Baird Marketing Tech & Services Industry Report 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Media Nations 2019

Media nations: UK 2019 Published 7 August 2019 Overview This is Ofcom’s second annual Media Nations report. It reviews key trends in the television and online video sectors as well as the radio and other audio sectors. Accompanying this narrative report is an interactive report which includes an extensive range of data. There are also separate reports for Northern Ireland, Scotland and Wales. The Media Nations report is a reference publication for industry, policy makers, academics and consumers. This year’s publication is particularly important as it provides evidence to inform discussions around the future of public service broadcasting, supporting the nationwide forum which Ofcom launched in July 2019: Small Screen: Big Debate. We publish this report to support our regulatory goal to research markets and to remain at the forefront of technological understanding. It addresses the requirement to undertake and make public our consumer research (as set out in Sections 14 and 15 of the Communications Act 2003). It also meets the requirements on Ofcom under Section 358 of the Communications Act 2003 to publish an annual factual and statistical report on the TV and radio sector. This year we have structured the findings into four chapters. • The total video chapter looks at trends across all types of video including traditional broadcast TV, video-on-demand services and online video. • In the second chapter, we take a deeper look at public service broadcasting and some wider aspects of broadcast TV. • The third chapter is about online video. This is where we examine in greater depth subscription video on demand and YouTube. -

The Retail Transformation Cultivating Choice, Experience, and Trust

The retail transformation Cultivating choice, experience, and trust From the Deloitte Center for the Edge A report in the Future of the Business Landscape series About the authors John Hagel III (co-chairman, Deloitte Center for the Edge) has nearly 30 years of experience as a management consultant, author, speaker, and entrepreneur. He has helped companies improve per- formance by applying IT to reshape business strategies. In addition to holding significant positions at leading consulting firms and companies throughout his career, Hagel is the author of bestselling business books such as Net Gain, Net Worth, Out of the Box, The Only Sustainable Edge, and The Power of Pull. John Seely Brown (JSB) (independent co-chairman, Deloitte Center for the Edge) is a prolific writer, speaker, and educator. In addition to his work with the Center for the Edge, JSB is Adviser to the Provost and a visiting scholar at the University of Southern California. This position followed a lengthy tenure at Xerox Corporation, where he was chief scientist and director of the Xerox Palo Alto Research Center. JSB has published more than 100 papers in scientific journals and authored or co-authored seven books, including The Social Life of Information, The Only Sustainable Edge, The Power of Pull, and A New Culture of Learning. Tamara Samoylova (head of research, Deloitte Center for the Edge) leads the Center’s research agenda and manages rotating teams of Edge Fellows. Prior to joining the Center, Samoylova served as a senior manager in Deloitte Consulting LLP’s Growth and Innovation practice, helping mature companies find new areas of growth by better understanding unmet customer needs, industry dynamics, and competitive moves. -

![The Market for Real Estate Presales: a Theoretical Approach [Electronic Version]](https://docslib.b-cdn.net/cover/0544/the-market-for-real-estate-presales-a-theoretical-approach-electronic-version-350544.webp)

The Market for Real Estate Presales: a Theoretical Approach [Electronic Version]

Cornell University School of Hotel Administration The Scholarly Commons Articles and Chapters School of Hotel Administration Collection 2012 The aM rket for Real Estate Presales: A Theoretical Approach Robert Edelstein University of California, Berkeley Peng Liu Cornell University School of Hotel Administration, [email protected] Fang Wu Citadel Asset Management Follow this and additional works at: http://scholarship.sha.cornell.edu/articles Part of the Real Estate Commons Recommended Citation Edelstein, R., Liu, P., & Wu, F. (2012). The market for real estate presales: A theoretical approach [Electronic version]. Retrieved [insert date], from Cornell University, School of Hotel Administration site: http://scholarship.sha.cornell.edu/articles/1007/ This Article or Chapter is brought to you for free and open access by the School of Hotel Administration Collection at The choS larly Commons. It has been accepted for inclusion in Articles and Chapters by an authorized administrator of The choS larly Commons. For more information, please contact [email protected]. The aM rket for Real Estate Presales: A Theoretical Approach Abstract Presale agreements have become a pervasive worldwide practice for residential sales, especially in many Asian markets. Although there is a burgeoning empirical literature on presales agreements, only a few papers actually address their theoretical foundations. We create a set of interrelated theoretical models for explaining how and why developers and buyers engage in presale contracts for non-completed residential dwellings. Given heterogeneous consumer beliefs about future market prices, developers and buyers enter into presale agreements to mitigate, two intertwined, fundamental risks: those of real estate market valuation and default. Our analyses are consistent with prior empirical findings and provide additional theoretical insights for understanding the market for presales. -

Market Update – April 2019

REPORTS Market Update – April 2019 DIGITAL SOCIAL TELEVISION 08 APR 2019 Welcome to the first of our MediaCom Market Updates of 2019. A few highlights include the introduction of News UK’s influencer marketing agency; BBC and ITV’s launch of BritBox in the UK and the new HFSS policy across TFL’s estate. Publishing News UK launches full-service influencer marketing agency The Fifth News UK recently announced they were launching their very own influencer marketing agency, The Fifth, offering a different approach to the variety of other influencer agencies in the market by focusing on an influencer’s editorial tone and format rather than their reach. The agency will also aim to identify talent and provide representation, storytelling strategy, creative production, cross-media amplification and events for both brands and influencers. The launch of The Fifth is an incredibly exciting entry from News UK into the area of Influencer marketing, which continues to grow at a rapid pace and which shows no signs of stopping. Having said that, the field is still very much in its infancy and a few bumps in the road are to be expected. Managing Director Oliver Lewis says, “Brands require more support identifying the right talent, building longer-term partnerships, authenticating their background, proving meaningful ROI and delivering authentic and diverse stories.” With their human first approach, The Fifth represents a measured response to challenges in the market (namely surrounding authenticity) and aims to provide a variety of opportunities for media agencies to strengthen partnerships for their clients. From an overall market view, this proposition is incredibly exciting as it adds another string to the News UK portfolio, already boasting a successful publishing and audio products. -

JH Inv Funds Series I OEIC AR 05 2021.Indd

ANNUAL REPORT & ACCOUNTS For the year ended 31 May 2021 Janus Henderson Investment Funds Series I Janus Henderson Investment Funds Series I A Who are Janus Henderson Investors? Global Strength 14% 13% £309.6B 55% 45% 31% 42% Assets under Over 340 More than 2,000 25 Over 4,300 management Investment professionals employees Offi ces worldwide companies met by investment teams in 2020 North America EMEA & LatAm Asia Pacifi c Source: Janus Henderson Investors, Staff and assets under management (AUM) data as at 30 June 2021. AUM data excludes Exchange-Traded Note (ETN) assets. Who we are Janus Henderson Investors (‘Janus Henderson’) is a global asset manager off ering a full suite of actively managed investment products across asset classes. As a company, we believe the notion of ‘connecting’ is powerful – it has shaped our evolution and our world today. At Janus Henderson, we seek to benefi t clients through the connections we make. Connections enable strong relationships based on trust and insight aswell as the fl ow of ideas among our investment teams and our engagement with companies. These connections are central to our values, to what active management stands for and to the long-term outperformance we seek to deliver. Our commitment to active management off ers clients the opportunity to outperform passive strategies over the course of market cycles. Through times of both market calm and growing uncertainty, our managers apply their experience weighing risk versus reward potential – seeking to ensure clients are on the right side of change. Why Janus Henderson Investors At Janus Henderson, we believe in linking our world-class investment teams and experienced global distribution professionals with our clients around the world. -

Building New Branding Experiences

Bulding New Brand Experiences We’re the Creative Agency You’ve Been Searching for WE’RE FEARLESS. WE’RE FRESH. WE’RE FUN. We’re not afraid of big ideas; We have stylish and Advertising is supposed to be a you shouldn’t be either. These sophisticated tastes. We little bit fun. Creating exciting are the game changers. It takes take great pride in being concepts, running campaigns, a little more work to sell them storytellers, solving problems, building websites…what’s not up the ladder, but it’s worth it. and making ideas work— to love? beautifully. We push creative ideas to the limit to break through the noise and engage a new breed of consumer. 1.669.223.1578 www.hivemindinc.com 2 1. A Blank Canvas Starting with a Blank Canvas hether you’re rebranding Companies are always looking for agencies with a bricks and mortar retail strong experience in their own brand category. And store, or simply adding that’s not completely unreasonable. One hopes to ecommerce to the mix, get an agency that understands the vernacular and most companies marketing maybe the “secrets” of the industry. But the truth to multiple audiences need to rethink their brands of the matter is that all clients are very different Wfrom time to time. and it’s unlikely that a solution that works for one If you’re very lucky, you can start at the beginning company will work for another. The idea of “best and reevaluate the name of your company or practices” assumes that one solution applies across product line. -

Advertising and Sales Promotion Guide

DOCUMENT RESUME ED 313 501 CE-053-52-7- TITLE Advertising and, Sales Promotion Guide. INSTITUTION North Carolina State Dept. cf Public Instruction-, Raleigh. Div. of Vocational Education. PUB DATE 89 NOTE 151p. PUB TYPE Guides - Classroom Use - Guides (For Teachers) (:52) EDRS PRICE MF01/PC07 Plus Postage. DESCRIPTORS *Advertising; Competency Based Education; Display Aids; *Distributive Education; High Schools; *Marketing; *Merchandising; *Publicity; Salesmanship; *Sales Occupations; State Curriculum Guides IDENTIFIERS North Carolina ABSTRACT This document contains teacher materials for a 4-unit, 1-year marketing education course in advertising and sales promotion offered in grades 11 and 12 in North Carolina. The preface contains a rationale for the development of the course, a course description,course objectives, a list of the instructional units of the course, and a list of the sections contained in each unit. A separate statement, which describes promotion activities intended to enable gOods and services to appear favorable to customers) as a major function of marketing states that this guide's purpose is tOprovide high school students with the initial training for career areas such as display, advertising, and sales promotion. Fifty-six competency objectives are _fisted for the course. Subjects of the four instructional units are: overview of advertising and -promotion; advertising, and publicity; visual merchandising/display; and selling. Components of each unit are: (1) a table of contents for the unit; (2) the competency goal statement and competency objectives; (3) a content-teaching outline; (4) student activities; (5) evaluation measures; (6) keys to the test items; and (7) references. (CML) * Reproductions' supplied by-EDRS are the best that can be made * * from the original document. -

March 2017 M&A and Investment Summary Table of Contents

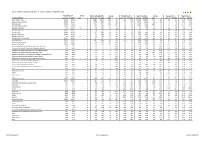

March 2017 M&A and Investment Summary Table of Contents 1 Overview of Monthly M&A and Investment Activity 3 2 Monthly M&A and Investment Activity by Industry Segment 8 3 Additional Monthly M&A and Investment Activity Data 40 4 About Petsky Prunier 52 Securities offered through Petsky Prunier Securities, LLC, member of FINRA. This M&A and Investment Summary has been prepared by and is being distributed in the United States by Petsky Prunier, a broker dealer registered with theU.S.SECandamemberof FINRA. 2| M&A and Investment Summary March 2017 M&A and Investment Summary for All Segments Transaction Distribution . A total of 545 deals were announced in March 2017, of which 315 were worth $19.9 billion in aggregate reported value . Software was the most active segment with 180 deals announced — 120 of these transactions reported $8.4 billion in value . Digital Media/Commerce was also active with 126 transactions announced, of which 90 were worth a reported $5.5 billion in value . Strategic buyers announced 242 deals (44 reported $11.0 billion in value) . VC/Growth Capital investors announced 290 transactions (267 reported $7.8 billion in value) . Private Equity investors announced 13 deals during the month (four reported $1.0 billion in value) March 2017 BUYER/INVESTOR BREAKDOWN Transactions Reported Value Strategic Buyout Venture/Growth Capital # % $MM % # $MM # $MM # $MM Software 180 33% $8,400.0 42% 60 $6,181.3 7 $215.6 113 $2,003.1 Digital Media/Commerce 126 23% 5,451.1 27% 37 853.2 2 ‐ 87 4,597.9 Marketing Technology 85 16% 3,120.9 16% -

FTSE Russell Publications

2 FTSE Russell Publications 19 August 2021 FTSE 250 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Infrastructure 0.43 UNITED Bytes Technology Group 0.23 UNITED Edinburgh Investment Trust 0.25 UNITED KINGDOM KINGDOM KINGDOM 4imprint Group 0.18 UNITED C&C Group 0.23 UNITED Edinburgh Worldwide Inv Tst 0.35 UNITED KINGDOM KINGDOM KINGDOM 888 Holdings 0.25 UNITED Cairn Energy 0.17 UNITED Electrocomponents 1.18 UNITED KINGDOM KINGDOM KINGDOM Aberforth Smaller Companies Tst 0.33 UNITED Caledonia Investments 0.25 UNITED Elementis 0.21 UNITED KINGDOM KINGDOM KINGDOM Aggreko 0.51 UNITED Capita 0.15 UNITED Energean 0.21 UNITED KINGDOM KINGDOM KINGDOM Airtel Africa 0.19 UNITED Capital & Counties Properties 0.29 UNITED Essentra 0.23 UNITED KINGDOM KINGDOM KINGDOM AJ Bell 0.31 UNITED Carnival 0.54 UNITED Euromoney Institutional Investor 0.26 UNITED KINGDOM KINGDOM KINGDOM Alliance Trust 0.77 UNITED Centamin 0.27 UNITED European Opportunities Trust 0.19 UNITED KINGDOM KINGDOM KINGDOM Allianz Technology Trust 0.31 UNITED Centrica 0.74 UNITED F&C Investment Trust 1.1 UNITED KINGDOM KINGDOM KINGDOM AO World 0.18 UNITED Chemring Group 0.2 UNITED FDM Group Holdings 0.21 UNITED KINGDOM KINGDOM KINGDOM Apax Global Alpha 0.17 UNITED Chrysalis Investments 0.33 UNITED Ferrexpo 0.3 UNITED KINGDOM KINGDOM KINGDOM Ascential 0.4 UNITED Cineworld Group 0.19 UNITED Fidelity China Special Situations 0.35 UNITED KINGDOM KINGDOM KINGDOM Ashmore -

Hallett Arendt Rajar Topline Results - Wave 3 2019/Last Published Data

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 3 2019/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share STATION/GROUP Last Pub W3 2019 000's % Last Pub W3 2019 000's % Last Pub W3 2019 Last Pub W3 2019 000's % Last Pub W3 2019 Last Pub W3 2019 Bauer Radio - Total 55032 55032 0 0% 18083 18371 288 2% 33% 33% 156216 158995 2779 2% 8.6 8.7 15.3% 15.9% Absolute Radio Network 55032 55032 0 0% 4743 4921 178 4% 9% 9% 35474 35522 48 0% 7.5 7.2 3.5% 3.6% Absolute Radio 55032 55032 0 0% 2151 2447 296 14% 4% 4% 16402 17626 1224 7% 7.6 7.2 1.6% 1.8% Absolute Radio (London) 12260 12260 0 0% 729 821 92 13% 6% 7% 4279 4370 91 2% 5.9 5.3 2.1% 2.2% Absolute Radio 60s n/p 55032 n/a n/a n/p 125 n/a n/a n/p *% n/p 298 n/a n/a n/p 2.4 n/p *% Absolute Radio 70s 55032 55032 0 0% 206 208 2 1% *% *% 699 712 13 2% 3.4 3.4 0.1% 0.1% Absolute 80s 55032 55032 0 0% 1779 1824 45 3% 3% 3% 9294 9435 141 2% 5.2 5.2 0.9% 1.0% Absolute Radio 90s 55032 55032 0 0% 907 856 -51 -6% 2% 2% 4008 3661 -347 -9% 4.4 4.3 0.4% 0.4% Absolute Radio 00s n/p 55032 n/a n/a n/p 209 n/a n/a n/p *% n/p 540 n/a n/a n/p 2.6 n/p 0.1% Absolute Radio Classic Rock 55032 55032 0 0% 741 721 -20 -3% 1% 1% 3438 3703 265 8% 4.6 5.1 0.3% 0.4% Hits Radio Brand 55032 55032 0 0% 6491 6684 193 3% 12% 12% 53184 54489 1305 2% 8.2 8.2 5.2% 5.5% Greatest Hits Network 55032 55032 0 0% 1103 1209 106 10% 2% 2% 8070 8435 365 5% 7.3 7.0 0.8% 0.8% Greatest Hits Radio 55032 55032 0 0% 715 818 103 14% 1% 1% 5281 5870 589 11% 7.4 7.2 0.5% -

Morning Wrap

Morning Wrap Today ’s Newsflow Equity Research 11 Mar 2019 08:55 GMT Upcoming Events Select headline to navigate to article UK Financials OSB; CCFS Previews / Genius M&A Ploy Company Events 11-Mar ARYZTA; H119 results Provident Financial FY18 Preview / NSF transaction Norwegian Air Shuttle; February 2019 Traffic Stats documentation review 12-Mar 888 Holdings; FY18 Results ARYZTA; H119 results Draper Esprit Maintaining a high level of activity Domino's Pizza Group; FY18 Results Forterra; FY results Building Materials Irish construction PMI rebounds in 13-Mar Provident Financial; FY18 Results 14-Mar Lufthansa; February 2019 Traffic Stats February OneSavings Bank; FY18 Results 15-Mar FBD Holdings; FY19 Results Lufthansa Recommendation moves to a Buy (prev. Hold) IPL Plastics; FY18 Results Economic View Optimism in short supply in advance of J D Wetherspoon; Q219 Results Restaurant Group; FY18 Results crucial week in Brexit Irish Banks Report to show that non-bank lenders best chance of lower rates Economic Events Ireland United Kingdom United States Europe This document is intended for the sole use of Goodbody Stockbrokers and its affiliates Goodbody Capital Markets Equity Research +353 1 6419221 Equity Sales +353 1 6670222 Bloomberg GDSE<GO> Goodbody Stockbrokers UC, trading as “Goodbody”, is regulated by the Central Bank of Ireland. In the UK, Goodbody is authorised and subject to limited regulation by the Financial Conduct Authority. Goodbody is a member of the Irish Stock Exchange and the London Stock Exchange. Goodbody is a member of the FEXCO group of companies. For the attention of US clients of Goodbody Securities Inc, this third-party research report has been produced by our affiliate, Goodbody Stockbrokers Goodbody Morning Wrap UK Financials OSB; CCFS Previews / Genius M&A Ploy OSB is due to publish FY18 results on Thursday 14th March. -

Hallett Arendt Rajar Topline Results - Wave 1 2020/Last Published Data

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 1 2020/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share STATION/GROUP Last Pub W1 2020 000's % Last Pub W1 2020 000's % Last Pub W1 2020 Last Pub W1 2020 000's % Last Pub W1 2020 Last Pub W1 2020 Bauer Radio - Total 55032 55032 0 0% 18160 17986 -174 -1% 33% 33% 155537 154249 -1288 -1% 8.6 8.6 15.9% 15.7% Absolute Radio Network 55032 55032 0 0% 4908 4716 -192 -4% 9% 9% 34837 33647 -1190 -3% 7.1 7.1 3.6% 3.4% Absolute Radio 55032 55032 0 0% 2309 2416 107 5% 4% 4% 16739 18365 1626 10% 7.3 7.6 1.7% 1.9% Absolute Radio (London) 12260 12260 0 0% 715 743 28 4% 6% 6% 5344 5586 242 5% 7.5 7.5 2.7% 2.8% Absolute Radio 60s 55032 55032 0 0% 136 119 -17 -13% *% *% 359 345 -14 -4% 2.6 2.9 *% *% Absolute Radio 70s 55032 55032 0 0% 212 230 18 8% *% *% 804 867 63 8% 3.8 3.8 0.1% 0.1% Absolute 80s 55032 55032 0 0% 1420 1459 39 3% 3% 3% 7020 7088 68 1% 4.9 4.9 0.7% 0.7% Absolute Radio 90s 55032 55032 0 0% 851 837 -14 -2% 2% 2% 3518 3593 75 2% 4.1 4.3 0.4% 0.4% Absolute Radio 00s 55032 55032 0 0% 217 186 -31 -14% *% *% 584 540 -44 -8% 2.7 2.9 0.1% 0.1% Absolute Radio Classic Rock 55032 55032 0 0% 740 813 73 10% 1% 1% 4028 4209 181 4% 5.4 5.2 0.4% 0.4% Hits Radio Brand 55032 55032 0 0% 6657 6619 -38 -1% 12% 12% 52607 52863 256 0% 7.9 8.0 5.4% 5.4% Greatest Hits Network 55032 55032 0 0% 1264 1295 31 2% 2% 2% 9347 10538 1191 13% 7.4 8.1 1.0% 1.1% Greatest Hits Radio 55032 55032 0 0% 845 892 47 6% 2% 2% 6449 7146 697 11% 7.6 8.0 0.7%