30789 18 Baskerville 9E.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Uila Supported Apps

Uila Supported Applications and Protocols updated Oct 2020 Application/Protocol Name Full Description 01net.com 01net website, a French high-tech news site. 050 plus is a Japanese embedded smartphone application dedicated to 050 plus audio-conferencing. 0zz0.com 0zz0 is an online solution to store, send and share files 10050.net China Railcom group web portal. This protocol plug-in classifies the http traffic to the host 10086.cn. It also 10086.cn classifies the ssl traffic to the Common Name 10086.cn. 104.com Web site dedicated to job research. 1111.com.tw Website dedicated to job research in Taiwan. 114la.com Chinese web portal operated by YLMF Computer Technology Co. Chinese cloud storing system of the 115 website. It is operated by YLMF 115.com Computer Technology Co. 118114.cn Chinese booking and reservation portal. 11st.co.kr Korean shopping website 11st. It is operated by SK Planet Co. 1337x.org Bittorrent tracker search engine 139mail 139mail is a chinese webmail powered by China Mobile. 15min.lt Lithuanian news portal Chinese web portal 163. It is operated by NetEase, a company which 163.com pioneered the development of Internet in China. 17173.com Website distributing Chinese games. 17u.com Chinese online travel booking website. 20 minutes is a free, daily newspaper available in France, Spain and 20minutes Switzerland. This plugin classifies websites. 24h.com.vn Vietnamese news portal 24ora.com Aruban news portal 24sata.hr Croatian news portal 24SevenOffice 24SevenOffice is a web-based Enterprise resource planning (ERP) systems. 24ur.com Slovenian news portal 2ch.net Japanese adult videos web site 2Shared 2shared is an online space for sharing and storage. -

Digital Distribution

HOW DIGITAL DISTRIBUTION AND EVALUATION IS IMPACTING PUBLIC SERVICE ADVERTISING Aggressive Promotion Yields Significant Results By Bill Goodwill & James Baumann It is no surprise to see that digital distribution of all media products is fast becoming the de facto standard for distribution of media content, particularly for shorter videos such as PSA messages. First let’s define the terms. Digital distribution (also called digital content delivery, online distribution, or electronic distribution), is the delivery of media content online, thus bypassing physical distribution methods, such as video tapes, CDs and DVDs. In additional to saving money on tapes and disks, digital distribution eliminates the need to print collateral materials such as storyboards, newsletters, bounce-back cards, etc. Finally, it provides the opportunity to preview messages online, and offers media high- quality files for download. The “Pull” Distribution Model In the pre-digital world, the media was spoiled because they had all the PSA messages they could ever use delivered right to their desktop, along with promotional materials explaining the importance of the campaigns. Today, the standard way for stations to get PSAs in the digital world is to go to a site created by the digital distribution company and download them from the “cloud.” Using a dashboard that has been created for PSAs, the media can preview the spots and download both the PSAs, as well as digital collateral materials such as storyboards, a newsletter and traffic instructions. This schematic shows the overall process flow for digital distribution. To provide more control over digital distribution, Goodwill Communications has its own digital distribution download site called PSA Digital™, and to see how we handle both TV and radio digital files, go to: http://www.goodwillcommunications.com/PSADigital.aspx. -

The Effects of Digital Music Distribution" (2012)

Southern Illinois University Carbondale OpenSIUC Research Papers Graduate School Spring 4-5-2012 The ffecE ts of Digital Music Distribution Rama A. Dechsakda [email protected] Follow this and additional works at: http://opensiuc.lib.siu.edu/gs_rp The er search paper was a study of how digital music distribution has affected the music industry by researching different views and aspects. I believe this topic was vital to research because it give us insight on were the music industry is headed in the future. Two main research questions proposed were; “How is digital music distribution affecting the music industry?” and “In what way does the piracy industry affect the digital music industry?” The methodology used for this research was performing case studies, researching prospective and retrospective data, and analyzing sales figures and graphs. Case studies were performed on one independent artist and two major artists whom changed the digital music industry in different ways. Another pair of case studies were performed on an independent label and a major label on how changes of the digital music industry effected their business model and how piracy effected those new business models as well. I analyzed sales figures and graphs of digital music sales and physical sales to show the differences in the formats. I researched prospective data on how consumers adjusted to the digital music advancements and how piracy industry has affected them. Last I concluded all the data found during this research to show that digital music distribution is growing and could possibly be the dominant format for obtaining music, and the battle with piracy will be an ongoing process that will be hard to end anytime soon. -

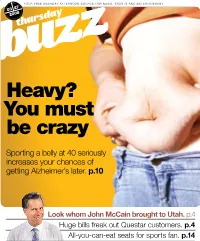

Heavy? You Must Be Crazy

YOUR FREE WEEKDAY AFTERNOON SOURCE FOR NEWS, SPORTS AND ENTERTAINMENT 03 27 2008 Heavy? You must be crazy Sporting a belly at 40 seriously increases your chances of getting Alzheimer’s later. p.10 Look whom John McCain brought to Utah. p.4 Huge bills freak out Questar customers. p.4 All-you-can-eat seats for sports fan. p.14 SOMETHING TO BUZZ ABOUT Bartender, Another Hemotoxin Please Murder Suspect Not a Flight Risk A Texas rattlesnake rancher found Popplewell said his intent is not A morbidly obese Texas woman Mayra Lizbeth Rosales, who a new way to make money: Stick a to sell an alcoholic beverage but a who authorities originally thought weighs at least 800 pounds and is rattler inside a bottle of vodka and healing tonic. He said he uses the might have crushed her 2-year-old bedridden, was photographed and market the concoction as an “an- cheapest vodka he can find as a nephew to death was arraigned in fingerprinted at her La Joya home cient Asian elixir.” But Bayou Bob preservative for the snakes. The her bedroom Wednesday on a cap- before being released on a per- Popplewell has no liquor license and end result is a super sweet mixed ital murder charge, accused of strik- sonal recognizance bond, Hidalgo faces charges. drink he compared to cough syrup. ing him in the head. County Sheriff Lupe Trevino said. 27mar08 TheWeather Tonight Partly cloudy. 29° theprimer Sunset: 7:47 p.m. Friday 50° Mostly cloudy; 50 INTERNET percent chance of late rain and snow An Educational, Saturday and Fruitful, Site 45° Mostly cloudy; 40 A colorful, new interactive Web site, percent chance of rain designed to educate children ages 2 and snow. -

Summit Guide Guide Du Sommet Guía De La Cumbre Contents/Sommaire/Sumario

New Frontiers for Creators in the Marketplace 9-10 June 2009 – Ronald Reagan Center – Washington DC, USA www.copyrightsummit.com Summit Guide Guide du Sommet Guía de la Cumbre Contents/Sommaire/Sumario Page Welcome 1 Conference Programme 3 What’s happening around the Summit? 11 Additional Summit Information 12 Page Bienvenue 14 Programme des conférences 15 Autres événements autour du sommet ? 24 Informations supplémentaires du sommet 25 Página Bienvenidos 27 Programa de las Conferencias 28 ¿Lo que pasa alrededor del conferencia? 38 Información sobre el conferencia 39 Page Sponsor & Advisory Committee Profiles 41 Partner Organization Profiles 44 Media Partner Profiles 49 Speaker Biographies 53 9-10 June 2009 – Ronald Reagan Center – Washington DC, USA New Frontiers for Creators in the Marketplace Welcome Welcome to the World Copyright Summit! Two years on from our hugely successful inaugural event in Brussels it gives me great pleasure to welcome you all to the 2009 World Copyright Summit in Washington, DC. This year’s slogan for the Summit – “New Frontiers for Creators in the Marketplace” – illustrates perfectly what we aim to achieve here: remind to the world that creators’ contributions are fundamental for cultural, economic and social development but also that creators – and those who represent them – face several daunting challenges in this new digital economy. It is imperative that we bring to the forefront of political debate the creative industries’ future and where we, creators, fit into this new landscape. For this reason we have gathered, under the CISAC umbrella, all the stakeholders involved one way or another in the creation, production and dissemination of creative works. -

Apple / Shazam Merger Procedure Regulation (Ec)

EUROPEAN COMMISSION DG Competition CASE M.8788 – APPLE / SHAZAM (Only the English text is authentic) MERGER PROCEDURE REGULATION (EC) 139/2004 Article 8(1) Regulation (EC) 139/2004 Date: 06/09/2018 This text is made available for information purposes only. A summary of this decision is published in all EU languages in the Official Journal of the European Union. Parts of this text have been edited to ensure that confidential information is not disclosed; those parts are enclosed in square brackets. EUROPEAN COMMISSION Brussels, 6.9.2018 C(2018) 5748 final COMMISSION DECISION of 6.9.2018 declaring a concentration to be compatible with the internal market and the EEA Agreement (Case M.8788 – Apple/Shazam) (Only the English version is authentic) TABLE OF CONTENTS 1. Introduction .................................................................................................................. 6 2. The Parties and the Transaction ................................................................................... 6 3. Jurisdiction of the Commission .................................................................................... 7 4. The procedure ............................................................................................................... 8 5. The investigation .......................................................................................................... 8 6. Overview of the digital music industry ........................................................................ 9 6.1. The digital music distribution value -

01 Worlock Editech 2008

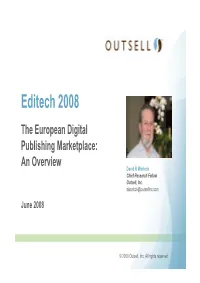

Editech 2008 The European Digital Publishing Marketplace: An Overview David R Worlock Chief Research Fellow Outsell, Inc. [email protected] June 2008 © 2008 Outsell, Inc. All rights reserved. Slower Growth Ahead © 2008 Outsell, Inc. All rights reserved. 2 Search Surges Ahead of Information Industry 26.1% 25.1% 25.2% 24.8% 21.6% 22.5% 18.3% 9.0% 5.0% 4.3% 3.1% 3.1% 3.2% 3.4% 2004 2005 2006 2007 (P) 2008 (P) 2009 (P) 2010 (P) Search, Aggregation & Syndication Info Industry w/o SAS Source: Outsell’s Publishers & Information Providers Database © 2008 Outsell, Inc. All rights reserved. 3 Information Industry $380 Billion in 2007 9% 7% B2B Trade Publishing & Company Information 10% Credit & Financial Information 11% Education & Training HR Information Legal, Tax & Regulatory 5% 10% Market Research, Reports & Services IT & Telecom Research, 1% Reports & Services News Providers & Publishers 4% Scientific, Technical & Medical Information Search, Aggregation & 8% Syndication 1% Yellow Pages & Telephone 34% Directories Source: Outsell’s Publishers & Information Providers Database © 2008 Outsell, Inc. All rights reserved. 4 Search to Soar, While News Nosedives 2007-2010 Est. Industry Growth 5.5% Search, Aggregation & 22.7% Syndication HR Information 15.4% 9.5% IT & Telecom Research, Reports & Services 8.4% Credit & Financial Information 8.1% Market Research, Reports & Services 6.7% Scientific, Technical & Medical 6.7% Information Legal, Tax & Regulatory 5.8% B2B Trade Publishing & 5.7% Company Information Education & Training 5.2% -2.9% Yellow Pages & Directories Source: Outsell's Publishers & Information Providers Database News Providers & Publishers © 2008 Outsell, Inc. All rights reserved. 5 Global Growth in Asia and EMEA © 2008 Outsell, Inc. -

The Obstacles of Streaming Digital Media and the Future of Transnational Licensing Jasmine A

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by UC Hastings Scholarship Repository (University of California, Hastings College of the Law) Hastings Communications and Entertainment Law Journal Volume 36 | Number 1 Article 7 1-1-2014 Lost in Translation: The Obstacles of Streaming Digital Media and the Future of Transnational Licensing Jasmine A. Braxton Follow this and additional works at: https://repository.uchastings.edu/ hastings_comm_ent_law_journal Part of the Communications Law Commons, Entertainment, Arts, and Sports Law Commons, and the Intellectual Property Law Commons Recommended Citation Jasmine A. Braxton, Lost in Translation: The Obstacles of Streaming Digital Media and the Future of Transnational Licensing, 36 Hastings Comm. & Ent. L.J. 193 (2014). Available at: https://repository.uchastings.edu/hastings_comm_ent_law_journal/vol36/iss1/7 This Note is brought to you for free and open access by the Law Journals at UC Hastings Scholarship Repository. It has been accepted for inclusion in Hastings Communications and Entertainment Law Journal by an authorized editor of UC Hastings Scholarship Repository. For more information, please contact [email protected]. Lost in Translation: The Obstacles of Streaming Digital Media and the Future of Transnational Licensing by JASMINE A. BRAXTON* I. Introduction ......................................................................................................................... 193 II. Background: The Current State of Copyright Law for -

Vinyl Theory

Vinyl Theory Jeffrey R. Di Leo Copyright © 2020 by Jefrey R. Di Leo Lever Press (leverpress.org) is a publisher of pathbreaking scholarship. Supported by a consortium of liberal arts institutions focused on, and renowned for, excellence in both research and teaching, our press is grounded on three essential commitments: to publish rich media digital books simultaneously available in print, to be a peer-reviewed, open access press that charges no fees to either authors or their institutions, and to be a press aligned with the ethos and mission of liberal arts colleges. This work is licensed under the Creative Commons Attribution- NonCommercial 4.0 International License. To view a copy of this license, visit http://creativecommons.org/licenses/by-nc/4.0/ or send a letter to Creative Commons, PO Box 1866, Mountain View, CA 94042, USA. The complete manuscript of this work was subjected to a partly closed (“single blind”) review process. For more information, please see our Peer Review Commitments and Guidelines at https://www.leverpress.org/peerreview DOI: https://doi.org/10.3998/mpub.11676127 Print ISBN: 978-1-64315-015-4 Open access ISBN: 978-1-64315-016-1 Library of Congress Control Number: 2019954611 Published in the United States of America by Lever Press, in partnership with Amherst College Press and Michigan Publishing Without music, life would be an error. —Friedrich Nietzsche The preservation of music in records reminds one of canned food. —Theodor W. Adorno Contents Member Institution Acknowledgments vii Preface 1 1. Late Capitalism on Vinyl 11 2. The Curve of the Needle 37 3. -

Internet Peer-To-Peer File Sharing Policy Effective Date 8T20t2010

Title: Internet Peer-to-Peer File Sharing Policy Policy Number 2010-002 TopicalArea: Security Document Type Program Policy Pages: 3 Effective Date 8t20t2010 POC for Changes Director, Office of Computing and Information Services (OCIS) Synopsis Establishes a Dalton State College-wide policy regarding copyright infringement. Overview The popularity of Internet peer-to-peer file sharing is often the source of network resource allocation problems and copyright infringement. Purpose This policy will define Internet peer-to-peer file sharing and state the policy of Dalton State College (DSC) on this issue. Scope The scope of this policy includes all DSC computing resources. Policy Internet peer-to-peer file sharing applications are frequently used to distribute copyrighted materials such as music, motion pictures, and computer software. Such exchanges are illegal and are not permifted on Dalton State Gollege computers or network. See the standards outlined in the Appropriate Use Policy. DSG Procedures and Sanctions Failure to comply with the appropriate use of these resources threatens the atmosphere for the sharing of information, the free exchange of ideas, and the secure environment for creating and maintaining information property, and subjects one to discipline. Any user of any DSC system found using lT resources for unethical and/or inappropriate practices has violated this policy and is subject to disciplinary proceedings including suspension of DSC privileges, expulsion from school, termination of employment and/or legal action as may be appropriate. Although all users of DSC's lT resources have an expectation of privacy, their right to privacy may be superseded by DSC's requirement to protect the integrity of its lT resources, the rights of all users and the property of DSC and the State. -

A Framework of Guidance for Building Good Digital Collections

A Framework of Guidance for Building Good Digital Collections 3rd edition December 2007 A NISO Recommended Practice Prepared by the NISO Framework Working Group with support from the Institute of Museum and Library Services About NISO Recommended Practices A NISO Recommended Practice is a recommended "best practice" or "guideline" for methods, materials, or practices in order to give guidance to the user. Such documents usually represent a leading edge, exceptional model, or proven industry practice. All elements of Recommended Practices are discretionary and may be used as stated or modified by the user to meet specific needs. This recommended practice may be revised or withdrawn at any time. For current information on the status of this publication contact the NISO office or visit the NISO website (www.niso.org). Published by National Information Standards Organization (NISO) One North Charles Street, Suite 1905 Baltimore, MD 21201 www.niso.org Copyright © 2007 by the National Information Standards Organization All rights reserved under International and Pan-American Copyright Conventions. For noncommercial purposes only, this publication may be reproduced or transmitted in any form or by any means without prior permission in writing from the publisher, provided it is reproduced accurately, the source of the material is identified, and the NISO copyright status is acknowledged. All inquires regarding translations into other languages or commercial reproduction or distribution should be addressed to: NISO, One North Charles Street, Suite -

300-313 – 16 Specifications for Phonograph Record Storage Boxes

Library of Congress Preservation Directorate Specification Number 300-313 – 16 Specifications for Phonograph Record Storage Boxes This specification is provided as a public service by the Preservation Directorate of the Library of Congress. Any commercial reproduction that implies endorsement of a product, service, or materials, in any publication, is strictly prohibited by law. This Specification is written for L.C. purchasing purposes and is subject to change when necessary. If you are reading a paper copy of this specification please check our website for the most up-to-date version. 1. Composition and Chemical Requirements 1.1 Fiber The stock must be made from rag or other high alpha-cellulose content pulp, minimum of 87%. It must not contain any post consumer waste recycled pulp. 1.2 Lignin The stock must give a negative reading for lignin as determined by the phloroglucinol test when tested according to TAPPI T 401, Appendix F, and shall have a Kappa number of 5 or less when tested according to TAPPI T 236. 1.3 Impurities The stock must be free of metal particles, waxes, plasticizers, residual bleach, peroxide, sulfur (which will be less than 0.0008% reducible sulfur as determined by TAPPI T 406), and other components that could lead to the degradation of the box itself, or the artifacts stored therein. 1.4 Metallic Impurities Iron must not exceed 150 ppm and copper shall not exceed 6 ppm when tested according to TAPPI T 266. 1.5 Optical Brighteners The stock must be free of optical brightening agents. 1.6 pH The stock must have a pH value within a range of 8.0 - 9.5 as determined by TAPPI T 509, cold extraction (modified by slurrying sample pulp before measurement).