Janfeb 2009.Qxd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

7-8 PR2 Annex

TRACECA Civil Aviation Safety PROGRESS REPORT n° 2 08/01/2010 Security & Environment Project Annex 7.8: ETS Seminar report – Istanbul, December 2009 TRACECA CIVIL AVIATION Safety, Security & Environment Project EUROPEAID/125350/C/SER/MULTI TRACECA CIVIL AVIATION Safety Security & Environment Project Ref. Contract ENPI 2008/150-669 Aviation Environment and ETS Seminar Report January 2010 Ayce Celikel ([email protected] ) TRACECA CIVIL AVIATION Safety, Security & Environment Project Executive Summary Organisation of the event TRACECA Civil Aviation Project Environmental Key Expert Ayce Celikel organised the Aviation ETS seminar which is hold in Istanbul 14-15 th December 2009 as part of Work Package 3. Although the time was very limited to organise such event in 6 weeks time and COP15 in parallel, the vide attendance from Beneficiaries and high level experts from EU officials, the top 2 ETS reporting country ministry levels (UK and Germany), industries (NATS, EUROCONTROL), airlines organisations (IATA, TAROM), experts from organisations and expert consultants (SABRE, SITA, DLR, Lufthansa Consulting) are provided. Purpose of the Seminar & Target groups During the assessment phase in WP1 for environmental issues, one of the main areas to improve is found to be the lack of information on aviation inclusion to European ETS. Given the deadline of ETS implementation for third countries, it is foreseen to be foremost important issue to tackle. Therefore the seminar is organised for TRACECA Beneficiary Countries in Istanbul, dealing with the issues surrounding “Aviation Environment and ETS” covering the discussions on aviation inclusion to emission trading system and European Climate Change policy issues. Target groups were; TRACECA region Civil Aviation Authorities, Airlines and other interested parties from the region; The speakers were chosen among EU officials, international and European experts. -

6. Current Status of the Environment

6. Current Status of the Environment 6.1. Natural Environment 6.1.1. Desertification Kazakhstan has more deserts within its territory than any other Central Asian country, and approximately 66% of the national land is vulnerable to desertification in various degrees. Desertification is expanding under the influence of natural and artificial factors, and some people, called “environmental refugees,” are obliged to leave their settlements due to worsened living environments. In addition, the Government of RK (Republic of Kazakhstan) issued an alarm in the “Environmental Security Concept of the Republic of Kazakhstan 2004-2015” that the crisis of desertification is not only confined to Kazakhstan but could raise problems such as border-crossing emigration caused by the rise of sandstorms as well as the transfer of pollutants to distant locations driven by large air masses. (1) Major factors for desertification Desertification is taking place due to the artificial factors listed below as well as climate, topographic and other natural factors. • Accumulated industrial wastes after extraction of mineral resources and construction of roads, pipelines and other structures • Intensive grazing of livestock (overgrazing) • Lack of farming technology • Regulated runoff to rivers • Destruction of forests 1) Extraction of mineral resources Wastes accumulated after extraction of mineral resources have serious effects on the land. Exploration for oil and natural gas requires vast areas of land reaching as much as 17 million hectares for construction of transportation systems, approximately 10 million hectares of which is reportedly suffering ecosystem degradation. 2) Overgrazing Overgrazing is the abuse of pastures by increasing numbers of livestock. In the grazing lands in mountainous areas for example, the area allocated to each sheep for grazing is 0.5 hectares, compared to the typical grazing space of 2 to 4 hectares per sheep. -

WEEK of STOCK MARKET of KAZAKHSTAN September 12 - 18

WEEK OF STOCK MARKET OF KAZAKHSTAN September 12 - 18 Money market indicators as of September 18 and Investment attractiveness of stock exchange instruments weekly changes from September 12 to September 18 Term Currency Rate Trend Financial Currency of Yield, % APR “Overnight” on autorepo at KASE(TONIA) instrument transaction value trend 1 day KZT 4.44 +0.03 Instruments denominated in national currency, tenge Repo opening at KASE (WA, % APR) TXBNb1 KZT 15.00 0 1 day KZT 4.44 +0.05 CS repo KZT *9.56 -1.64 7 days KZT 4.50 -0.18 МЕОКАМ, МЕАКАМ KZT 8.98 +1.31 14 days KZT 5.20 +0.20 МЕККАМ, notes KZT *5.39 +0.10 28 days KZT 6.50 +0.85 GS repo KZT *4.34 -0.44 KIBOR (indicative, % APR) Instruments indexed by devaluation 1 week KZT 6.83 -0.84 SMGZb1 USD 13.36 +0.20 2 weeks KZT 7.92 -0.58 ALKSb2 USD 11.88 +0.01 1 month KZT 9.00 -0.50 VTBNb1 USD 11.07 -0.43 2 months KZT 10.08 -0.25 KARMb1 USD 10.97 +0.85 3 months KZT 10.92 -0.08 ASFIb2 USD 10.97 0 RGBRb2 USD 10.83 +1.83 KZASb1 USD 10.82 -0.02 Stock market indicators as of September 18 TEBNb2 USD 10.80 -0.04 and their weekly change BTASb2 USD 10.36 -0.01 Index Value Trend BTASb1 USD 10.27 0 Shares of “А” listing TEBNb USD 10.09 +0.02 KASE_Shares 112.11 -0.07% ASFIb1 USD 10.05 -0.01 Corporate bonds of “А” listing CSBNb1 USD 10.00 0 KASE_BP 128.45 +0.40% CCBNb2 USD 9.91 +0.04 KASE_BC 107.06 +0.26% ATFBb2 USD 9.28 0 KASE_BY 9.80 -0.82% BRKZb1 USD 8.64 0 SYRGb1 USD 8.50 0 Euronotes of Kazakhstan KZTKb1 USD 8.50 +0.73 KASE_EP 142.59 +0.40% CCBNb1 USD 8.41 -0.02 KASE_EC 115.53 +0.31% HSBKb2 USD 8.16 -0.02 KASE_EY 4.39 -4.22% HSBKb USD 8.16 0 US dollar = 154.45 tenge at official rate for the end of the period ALBNb1 USD 8.10 0 US dollar = 154.45 tenge at weighted average rate of the Exchange TMJLb2 USD 8.00 +0.26 for the end of the period KZTOb USD 7.90 -0.14 Weekly rate of tenge devaluation at the Exchange’s rate – negative VKU036.002 USD 7.71 -0.01 1.2%. -

B REGLAMENTO (CE) No 748/2009 DE LA COMISIÓN

2009R0748 — ES — 01.02.2010 — 001.001 — 1 Este documento es un instrumento de documentación y no compromete la responsabilidad de las instituciones ►B REGLAMENTO (CE) No 748/2009 DE LA COMISIÓN de 5 de agosto de 2009 sobre la lista de operadores de aeronaves que han realizado una actividad de aviación enumerada en el anexo I de la Directiva 2003/87/CE el 1 de enero de 2006 o a partir de esta fecha, en la que se especifica el Estado miembro responsable de la gestión de cada operador (Texto pertinente a efectos del EEE) (DO L 219 de 22.8.2009, p. 1) Modificado por: Diario Oficial n° página fecha ►M1 Reglamento (UE) no 82/2010 de la Comisión de 28 de enero de 2010 L 25 12 29.1.2010 2009R0748 — ES — 01.02.2010 — 001.001 — 2 ▼B REGLAMENTO (CE) No 748/2009 DE LA COMISIÓN de 5 de agosto de 2009 sobre la lista de operadores de aeronaves que han realizado una actividad de aviación enumerada en el anexo I de la Directiva 2003/87/CE el 1 de enero de 2006 o a partir de esta fecha, en la que se especifica el Estado miembro responsable de la gestión de cada operador (Texto pertinente a efectos del EEE) LA COMISIÓN DE LAS COMUNIDADES EUROPEAS, Visto el Tratado constitutivo de la Comunidad Europea, Vista la Directiva 2003/87/CE del Parlamento Europeo y del Consejo, de 13 de octubre de 2003, por la que se establece un régimen para el comercio de derechos de emisión de gases de efecto invernadero en la Comunidad y por la que se modifica la Directiva 96/61/CE del Consejo (1), y, en particular, su artículo 18 bis, apartado 3, letra a), Considerando lo siguiente: (1) La Directiva 2003/87/CE, modificada por la Directiva 2008/101/CE (2), incluye las actividades de aviación en el régi- men para el comercio de derechos de emisión de gases de efecto invernadero en la Comunidad (denominado en lo sucesivo el «régimen comunitario»). -

Airliner Census Western-Built Jet and Turboprop Airliners

World airliner census Western-built jet and turboprop airliners AEROSPATIALE (NORD) 262 7 Lufthansa (600R) 2 Biman Bangladesh Airlines (300) 4 Tarom (300) 2 Africa 3 MNG Airlines (B4) 2 China Eastern Airlines (200) 3 Turkish Airlines (THY) (200) 1 Equatorial Int’l Airlines (A) 1 MNG Airlines (B4 Freighter) 5 Emirates (300) 1 Turkish Airlines (THY) (300) 5 Int’l Trans Air Business (A) 1 MNG Airlines (F4) 3 Emirates (300F) 3 Turkish Airlines (THY) (300F) 1 Trans Service Airlift (B) 1 Monarch Airlines (600R) 4 Iran Air (200) 6 Uzbekistan Airways (300) 3 North/South America 4 Olympic Airlines (600R) 1 Iran Air (300) 2 White (300) 1 Aerolineas Sosa (A) 3 Onur Air (600R) 6 Iraqi Airways (300) (5) North/South America 81 RACSA (A) 1 Onur Air (B2) 1 Jordan Aviation (200) 1 Aerolineas Argentinas (300) 2 AEROSPATIALE (SUD) CARAVELLE 2 Onur Air (B4) 5 Jordan Aviation (300) 1 Air Transat (300) 11 Europe 2 Pan Air (B4 Freighter) 2 Kuwait Airways (300) 4 FedEx Express (200F) 49 WaltAir (10B) 1 Saga Airlines (B2) 1 Mahan Air (300) 2 FedEx Express (300) 7 WaltAir (11R) 1 TNT Airways (B4 Freighter) 4 Miat Mongolian Airlines (300) 1 FedEx Express (300F) 12 AIRBUS A300 408 (8) North/South America 166 (7) Pakistan Int’l Airlines (300) 12 AIRBUS A318-100 30 (48) Africa 14 Aero Union (B4 Freighter) 4 Royal Jordanian (300) 4 Europe 13 (9) Egyptair (600R) 1 American Airlines (600R) 34 Royal Jordanian (300F) 2 Air France 13 (5) Egyptair (600R Freighter) 1 ASTAR Air Cargo (B4 Freighter) 6 Yemenia (300) 4 Tarom (4) Egyptair (B4 Freighter) 2 Express.net Airlines -

Study Report on Comprehensive Support Strategies for Environment and Development in the Early 21St Century

STUDY REPORT ON COMPREHENSIVE SUPPORT STRATEGIES FOR ENVIRONMENT AND DEVELOPMENT IN THE EARLY 21ST CENTURY REPUBLIC OF KAZAKHSTAN MARCH 2006 OVERSEAS ENVIRONMENTAL COOPERATION CENTER, JAPAN Table of Contents 1. Background and Objectives ........................................................................................ 1 2. Outline of the Study..................................................................................................... 2 3. Profile of the Country.................................................................................................. 3 3.1. Geography and Topography .................................................................................. 3 3.2. Climate ................................................................................................................... 5 3.3. History .................................................................................................................... 9 4. Overview of Society and Economy............................................................................ 10 4.1. Overview of Society.............................................................................................. 10 4.2. Overview of Economy .......................................................................................... 13 4.3. Industries.............................................................................................................. 15 4.3.1. Mining and Manufacturing Industries ....................................................... 15 4.4. Agriculture -

Western-Built Jet and Turboprop Airliners

WORLD AIRLINER CENSUS Data compiled from Flightglobal ACAS database flightglobal.com/acas EXPLANATORY NOTES The data in this census covers all commercial jet- and requirements, put into storage, and so on, and when airliners that have been temporarily removed from an turboprop-powered transport aircraft in service or on flying hours for three consecutive months are reported airline’s fleet and returned to the state may not be firm order with the world’s airlines, excluding aircraft as zero. shown as being with the airline for which they operate. that carry fewer than 14 passengers, or the equivalent The exception is where the aircraft is undergoing Russian aircraft tend to spend a long time parked in cargo. maintenance, where it will remain classified as active. before being permanently retired – much longer than The tables are in two sections, both of which have Aircraft awaiting a conversion will be shown as parked. equivalent Western aircraft – so it can be difficult to been compiled by Flightglobal ACAS research officer The region is dictated by operator base and does not establish the exact status of the “available fleet” John Wilding using Flightglobal’s ACAS database. necessarily indicate the area of operation. Options and (parked aircraft that could be returned to operation). Section one records the fleets of the Western-built letters of intent (where a firm contract has not been For more information on airliner types see our two- airliners, and the second section records the fleets of signed) are not included. Orders by, and aircraft with, part World Airliners Directory (Flight International, 27 Russian/CIS-built types. -

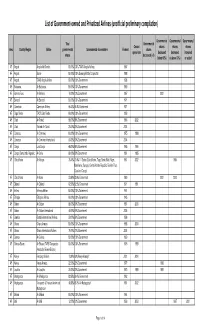

List of Government-Owned and Privatized Airlines (Unofficial Preliminary Compilation)

List of Government-owned and Privatized Airlines (unofficial preliminary compilation) Governmental Governmental Governmental Total Governmental Ceased shares shares shares Area Country/Region Airline governmental Governmental shareholders Formed shares operations decreased decreased increased shares decreased (=0) (below 50%) (=/above 50%) or added AF Angola Angola Air Charter 100.00% 100% TAAG Angola Airlines 1987 AF Angola Sonair 100.00% 100% Sonangol State Corporation 1998 AF Angola TAAG Angola Airlines 100.00% 100% Government 1938 AF Botswana Air Botswana 100.00% 100% Government 1969 AF Burkina Faso Air Burkina 10.00% 10% Government 1967 2001 AF Burundi Air Burundi 100.00% 100% Government 1971 AF Cameroon Cameroon Airlines 96.43% 96.4% Government 1971 AF Cape Verde TACV Cabo Verde 100.00% 100% Government 1958 AF Chad Air Tchad 98.00% 98% Government 1966 2002 AF Chad Toumai Air Tchad 25.00% 25% Government 2004 AF Comoros Air Comores 100.00% 100% Government 1975 1998 AF Comoros Air Comores International 60.00% 60% Government 2004 AF Congo Lina Congo 66.00% 66% Government 1965 1999 AF Congo, Democratic Republic Air Zaire 80.00% 80% Government 1961 1995 AF Cofôte d'Ivoire Air Afrique 70.40% 70.4% 11 States (Cote d'Ivoire, Togo, Benin, Mali, Niger, 1961 2002 1994 Mauritania, Senegal, Central African Republic, Burkino Faso, Chad and Congo) AF Côte d'Ivoire Air Ivoire 23.60% 23.6% Government 1960 2001 2000 AF Djibouti Air Djibouti 62.50% 62.5% Government 1971 1991 AF Eritrea Eritrean Airlines 100.00% 100% Government 1991 AF Ethiopia Ethiopian -

Air Astana Zebra Design Bureau

Annual Report 2017 HIGH VALUE Our ability to deliver full service with a low cost base makes us very competitive, and we are committed to remain so. CONTENTS 1 2 About This Report Company profile Strategic report This report was prepared by Air Astana JSC (the “Company”) and covers the period from 1 January 2017 to 31 December 2017. Business model ......................................................... 4 2.1. Chairman’s statement ......................................18 The report uses internally audited data from operational reports. Peter Foster Development of the route network ...................... 6 2.2. President and CEO’s statement .....................20 In Deсember 2017 the Company changed its functional currency President, Air Astana JSC from Tenge to US Dollar, as the latter currency better represents the Our Aircraft Fleet....................................................... 8 2.3. Market overview .............................................22 underlying economic environment. Customer service .....................................................10 2.4. Strategy review ...............................................26 The consolidated financial data presented in the report are as per the Company’s audited IFRS financial statements. Key events ................................................................12 Azamat Ospanov Vice President Finance Accounts, Air Astana JSC About Air Astana 3 4 Air Astana JSC was established in 2001 by Resolution of the Government of the Republic Management report Corporate governance of Kazakhstan No. 1118 of 29 August 2001. The Company’s shareholders are JSC National Welfare Fund Samruk-Kazyna (on behalf of the Government of the Republic of Kazakhstan) 3.1. Operating results .............................................. 34 4.1. Corporate governance system ....................... 76 and BAE Systems (Kazakhstan) Limited, which own 51% and 49% of the Company’s shares, respectively. The Company’s head office is located in Almaty, Kazakhstan. 3.2. -

Kazakhstan and the New International Politics of Eurasia

Kazakhstan and the New International Politics of Eurasia Richard Weitz SILK ROAD PAPER July 2008 Kazakhstan and the New International Politics of Eurasia Richard Weitz © Central Asia-Caucasus Institute & Silk Road Studies Program – A Joint Transatlantic Research and Policy Center Johns Hopkins University-SAIS, 1619 Massachusetts Ave. NW, Washington, D.C. 20036 Institute for Security and Development Policy, V. Finnbodav. 2, Stockholm-Nacka 13130, Sweden www.silkroadstudies.org “Kazakhstan and the New International Politics of Eurasia” is a Silk Road Paper published by the Central Asia-Caucasus Institute and the Silk Road Studies Program. The Silk Road Papers Series is the Occasional Paper series of the Joint Center, and addresses topical and timely subjects. The Joint Center is a transatlantic independent and non-profit research and policy center. It has offices in Washington and Stockholm and is affiliated with the Paul H. Nitze School of Advanced International Studies of Johns Hopkins University and the Stockholm-based Institute for Security and Development Policy. It is the first institution of its kind in Europe and North America, and is firmly established as a leading research and policy center, serving a large and diverse community of analysts, scholars, policy-watchers, business leaders, and journalists. The Joint Center is at the forefront of research on issues of conflict, security, and development in the region. Through its applied research, publications, research cooperation, public lectures, and seminars, it functions as a focal point for academic, policy, and public discussion regarding the region. The opinions and conclusions expressed are those of the author and do not necessarily reflect the views of the Central Asia-Caucasus Institute and Silk Road Studies Program. -

USAID Cooperative Agreement Award No. 72011518-CA-00001

INTERNEWS CENTRAL ASIA MEDIA PROGRAM USAID Cooperative Agreement Award No. 72011518-CA-00001 QUARTERLY PROGRESS REPORT JANUARY 1, 2019 – MARCH 31, 2019 Dmitri Surnin Dylan Gray Regional Director, Europe & Eurasia Director of Grants and Contracts Olimpieciu 1, Office 36 PO Box 4448 Vilnius, Lithuania Arcata, CA 95518 tel. +370 (677) 42 408 tel. +1 (707) 826-2030 [email protected] [email protected] 1 Table of Contents Executive Summary ................................................................................................................................ 3 Highlights/Impact ................................................................................................................................... 3 Background/Context .............................................................................................................................. 4 Project Activities ..................................................................................................................................... 9 Objective 1: Improve media capacity to provide balanced, informed and unbiased reporting on key policy and public interest issues .................................................................................................... 9 1.1. Increase supply of fact-based, balanced information through local content ................................ 9 1.2. Strengthen professional development of media practitioners across traditional and “new” media platforms .......................................................................................................................................... -

G:\JPH Section\ADU CODELIST\Codelist.Snp

Codelist Economic Regulation Group Aircraft By Name By CAA Code Airline By Name By CAA Code By Prefix Airport By Name By IATA Code By ICAO Code By CAA Code Codelist - Aircraft by Name Civil Aviation Authority Aircraft Name CAA code End Month AEROSPACELINES B377SUPER GUPPY 658 AEROSPATIALE (NORD)262 64 AEROSPATIALE AS322 SUPER PUMA (NTH SEA) 977 AEROSPATIALE AS332 SUPER PUMA (L1/L2) 976 AEROSPATIALE AS355 ECUREUIL 2 956 AEROSPATIALE CARAVELLE 10B/10R 388 AEROSPATIALE CARAVELLE 12 385 AEROSPATIALE CARAVELLE 6/6R 387 AEROSPATIALE CORVETTE 93 AEROSPATIALE SA315 LAMA 951 AEROSPATIALE SA318 ALOUETTE 908 AEROSPATIALE SA330 PUMA 973 AEROSPATIALE SA341 GAZELLE 943 AEROSPATIALE SA350 ECUREUIL 941 AEROSPATIALE SA365 DAUPHIN 975 AEROSPATIALE SA365 DAUPHIN/AMB 980 AGUSTA A109A / 109E 970 AGUSTA A139 971 AIRBUS A300 ( ALL FREIGHTER ) 684 AIRBUS A300-600 803 AIRBUS A300B1/B2 773 AIRBUS A300B4-100/200 683 AIRBUS A310-202 796 AIRBUS A310-300 775 AIRBUS A318 800 AIRBUS A319 804 AIRBUS A319 CJ (EXEC) 811 AIRBUS A320-100/200 805 AIRBUS A321 732 AIRBUS A330-200 801 AIRBUS A330-300 806 AIRBUS A340-200 808 AIRBUS A340-300 807 AIRBUS A340-500 809 AIRBUS A340-600 810 AIRBUS A380-800 812 AIRBUS A380-800F 813 AIRBUS HELICOPTERS EC175 969 AIRSHIP INDUSTRIES SKYSHIP 500 710 AIRSHIP INDUSTRIES SKYSHIP 600 711 ANTONOV 148/158 822 ANTONOV AN-12 347 ANTONOV AN-124 820 ANTONOV AN-225 MRIYA 821 ANTONOV AN-24 63 ANTONOV AN26B/32 345 ANTONOV AN72 / 74 647 ARMSTRONG WHITWORTH ARGOSY 349 ATR42-300 200 ATR42-500 201 ATR72 200/500/600 726 AUSTER MAJOR 10 AVIONS MUDRY CAP 10B 601 AVROLINER RJ100/115 212 AVROLINER RJ70 210 AVROLINER RJ85/QT 211 AW189 983 BAE (HS) 748 55 BAE 125 ( HS 125 ) 75 BAE 146-100 577 BAE 146-200/QT 578 BAE 146-300 727 BAE ATP 56 BAE JETSTREAM 31/32 340 BAE JETSTREAM 41 580 BAE NIMROD MR.