Information & Guidance for Students on Placements

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

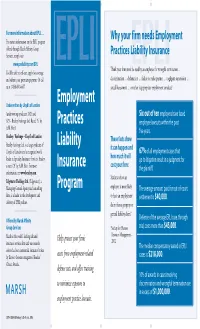

Employment Practices Liability Insurance Program EPLI

B5848_EPLI 2/14/06 2:49 PM Page 1 For more information about EPLI … Why your firm needs Employment For instant information on the EPLI program offered through Marsh Affinity Group Services, simply visit Practices Liability Insurance www.proliablity.com/EPLI Think your firm won’t be sued by an employee for wrongful termination … You’ll be able to self-rate, apply for coverage EPLI EPLI and submit your premium payment. Or call discrimination … defamation … failure to make partner … negligent supervision … us at 1-888-601-6667. sexual harassment … or other inappropriate employment conduct? Underwritten by Lloyd’s of London Employment (underwriting syndicates 2623 and Six out of ten employers have faced 623 – Beazley Furlonge Ltd. Rated “A” by Practices employee lawsuits within the past A.M. Best) five years. Beazley / Furlonge – Lloyd’s of London These facts show Beazley Furlonge Ltd. is a large syndicate of Liability it can happen and Lloyd’s of London and a recognized world 67% of all employment cases that leader in Specialty Insurance Services. Beazley how much it will go to litigation result in a judgment for is rated “A” by A.M. Best. For more Insurance cost your firm: the plaintiff. information, see www.beazley.com. Statistics show an Edgewater Holdings Ltd. (Edgewater), a Managing General Agency and consulting Program employer is more likely The average amount paid for out-of-court firm, is a leader in the development and to have an employment settlement is $40,000. delivery of EPLI policies. claim than a property or general liability claim.* Offered by Marsh Affinity Defense of the average EPLI case, through Group Services *Society for Human trial, costs more than $45,000. -

Consumers Guide to Auto Insurance

CONSUMERS GUIDE TO AUTO INSURANCE PRESENTED TO YOU BY THE DEPARTMENT OF BUSINESS REGULATION INSURANCE DIVISION 1511 PONTIAC AVENUE, BLDG 69-2 CRANSTON, RI 02920 TELEPHONE 401-462-9520 www.dbr.ri.gov Elizabeth Kelleher Dwyer Superintendent of Insurance TABLE OF CONTENTS Introduction………………………………………………………………1 Underwriting and Rating………………………………………………...1 What is meant by underwriting and how is it accomplished…………..1 How are rates and premium charges determined in Rhode Island……1 What factors are considered in ratemaking……………………………. 2 What discounts are used in determining final premium cost…………..3 Rhode Island Automobile Insurance Plan…………………..…………..4 Regulation of Rates……………………………………………………….4 The Tort System…………………………………………………………..4 Liability Coverages………………………………………………………..5 Coverages Other Than Liability…………………………………………5 Physical Damage to the Automobile……………………………………..6 Other Optional Coverages………………………………………………..6 The No-Fault System……………….……………………………………..7 Smart Shopping……………………………………………………………7 Shop for True Comparison………………………………………………..8 Consumer Protection Available...…………………………………………8 What to Do if You are in an Automobile Accident………………………9 Your State Insurance Department………………………………….........9 Auto Insurance Buyer’s Worksheet…………………………………….10 Introduction Auto insurance is an expensive purchase for most Americans, and is especially expensive for Rhode Islanders. Yet consumers rarely comparison-shop for auto insurance as they might for other products and services. Auto insurance companies vary substantially both in price and service to policyholders, so it pays to shop around and compare different insurance companies. This guide to buying auto insurance was developed to help you become a more knowledgeable policyholder and to get the combination of price and service best suited to your needs. It provides information on how to shop for coverage and how insurance premiums are determined. You will also find an Auto Insurance Buyer’s Worksheet in the guide to help you compare premium prices among insurers. -

Tax Risk Insurance: Taking It Captive

taxnotes federal ■ Volume 171, Number 4 April 26, 2021 Tax Risk Insurance: Taking It Captive by Ken Brewer and Albert Liguori Reprinted from Tax Notes Federal, April 26, 2021, p. 549 For more Tax Notes content, please visit www.taxnotes.com. © 2021 Tax Analysts. All rights reserved. Analysts does not claim copyright in any public domain or third party content. TAX PRACTICE tax notes federal Tax Risk Insurance: Taking It Captive by Ken Brewer and Albert Liguori is to explore the U.S. tax implications of that meeting. Behold: captive tax risk insurance!3 In our experiences, the use of tax risk insurance has been most prevalent in the mergers and acquisitions context. But as we mentioned in our last article, we have seen it becoming more common in the context of large corporate groups seeking to manage their global tax risks, regardless of whether they are related to M&A.4 In either context, the use of tax risk insurance lends itself to captive arrangements, for the same reasons that have caused captive arrangements to be desirable for other types of insurance risks. Ken Brewer is a senior adviser and Captive Insurance and the U.S. Tax Implications international tax practitioner with Alvarez & Thereof Marsal Taxand LLC in Miami, and Albert Liguori is a managing director in the firm’s New As an alternative to traditional insurance York office. The authors send special thanks to protection, which is obtained from one or more of Brian Pedersen, managing director at Alvarez & the many underwriters offering that coverage to Marsal Taxand, for his contributions and the public, captive insurance is obtained from a review. -

Auto Insurance and How Those Terms Affect Your Coverage

Arkansas Insurance Department AUTOMOBILE INSURANCE Asa Hutchinson Allen Kerr Governor Commissioner A Message From The Commissioner The Arkansas Insurance Department takes very seriously its mission of “consumer protection.” We believe part of that mission is accomplished when consumers are equipped to make informed decisions. We believe informed decisions are made through the accumulation and evaluation of relevant information. This booklet is designed to provide basic information about automobile insurance. Its purpose is to help you understand terms used in the purchase of auto insurance and how those terms affect your coverage. If you have questions or need additional information, please contact our Consumer Services Division at: Phone: (501) 371-2640; 1-800-852-5494 Fax: (501) 371-2749 Email: [email protected] Web site: www.insurance.arkansas.gov Mission Statement The primary mission of the State Insurance Department shall be consumer protection through insurer insolvency and market conduct regulation, and fraud prosecution and deterrence. 1 Coverages Provided by Automobile Insurance The automobile insurance policy is comprised of several separate types of coverages: COLLISION, COMPREHENSIVE, LIABILITY, PERSONAL INJURY PROTECTION, UNINSURED MOTORIST, UNDERINSURED MOTORIST and other coverages. You are required by law to purchase liability protection only. All others are voluntary unless required by a lienholder. LIABILITY Under Legislation passed in 1987 and 1999, it is unlawful for any person to operate a motor vehicle within this state unless the vehicle is insured with the minimum amount of liability coverage: $25,000 for bodily injury or death of one person in any one accident; $50,000 for bodily injury or death of two or more persons in any one accident and $25,000 for damage to or destruction of the property of others. -

Coronavirus Insurance Coverage and Claims Guidance

Coronavirus Insurance Coverage and Claims Guidance April 15, 2020 With the exposure of the coronavirus (COVID-19) increasing, organizations are evaluating the potential coverage which may be triggered from their insurance policies. Actual loss situations and a review of individual policy forms will be a crucial step to properly evaluate potential available coverage application. Insurance carriers have the ultimate authority in determining coverage for presented claims. Any suspected COVID-19 related losses should be reported per the policy guidelines. Policyholders should be aware that some policies may require specific time frames from notice of potential claim, such as 48 hours. This document provides factors that will be examined in the event losses related to COVID-19 occur. Coronavirus Insurance Coverage and 2 Lockton Companies Claims Guidance Workers’ compensation Each injured employee situation will be evaluated on its own individual merits. Workers’ compensation insurance covers employees who suffer injury or illness “arising out of or in the course of their employment.” Many factors will need to be considered if presented COVID-19-type claims are work related. These include but are not limited to: • The timing of when the loss occurs: were there reports of previously infected individuals made in this same time period? • The location(s) where the injured worker was present leading up the injury or exposure: was the injured worker within an area where exposure of the virus was present or carried a greater risk? • The activities the injured worker was engaged in leading up to when the loss or exposure took place: was the individual in contact with others or working remotely? • The specific nature of the loss: what further details can be uncovered to provide greater clarity around exposure to the virus as an occupational disease? In most jurisdictions, individuals seeking benefits under workers’ compensation will also need to meet the burden that the coronavirus illness arose out of, or was caused by, conditions “peculiar” to the work. -

Captive Insurance Companies

Estate Planning – August 2011 CAPTIVE INSURANCE COMPANIES Possibilities and Pitfalls With Captive Insurance Companies Profitable family businesses can use captive insurance companies to manage business risk and shift wealth accumulated in a profitable captive from senior to junior generations thereby avoiding inclusion of those funds in the senior generation's estates. Author: KIMBERLY S. BUNTING, J. SCOT KIRKPATRICK, AND KAREN S. KURTZ, ATTORNEYS KIMBERLY S. BUNTING is a shareholder in Chamberlain, Hrdlicka, White, Williams & Martin LLP's Atlanta, Georgia, office. She practices in the areas of commercial and corporate law, and has significant experience with risk management and captive insurance companies. J. SCOT KIRKPATRICK is also a shareholder in Chamberlain, Hrdlicka's Atlanta office. His practice focuses principally on estate and income tax planning for high net worth individuals and their businesses. KAREN S. KURTZ is an associate in the Tax Section of Chamberlain Hrdlicka's Atlanta office, concentrating in estate and gift tax planning and litigation. A captive insurance company ("Captive") is an insurance company formed by a business owner to insure the risks of related or affiliated businesses. A Captive permits a business to manage its risks while potentially providing substantial benefits to that related business. The premiums received by the Captive are invested and thus not "lost" if not used to pay claims in the same sense that commercial insurance premiums are when paid to an unrelated insurer. This one benefit drives the use of Captives for the family business more than any other. Captives may issue property or casualty insurance coverage against a wide variety of possible liabilities. -

Effective with UNDERWRITERS at LLOYD's, LONDON Insurance For

Effective with UNDERWRITERS AT LLOYD'S, LONDON Administered by Hiscox Inc. 520 Madison Avenue 32nd Floor, New York, NY 10022 (646) 452-2353 Insurance for General Liability DECLARATIONS This insurance has been placed with an insurer that is not licensed by the state of Michigan. In case of insolvency, payment of claims may not be guaranteed. Broker No.: US 0001488 RT Specialty of Illinois, LLC Policy No.: MPL1934916.18 500 W. Monroe St., 30th Floor Renewal of: MPL1934916.17 Chicago, IL 60661 1. Named Insured: Stateside APM Address: 6445 Citation Dr Ste F Clarkston, MI 48346-2996 2. Policy Period: Inception Date: 03/31/2018 Expiration Date: 03/31/2019 Inception date shown shall be at 12:01 A.M. (Standard Time) to Expiration date shown above at 12:01 A.M. (Standard Time) at the address of the Named Insured. 3. General terms and WCL P0001 CW (09/14) conditions wording: The General terms and conditions apply to this policy in conjunction with the specific wording detailed in each section below. 4. Endorsements: E6015.6 - Lloyd’s Syndicate (3624) Endorsement, E6016.1 - Service of Suit, E6017.2 - Nuclear Incident Exclusion Clause-Liability-Direct (Broad) Endorsement, E6018.2 - Applicable Law Endorsement, E6020.2 - War and Civil War Exclusion Endorsement, E6023.1 - Minimum Earned Premium Endorsement, and E9998.2 - TRIA Not Purchased Endorsement 5. Optional Extension Extended Reporting Period of 12/24/36 months at 75/150/225 percent of the annual premium. Period: 6. Notification of Hiscox Claims claims to: 520 Madison Avenue, 32nd floor New York, NY 10022 Fax: 212-922-9652 Email: [email protected] 7. -

What Is Fiduciary Liability Insurance and Why Do You Need It?

What Is Fiduciary Liability Insurance and Why Do You Need It? Not knowing the answer could cost you everything. Fiduciary Liability Insurance Policies (FLIPs) are arguably one of the least Who is Considered a Fiduciary? What is Considered to be a Plan? understood insurance products on the market. However, it may be the Any individual included in the plan Employee benefit plans fall into only coverage that adequately protects document by name or title, along two broad categories - retirement people against liability for managing or with anyone who has discretionary plans and welfare plans. Retirement administering an employee benefit plan decision-making authority over the plans include a wide gamut of plans, - from top corporate executives that hire administration or management of a including but not limited to defined investment managers to payroll clerks plan or its assets may be considered benefit pension plans, profit sharing that process enrollment forms. With the a fiduciary under ERISA. Fiduciaries or savings plans such as 401(k)s, rising frequency of expensive and time commonly include the plan sponsor 403(b) plans, stock purchase plans, consuming litigation and regulatory efforts (which is typically the employer), and employee stock ownership in today’s evolving legal environment, the plan trustee and the plan plans (ESOPs). Welfare Plans include employers and plan fiduciaries are administrator, directors and officers medical, dental, life and disability increasingly being held accountable for (including when they appoint other plans. their actions (or failure to act) with respect fiduciaries or retain third party to employee benefit plans. Thus, FLIPs are service providers) and internal an important part of any comprehensive investment committees. -

2019 Insurance Fact Book

2019 Insurance Fact Book TO THE READER Imagine a world without insurance. Some might say, “So what?” or “Yes to that!” when reading the sentence above. And that’s understandable, given that often the best experience one can have with insurance is not to receive the benefits of the product at all, after a disaster or other loss. And others—who already have some understanding or even appreciation for insurance—might say it provides protection against financial aspects of a premature death, injury, loss of property, loss of earning power, legal liability or other unexpected expenses. All that is true. We are the financial first responders. But there is so much more. Insurance drives economic growth. It provides stability against risks. It encourages resilience. Recent disasters have demonstrated the vital role the industry plays in recovery—and that without insurance, the impact on individuals, businesses and communities can be devastating. As insurers, we know that even with all that we protect now, the coverage gap is still too big. We want to close that gap. That desire is reflected in changes to this year’s Insurance Information Institute (I.I.I.)Insurance Fact Book. We have added new information on coastal storm surge risk and hail as well as reinsurance and the growing problem of marijuana and impaired driving. We have updated the section on litigiousness to include tort costs and compensation by state, and assignment of benefits litigation, a growing problem in Florida. As always, the book provides valuable information on: • World and U.S. catastrophes • Property/casualty and life/health insurance results and investments • Personal expenditures on auto and homeowners insurance • Major types of insurance losses, including vehicle accidents, homeowners claims, crime and workplace accidents • State auto insurance laws The I.I.I. -

NAIC Risk Retention and Purchasing Group Handbook

Risk Retention and Purchasing Group Handbook NAIC Risk Retention and Purchasing Group Handbook 2020 The NAIC is the authoritative source for insurance industry information. Our expert solutions support the efforts of regulators, insurers and researchers by providing detailed and comprehensive insurance information. The NAIC offers a wide range of publications in the following categories: Accounting & Reporting Special Studies Information about statutory accounting principles and the Studies, reports, handbooks and regulatory research procedures necessary for fi ling fi nancial annual statements conducted by NAIC members on a variety of insurance- and conducting risk-based capital calculations. related topics. Consumer Information Statistical Reports Important answers to common questions about auto, Valuable and in-demand insurance industry-wide statistical home, health and life insurance — as well as buyer’s data for various lines of business, including auto, home, guides on annuities, long-term care insurance and health and life insurance. Medicare supplement plans. Supplementary Products Financial Regulation Guidance manuals, handbooks, surveys and research Useful handbooks, compliance guides and reports on on a wide variety of issues. fi nancial analysis, company licensing, state audit requirements and receiverships. Capital Markets & Investment Analysis Information regarding portfolio values and procedures for Legal complying with NAIC reporting requirements. Comprehensive collection of NAIC model laws, regulations and guidelines; state laws on insurance topics; and other White Papers regulatory guidance on antifraud and consumer privacy. Relevant studies, guidance and NAIC policy positions on a variety of insurance topics. Market Regulation Regulatory and industry guidance on market-related issues, including antifraud, product fi ling requirements, For more information about NAIC producer licensing and market analysis. -

Disclosure 1

ANNUAL REPORT 2012 Social Responsibility Vision MAPFRE wants to be the most trusted global insurance company Mission We are a multinational team that continuously strives to improve our service and develop the best relationship possible with our customers, distributors, suppliers, shareholders and Society Values SOLVENCY INTEGRITY SERVICE VOCATION INNOVATIVE LEADERSHIP COMMITTED TEAM Values SOLVENCY Financial strength with sustainable results. International diversification and consolidation in various markets. INTEGRITY Ethics govern the behaviour of all personnel. Socially responsible focus in all of our activities. SERVICE VOCATION Constant search for excellence in the development of our activities. Continuous initiatives focused on minding our relationship with our customers. INNOVATIVE LEADERSHIP Willingness to surpass ourselves and to constantly improve. Useful technology for servicing the businesses and their objectives. COMMITTED TEAM Total team commitment with MAPFRE’s project. Constant training and development of the team’s capabilities and skills. ANNUAL REPORT 2012 Social Responsibility Table of contents 2 1. Chairman’s Letter 4 4. MAPFRE’s social dimension 26 2. General Information 6 MAPFRE and its employees 27 MAPFRE and its customers 38 Presence 8 MAPFRE and its shareholders 55 MAPFRE Group’s corporate organization chart 9 MAPFRE and the professionals and entities Key economic figures 10 that help distribute products 57 Governing Bodies 11 MAPFRE and its suppliers 62 3. MAPFRE and Corporate Social 5. MAPFRE’s environmental -

Transactional Tax Liability Policies

MemorandumTM Reproduced with permission from Tax Management Memorandum, 61 TMM 12, 06/01/2020. Copyright 2020 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com seller escrow to provide compensation to insured par- Transactional Tax Liability ties in the event of audit or tax controversy. Policies — At the Top of the A long time ago in transaction insurance time (five years ago in real time), there was a little-known prod- Adoption Curve? uct called representation and warranty insurance * which certain private equity companies were using to By William Rowe, Jonathan Welbel & Mark Roche cover representations on their exit from existing busi- Baker McKenzie nesses in M&A transactions. Generally, only risks that Chicago, IL & San Francisco, CA were not identified in due diligence are covered (mat- ters identified in due diligence reports are generally excluded). This product had lots of exclusions, took With the current and expected increase in distressed six weeks to put in place, and was in its infancy. To- mergers and acquisitions (M&A) resulting from day, the parties to many M&A transactions purchase Covid-19, either in the bankruptcy context of §363 representation and warranty insurance and many more 1 sales or outside of bankruptcy in expedited transac- consider it. Indeed, by some estimates, at least one of tions, it is worth revisiting tools to provide buyers the parties (often the buyer) purchases representation with protection from transactional risks where sell and warranty insurance in about 1⁄3 of all transactions side indemnities are either scarce or impossible. This in the United States.