The German Private Commercial Banks' Statutory Deposit Guarantee

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Verzeichnis Des Anteilsbesitzes 2007 List of Shareholdings 2007

Verzeichnis des Anteilsbesitzes 2007 List of Shareholdings 2007 ANTEILSBESITZ gemäß § 313 Abs. 2 und 4 HGB zum Konzernabschluss sowie gemäß § 285 Nr. 11 HGB zum Jahresabschluss der Deutschen Bank AG einschließlich der Angaben nach § 285 Nr. 11a HGB* SHAREHOLDINGS** pursuant to § 313 (2) and (4) CommC for the Consolidated Statement of Accounts and pursuant to § 285 No. 11 CommC for the Annual Statement of Accounts of Deutsche Bank AG including information pursuant to § 285 No. 11a CommC* ANTEILSBESITZ gemäß § 313 Abs. 2 und 4 HGB zum Konzernabschluss sowie gemäß § 285 Nr. 11 HGB zum Jahresabschluss der Deutschen Bank AG einschließlich der Angaben nach § 285 Nr. 11a HGB* SHAREHOLDINGS01 // Verbundene Unternehmen** 2 pursuantSubsidiaries to § 313 (2) and (4) CommC for the Consolidated Statement of Accounts and pursuant to § 285 No. 11 CommC for the Annual Statement of Accounts of Deutsche Bank AG including information pursuant to § 285 No. 11a CommC* 02 // Zweckgesellschaften und ähnliche Strukturen 27 Special Purpose Entities 0301 // AtVerbundene equity bewertete Unternehmen Beteiligungen 239 CompaniesSubsidiaries accounted for at equity 0402 // BeteiligungenZweckgesellschaften an großen und Kapitalgesellschaften, ähnliche Strukturen 4278 beiSpecial denen Purpose die Beteiligung Entities 5% der Stimmrechte überschreitet Holdings in large corporations, where the holding exceeds 5% of voting rights 03 // At equity bewertete Beteiligungen 39 Companies accounted for at equity 04 //Anmerkungen Beteiligungen an großen Kapitalgesellschaften, 5049 beiNotes denen die Beteiligung 5% der Stimmrechte überschreitet Holdings in large corporations, where the holding exceeds 5% of voting rights Stichtagskurse 50 Reporting-Date Exchange Rates Anhang:Anmerkungen Alphabetisches Verzeichnis der Gesellschaften 5501 Appendix:Notes Index of Companies in alphabetical order Stichtagskurse 51 Reporting-Date Exchange Rates Anhang: Alphabetisches Verzeichnis der Gesellschaften 52 Appendix: Index of Companies in alphabetical order * Die Angabe nach § 285 Nr. -

Annual Report 2007 Sales in € Million 14,430 14,125 EBITDA (Before Non-Operating Result) in € Million 2,221 2,157

The first annual report published under the Evonik brand. Overview Evonik Group: Key figures 2007 2006 Annual Report 2007 Sales in € million 14,430 14,125 EBITDA (before non-operating result) in € million 2,221 2,157 EBITDA margin in % 15.4 15.3 EBIT (before non-operating result) in € million 1,348 1,179 Return on capital employed (ROCE) in % 9.5 8.4 Net income in € million 876 1,046 The First. Total assets in € million 19,800 20,953 Equity ratio in % 25.7 20.6 Annual Report Annual 2007 Cash flow from operating activities in € million 1,215 1,142 Capital expenditures1) in € million 1,032 935 Depreciation and amortization1) in € million 862 943 The The First. Net financial debt in € million 4,645 5,434 Employees as of December 31 43,057 46,430 1) Intangible assets, property, plant, equipment and investment property. A clear structure Evonik Industries The information contained herein is not for publication or distribution, directly or indirectly, in or into the United States of America, Canada, Japan or Australia. Chemicals Energy Real Estate Business areas Business units Industrial Consumer Coatings & Energy Real Estate Chemicals Specialties Additives Inorganic Health & Performance Materials Nutrition Polymers Technology Consumer Specialty Energy Real Estate Segments Evonik Industries AG Specialties Solutions Materials Rellinghauser Straße 1–11 45128 Essen Germany www.evonik.com The first annual report published under the Evonik brand. Overview Evonik Group: Key figures 2007 2006 Annual Report 2007 Sales in € million 14,430 14,125 EBITDA (before non-operating result) in € million 2,221 2,157 EBITDA margin in % 15.4 15.3 EBIT (before non-operating result) in € million 1,348 1,179 Return on capital employed (ROCE) in % 9.5 8.4 Net income in € million 876 1,046 The First. -

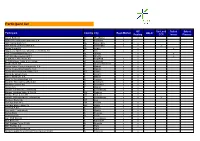

Participant List

Participant list GC SecLend Select Select Participant Country City Repo Market HQLAx Pooling CCP Invest Finance Aareal Bank AG D Wiesbaden x x ABANCA Corporaction Bancaria S.A E Betanzos x ABN AMRO Bank N.V. NL Amsterdam x x ABN AMRO Clearing Bank N.V. NL Amsterdam x x x Airbus Group SE NL Leiden x x Allgemeine Sparkasse Oberösterreich Bank AG A Linz x x ASR Levensverzekering N.V. NL Utrecht x x ASR Schadeverzekering N.V. NL Utrecht x x Augsburger Aktienbank AG D Augsburg x x B. Metzler seel. Sohn & Co. KGaA D Frankfurt x x Baader Bank AG D Unterschleissheim x x Banco Bilbao Vizcaya Argentaria, S.A. E Madrid x x Banco Cooperativo Español, S.A. E Madrid x x Banco de Investimento Global, S.A. PT Lisbon x x Banco de Sabadell S.A. E Alicante x x Banco Santander S.A. E Madrid x x Bank für Sozialwirtschaft AG D Cologne x x Bank für Tirol und Vorarlberg AG A Innsbruck x x Bankhaus Lampe KG D Dusseldorf x x Bankia S.A. E Madrid x x Banque Centrale du Luxembourg L Luxembourg x x Banque Lombard Odier & Cie SA CH Geneva x x Banque Pictet & Cie AG CH Geneva x x Banque Internationale à Luxembourg L Luxembourg x x x Bantleon Bank AG CH Zug x Barclays Bank PLC GB London x x Barclays Bank Ireland Plc IRL Dublin x x BAWAG P.S.K. A Vienna x x Bayerische Landesbank D Munich x x Belfius Bank B Brussels x x Berlin Hyp AG D Berlin x x BGL BNP Paribas L Luxembourg x x BKS Bank AG A Klagenfurt x x BNP Paribas Fortis SA/NV B Brussels x x BNP Paribas S.A. -

Deutsche Postbank Ag, Bonn Annual Financial Statements (Hgb) As of December 31, 2014

DEUTSCHE POSTBANK AG, BONN ANNUAL FINANCIAL STATEMENTS (HGB) AS OF DECEMBER 31, 2014 DEUTSCHE POSTBANK AG, BONN ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD ENDED DECEMBER 31, 2014 AND MANAGEMENT REPORT FOR FISCAL YEAR 2014 MANAGEMENT REPORT 2 BALANCE SHEET AS OF DECEMBER 31, 2014 44 INCOME STATEMENT FOR THE PERIOD JANUARY 1, 2014 TO DECEMBER 31, 2014 46 NOTES 48 AUDITOR‘S REPORT 81 POSTBANK MANAGEMENT REPORT In addition to retail banking, Postbank is involved in the cor- porate banking business. As a mid-sized market player in BUSINESS AND ENVIRONMENT this area, it focuses particularly on German SMEs. Postbank’s most significant competitors also in this business area are Corporate profile providers from the sector of savings banks and cooperative banks as well as several major banks. Business model of Postbank Deutsche Postbank AG (Postbank) provides financial services Management at Postbank for retail and corporate customers as well as for other finan- Postbank is responsible for the management of the entire cial service providers primarily in Germany. The focus of its Postbank subgroup. business activities is retail banking and corporate banking (payment transactions and financing). The Bank’s work is Non-financial key performance indicators at Postbank rounded out by money market and capital market activities. In its corporate management, Postbank makes use of financial On December 3, 2010, Postbank became part of the Deut- as well as non-financial key performance indicators. Essen- sche Bank Group, Frankfurt am Main, which directly and in- tial non-financial key performance indicators measure em- directly holds 94.1 % of the shares in Deutsche Postbank AG. -

Is Customer Recovery Management in Retail Banking Worth the Investment? Lessons from the Field

Is Customer Recovery Management in Retail Banking Worth the Investment? Lessons from the Field Felix Hübnera* Tim Alexander Herbergerb & Michel Charifzadehc Version: January 2021 Abstract Due to the increased willingness of private retail banking customers to switch and churn their banking relation- ships, a question arises: Is it possible to win back lost customers, and if so, is such a possibility even desirable after all economic factors have been considered? To answer these questions, this paper examines selected determinants for the recovery of terminated customer–bank relationships from the perspective of former customers. From the results, a correlation is shown between the willingness to resume a banking relationship and some specific deter- minants: seeking variety, attractiveness of alternatives and customer satisfaction with the former business relation- ship. In addition, we show that a customer’s intention to return varies depending on the reason for churn and is greater when the customer defected for reasons that lie within the scope of the customer himself. The results also show that the chances for successful customer recovery management are rather low for retail banks that charge a fee for account services. JEL Classification: G20, G21, G29 Key Words: Retail Banking, Relationship Marketing, Dissonance Theory, Customer Recov- ery Management a Associate Researcher and Chair of Business Administration, especially Entrepreneurship, Finance and Digitali- zation, Andrássy University, Budapest, Hungary. b Associate Professor and Head of Chair of Business Administration, especially Entrepreneurship, Finance and Digitalization, Andrássy University, Budapest, Hungary. c Professor at the ESB Business School, Reutlingen University, Reutlingen, Germany. * Correspondence address: Chair of Business Administration, especially Entrepreneurship, Finance and Digitali- zation, Andrássy University Budapest, Pollack Mihály tér 3, 1088 Budapest, Hungary. -

Verzeichnis Der Kreditinstitute Und Ihrer Verbände Sowie Der Treuhänder Für Kreditinstitute in Der Bundesrepublik Deutschland

Verzeichnis der Kreditinstitute und ihrer Verbände sowie der Treuhänder für Kreditinstitute in der Bundesrepublik Deutschland Bankgeschäftliche Informationen 2 2020 Deutsche Bundesbank Zentralbereich Banken und Finanzaufsicht Wilhelm-Epstein-Straße 14 60431 Frankfurt am Main Postfach 10 06 02 60006 Frankfurt am Main Telefon 069 9566-1 Durchwahl 069 9566-7194 Telefax 069 9566-5252 bzw. 5601071 Internet http://www.bundesbank.de E-Mail: [email protected] Für die Richtigkeit und Vollständigkeit übernehmen wir keine Gewähr. Bei Auswertungen für Veröffentlichungen oder Nachdruck Quellenangabe erbeten. ISSN 0506-7928 Abgeschlossen am 01. Januar 2020 Vordr. 1035 (INT) Erläuterungen Im “Verzeichnis der Kreditinstitute“ sind alle Kreditinstitute aufgeführt, die Bankgeschäfte gemäß § 1 KWG betreiben. Von den in § 2 KWG erwähnten Instituten sind nur folgende namentlich erfasst: - Deutsche Bundesbank, einschließlich Hauptverwaltungen und Filialen - Kreditanstalt für Wiederaufbau. Die Einteilung der Kreditinstitute nach Bankengruppen wurde nach bankaufsichtlichen Gesichtspunkten vorgenommen. Bei jedem Kreditinstitut ist die Gesamtzahl der Zweigstellen angegeben (bei inländischen Zweigstellen im Regelfall der Vorjahresstand, da die Daten für das laufende Jahr erst zu einem späteren Zeitpunkt erhoben werden); Zweigstellen im Ausland sind einzeln erwähnt. Bei den Zweigstellen ausländischer Banken in der Bundesrepublik (§ 53 KWG) gilt eine vom Mutterinstitut benannte Niederlassung als Kreditinstitut, die weiteren Niederlassungen sind als -

Oracle Global Leaders Summer Meeting EMEA 2020 Oracle Exadata for Analytics Panel

June 23 - 16.15 CET Oracle Global Leaders Program Oracle Global Leaders Summer Meeting EMEA 2020 Oracle Exadata for Analytics Panel Dr. Marcus Prätzas Luis Esteban Stephen Bendall André Giger Enterprise Architect CDO Oracle Technical Authority Head of Unix Platform Services Deutsche Bank - Germany CaixaBank - Spain Vodafone - UK Zürcher Kantonalbank - CH Copyright © 1995, 2019, Oracle. All rights reserved. June 23 - 16.15 CET Oracle Global Leaders Program Oracle Global Leaders Summer Meeting EMEA 2020 Oracle Exadata for Analytics Panel Dr. Marcus Prätzas Luis Esteban Stephen Bendall André Giger Enterprise Architect CDO Oracle Technical Authority Head of Unix Platform Services Deutsche Bank - Germany CaixaBank - Spain Vodafone - UK Zürcher Kantonalbank - CH Copyright © 1995, 2019, Oracle. All rights reserved. Deutsche Bank Oracle Exadata for Analytics Update Dr. Marcus Praetzas, June 2020,Deutsche Bank AG 3 Agenda 1. Introduction Deutsche Bank Exadata Experience & Estate 2. Analytics - Example dbART Platform - Analytics, Reporting and Trending Change Risk Prediction and Quality Assessment Production Support Effort Corona / WfH 3. Exadata Outlook PoC Exadata Cloud Service + Autonomous Database 4 Deutsche Bank AG Founded 1870 in Berlin Picture: Frankfurt Branch by Roßmarkt 18 around 1930. Internationalisation 1955 1988 Global from 1989 now 1989: Acquisition of the British merchant bank Morgan Grenfell 1999: acquisition of Bankers Trust 2006: acquisition Berliner Bank, Norisbank 2010: acquisition Postbank, SalOp. 2017: -

Willkommen Bei Ihrer Worksitebank!

Willkommen bei Ihrer WorksiteBank! Stand: 16.09.2018 Agenda Über die Degussa Bank Unser Produkt- und Serviceangebot Depotführung für Mitarbeiter der M.M. Warburg & CO Anhang Depotführung für Mitarbeiter der M.M. Warburg & CO – Vermögensberatung 2 Über die Degussa Bank WorksiteBanking – Ein einzigartiges Geschäftsmodell Deutschlands einzige WorksiteBank – spezialisiert auf Bankdienstleistungen für Mitarbeiter in Unternehmen Seit mehr als 50 Jahren mit diesem Geschäftsmodell – mit unverwechselbarem Profil Marktführer Aktuell über 411.000 Kunden und 190 Bank-Shops an Standorten renommierter Partnerunternehmen Mitglied des Bankenverbands und des „Einlagensicherungsfonds des Bundesverbandes deutscher Banken e. V. (Einlagenschutz bis zu einer Höhe von rd. 45 Millionen Euro pro Kunde) Umfassendes Worksite Financial Service Angebot über die Tochtergesellschaften Industria (Immobilien), Prinas (Versicherungen) und mitarbeitervorteile.de (exklusive Einkaufsvorteile) Depotführung für Mitarbeiter der M.M. Warburg & CO – Vermögensberatung 4 Eine Bank mit „goldener“ Geschichte 1873: Gründung des Unternehmens Degussa (Deutsche Gold- und Silber- Scheideanstalt) als Bank, hervorgegangen aus der ehemaligen Münzmeisterei Frankfurt 1936: Anerkennung der Degussa als „Devisenbank“ 1947: Zulassung als „Außenhandelsbank“ 1979: Ausgründung der Degussa Bank GmbH als Universalbank aus der Degussa AG Depotführung für Mitarbeiter der M.M. Warburg & CO – Vermögensberatung 5 Dafür stehen wir: Nähe, Transparenz und Vertrauen! Nähe Kurze Wege, schnelle -

2016Deutsche Postbank Ag, Bonn Annual

DEUTSCHE POSTBANK AG, BONN 2016ANNUAL FINANCIAL STATEMENTS (HGB) AS OF DECEMBER 31, 2016 DEUTSCHE POSTBANK AG, BONN ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD ENDED DECEMBER 31, 2016 AND MANAGEMENT REPORT FOR FISCAL YEAR 2016 CONTENTS Management Report 2 Balance Sheet as of December 31, 2016 46 Income Statement for the Period January 1, 2016 to December 31, 2016 48 Notes 50 Auditor‘s Report 96 POSTBANK MANAGEMENT REPORT range for retail customers. In all these areas, Postbank offers some products and services as part of partnerships with fund BUSINESS AND ENVIRONMENT companies, banks, and insurance companies. The Bank also wants to offer its customers prudent guidance on invest - Corporate profile and business model of Postbank ments in a low interest rate environment that go above and beyond savings and checking products, and has recently Corporate profile introduced a new securities strategy in connection with a Postbank has been part of the Deutsche Bank Group, new integrated advisory concept for that purpose. Frankfurt am Main, since December 3, 2010. On its journey to independence Postbank has succeeded with efforts to In its own 1,043 Finance Centers, including the recently estab - create in fiscal year 2016 the general framework for techni- lished sales centers, Postbank offers both comprehensive cal and operational deconsolidation from Deutsche Bank. banking and financial services as well as Deutsche Post AG These efforts have been based on the results of internal services. In addition, the Bank has more than 4,300 Deutsche projects and constitute a necessary prerequisite for the Post AG partner retail outlets, where customers can access planned deconsolidation on the balance sheet. -

DWS Group Gmbh & Co. Kgaa

DWS Group GmbH & Co. KGaA Content Balance Sheet as of December 31, 2018 ...................... 2 Income Statement for the Period from January 1 to December 31, 2018 ........................................................ 3 Notes to the Accounts ..................................................... 4 Corporate Information .................................................. 4 Basis of Presentation ................................................... 4 Accounting and Valuation Principles ............................ 4 Notes to the Balance Sheet ......................................... 6 Notes to the Income Statement .................................. 10 Other Information ....................................................... 12 Corporate Bodies ....................................................... 14 Confirmations .............................................................. 22 Responsibility Statement by the Executive Board ...... 22 Independent Auditor’s Report .................................... 23 Imprint ........................................................................... 28 For internal use only DWS Group GmbH & Co. KGaA Annual Financial Statements Balance Sheet as of December 31, 2018 Annual Report 2018 Balance Sheet as of December 31, 2018 ASSETS in € t. Dec 31, 2018 Dec 31, 2017 A. Fixed assets I. Tangible assets 1. Office furniture and equipment 4 0 II. Financial assets 1. Investments in affiliated companies 7,648,842 6,436,030 7,648,845 6,436,030 B. Current assets I. Receivables and other assets 1. Receivables from affiliated companies a) with term of up to one year 407,168 33,618 b) with term of more than one year 100,000 0 507,168 33,618 2. Other assets 43,097 0 II. Cash on hand, balances with Bundesbank, bank balances and cheques 211,319 41,529 761,584 75,147 C. Deferred tax assets 27,722 0 D. Excess of plan assets over pension liabilities 1,345 0 Total assets 8,439,496 6,511,177 Assets held in trust 3,068 3,068 LIABILITIES AND SHAREHOLDERS' EQUITY in € t. Dec 31, 2018 Dec 31, 2017 A. -

The Pfandbrief Roundtable 2019 in ASSOCIATION with the VDP

The Covered Bond Report www.coveredbondreport.com August 2019 The Pfandbrief Roundtable 2019 IN ASSOCIATION WITH THE VDP The Pfandbrief Roundtable 2019 The EU covered bond legislative package, sustainable finance developments, and a possible revival of APP were key topics in our annual Pfandbrief roundtable, produced in association with the vdp and hosted by pbb on 26 June, with leading players sharing their views ahead of the 250th anniversary of the Pfandbrief in August. Neil Day, The Covered Bond Report: are discussions about tightening the regu- Matthias Melms, NordLB: Indepen- What is it about the Pfandbrief that latory framework, it is important to ensure dently of the issuers and the assets that has resulted in it being such a long- that the Pfandbrief remains competitive are behind the Pfandbrief, when we talk lasting and successful product? versus other products. about 250 years of a success story we have to talk about the Pfandbrief law. A Jens Tolckmitt, Association of German Felix Rieger, Deutsche Bundesbank: foreign investor once told me: I want to Pfandbrief Banks (vdp): The stability I am here representing the Bundesbank as invest in Germany, in the German Pfand- and the high quality of the legal frame- an investor today — not for its role regard- brief, but I don’t care about the issuer, I work have been decisive in making the ing monetary policy — and in this respect, don’t care about the assets, I just want Pfandbrief such a long-lasting product. investing money on behalf of Federal gov- to have the Pfandbrief with the highest What is especially important today, is that ernment entities, the Bundesbank is a spread. -

Scale Economies, Scope Economies, and Looking Beyond the Test of Market-Power and Efficient-Structure Hypotheses: Empirical Evid

Wirtschaftswissenschaftliche Fakultät der Eberhard-Karls-Universität Tübingen Market Structure, Scale Efficiency, and Risk as Determinants of German Banking Profitability Peiyi Yu Werner Neus Tübinger Diskussionsbeitrag Nr. 294 Juni 2005 Wirtschaftswissenschaftliches Seminar Mohlstraße 36, D – 72074 Tübingen Market Structure, Scale Efficiency, and Risk as Determinants of German Banking Profitability 1 2 Peiyi Yu and Werner Neus Abstract The Scale-Efficiency version of the Efficient-Structure Hypothesis and the Structure- Conduct-Performance Hypothesis find empirical support in German banking data from 1998 to 2002. Due to the acceptance of the two hypotheses and the existence of overall economies of scale, we conclude that German banks may improve their profitability by increasing their asset size and/or by consolidation. The increased banking profitability will not only come from monopolistic power (higher concentration rate) but also from the scale efficiency benefit. We also find that portfolio risk is a key factor in determining the profit-structure relationship. Keywords: Profit-structure relationship, Market Structure, Scale efficiency, Portfolio Risk JEL Classification: C33, G21, G14, L11 1 Corresponding Author; Post-doctoral researcher, Faculty of Economics and Business, University of Tübingen, Germany. E-mail: [email protected]. 2 Faculty of Economics and Business, Department of Banking, University of Tübingen, Germany. 1 1. Introduction In a recent paper published by the IMF, Decressin et al. (2003) propose that recent weak bank profitability in Germany appears to be related with structural factors rather than the macro- economic cycle. Some anecdotal evidence and financial ratio analyses are also presented to support this claim. The motivation of this paper is to study the issue of bank profitability in a coherent and rigorous econometric framework with a large panel data set of the German bank- ing industry.