Dodd-Frank's Attempted Reform on Broker-Dealers

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Perelman, M. (2007). Some Economics of Class. in M. Yates (Ed.), More

Perelman, M. (2007). Some economics of class. In M. Yates (ed.), More unequal: Aspects of class in the United States. New York: Monthly Review Press. How much more will be required before the U.S. public awakes from its political slumber? Tepid action in the workplace, the voting booth, and the streets have allowed the right wing to steamroll revolutionary changes that have remade the entire sociopolitical structure of the United States. Since the election of Franklin Roosevelt in 1932, every Democratic administration with the exception of Lyndon Johnson's has been more conservative—often far more conservative—than the previous Democratic administration. Similarly, every elected Republican administration, with the single exception of George Herbert Walker Bush's, has been more conservative than the previous Republican administration. The deterioration in the distribution of income is a symptom of a far larger problem. Perhaps formulating the situation in the United States might help people understand their class interests as well as reveal who has benefited from the right-wing revolution. Critics of Marx have long taken pleasure in claiming that the rise of the middle class in the United States and other advanced capitalist economies disproves Marx's "predictions" of the course of capitalism. In recent decades, however, the distribution of income in the United States is coming to resemble that of many poor Latin American economies, with a shrinking middle class and an obscene share of wealth going to the richest members of society. Although proponents of the U.S. model pretend that recent economic trends represent a success, in truth they are signs of capitalism's failure. -

Understanding Enron: "It's About Gatekeepers, Stupid"

Columbia Law School Scholarship Archive Faculty Scholarship Faculty Publications 2002 Understanding Enron: "It's about Gatekeepers, Stupid" John C. Coffee Jr. Columbia Law School, [email protected] Follow this and additional works at: https://scholarship.law.columbia.edu/faculty_scholarship Part of the Banking and Finance Law Commons, Business Organizations Law Commons, and the Law and Economics Commons Recommended Citation John C. Coffee Jr., Understanding Enron: "It's about Gatekeepers, Stupid", 57 BUS. LAW. 1403 (2002). Available at: https://scholarship.law.columbia.edu/faculty_scholarship/2117 This Article is brought to you for free and open access by the Faculty Publications at Scholarship Archive. It has been accepted for inclusion in Faculty Scholarship by an authorized administrator of Scholarship Archive. For more information, please contact [email protected]. Understanding Enron: "It's About the Gatekeepers, Stupid" By John C. Coffee, Jr* What do we know after Enron's implosion that we did not know before it? The conventional wisdom is that the Enron debacle reveals basic weaknesses in our contemporary system of corporate governance.' Perhaps, this is so, but where is the weakness located? Under what circumstances will critical systems fail? Major debacles of historical dimensions-and Enron is surely that-tend to produce an excess of explanations. In Enron's case, the firm's strange failure is becoming a virtual Rorschach test in which each commentator can see evidence confirming 2 what he or she already believed. Nonetheless, the problem with viewing Enron as an indication of any systematic governance failure is that its core facts are maddeningly unique. -

Systemic Risk Through Securitization: the Result of Deregulation and Regulatory Failure

Revised Feb. 9, 2009 Systemic Risk Through Securitization: The Result of Deregulation and Regulatory Failure by Patricia A. McCoy, * Andrey D. Pavlov, † and Susan M. Wachter ‡ Abstract This paper argues that private-label securitization without regulation is unsustainable. Without regulation, securitization allowed mortgage industry actors to gain fees and to put off risks. During the housing boom, the ability to pass off risk allowed lenders and securitizers to compete for market share by lowering their lending standards, which activated more borrowing. Lenders who did not join in the easing of lending standards were crowded out of the market. In theory, market controls in the form of risk pricing could have constrained heightened mortgage risk without additional regulation. But in reality, as the mortgages underlying securities became more exposed to growing default risk, investors did not receive higher rates of return. Artificially low risk premia caused the asset price of houses to go up, leading to an asset bubble and creating a breeding ground for market fraud. The consequences of lax lending were covered up and there was no immediate failure to discipline the markets. The market might have corrected this problem if investors had been able to express their negative views by short selling mortgage-backed securities, thereby allowing fundamental market value to be achieved. However, the one instrument that could have been used to short sell mortgage-backed securities – the credit default swap – was also infected with underpricing due to lack of minimum capital requirements and regulation to facilitate transparent pricing. As a result, there was no opportunity for short selling in the private-label securitization market. -

The Role of Government Affordable Housing Policy in Creating the Global Financial Crisis of 2008 STAFF REPORT U.S

U.S. House of Representatives Committee on Oversight and Government Reform Darrell Issa (CA-49), Ranking Member The Role of Government Affordable Housing Policy in Creating the Global Financial Crisis of 2008 STAFF REPORT U.S. HOUSE OF REPRESENTATIVES 111TH CONGRESS COMMITTEE ON OVERSIGHT AND GOVERNMENT REFORM ORIGINALLY RELEASED JULY 1, 2009 * UPDATED MAY 12, 2010 INTRODUCTION The housing bubble that burst in 2007 and led to a financial crisis can be traced back to federal government intervention in the U.S. housing market intended to help provide homeownership opportunities for more Americans. This intervention began with two government-backed corporations, Fannie Mae and Freddie Mac, which privatized their profits but socialized their risks, creating powerful incentives for them to act recklessly and exposing taxpayers to tremendous losses. Government intervention also created “affordable” but dangerous lending policies which encouraged lower down payments, looser underwriting standards and higher leverage. Finally, government intervention created a nexus of vested interests – politicians, lenders and lobbyists – who profited from the “affordable” housing market and acted to kill reforms. In the short run, this government intervention was successful in its stated goal – raising the national homeownership rate. However, the ultimate effect was to create a mortgage tsunami that wrought devastation on the American people and economy. While government intervention was not the sole cause of the financial crisis, its role was significant and has received too little attention. In recent months it has been impossible to watch a television news program without seeing a Member of Congress or an Administration official put forward a new recovery proposal or engage in the public flogging of a financial company official whose poor decisions, and perhaps greed, resulted in huge losses and great suffering. -

Stephen Ross (Net Worth: $4.6 Billion)

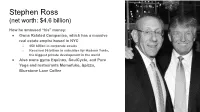

Stephen Ross (net worth: $4.6 billion) How he amassed “his” money: ● Owns Related Companies, which has a massive real estate empire based in NYC ○ $50 billion in corporate assets ○ Received $6 billion in subsidies for Hudson Yards, the biggest private development in the world ● Also owns gyms Equinox, SoulCycle, and Pure Yoga and restaurants Momofuko, &pizza, Bluestone Lane Coffee Stephen Ross (net worth: $7.6 billion) How he keeps “his” money: ● Political donations ○ Raised $12 million for Donald Trump at Hamptons fundraiser ○ Given $80,000 to Andrew Cuomo since 2005 ○ Donates to Republicans in Congress & NYS legislature ● Tax games ○ Billions in tax breaks and other subsidies for Hudson Yards project ○ Overstated value of a property donated to University of Michigan to claim large charitable deduction Stephen Ross (net worth: $7.6 billion) How he spends “his” money: ● At least six homes worth as much as $150 million ○ Hudson Yards penthouse, TriBeCa condo, West Village condo, mansions in the Hamptons and Palm Beach, and a Palm Beach condo ● Owns the Miami Dolphins NFL team ● Board seats at cultural institutions ○ Lincoln Center, Solomon R Guggenheim Foundation Stephen Ross (net worth: $114 billion) How we can tax “his” money: ● Billionaire Wealth Tax ○ Tax on wealth, including unrealized capital gains ● Ultramillionaire Income Tax ○ New 10.32% top PIT rate ● Stock Buyback Tax ○ Hits stunts like his attack on AT&T ● Carried Interest Fairness Fee ○ State tax on his under-taxed fees to investors ● 21st Century Bank Tax ○ State tax on hedge -

After the Meltdown

Tulsa Law Review Volume 45 Issue 3 Regulation and Recession: Causes, Effects, and Solutions for Financial Crises Spring 2010 After the Meltdown Daniel J. Morrissey Follow this and additional works at: https://digitalcommons.law.utulsa.edu/tlr Part of the Law Commons Recommended Citation Daniel J. Morrissey, After the Meltdown, 45 Tulsa L. Rev. 393 (2013). Available at: https://digitalcommons.law.utulsa.edu/tlr/vol45/iss3/2 This Article is brought to you for free and open access by TU Law Digital Commons. It has been accepted for inclusion in Tulsa Law Review by an authorized editor of TU Law Digital Commons. For more information, please contact [email protected]. Morrissey: After the Meltdown AFTER THE MELTDOWN Daniel J. Morrissey* We will not go back to the days of reckless behavior and unchecked excess that was at the heart of this crisis, where too many were motivated only by the appetite for quick kills and bloated bonuses. -President Barack Obamal The window of opportunityfor reform will not be open for long .... -Princeton Economist Hyun Song Shin 2 I. INTRODUCTION: THE MELTDOWN A. How it Happened One year after the financial markets collapsed, President Obama served notice on Wall Street that society would no longer tolerate the corrupt business practices that had almost destroyed the world's economy. 3 In "an era of rapacious capitalists and heedless self-indulgence," 4 an "ingenious elite" 5 set up a credit regime based on improvident * A.B., J.D., Georgetown University; Professor and Former Dean, Gonzaga University School of Law. This article is dedicated to Professor Tom Holland, a committed legal educator and a great friend to the author. -

990-PF and Its Instructions Is at Www

l efile GRAPHIC p rint - DO NOT PROCESS As Filed Data - DLN: 93491318011814 Return of Private Foundation OMB No 1545-0052 Form 990 -PF or Section 4947 ( a)(1) Trust Treated as Private Foundation 0- Do not enter Social Security numbers on this form as it may be made public. By law, the 2013 IRS cannot redact the information on the form. Department of the Treasury 0- Information about Form 990-PF and its instructions is at www. irs.gov/form990pf . Internal Revenue Service For calendar year 2013 , or tax year beginning 01 - 01-2013 , and ending 12-31-2013 Name of foundation A Employer identification number PAULSON FAMILY FOUNDATION CO PAULSON & CO INC 26-3922995 Number and street (or P 0 box number if mail is not delivered to street address) Room/suite U ieiepnone number (see instructions) 1251 AVENUE OF THE AMERICAS 50TH FLOOR (212) 956-2221 City or town, state or province, country, and ZIP or foreign postal code C If exemption application is pending, check here F NEW YORK, NY 10020 G Check all that apply r'Initial return r'Initial return of a former public charity D 1. Foreign organizations, check here F r-Final return r'Amended return 2. Foreign organizations meeting the 85% test, r Address change r'Name change check here and attach computation E If private foundation status was terminated H Check type of organization Section 501(c)(3) exempt private foundation und er section 507 ( b )( 1 )( A ), c hec k here F_ Section 4947(a)(1) nonexempt charitable trust r'Other taxable private foundation I Fair market value of all assets at end J Accounting method F Cash F Accrual F If the foundation is in a 60-month termination of year (from Part II, col. -

A Business Lawyer's Bibliography: Books Every Dealmaker Should Read

585 A Business Lawyer’s Bibliography: Books Every Dealmaker Should Read Robert C. Illig Introduction There exists today in America’s libraries and bookstores a superb if underappreciated resource for those interested in teaching or learning about business law. Academic historians and contemporary financial journalists have amassed a huge and varied collection of books that tell the story of how, why and for whom our modern business world operates. For those not currently on the front line of legal practice, these books offer a quick and meaningful way in. They help the reader obtain something not included in the typical three-year tour of the law school classroom—a sense of the context of our practice. Although the typical law school curriculum places an appropriately heavy emphasis on theory and doctrine, the importance of a solid grounding in context should not be underestimated. The best business lawyers provide not only legal analysis and deal execution. We offer wisdom and counsel. When we cast ourselves in the role of technocrats, as Ronald Gilson would have us do, we allow our advice to be defined downward and ultimately commoditized.1 Yet the best of us strive to be much more than legal engineers, and our advice much more than a mere commodity. When we master context, we rise to the level of counselors—purveyors of judgment, caution and insight. The question, then, for young attorneys or those who lack experience in a particular field is how best to attain the prudence and judgment that are the promise of our profession. For some, insight is gained through youthful immersion in a family business or other enterprise or experience. -

Document Relates To: ALL ACTIONS ———— REPORT of PAUL GOMPERS, Ph.D

No. 20-222 In the Supreme Court of the United States GOLDMAN SACHS GROUP, INC., ET AL., PETITIONERS v. ARKANSAS TEACHER RETIREMENT SYSTEM, ET AL. ON WRIT OF CERTIORARI TO THE UNITED STATES COURT OF APPEALS FOR THE SECOND CIRCUIT JOINT APPENDIX (VOLUME 2; PAGES 401-804) KANNON K. SHANMUGAM THOMAS C. GOLDSTEIN PAUL, WEISS, RIFKIND, GOLDSTEIN & RUSSELL, P.C. WHARTON & GARRISON LLP 7475 Wisconsin Avenue 2001 K Street, N.W. Suite 850 Washington, DC 20006 Bethesda, MD 20814 (202) 223-7300 (202) 362-0636 [email protected] [email protected] Counsel of Record Counsel of Record for Petitioners for Respondents PETITION FOR A WRIT OF CERTIORARI FILED: AUGUST 21, 2020 CERTIORARI GRANTED: DECEMBER 11, 2020 TABLE OF CONTENTS Page VOLUME 1 Court of appeals docket entries (No. 18-3667) ................... 1 Court of appeals docket entries (No. 16-250) ..................... 5 District court docket entries (No. 10-3461) ........................ 8 Goldman Sachs 2007 Form 10-K: Conflicts Warning (D. Ct. Dkt. No. 78-6) .................................................... 23 Goldman Sachs 2007 Annual Report: Business Principles (D. Ct. Dkt. No. 143-16) ............................. 30 Financial Times, Markets & Investing, “Goldman’s risk control offers right example of governance,” Dec. 5, 2007 (D. Ct. Dkt. No. 193-20) .......................... 34 Dow Jones Business News, “13 Reasons Bush’s Bailout Won’t Stop Recession,” Dec. 11, 2007 (D. Ct. Dkt. No. 170-24) ................................................ 37 The Wall Street Journal, “How Goldman Won Big on Mortgage Meltdown,” Dec. 14, 2007 (front page) (D. Ct. Hearing Ex. T) ....................................... 42 The New York Times, Off the Shelf, “Economy’s Loss Was One Man’s Gain,” Dec. -

Richest Hedge Funds the World's

THE WORLD’S DR. BROWNSTEIN’S WINNING FORMULA RICHEST PAGE 40 CANYON’S SECRET EMPIRE HEDGE PAGE 56 CASHING IN ON CHAOS FUNDS PAGE 68 February 2011 BLOOMBERG MARKETS 39 100 THE WORLD’S RICHEST HEDGE FUNDS COVER STORIES FOR 20 YEARS, DON BROWNSTEIN TAUGHT philosophy at the University of Kansas. He special- ized in metaphysics, which examines the character of reality itself. ¶ In a photo from his teaching days, he looks like a young Karl Marx, with a bushy black beard and unruly hair. That photo is now a relic standing behind the curved bird’s-eye-maple desk in Brownstein’s corner office in Stamford, Connecticut. Brownstein abandoned academia in 1989 to try to make some money. ¶ The career change paid off. Brownstein is the founder of Structured Portfolio Man- agement LLC, a company managing $2 billion in five partnerships. His flagship fund, the abstrusely named Structured Servicing Holdings LP, returned 50 percent in the first 10 months of 2010, putting him at the top of BLOOMBERG MARKETS’ list of the 100 best-performing hedge CONTINUED ON PAGE 43 DR. BROWNSTEIN’S By ANTHONY EFFINGER and KATHERINE BURTON WINNING PHOTOGRAPH BY BEN BAKER/REDUX FORMULA THE STRUCTURED PORTFOLIO MANAGEMENT FOUNDER MINE S ONCE-SHUNNED MORTGAGE BONDS FOR PROFITS. HIS FLAGSHIP FUND’S 50 PERCENT GAIN PUTS HIM AT THE TOP OF OUR ROSTER OF THE BEST-PERFORMING LARGE HEDGE FUNDS. 40 BLOOMBERG MARKETS February 2011 NO. BEST-PERFORMING 1 LARGE FUNDS Don Brownstein, left, and William Mok Structured Portfolio Management FUND: Structured Servicing Holdings 50% 2010 135% 2009 TOTAL RETURN In BLOOMBERG MARKETS’ first-ever THE 100 TOP- ranking of the top 100 large PERFORMING hedge funds, bets on mortgages, gold, emerging markets and global LARGE HEDGE FUNDS economic trends stand out. -

Economic Principals \273 Blog Archive \273 a Normal Professor

Economic Principals » Blog Archive » A Normal Professor http://www.economicprincipals.com/issues/2008.06.01/320.html Home June 1, 2008 David Warsh, Proprietor About Archives previous | contents | next Books A Normal Professor Receive the Bulldog Edition Perhaps, now that Harvard’s Russia scandal is receding into the past, Andrei Shleifer, 47, will take it easy. He has a steady stream of students, presides over a growing literature in comparative economics, and has developed an interesting sideline in the economics of persuasion. His wife, Nancy Zimmerman , runs a hedge fund that has seen explosive growth, today managing more than $3 billion for institutional clients; together the pair, through their start-ups, may have Economic Blogosphere amassed net worth of $40 million or more. (A columnist for Economics Portfolio magazine’s website subsequently estimated that Roundtable the figure may be closer to $1 bullion.) Their children are Economists View growing, his energetic parents live nearby, he superintends a steady stream of visitors to his villa in the south of France, and he keeps a hand in with developments in Russia. Economic Journalists For example, when Anders Aslund , of Washington’s Peterson Allan Sloan institute for International Economics, was in Cambridge, Amity Shlaes Mass. last winter, to celebrate the publication of How Andrew Leonard Capitalism Was Built: The Transformation of Central and Binyamin Appelbaum Eastern Europe, Russia, and Central Asia and Russia’s Bruce Bartlett Capitalist Revolution: Why Market Reform Succeeded and Carl Bialik Democracy Failed , Shleifer, the author of A Normal Catherine Rampell Country: Russia After Communism , threw a party for him at Charles Duhigg his spacious home on unpaved Bracebridge Road in suburban Christopher Caldwell Newton. -

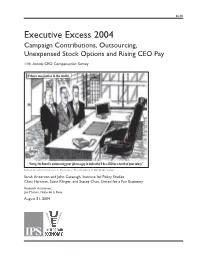

EE2004 Report

$6.00 Executive Excess 2004 Campaign Contributions, Outsourcing, Unexpensed Stock Options and Rising CEO Pay 11th Annual CEO Compensation Survey If there was justice in the world... “Sorry, the Board is outsourcing your job to a guy in India who’ll be a CEO for a tenth of your salary.” Reprinted with permission from the Seattle Post-Intelligencer. First published June 13, 2003. All rights reserved. Sarah Anderson and John Cavanagh, Institute for Policy Studies Chris Hartman, Scott Klinger, and Stacey Chan, United for a Fair Economy Research Assistance: Jon Minton, Nikki de la Rosa August 31, 2004 IPS About the Authors Sarah Anderson is the Director of the Institute for Policy Studies’ Global Economy Project. John Cavanagh is the Director of the Institute for Policy Studies. Chris Hartman is Research Director at United for a Fair Economy. Scott Klinger is Corporate Accountability Coordinator at United for a Fair Economy. Stacey Chan is pursuing degrees in Mathematics and Economics at Brandeis University. The Institute for Policy Studies is an independent center for progressive research and education founded in Washington, DC in 1963. IPS scholar- activists are dedicated to providing politicians, journalists, academics and activists with exciting policy ideas that can make real change possible. United for a Fair Economy is a national, independent, nonpartisan, 501(c)(3) non-profit organization. UFE raises awareness that concentrated wealth and power undermine the economy, corrupt democracy, deepen the racial divide, and tear communities apart. We support and help build social movements for greater equality. © 2004 Institute for Policy Studies and United for a Fair Economy For additional copies of this report, send $6.00 plus $3.00 shipping and handling to: Executive Excess 2004 United for a Fair Economy 37 Temple Place, 2nd Floor Boston, MA 02111 Institute for Policy Studies United for a Fair Economy 733 15th St.