Market Update – April 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Media Nations 2019

Media nations: UK 2019 Published 7 August 2019 Overview This is Ofcom’s second annual Media Nations report. It reviews key trends in the television and online video sectors as well as the radio and other audio sectors. Accompanying this narrative report is an interactive report which includes an extensive range of data. There are also separate reports for Northern Ireland, Scotland and Wales. The Media Nations report is a reference publication for industry, policy makers, academics and consumers. This year’s publication is particularly important as it provides evidence to inform discussions around the future of public service broadcasting, supporting the nationwide forum which Ofcom launched in July 2019: Small Screen: Big Debate. We publish this report to support our regulatory goal to research markets and to remain at the forefront of technological understanding. It addresses the requirement to undertake and make public our consumer research (as set out in Sections 14 and 15 of the Communications Act 2003). It also meets the requirements on Ofcom under Section 358 of the Communications Act 2003 to publish an annual factual and statistical report on the TV and radio sector. This year we have structured the findings into four chapters. • The total video chapter looks at trends across all types of video including traditional broadcast TV, video-on-demand services and online video. • In the second chapter, we take a deeper look at public service broadcasting and some wider aspects of broadcast TV. • The third chapter is about online video. This is where we examine in greater depth subscription video on demand and YouTube. -

Hallett Arendt Rajar Topline Results - Wave 3 2019/Last Published Data

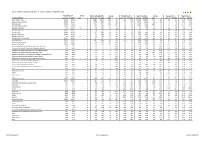

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 3 2019/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share STATION/GROUP Last Pub W3 2019 000's % Last Pub W3 2019 000's % Last Pub W3 2019 Last Pub W3 2019 000's % Last Pub W3 2019 Last Pub W3 2019 Bauer Radio - Total 55032 55032 0 0% 18083 18371 288 2% 33% 33% 156216 158995 2779 2% 8.6 8.7 15.3% 15.9% Absolute Radio Network 55032 55032 0 0% 4743 4921 178 4% 9% 9% 35474 35522 48 0% 7.5 7.2 3.5% 3.6% Absolute Radio 55032 55032 0 0% 2151 2447 296 14% 4% 4% 16402 17626 1224 7% 7.6 7.2 1.6% 1.8% Absolute Radio (London) 12260 12260 0 0% 729 821 92 13% 6% 7% 4279 4370 91 2% 5.9 5.3 2.1% 2.2% Absolute Radio 60s n/p 55032 n/a n/a n/p 125 n/a n/a n/p *% n/p 298 n/a n/a n/p 2.4 n/p *% Absolute Radio 70s 55032 55032 0 0% 206 208 2 1% *% *% 699 712 13 2% 3.4 3.4 0.1% 0.1% Absolute 80s 55032 55032 0 0% 1779 1824 45 3% 3% 3% 9294 9435 141 2% 5.2 5.2 0.9% 1.0% Absolute Radio 90s 55032 55032 0 0% 907 856 -51 -6% 2% 2% 4008 3661 -347 -9% 4.4 4.3 0.4% 0.4% Absolute Radio 00s n/p 55032 n/a n/a n/p 209 n/a n/a n/p *% n/p 540 n/a n/a n/p 2.6 n/p 0.1% Absolute Radio Classic Rock 55032 55032 0 0% 741 721 -20 -3% 1% 1% 3438 3703 265 8% 4.6 5.1 0.3% 0.4% Hits Radio Brand 55032 55032 0 0% 6491 6684 193 3% 12% 12% 53184 54489 1305 2% 8.2 8.2 5.2% 5.5% Greatest Hits Network 55032 55032 0 0% 1103 1209 106 10% 2% 2% 8070 8435 365 5% 7.3 7.0 0.8% 0.8% Greatest Hits Radio 55032 55032 0 0% 715 818 103 14% 1% 1% 5281 5870 589 11% 7.4 7.2 0.5% -

Hallett Arendt Rajar Topline Results - Wave 1 2020/Last Published Data

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 1 2020/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share STATION/GROUP Last Pub W1 2020 000's % Last Pub W1 2020 000's % Last Pub W1 2020 Last Pub W1 2020 000's % Last Pub W1 2020 Last Pub W1 2020 Bauer Radio - Total 55032 55032 0 0% 18160 17986 -174 -1% 33% 33% 155537 154249 -1288 -1% 8.6 8.6 15.9% 15.7% Absolute Radio Network 55032 55032 0 0% 4908 4716 -192 -4% 9% 9% 34837 33647 -1190 -3% 7.1 7.1 3.6% 3.4% Absolute Radio 55032 55032 0 0% 2309 2416 107 5% 4% 4% 16739 18365 1626 10% 7.3 7.6 1.7% 1.9% Absolute Radio (London) 12260 12260 0 0% 715 743 28 4% 6% 6% 5344 5586 242 5% 7.5 7.5 2.7% 2.8% Absolute Radio 60s 55032 55032 0 0% 136 119 -17 -13% *% *% 359 345 -14 -4% 2.6 2.9 *% *% Absolute Radio 70s 55032 55032 0 0% 212 230 18 8% *% *% 804 867 63 8% 3.8 3.8 0.1% 0.1% Absolute 80s 55032 55032 0 0% 1420 1459 39 3% 3% 3% 7020 7088 68 1% 4.9 4.9 0.7% 0.7% Absolute Radio 90s 55032 55032 0 0% 851 837 -14 -2% 2% 2% 3518 3593 75 2% 4.1 4.3 0.4% 0.4% Absolute Radio 00s 55032 55032 0 0% 217 186 -31 -14% *% *% 584 540 -44 -8% 2.7 2.9 0.1% 0.1% Absolute Radio Classic Rock 55032 55032 0 0% 740 813 73 10% 1% 1% 4028 4209 181 4% 5.4 5.2 0.4% 0.4% Hits Radio Brand 55032 55032 0 0% 6657 6619 -38 -1% 12% 12% 52607 52863 256 0% 7.9 8.0 5.4% 5.4% Greatest Hits Network 55032 55032 0 0% 1264 1295 31 2% 2% 2% 9347 10538 1191 13% 7.4 8.1 1.0% 1.1% Greatest Hits Radio 55032 55032 0 0% 845 892 47 6% 2% 2% 6449 7146 697 11% 7.6 8.0 0.7% -

Baird Marketing Tech & Services Industry Report 2020

BAIRD’S MARKETING TECH & SERVICES SECTOR OVERVIEW TABLE OF CONTENTS Industry Overview 1 Industry Trends & Update 2 Market Landscape 3 A. Advertising B. Digital Experience C. Customer Journey Management D. Social & Relationships E. Customer Experience F. Data & Insights Appendix 4 A. Baird Overview B. Valuation Perspectives Page 1 INTRODUCTION TO MARKETING TECHNOLOGY & SERVICES We are excited to share with you our first edition of Baird’s Marketing Technology & Services industry report, which details our views on the industry, including segmentation, sizing, key market players and trends impacting various segments. Marketing means different things to different people. For us, we generally view marketing as the business process of identifying, anticipating and satisfying customers needs and wants. Marketing spans many customer or business-facing activities, which cross other functions that we did not cover in this report. Here, we addressed marketing technology and services that are utilized to identify, attract, engage, convert and retain customers. We have segmented the market into six core segments, including advertising, digital experience, customer journey management, social and relationships, customer experience, and data and insights. We further segmented the industry into 31 sub-segments, all of which we cover in detail herein. Marketing is mission critical and one of the cornerstones of business management and commerce. Every company, whether B2C or B2B, must appropriately engage customers to grow. As a result, companies spend billions of dollars annually on third party technology and outsourced services to define and execute their marketing strategies which has created an ecosystem of thousands of companies to address a broad range of needs. -

Authorized Catalogs - United States

Authorized Catalogs - United States Miché-Whiting, Danielle Emma "C" Vic Music @Canvas Music +2DB 1 Of 4 Prod. 10 Free Trees Music 10 Free Trees Music (Admin. by Word Music Group, 1000 lbs of People Publishing 1000 Pushups, LLC Inc obo WB Music Corp) 10000 Fathers 10000 Fathers 10000 Fathers SESAC Designee 10000 MINUTES 1012 Rosedale Music 10KF Publishing 11! Music 12 Gate Recordings LLC 121 Music 121 Music 12Stone Worship 1600 Publishing 17th Avenue Music 19 Entertainment 19 Tunes 1978 Music 1978 Music 1DA Music 2 Acre Lot 2 Dada Music 2 Hour Songs 2 Letit Music 2 Right Feet 2035 Music 21 Cent Hymns 21 DAYS 21 Songs 216 Music 220 Digital Music 2218 Music 24 Fret 243 Music 247 Worship Music 24DLB Publishing 27:4 Worship Publishing 288 Music 29:11 Church Productions 29:Eleven Music 2GZ Publishing 2Klean Music 2nd Law Music 2nd Law Music 2PM Music 2Surrender 2Surrender 2Ten 3 Leaves 3 Little Bugs 360 Music Works 365 Worship Resources 3JCord Music 3RD WAVE MUSIC 4 Heartstrings Music 40 Psalms Music 442 Music 4468 Productions 45 Degrees Music 4552 Entertainment Street 48 Flex 4th Son Music 4th teepee on the right music 5 Acre Publishing 50 Miles 50 States Music 586Beats 59 Cadillac Music 603 Publishing 66 Ford Songs 68 Guns 68 Guns 6th Generation Music 716 Music Publishing 7189 Music Publishing 7Core Publishing 7FT Songs 814 Stops Today 814 Stops Today 814 Today Publishing 815 Stops Today 816 Stops Today 817 Stops Today 818 Stops Today 819 Stops Today 833 Songs 84Media 88 Key Flow Music 9t One Songs A & C Black (Publishers) Ltd A Beautiful Liturgy Music A Few Good Tunes A J Not Y Publishing A Little Good News Music A Little More Good News Music A Mighty Poythress A New Song For A New Day Music A New Test Catalog A Pirates Life For Me Music A Popular Muse A Sofa And A Chair Music A Thousand Hills Music, LLC A&A Production Studios A. -

Media Perspektiven Basisdaten

ISSN 0942-072X Media Perspektiven Basisdaten Daten zur Mediensituation in Deutschland 2020 Rundfunk: Programmangebot und Empfangssituation Öffentlich-rechtlicher Rundfunk: Erträge/Leistungen Privater Rundfunk: Erträge/Leistungen Programmprofile im dualen Rundfunksystem Medienkonzerne: Beteiligungen Presse, Buch Kino/Film und Video/DVD Theater Unterhaltungselektronik, Musikmedien Mediennutzung Werbung Allgemeine Daten Media Perspektiven Basisdaten 2020 Media Perspektiven Basisdaten Daten zur Mediensituation in Deutschland 2020 In dieser jährlich aktualisierten Publikation werden Basisdaten zum gesamten Mediensektor zusammengestellt. Berücksichtigt werden Hörfunk und Fernsehen, Presse, der Buchmarkt, Kino/Film, Video/DVD, Theater, Unterhaltungselektronik/Musikmedien sowie Werbung. Weitere Schwerpunkte sind die Beteiligungen und Verflechtungen der großen Medienkonzerne sowie die Nutzung der tagesaktuellen Medien Fernsehen, Radio, Presse und Internet. In der Sammlung werden nur kontinuierlich erhobene Datenquellen berücksichtigt, um Entwicklungen im Zeitverlauf dokumentieren zu können. Frankfurt am Main, Februar 2021 Datenrecherche: Michael Braband Redaktion: Hanna Puffer Verzeichnis der Tabellen und Grafiken Media Perspektiven Basisdaten 2020 1 Seite Rundfunk: Programmangebot und Empfangssituation TV-Haushalte nach Empfangsebenen in Deutschland 2020 4 Empfangspotenzial der deutschen Fernsehsender 2020 4 Öffentlich-rechtlicher Rundfunk: Erträge/Leistungen Rundfunkgebühren/Rundfunkbeitrag 6 Erträge aus der Rundfunkgebühr bzw. dem Rundfunkbeitrag -

Media Sector Review

MEDIA SECTOR REVIEW INTERNET AND DIGITAL MEDIA COMMENTARY Ad Tech – Back in the Saddle and Riding High Last quarter we noted that advertising technology (Ad Tech) stocks were the strongest performing sector over the previous 12-month period. The average stock in the Ad Tech sector at the end of INSIDE THIS ISSUE the first quarter of 2021 was up 339% over the prior year. Part of this reflected the starting point: Internet and Digital Media Commentary 1 at the end of March 2020, concerns about Covid-19 and its impact on advertising had caused the Digital Media 5 average stock in the sector to decline by 27%. The other part of the story is how well Ad Tech Advertising Tech. 6 stocks recovered from the initial advertising downturn: while 2Q 2020 revenues declined, they Marketing Tech. 7 rebounded strongly in 3Q and 4Q of 2020, and that strength has continued into the first half of Social Media 8 Esports/iGaming 9 2021. Internet & Digital Media M&A Activity 10 The strong recovery in operating results combined with the strong stock price recovery has led to Traditional Media Commentary 13 TV 16 a rebound in the Ad Tech IPO market. The first half of 2021 saw Pubmatic (PUBM), Viant (DSP), Radio 17 AppLovin (APP), DoubleVerify (DV) and Integral Ad Science (IAS) go public, while Outbrain and Traditional Media M&A Activity 18 Teads filed to go public. Meanwhile, IronSource, Taboola and Innovid all agreed to go public via a Noble Overview 19 reverse merger with a SPAC (Special Purpose Acquisition Company). -

Bauer Digital Radio Limited

BAUER DIGITAL RADIO LIMITED An application to Ofcom for a local DAB digital radio multiplex licence to serve North & West Cumbria Part A – Public Section September 2019 Executive summary Please provide a summary of your application, of no more than four pages in length. 1. Bauer Digital Radio, a subsidiary of Bauer Radio, is pleased to submit an application for a local DAB digital radio multiplex to serve North & West Cumbria (‘BDR Cumbria’), bringing a combination of established and respected local and branded radio services. 2. When designing its coverage plans, BDR was cognisant of the coverage of the national multiplexes and existing neighbouring local multiplexes, and Ofcom's plans for small scale multiplexes in the area. Whilst Digital One covers parts of North & West Cumbria, Sound Digital does not and there are no plans to expand coverage to the area. In addition, Ofcom has identified two small scale polygons in North & West Cumbria which will provide opportunities for community and localised commercial services. As such, BDR has focused on delivering a North & West Cumbria multiplex that will enable existing analogue services in the area to broadcast on DAB and for a range of branded services to broaden choice, catering for a wide range of tastes and interests. 3. BDR Cumbria’s proposal is to launch with 13 services: 4. Capacity has been allocated to accommodate existing local analogue services from launch - BBC Radio Cumbria and CFM. These services collectively account for 26.3% of total radio listening in the CFM TSA. 190908 Public Part A - Bauer Digital Radio - Cumbria Application.docx Page 2 5. -

DOCUMENT RESUME AC 006 374 Facts and Figureson West Virginia

DOCUMENT RESUME ED 036 687 AC 006 374 TITLE Facts and Figureson West Virginia Audiences and Their Special Needs. INSTITUTION West Virginia Univ., Morgantown. W. Va. Center for Appalachian Studies andDevelopment. PUB DATE 69 NOTE 35p0 ;Selected proceedings ofa Critical Issues seminar, Charleston, W.Va., May 28, 1969 EDRS PRICE EDRS Price MF-$0.25 HC-$1485 DESCRIPTORS *Audiences, Broadcast Industry,*Depressed Areas (Geographic), Economic Development,*Educational Needs, *Mass Media, Radio,*Rural Areas, Social Change, Statistical Data,Television Viewing IDENTIFIERS *Appalachia ABSTRACT Drawn from a one-day seminarsponsored by the West Virginia University AppalachianCenter and the West Virginia Broadcasters Association, theseselected proceedings deal withsocial change in rural Appalachia,mass communication linkages with urban America, results ofa. projection of the West Virginiaeconomy up to 1975, findings ofa pilot study on mass mediause in West Virginia, some issues and objectives in educationalbroadcasting, anda brief assessment of public affairs andother telecasting in thestate. The document includes four chartsand tables, the agenda, andsummary population statisticson West Virginia. (1y) U SDEPARTMENT OF HEALTH, EDUCATION 8 WELFARE OFFICE OF EDUCATION CC) '40 THIS DOCUMENT HAS BfEN REPRODUCED EXACTLY AS RECEIVED FROM THE A CR ITICAL ISSUES SEMINAR PERSON OR ORGANIZATION ORIGINATING IT POINTS OF VIEW OR OPINIONS 4, STATED DO NOT NECESSARILY REPRESENT OFFICIAL OFFICE OF EDUCATION partially funded under Title I POSITION OR POLICY Higher EduOation Act of 1965 / Sponsored by:West Virginia University AppalachianCenter West Virginia Broadcasters Association Daniel Boone Hotel Charleston, W. Va. May 28, 1969 THE CHANGING APPALACHIAN POPULATION:some facts West Virginia's population, estimated to be 1,815,000 in 1965, should be almost exactly the same in 1985--1,810,000. -

Independent Radio (Alphabetical Order) Frequency Finder

Independent Radio (Alphabetical order) Frequency Finder Commercial and community radio stations are listed together in alphabetical order. National, local and multi-city stations A ABSOLUTE RADIO CLASSIC ROCK are listed together as there is no longer a clear distinction Format: Classic Rock Hits Broadcaster: Bauer between them. ABBEY 104 London area, Surrey, W Kent, Herts, Luton (Mx 3) DABm 11B For maps and transmitter details see: Mixed Format Community Swansea, Neath Port Talbot and Carmarthenshire DABm 12A • Digital Multiplexes Sherborne, Dorset FM 104.7 Shropshire, Wolverhampton, Black Country b DABm 11B • FM Transmitters by Region Birmingham area, West Midlands, SE Staffs a DABm 11C • AM Transmitters by Region ABC Coventry and Warwickshire DABm 12D FM and AM transmitter details are also included in the Mixed Format Community Stoke-on-Trent, West Staffordshire, South Cheshire DABm 12D frequency-order lists. Portadown, County Down FM 100.2 South Yorkshire, North Notts, Chesterfield DABm 11C Leeds and Wakefield Districts DABm 12D Most stations broadcast 24 hours. Bradford, Calderdale and Kirklees Districts DABm 11B Stations will often put separate adverts, and sometimes news ABSOLUTE RADIO East Yorkshire and North Lincolnshire DABm 10D and information, on different DAB multiplexes or FM/AM Format: Rock Music Tees Valley and County Durham DABm 11B transmitters carrying the same programmes. These are not Broadcaster: Bauer Tyne and Wear, North Durham, Northumberland DABm 11C listed separately. England, Wales and Northern Ireland (D1 Mux) DABm 11D Greater Manchester and North East Cheshire DABm 12C Local stations owned by the same broadcaster often share Scotland (D1 Mux) DABm 12A Central and East Lancashire DABm 12A overnight, evening and weekend, programming. -

MEDIA PACK Brand/ Mission

MEDIA PACK Brand/ Mission Country Hits Radio is the UK’s first country multimedia radio brand for 20-39-year olds. Our presenters are young, fun, bright and full of energy, just like the music we play. Broadcasting on digital radio across the UK playing today’s best country music, we make country accessible to everyone. Country Hits Radio won’t just play the biggest country hits – it will be the only radio brand in the UK to make and break them. Audience/ Listener TGI data tells us that some 8.7m people across the UK listen to country music – it’s probably the largest genre of music not to have its own UK radio station. Music is a passion for this audience with well over 60% saying that they couldn’t get through their day without it. They’re also twice as likely to be regular festival goers compared with the UK norm. Country Hits Radio listeners tune in for the music and the brand’s lifestyle, joining us in celebrating the exhilarating and fun experience of the latest country music hits, with some fun moments where we tip our hat to some of the greatest country hits of all time. Shows/ key opportunities With a playlist spanning Keith Urban, Thomas Rhett, Maren Morris, Florida Georgia Line, Dan + Shay and Carrie Underwood, Country Hits Radio will appeal to modern country music-lovers aged 25-44. Esteemed country music broadcaster Baylen Leonard (BBC Radio 2, BBC Radio 4) was the first voice on the station delivering his weekday show and bringing his passion and knowledge of country music to our listeners. -

Unlock the Future

Ascential plc Annual Report 2018 UNLOCK THE FUTURE ANNUAL REPORT 2018 CONTENTS Strategic report / 04 2018 in summary 06 Company overview 08 Geographic presence 10 Chief Executive’s statement 14 Market review 16 Business model 18 Strategy 20 Segmental reviews 24 Financial review 30 Our alternative performance measures 34 Risk management and viability statement 37 Principal risks 42 Our people 45 Corporate and social responsibility report Governance / 54 Chairman’s introduction to governance 56 Board of Directors 58 A strong governance framework 61 Report of the Audit Committee 66 Report of the Nomination Committee 68 Directors’ Remuneration Report More information online: 76 Directors’ Report Our website gives you fast, 81 Independent Auditor’s Report direct access to a wide range of Company information. Financial statements / ascential.com 90 Consolidated statement of profit or loss 91 Consolidated statement of other comprehensive income Follow us on social media: 92 Consolidated statement of financial position linkedin.com search ‘Ascential’ 93 Consolidated statement of changes in equity 94 Consolidated statement of cash flows twitter.com @Ascential_ 95 Notes to the financial statements 128 Parent Company balance sheet 129 Parent Company statement of changes in equity 130 Notes to the Company financial statements 01 STRATEGIC REPORT 02 03 Ascential plc/Annual Report 2018 Strategic report 2018 IN SUMMARY ASCENTIAL IS A SPECIALIST, GLOBAL INFORMATION COMPANY THAT HELPS THE WORLD’S MOST AMBITIOUS BUSINESSES WIN IN THE DIGITAL ECONOMY. 2018 has been a year of refining the acquisition of WARC, the digital subscription this vision. We came to the conclusion that shape of our business to support our product for marketing effectiveness.