purchases Entertainment 80% are responsible for These listeners are more purchases -

남아프리카공화국 Republic of South Africa

남아프리카공화국 REPUBLIC OF SOUTH AFRICA 01 | 정보통신(ICT)・방송 _ 정책 현황 02 | 정보통신(ICT)・방송 _ 품목 현황 03 | 정보통신(ICT)・방송 _ 사업자 현황 04 | 정보통신(ICT)・방송 _ 협력 현황 남아프리카공화국 정보통신(ICT)・방송 시장 주요 이슈 ■ 시장 - 2015년 12월 말 기준, 재원 확보의 어려움과 디지털 셋톱박스 보급 실패 등으로 남아공의 디지털 방송 전환은 지연 상태 - 2015년 7월, 남아공 법무부는 개인정보보호법 준수 여부를 감독할 정보 규제당국 설립 절차 착수 - 남아공은 온라인 사기와 피싱 공격으로 인해 연간 22억 랜드 이상의 피해가 발생 - 2014년 남아공 디지털 TV 보유가구 수는 597만 가구로 2013년 대비 11.5% 증가 - 2014년 남아공의 이동통신 가입자 수는 2013년 대비 3.4% 증가한 7,954만 명, 보급률은 149.7%로 집계 ■ 사업자 - 2014년 말 Telkom은 LTE-Advanced 네트워크를 남아공 외곽 5개 지역을 대상으로 증설 - Telkom은 2018년 3월 말까지 100만 가구를 커버리지 대상으로 광네트워크 구축 계획 수립 - 2015년 12월 Vodacom, 유선 사업자 Neotel의 이동통신 부문을 제외한 자산 인수案에 합의 - Cell C, 2015년 12월부터 Western Cape 지역을 중심으로 LTE 서비스 제공 개시 1. 정보통신(ICT)・방송 정책 현황 1.1. 정보통신(ICT)・방송 정책 및 규제 기관 정보통신(ICT)・방송 주무 기관 정보통신(ICT) 및 우편 부문 정책 수립 - 통신우편서비스부(Department of Telecommunications and Postal Services, DTPS) 남아공의 미디어, 방송, 영화, 출판 산업 및 공보부문 담당 - 통신부(Department of Communications, DOC) 정보통신(ICT)・방송 및 우편 부문 규제 - 독립통신청(Independent Communication Authority of South Africa, ICASA) 정보통신(ICT)・방송 관련 업무 구조 정보통신(ICT)・방송 정책 주요 계획 국가 브로드밴드 정책(SA Initiative) - 2010년 6월, 남아공 정부는 국가 브로드밴드 정책을 승인, 상기 계획은 2020년까지 추진되며, 同 계획의 비전은 적절한 가격에 안정된 브로드밴드 서비스를 보편적으로 이용할 수 있도록 보급 추구 독립통신청(ICASA) 2013~2017년 5개년 계획 - 브로드밴드 보급, 주파수 발급, 디지털 지상파 방송 리뷰, 적합한 규제 시행 등이 포함됨 디지털 지상파 방송 전환 계획 - 남아공은 당초 2011년 11월 1일을 디지털 지상파 방송 전환 완료일로 결정했으나, 2009년 9월 일정이 촉박하다고 판단한 독립통신청(ICASA)은 2013년으로 연기함 - 이후 2016년 6월로 다시 연기를 했으나, 2015년 12월 기준 디지털 방송 전환 관련 관계부처 장관들 간의 불협화음과 디지털 셋톱박스 보급 문제 등으로 인해 재차 지연되고 있는 상황 108 | 정보통신산업진흥원 정보통신(ICT) -

Media Development and Diversity Agency Postion Paper

T h e Medi a De vel opme nt and Div ersi ty A g e n c y The Position Paper process The Media Development and Diversity Agency (MDDA) Position Paper was finalised taking into account public comments received in February 2001, the public hearings conducted by the parliamentary Portfolio Committee on Communication in March 2001, and consultations with stakeholders throughout 2001. This Position Paper contains the underlying philosophy and rationale of the MDDA, and as such represents government policy that has guided the drafting of the MDDA Bill, which will be debated in Parliament during 2002. The Executive Summary is available in all official languages on request. This Position Paper is also available on the GCIS website: http://www.gcis.gov.za page 1 "Everyone has a right to freedom of expression, which includes: (a) freedom of the press and other media, and (b) freedom to receive or impart information or ideas." From the South African Constitution, Chapter Two, Section 16 "Open debate and transparency in government and society are crucial elements of reconstruction and development. This requires an information policy which guarantees active exchange of information and opinion among all members of society…….. The democratic government must encourage the development of all tiers of media – public, community and private. However, it must seek to correct the skewed legacy of apartheid where public media were turned into instruments of National Party policy; where community media were repressed; where private media are concentrat- ed in the hands of a few monopolies, and where a few individuals from the white community determine the content of media.