Minicar Subcompact Compact Coupe Mid-Sized Convertible & Roadster Medium Minivan Small Minivan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sportz Sizing Chart Rev

Sportz Truck Tent Sizing Chart Sportz III Tailgate 55011 55022 55044 55055 55077 55099 55890 Sportz III Tailgate Camo 56011 56022 56044 - - - - Sportz Mid Size Quad SPORTZ FULL SIZE CREW Truck Size Full Size Long Bed Full Size Short Bed Compact Short Bed Step/Flare Sport Mid Size Short Bed Cab CAB Bed Size 96-98" 72-79" 72-74" 78-82" 72-78" 65" 68-70" Double/Model # 30951 or Double/Model # 30951 or Double/Model # 30951 or Mid Air Mattress Mid Size/Model #32000SP Mid Size/Model #32000SP Twin/Model # 30954 Twin/Model # 30954 Twin/Model # 30954 Twin/Model # 30954 Size/Model #32000SP T Chevrolet C/K * Chevrolet C/K * Chevrolet S-10 * Chevrolet Silverado* Dodge Dakota Short Bed* Dodge Dakota Quad Cab* GMC Sierra 1500 Crew Cab* R Chevrolet Silverado * Chevrolet Silverado * Chevrolet Colorado 6' Ford F-150 '96 & older* Dodge Dakota SLT Short* Toyota Tacoma (Yr 2005 anChevrolet Crew Cab* U Dodge Dakota * Dodge Ram 1500 * Chevrolet Canyon 6' Ford F-250 '96 & older* Dodge Dakota Sport Short* up for 60 inch box)* Ford Super Crew* C Dodge Dakota SLT * Dodge Ram 2500 * Ford Ranger XL * GMC Sierra 1500* Toyota T-100 * Nissan Titan Crew* K Dodge Dakota Sport * Ford F-150 * Ford Ranger XLT * Toyota Tacoma (Yr 2004 and Dodge Ram 1500 * Ford F-250 * GMC S-15 * up for 73.5 inch box)* M Dodge Ram 2500 * Ford F-250 Super Duty* GMC Sonoma * O Dodge Ram 3500 (^DRW) Ford F-350 Super Duty* Isuzu Hombre * D Ford F-150 * GMC Sierra 2500 Series* Jeep Camanche * E Ford F-250 * Nissan Titan* Mazda B 2000* L Ford F-250 Super Duty* Toyota Tundra * Mazda B 2500* Ford F-350 Super Duty* Mazda B 3000* N Ford F-350SD (^DRW) Mazda B 4000* A GMC Sierra * Mitsubishi Pick-up * M Nissan Titan* Nissan Frontier * E Toyota T-100 * Toyota Hilux* Toyota Tundra * Toyota Tacoma(before2004)* Nissan Frontier King Cab ('02 and Newer)* Models Not Applicable: * Indicates truck must be measured to determine long or short bed. -

Minivan Motoring, Or Why I Miss That Old Car Smell by Sam Patteson

e-Vision volume eight 1 Minivan Motoring, or Why I Miss that Old Car Smell by Sam Patteson It is very difficult to look “cool” while driving a minivan, and I never bothered to try. “Cool” is overrated anyway. What’s not overrated is the urban camouflage a minivan affords. “No one suspects the soccer mom,” Joe deadpanned as he rolled us a joint on the open door of the glove box. I had to agree as I pulled the van into the Shell station to gas up before our long trip to Charleston. I let the tank fill while I checked the various reservoir levels for brake fluid, antifreeze, power steering, and the like. As usual, I needed a quart of oil. Rednecks on last minute beer runs cruised through the parking lot as I returned from the store. Joe blasted Frampton Comes Alive through the open windows. Pete’s guitar had something to say, and the van was rocking. I poured the oil into the engine, slammed the hood home, and slid into the driver’s seat. I turned to quiz Joe on last minute preparations. We had planned this trip for months, and I didn’t want to forget anything. “Suitcases?” He turned to look back at the empty rear of the van. We had removed the back seats in favor of a twin-sized bed. Our suitcases nestled securely between the bed and the back door. “Check.” Pillows and blankets? “Check.” Wallet, money, keys? “Check.” Er… extras? “Check!” Joe coughed and handed me the joint. I took a deep drag and handed it back. -

My Peugeot 3008 My Peugeot 5008

MY PEUGEOT 3008 MY PEUGEOT 5008 HANDBOOK Access to the Handbook MOBILE APPLICATION ONLINE Install the (content available Visit the website and select the Scan MyPeugeot App PEUGEOT offline). ‘MyPeugeot’ section to view or download the handbook or go to the following address: http://public.servicebox.peugeot.com/APddb/ Scan this QR Code for direct access. Then select: – the vehicle, Select: – the issue period corresponding to the vehicle’s initial – the language, registration date. – the vehicle and body style, – the issue period of the handbook corresponding to the vehicle’s initial registration date. This symbol indicates the latest information available. Welcome Key Safety warning Thank you for choosing a Peugeot 3008 or a Peugeot 5008. This document presents the key information and recommendations required Additional information for you to be able to explore your vehicle in complete safety. We strongly recommend familiarising yourself with this document and the Warranty and Maintenance Record. Environmental protection feature Your vehicle will be fitted with only some of the equipment described in this document, depending on its trim level, version and the specification for the Left-hand drive vehicle country in which it was sold. The descriptions and illustrations are for guidance only. Automobiles PEUGEOT reserves the right to modify the technical specifications, Right-hand drive vehicle equipment and accessories without having to update this guide. If ownership of your vehicle is transferred, please ensure this Handbook is Location -

All-New Peugeot 508 Now with Technology

ALL-NEW PEUGEOT 508 NOW WITH TECHNOLOGY PRICES, EQUIPMENT AND TECHNICAL SPECIFICATIONS Version 11 - November 2019 Model Year - 2020 Standard Specification- all-new PEUGEOT 508 All-New PEUGEOT 508 models come with the following equipment as standard: Safety and Security Interior Features − ABS (Anti-lock Braking System) − Dashboard, front and rear door panel finish : Carbon effect − Active bonnet − Flocked glove box interior with illumination − Airbags − Gear lever - automatic in full grain leather and satin − Adaptive driver and front passenger airbags (includes passenger airbag chrome deactivation function) − Gear lever - manual in satin chrome (6 speed gearbox) − Driver and front passenger side thorax airbags − 'Interior LED lighting: front LED roof lighting with 3 x − Front and rear curtain airbags spotlights, 2 x LED ambient lights and 2 x rear reading − Alarm (perimetric, volumetric with lift and tilt sensor) lamps, LED lighting in boot, glove box and connecting − Automatic door locking when moving off zone − Automatic hazard light activation upon heavy brake application − Pedals and foot rest: black rubber − DAA1 (Driver attention alert system) − 'Piano keys': chrome plated toggle switches to access − Eco-coaching touchscreen functions − Electric child locking functionality on rear windows and doors − Roof lining - 'Salin' light grey − EBA (Emergency Brake Assist) − EBD (Electronic Brake Force Distribution) In Car Entertainment − ESP (Electronic Stability Programme) − Exterior temperature indicator with ice warning − Bluetooth® telephone facility − Front optimised safety headrests and rear retractable headrests (x3), height- − USB socket (x2) front adjustable. − 8-speaker radio, MP3 compatible − Front three-point retractable seatbelts, height adjustable with pre-tensioners − 12 V socket (Active only) and force limiters. -

BMW Price List

Recommended Retail Price List – January 2021 Fuel Consumption Electrical Energy VES (band) Retail Price (l/100km) (kWh/100km) BMW 1 Series 116i Sport B 5.5 $146,888 116i Luxury B 5.5 $151,888 BMW 2 Series 216i Active Tourer Sport B 6.3 $157,888 216i Gran Tourer Sport B 6.5 $163,888 216i Gran Tourer Luxury B 6.5 $170,888 218i Gran Coupe Luxury B 5.5 $171,888 218i Gran Coupe M Sport B 5.5 $174,888 BMW 3 Series 318i Sedan Sport B 5.8 $208,888 320i Sedan Luxury - - P.O.A. 320i Sedan M Sport - - P.O.A. 330e Sedan Luxury A2 2.2 15.4 $261,888 BMW 4 Series 420i Coupe M Sport B 5.8 $228,888 430i Coupe M Sport Pro B 6.2 $276,888 BMW 5 Series 520i Sedan C1 5.5 $259,888 520i Sedan Luxury C1 5.5 $277,888 520i Sedan M Sport C1 5.5 $287,888 530i Sedan M Sport B 5.6 $299,888 530i Sedan M Sport Edition B 5.6 $308,888 530e Sedan B 1.9 15.3 $278,888 Booking Fees (Non-refundable and inclusive of $10,000 COE deposit): A1. BMW 1 Series / BMW 2 Series / BMW 3 Series / BMW X1/ BMW X2 / BMW i3 $20,000 A2. BMW 4 Series / BMW 5 Series / BMW 6 Series / BMW 7 Series / BMW 8 Series / BMW X3 / BMW X4 / BMW X5 / BMW X6 / BMW $28,000 X7 / BMW Z4 B1. Special Indent cars – BMW 1 Series / BMW 2 Series / BMW 3 Series / BMW 4 Series / BMW 5 Series $30,000 BMW X1 / BMW X2 / BMW X3 / BMW X4 / BMW i3 / BMW Z4 B2. -

Quantitative Study to Define the Relevant Market in the Passenger Car Sector by Frank Verboven, K.U

1 17 September 2002 Final Report _____________________ Frank Verboven _____________________ Catholic University of Leuven 1 This study has been commissioned by the Directorate General of Competition of the European Commission. Any views expressed in it are those of the author: they do not necessarily reflect the views of the Directorate General of Competition or the European Commission. 1 EXECUTIVE SUMMARY ....................................................................................................................3 1 INTRODUCTION.........................................................................................................................7 2 DEFINING THE RELEVANT MARKET .................................................................................8 2.1 COMPETITIVE CONSTRAINTS ..................................................................................................8 2.2 DEMAND SUBSTITUTION.........................................................................................................9 2.3 PRODUCT VERSUS GEOGRAPHIC MARKET............................................................................10 3 THE RELEVANT GEOGRAPHIC MARKET .......................................................................11 3.1 HISTORICAL EVIDENCE.........................................................................................................11 3.2 OBSTACLES TO CROSS-BORDER TRADE.................................................................................12 4 THE DEMAND FOR NEW PASSENGER CARS...................................................................14 -

QUAD-CITIES BRITISH AUTO CLUB 2017 Edition / Issue 12 5 December 2017

QUAD-CITIES BRITISH AUTO CLUB 2017 Edition / Issue 12 5 December 2017 CHRISTMAS EDITION CONTENTS The QCBAC 1 THE QCBAC The QCBAC was formed to promote interest and usage of any and all British Christmas Puzzle 1 cars. The QCBAC website is at: http://www.qcbac.com QCBAC Contacts 1 Christmas Dinner 2 Clues and Puzzle Clues 2 word list are on Puzzle Word List 2 page 2. Board Meeting 3 Car of the Month 4 British Auto News 15 Crossword Answer 20 Question Answer 20 Thanks to the Board 20 QCBAC CONTACTS President Jerry Nesbitt [email protected] Vice President Larry Hipple [email protected] Secretary John Weber [email protected] Treasurer Dave Bishop [email protected] Board member Carl Jamison [email protected] Board member Gary Spohn [email protected] Autofest Chair Frank Becker [email protected] 2017 Santa Test Run Membership Chair Pegg Shepherd [email protected] Publicity Chair Glen Just [email protected] Page 1 of 20 QCBAC CHRISTMAS DINNER BRIT CAR QUESTION The QCBAC Christmas will take place on 10 December at Montana Jacks, 5400 27th St, Moline, IL. Bring a wrapped $5 gift for the traditional secret gift You are probably familiar exchange. with the British driver Malcolm Campbell who RSVP to Linda Weber: [email protected] held numerous land speed by 30 November so the appropriate space can be reserved. records from 1924 to 1935. The 1935 301.3 mph LSR was made in the 1931 Blue CHRISTMAS PUZZLE CLUES Bird powered by a 2,300 hp Rolls Royce V12. -

Peugeot 508 / 508 Sw Experience Quality Time

PEUGEOT 508 / 508 SW EXPERIENCE QUALITY TIME The Peugeot 508 combines Peugeot’s new visual identity with the latest engine technology, class leading driveability, high levels of quality and safety to offer a spacious and comfortable car in both saloon or SW guise. INTENSE EMOTIONS The Peugeot 508’s strong but elegant exterior design exudes power and refinement. At the front, Peugeot’s designers have paid particular attention to the single floating grille and piercing headlights to create a slick, feline look. At the rear, three prominent red claws house the rows of six LEDs to form the stylish rear tail lights. MOMENTS OF REFINEMENT Inside the 508, the stylish high-tech interior rewards passengers with easy to reach controls, exceptional space and superb levels of comfort. The simple and elegant style of the fascia, the durable and high-quality materials used and the meticulous finish add to the ambience of the passenger compartment. COMFORT ON DEMAND Take your seat on board the 508 or 508 SW and you’ll immediately experience a feeling of satisfaction. Well-designed architecture means you’ll enjoy both a generous amount of space and equipment that is perfectly suited to your needs. Storage compartments For convenience, the 508 and 508 SW include several carefully considered storage spaces to make life on board even easier: a glove box ventilated with cool air, 2 cup holders in the front, spacious door pockets and a storage compartment under the central armrest. Seats The front seats have been developed to deliver style, comfort and support. Electric and heated front seats are available as standard on Allure models, along with full leather upholstery. -

Das Flottenprogramm Von Hyundai Für Jedes Business Das Richtige Format EDITORIAL INHALT Liebe Leserinnen Und Leser

Sonderedition aboutFLEET Das Flottenprogramm von Hyundai Für jedes Business das richtige Format EDITORIAL INHALT Liebe Leserinnen und Leser Hyundai gehört zu den drei grössten Automobilproduzenten der Hyundai im Porträt Welt. Das verdankt die Marke ihrer Innovationskraft, der attraktiven Entwicklung weltweit und in der Schweiz Seite 3 Modellpalette und nicht zuletzt einer herausragenden Qualität, die durch ein Top-Garantieversprechen - jeder neue Hyundai Perso- Vorteile für Flottenbetreiber nenwagen hat fünf Jahre Werksgarantie ohne Kilometerbegrenzung Top bei Garantien und TCOs Seite 4 - untermauert wird. Die Hyundai Fleet Business Center Auch in Europa und der Schweiz reitet Hyundai seit Jahren auf Geballte Flottenkompetenz Seite 5 einer Erfolgswelle. Mit ein Grund dafür ist das Hyundai Motor Europe Technical Center im deutschen Rüsselsheim. Hier entwickeln Hyundai i10 und i20 versierte Ingenieure Fahrzeuge, die gezielt auf die Bedürfnisse der Kleinwagen für Anspruchsvolle Seite 6 europäischen Kunden ausgerichtet sind. Hyundai i20 Coupé und ix20 In den letzten Monaten hat Hyundai eine Vielzahl attraktiver Mo- Noch mehr Vielfalt im City-Format Seite 7 dellneuheiten präsentiert. Dazu gehören beispielsweise der Klein- wagen New Generation i20, der frisch aufgelegte Kompakte i30, der Hyundai i30 Coupé, 5-Door und Wagon ebenfalls neue Mittelklasse-Vertreter i40 sowie das leichte Nutz- Kompakte Trendsetter Seite 8 fahrzeug H350. Zusammen mit diesen und den weiteren Modellen ist Hyundai vom Cityflitzer bis zum 3,5-Tönner in jedem wichtigen Hyundai i40 Sedan und Wagon Segment vertreten. Oberklassige Mittelklasse Seite 9 Viele Flottenbetreiber haben die Modellvielfalt von Hyundai für sich Hyundai Tucson entdeckt und setzen auf die koreanisch-europäische Erfolgsmarke. SUV auf die kompakte Art Seite 10 Kein Wunder, denn die Vorzüge der Modelle zeigen sich besonders im Flottenbetrieb. -

The Bmw 1 Series

THE BMW 1 SERIES. April 2019 MODELS. 118i (1R52) Model Highlights: • 8-speed Steptronic transmission • 16" light alloy wheels Star-spoke style 654 • BMW TwinPower Turbo 3-cylinder petrol engine Product Details: • Concierge Services [1] [1] • Cruise control with braking function Consumption: 5.2l / 100km CO2: 122g/ km • Navigation system Business 0-100km/h: 8.7 sec Transmission: 8-speed automatic • Park Distance Control (PDC), rear • Rain sensor Engine: 3-cylinder Power/Torque: 100kW / 220Nm • Real Time Traffic Information (RTTI) • Rear view camera Price incl. GST $47,200 125i (1S32) Model Highlights: • 8-speed Steptronic sport transmission • 18'' light alloy wheels Double-spoke style 385 • Automatic air conditioning, 2 zone • BMW TwinPower Turbo 4-cylinder petrol engine Product Details: • Interior rear-view mirror with automatic anti- [1] [1] dazzle function Consumption: 5.9l / 100km CO2: 134g / km • LED fog lights 0-100km/h: 6.1 sec Transmission: 8-speed sport automatic • LED headlights • Seat heating for driver and front passenger Engine: 4-cylinder Power/Torque: 165kW / 310Nm • Sport Line • Sport seats for driver and front passenger Price incl. GST $59,700 [1] IMPORTANT INFORMATION ABOUT OUR DATA Fuel consumption is determined in accordance with the ECE driving cycle (93/116/EC) made up of approximately one third urban traffic and two thirds extra-urban driving (based on the distance covered). CO2 emissions are measured in addition to fuel consumption. All data is presented based on a vehicle of this model with standard equipment as tested for the German market. Where those vehicles are available in a right hand drive variant, they can be specially ordered from the factory by New Zealand customers. -

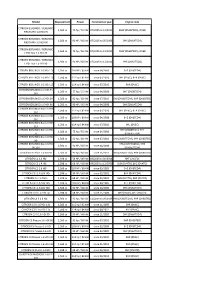

Model Displacement Power Construction Year Engine Code

Model Displacement Power Construction year Engine code CITROËN BERLINGO / BERLINGO 1,560 cc 75 hp / 55 kW 07/2005 to 12/2011 9HW (DV6BTED4), DV6B FIRST MPV 1.6 HDI 75 CITROËN BERLINGO / BERLINGO 1,560 cc 90 HP / 66 kW 07/2005 to 05/2008 9HX (DV6ATED4) FIRST MPV 1.6 HDI 90 CITROËN BERLINGO / BERLINGO 1,560 cc 75 hp / 55 kW 07/2005 to 12/2011 9HW (DV6BTED4), DV6B FIRST Box 1.6 HDI 75 CITROËN BERLINGO / BERLINGO 1,560 cc 90 HP / 66 kW 07/2005 to 12/2011 9HX (DV6ATED4) FIRST Box 1.6 HDI 90 CITROËN BERLINGO 1.6 HDi 110 1,560 cc 109 HP / 80 kW since 04/2008 9HZ (DV6TED4) CITROËN BERLINGO 1.6 HDi 110 1,560 cc 112 hp / 82 kW since 07/2010 9HL (DV6C), 9HR (DV6C) CITROËN BERLINGO 1.6 HDi 115 1,560 cc 114 hp / 84 kW since 07/2010 9HR (DV6C) CITROËN BERLINGO 1.6 HDi 75 1,560 cc 75 hp / 55 kW since 04/2008 9HT (DV6BTED4) 16V CITROËN BERLINGO 1.6 HDi 90 1,560 cc 92 hp / 68 kW since 07/2010 9HJ (DV6DTEDM), 9HP (DV6DTED) CITROËN BERLINGO 1.6 HDi 90 1,560 cc 90 HP / 66 kW since 04/2008 9HX (DV6ATED4) CITROËN BERLINGO Box 1.6 HDi 1,560 cc 112 hp / 82 kW since 07/2010 9HL (DV6C), 9HR (DV6C) 110 CITROËN BERLINGO Box 1.6 HDi 1,560 cc 109 HP / 80 kW since 04/2008 9HZ (DV6TED4) 110 CITROËN BERLINGO Box 1.6 HDi 1,560 cc 114 hp / 84 kW since 07/2010 9HL (DV6C) 115 CITROËN BERLINGO Box 1.6 HDi 9HT (DV6BTED4), 9HT 1,560 cc 75 hp / 55 kW since 04/2008 75 (DV6BUTED4) CITROËN BERLINGO Box 1.6 HDi 1,560 cc 92 hp / 68 kW since 07/2010 9HJ (DV6DTEDM), 9HP (DV6DTED) 90 CITROËN BERLINGO Box 1.6 HDi 9HS (DV6TED4BU), 9HX 1,560 cc 90 HP / 66 kW since 04/2008 90 16V (DV6AUTED4) -

PEUGEOT 108 Top Range : Equipment

PEUGEOT 108 top range : equipment PEUGEOT Car Range Pricing Guide Pricing Valid from 1st November 2019 A PEUGEOT For EVERY Occasion Hatchbacks Page 4 Page 9 Page 17 108 208 Compact, chic and full of character. If you're looking for a 308 fun way to get around town, the 108 will be right up your Behind its neat and compact appearance, this car is The PEUGEOT 308 is a real show-stopper, with a street. bursting with energy and ambition – just like you. stunning design, superior technology and ultra-efficient engines. SUVs Page 13 Page 23 Page 28 2008 SUV 3008 SUV 5008 SUV A strong visual signature ensures the 2008 SUV The PEUGEOT 3008 SUV unveils its strength and Enter a new dimension with PEUGEOT 5008 SUV,offering commands road presence and offers a distinctive air of character. Featuring a sleek design,this distinct SUV cutting edge technology and the flexibility offered by adventure. combines robustness with elegance. seven individual seats Fastback Estate Page 39 Page 40 Page 17 All-new 508 All-new 508 SW 308 SW Discover the all-new PEUGEOT 508: the radical Fastback Discover the all-new Peugeot 508 SW: the premium estate The 308 SW, is the ultimate family car. with a bold look , offering advanced technology for an car with uncompromising design, combining the comfort Feel good behind the wheel, its attention to detail and outstanding driving experience. of a tourer. cavernous 660 litre boot set it apart from its rivals. MPVs Cabrio Page 4 Page 33 Page 44 108 TOP! All-new Rifter This 5-door cabrio, comes with a retractable electric fabric Traveller Featuring great levels of comfort, outstanding modularity roof and wind deflector so that you can enjoy that Distinctive design, expert PEUGEOT handling, elegance and intelligent storage solutions, all-new Rifter is the “outdoor” experience throughout the year.