A Business Model for the Digital Distribution of Music in the South African Context

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Uila Supported Apps

Uila Supported Applications and Protocols updated Oct 2020 Application/Protocol Name Full Description 01net.com 01net website, a French high-tech news site. 050 plus is a Japanese embedded smartphone application dedicated to 050 plus audio-conferencing. 0zz0.com 0zz0 is an online solution to store, send and share files 10050.net China Railcom group web portal. This protocol plug-in classifies the http traffic to the host 10086.cn. It also 10086.cn classifies the ssl traffic to the Common Name 10086.cn. 104.com Web site dedicated to job research. 1111.com.tw Website dedicated to job research in Taiwan. 114la.com Chinese web portal operated by YLMF Computer Technology Co. Chinese cloud storing system of the 115 website. It is operated by YLMF 115.com Computer Technology Co. 118114.cn Chinese booking and reservation portal. 11st.co.kr Korean shopping website 11st. It is operated by SK Planet Co. 1337x.org Bittorrent tracker search engine 139mail 139mail is a chinese webmail powered by China Mobile. 15min.lt Lithuanian news portal Chinese web portal 163. It is operated by NetEase, a company which 163.com pioneered the development of Internet in China. 17173.com Website distributing Chinese games. 17u.com Chinese online travel booking website. 20 minutes is a free, daily newspaper available in France, Spain and 20minutes Switzerland. This plugin classifies websites. 24h.com.vn Vietnamese news portal 24ora.com Aruban news portal 24sata.hr Croatian news portal 24SevenOffice 24SevenOffice is a web-based Enterprise resource planning (ERP) systems. 24ur.com Slovenian news portal 2ch.net Japanese adult videos web site 2Shared 2shared is an online space for sharing and storage. -

Heavy? You Must Be Crazy

YOUR FREE WEEKDAY AFTERNOON SOURCE FOR NEWS, SPORTS AND ENTERTAINMENT 03 27 2008 Heavy? You must be crazy Sporting a belly at 40 seriously increases your chances of getting Alzheimer’s later. p.10 Look whom John McCain brought to Utah. p.4 Huge bills freak out Questar customers. p.4 All-you-can-eat seats for sports fan. p.14 SOMETHING TO BUZZ ABOUT Bartender, Another Hemotoxin Please Murder Suspect Not a Flight Risk A Texas rattlesnake rancher found Popplewell said his intent is not A morbidly obese Texas woman Mayra Lizbeth Rosales, who a new way to make money: Stick a to sell an alcoholic beverage but a who authorities originally thought weighs at least 800 pounds and is rattler inside a bottle of vodka and healing tonic. He said he uses the might have crushed her 2-year-old bedridden, was photographed and market the concoction as an “an- cheapest vodka he can find as a nephew to death was arraigned in fingerprinted at her La Joya home cient Asian elixir.” But Bayou Bob preservative for the snakes. The her bedroom Wednesday on a cap- before being released on a per- Popplewell has no liquor license and end result is a super sweet mixed ital murder charge, accused of strik- sonal recognizance bond, Hidalgo faces charges. drink he compared to cough syrup. ing him in the head. County Sheriff Lupe Trevino said. 27mar08 TheWeather Tonight Partly cloudy. 29° theprimer Sunset: 7:47 p.m. Friday 50° Mostly cloudy; 50 INTERNET percent chance of late rain and snow An Educational, Saturday and Fruitful, Site 45° Mostly cloudy; 40 A colorful, new interactive Web site, percent chance of rain designed to educate children ages 2 and snow. -

Summit Guide Guide Du Sommet Guía De La Cumbre Contents/Sommaire/Sumario

New Frontiers for Creators in the Marketplace 9-10 June 2009 – Ronald Reagan Center – Washington DC, USA www.copyrightsummit.com Summit Guide Guide du Sommet Guía de la Cumbre Contents/Sommaire/Sumario Page Welcome 1 Conference Programme 3 What’s happening around the Summit? 11 Additional Summit Information 12 Page Bienvenue 14 Programme des conférences 15 Autres événements autour du sommet ? 24 Informations supplémentaires du sommet 25 Página Bienvenidos 27 Programa de las Conferencias 28 ¿Lo que pasa alrededor del conferencia? 38 Información sobre el conferencia 39 Page Sponsor & Advisory Committee Profiles 41 Partner Organization Profiles 44 Media Partner Profiles 49 Speaker Biographies 53 9-10 June 2009 – Ronald Reagan Center – Washington DC, USA New Frontiers for Creators in the Marketplace Welcome Welcome to the World Copyright Summit! Two years on from our hugely successful inaugural event in Brussels it gives me great pleasure to welcome you all to the 2009 World Copyright Summit in Washington, DC. This year’s slogan for the Summit – “New Frontiers for Creators in the Marketplace” – illustrates perfectly what we aim to achieve here: remind to the world that creators’ contributions are fundamental for cultural, economic and social development but also that creators – and those who represent them – face several daunting challenges in this new digital economy. It is imperative that we bring to the forefront of political debate the creative industries’ future and where we, creators, fit into this new landscape. For this reason we have gathered, under the CISAC umbrella, all the stakeholders involved one way or another in the creation, production and dissemination of creative works. -

01 Worlock Editech 2008

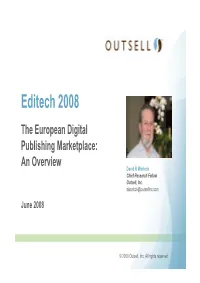

Editech 2008 The European Digital Publishing Marketplace: An Overview David R Worlock Chief Research Fellow Outsell, Inc. [email protected] June 2008 © 2008 Outsell, Inc. All rights reserved. Slower Growth Ahead © 2008 Outsell, Inc. All rights reserved. 2 Search Surges Ahead of Information Industry 26.1% 25.1% 25.2% 24.8% 21.6% 22.5% 18.3% 9.0% 5.0% 4.3% 3.1% 3.1% 3.2% 3.4% 2004 2005 2006 2007 (P) 2008 (P) 2009 (P) 2010 (P) Search, Aggregation & Syndication Info Industry w/o SAS Source: Outsell’s Publishers & Information Providers Database © 2008 Outsell, Inc. All rights reserved. 3 Information Industry $380 Billion in 2007 9% 7% B2B Trade Publishing & Company Information 10% Credit & Financial Information 11% Education & Training HR Information Legal, Tax & Regulatory 5% 10% Market Research, Reports & Services IT & Telecom Research, 1% Reports & Services News Providers & Publishers 4% Scientific, Technical & Medical Information Search, Aggregation & 8% Syndication 1% Yellow Pages & Telephone 34% Directories Source: Outsell’s Publishers & Information Providers Database © 2008 Outsell, Inc. All rights reserved. 4 Search to Soar, While News Nosedives 2007-2010 Est. Industry Growth 5.5% Search, Aggregation & 22.7% Syndication HR Information 15.4% 9.5% IT & Telecom Research, Reports & Services 8.4% Credit & Financial Information 8.1% Market Research, Reports & Services 6.7% Scientific, Technical & Medical 6.7% Information Legal, Tax & Regulatory 5.8% B2B Trade Publishing & 5.7% Company Information Education & Training 5.2% -2.9% Yellow Pages & Directories Source: Outsell's Publishers & Information Providers Database News Providers & Publishers © 2008 Outsell, Inc. All rights reserved. 5 Global Growth in Asia and EMEA © 2008 Outsell, Inc. -

Internet Peer-To-Peer File Sharing Policy Effective Date 8T20t2010

Title: Internet Peer-to-Peer File Sharing Policy Policy Number 2010-002 TopicalArea: Security Document Type Program Policy Pages: 3 Effective Date 8t20t2010 POC for Changes Director, Office of Computing and Information Services (OCIS) Synopsis Establishes a Dalton State College-wide policy regarding copyright infringement. Overview The popularity of Internet peer-to-peer file sharing is often the source of network resource allocation problems and copyright infringement. Purpose This policy will define Internet peer-to-peer file sharing and state the policy of Dalton State College (DSC) on this issue. Scope The scope of this policy includes all DSC computing resources. Policy Internet peer-to-peer file sharing applications are frequently used to distribute copyrighted materials such as music, motion pictures, and computer software. Such exchanges are illegal and are not permifted on Dalton State Gollege computers or network. See the standards outlined in the Appropriate Use Policy. DSG Procedures and Sanctions Failure to comply with the appropriate use of these resources threatens the atmosphere for the sharing of information, the free exchange of ideas, and the secure environment for creating and maintaining information property, and subjects one to discipline. Any user of any DSC system found using lT resources for unethical and/or inappropriate practices has violated this policy and is subject to disciplinary proceedings including suspension of DSC privileges, expulsion from school, termination of employment and/or legal action as may be appropriate. Although all users of DSC's lT resources have an expectation of privacy, their right to privacy may be superseded by DSC's requirement to protect the integrity of its lT resources, the rights of all users and the property of DSC and the State. -

OECD‘S Directorate for Science Technology and Industry

THE ECONOMIC AND SOCIAL ROLE OF INTERNET INTERMEDIARIES APRIL 2010 2 FOREWORD FOREWORD This report is Part I of the larger project on Internet intermediaries. It develops a common definition and understanding of what Internet intermediaries are, of their economic function and economic models, of recent market developments, and discusses the economic and social uses that these actors satisfy. The overall goal of the horizontal report of the Committee for Information, Computer and Communications Policy (ICCP) is to obtain a comprehensive view of Internet intermediaries, their economic and social function, development and prospects, benefits and costs, and responsibilities. It corresponds to the item on 'Forging Partnerships for Advancing Policy Objectives for the Internet Economy' in the Committee‘s work programme. This report was prepared by Ms. Karine Perset of the OECD‘s Directorate for Science Technology and Industry. It was declassified by the ICCP Committee at its 59th Session in March 2010. It was originally issued under the code DSTI/ICCP(2009)9/FINAL. Issued under the responsibility of the Secretary-General of the OECD. The opinions expressed and arguments employed herein do not necessarily reflect the official views of the OECD member countries. ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT The OECD is a unique forum where the governments of 30 democracies work together to address the economic, social and environmental challenges of globalisation. The OECD is also at the forefront of efforts to understand and to help governments respond to new developments and concerns, such as corporate governance, the information economy and the challenges of an ageing population. -

On the Superdistribution of Digital Goods

On the Superdistribution of Digital Goods (Invited Paper) Andreas U. Schmidt Fraunhofer Institute for Secure Information Technology SIT Rheinstraße 75, 64295 Darmstadt, Germany Email: [email protected] Abstract— Business models involving buyers of digital goods or of p2p systems, and research on its fundamentals is still in the distribution process are called superdistribution schemes. scarce. For instance, basic economic questions pertaining to We review the state-of-the art of research and application of the viability of superdistribution in particular in competition superdistribution and propose systematic approach to market mechanisms using super-distribution and technical system archi- with free riders have only been examined in our previous tectures supporting it. The limiting conditions on such markets work [10]. The present paper presents a first contribution to are of economic, legal, technical, and psychological nature. a treatment of other characteristic issues of superdistribution ©2008 IEEE. Personal use of this material is permitted. How- systems, viewed as information systems in their application ever, permission to reprint/republish this material for advertising and economic context. A system model for generic superdis- or promotional purposes or for creating new collective works for resale or redistribution to servers or lists, or to reuse any tribution is proposed in Section II, while Section III presents copyrighted component of this work in other works must be two concrete realisations with distinct traits. Section IV is obtained from the IEEE. the core part of the paper which collects the (in our view) most important research topics on superdistribution and tries I. INTRODUCTION to give an overview over the current state of knowledge in Information systems in general and the distribution of digital the area. -

Music Labels Cut Friendlier Deals with Start-Ups

New Flexibility at Music Labels Aims to Help Web Start-Ups Thrive - NYTimes.com Page 1 of 3 This copy is for your personal, noncommercial use only. You can order presentation-ready copies for distribution to your colleagues, clients or customers here or use the "Reprints" tool that appears next to any article. Visit www.nytreprints.com for samples and additional information. Order a reprint of this article now. May 28, 2009 Music Labels Cut Friendlier Deals With Start-Ups By BRAD STONE SAN FRANCISCO — With CD sales dropping fast, it is not hard to imagine how the major music labels could benefit from the growth of Web start-ups like Imeem. The company’s service lets people listen to songs, discover new artists and share their favorites with friends. And in return, Imeem owes the labels licensing fees for use of the music. But two months ago, Imeem’s founder, Dalton Caldwell, was ready to pull the plug. While 26 million people a month were using the service, Imeem owed millions of dollars to the music labels, and income from advertising was nowhere close to covering expenses. “It reached a point where it was not even clear it was worth doing any more,” Mr. Caldwell said. Then the ground shifted. This month, Warner Music Group forgave Imeem’s debt, and both Warner and Universal Music agreed to relax the terms of their licensing deals with the site. That allowed Imeem to raise more money from investors and plan for a profitable future. Imeem’s amnesty is one sign that a new accommodation is being forged between Web music start-ups and the companies on which they are almost wholly dependent, the major music labels. -

Effect of Networking Revolution on Digital Music

International Journal of Digital Society (IJDS), Volume 4, Issue 2, June 2013 The Effect of Networking Revolution on Digital Music Margounakis Dimitrios, Politis Dionysios Computer Science Department, Aristotle University of Thessaloniki Thessaloniki, Greece Abstract The way people consume music in our days has additional advantage of extreme usability and totally changed as a result of the current accessibility. developments in hardware and software, as well as This emerging form of the Internet and the WWW the evolution of the Internet. People do not buy CDs is known by the term “Web 2.0”. The former or records anymore. Nowadays, people store music structure (now known as “Web 1.0”) was based data on their disks and listen to music via portable primarily on passive access to content that someone devices (i-pods, mobile phones etc.). However, the else (usually a professional) created and published. advent of Web 2.0 foretokens colossal changes in the The current trend facilitates the creation, assimilation fields of music production, distribution and and distribution of information and knowledge. management. Cloud computing, social networks and There is a clear separation between highly popular web-based operating systems are some of the recent Web 2.0 sites and the “old Web”. Three kinds of trends that affect these fields and introduce a new shifts can be distinguished: technological (scripting era beyond MP3. and presentation technologies used to render the site and allow user interaction), structural (purpose and layout of the site), and sociological (notions of 1. Introduction friends and groups) [2]. Web sites that have only some of the social Web 2.0 features, but not all, fall in an intermediate category: Web 1.5. -

Social Media Software and How It Can Assist In

SOCIALSOCIAL MEDIAMEDIA SOFTWARESOFTWARE adding social dimensions to your business Social Media involves all the internet enabled means that people may use to communicate, share and collaborate. This whitepaper features the social media phenomenon and the important social media trends that are being adopted successfully by various businesses. Through various real life examples, it shares that how social media has made a tremendous impact in the growth and development of these businesses. The whitepaper also introduces the social media software and how it can assist in leveraging effective social technologies and the available solutions . Abstract 1 Introduction 2 Defining Social Media 2 Software The Power of Social Media 2 A Deeper Insight 3 Leveraging the Social Magic 3 Social Enablers 4 Crafting the Open Web 5 Add the Social “D” to 5 yor Domain Our Footprints on Social Web 6 Call for a Comprehensive 6 Platform Our Solution - 7 Impetus Technologies Inc. Unvailing Espirit 1 www.impetus.com About Impetus 9 October 2009 WHITE PAPER SOCIAL MEDIA SOFTWARE Introduction Defining Social Media Software The Social Media Software spectrum The recent era has experienced a shift from the comprises a variety of software systems that “static” Web 1.0 internet to an interactive or allow users to communicate and share data. “conversational” world of Web 2.0. Social media can take many different forms, Participation in this social media revolution is including Internet forums, blogs, wikis, the key to harness the unparalleled marketing podcasts, pictures, video, etc. These and branding power of the internet for your interactions have become seismically business. successful on social networking sites Social Networking enables your customers to (Facebook, Orkut, hi5 and MySpace), become the strongest advocates of your multimedia sites (Flickr, Imeem and YouTube), products/services. -

30789 18 Baskerville 9E.Pdf

CHAPTER18 The Digital Age or nearly a century the modern music industry was forged by two then-new F technologies—the phonograph record and broadcasting. In the late 20th century, a third “The future is here. force—digital technology—emerged to shake the industry’s foundations. Digital technology It’s just not widely radically altered not only the business of music but also its creation, manufacture, and distribu- distributed yet.” tion. Furthermore, it changed the very culture of how music is created, with inexpensive tech- —William Gibson nologies to record, present, distribute, promote, and play music, fashioning a unique artistic and commercial digital democracy, which drew mu- sic artist and music consumer closer even as it blurred the boundary between them. Digital’s power was most graphically illustrated in the arena of distribution. The unauthorized digital distribution of music via peer-to-peer (P2P) networks like Napster and Grokster was often cited as the primary force behind the music industry sales slump that began in 2001. Ironically, although these P2P networks also presented a method for legitimate digital distribution via the Internet, record labels, which had reaped a fortune from the sales of CDs for two decades, perceived digital distribution as a threat rather than an opportunity. When Philips and Sony collaborated on the development of the compact disc (CD) in the early 1980s, no one could have predicted the extent to which digital technology, in combination with the Internet (which was still gestating at the time), would revolutionize the music industry. Left: Steve Jobs unveils Apple’s iPod Mini, 2004. -

Identifying Ideological Perspectives of Web Videos Using Folksonomies

Identifying Ideological Perspectives of Web Videos Using Folksonomies Wei-Hao Lin and Alexander Hauptmann Language Technologies Institute School of Computer Science Carnegie Mellon University 5000 Forbes Ave Pittsburgh, PA 15213 USA +1-412-268-f3119,1448g fwhlin,[email protected] Abstract awareness of individual news broadcasters’ or video au- thors’ biases, and can encourage viewers to seek videos ex- We are developing a classifier that can automatically identify pressing contrasting viewpoints. Classifiers that can auto- a web video’s ideological perspective on a political or social matically identify a web video’s ideological perspective will issue (e.g., pro-life or pro-choice on the abortion issue). The problem has received little attention, possibly due to inherent enable video sharing sites to organize videos on various so- difficulties in content-based approaches. We propose to de- cial and political views according to their ideological per- velop such a classifier based on the pattern of tags emerging spectives, and allow users to subscribe to videos based on from folksonomies. The experimental results are positive and their personal views. Automatic perspective classifiers will encouraging. also enable content control or web filtering software to filter out videos expressing extreme political, social or religious views that may not be suitable for children. 1 Introduction Although researchers have made great advances in au- Video sharing websites such as YouTube, Metacafe, and tomatically detecting “visual concepts” (e.g., car, outdoor, Imeem have been extremely popular among Internet users. and people walking) (Naphade & Smith 2004), developing More than three quarters of Internet users in the United classifiers that can automatically identify whether a video is States have watched video online.