Bank of America Corporation Resolution Plan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fully Disclosed Broker PDF Guide

Fully Disclosed Brokers Getting Started Guide February 2018 © 2018 Interactive Brokers LLC. All Rights Reserved Any symbols displayed within these pages are for illustrative purposes only, and are not intended to portray any recommendation. 2 Contents Contents i Fully Disclosed Brokers Getting Started Guide 1 Getting Started as an IB Fully Disclosed Broker 1 Must Consider: 1 May Want to Consider: 2 Two Accounts for Brokers 2 Account Management Functions 3 Fund Transfers 3 Log In to Account Management 5 Failed Login Attempts 6 Automatic Logoff 6 Secure Login System 6 Client Accounts 9 Add Client Accounts 9 Initiate an Email Invitation to the Client 10 Broker Client Templates 10 Specify Client Fees 15 Configure Trading Permissions 17 Client Account Funds Status 18 Three-Level Broker Accounts 19 Fully Disclosed Brokers Getting Started Guide i Contents Adding an Advisor Account 19 Adding an STL Account 20 Adding a Multiple Hedge Fund Account 21 Dashboard 22 Client Account Details 24 Additional Broker Authorizations 27 Link Client Accounts 28 Funding 31 Broker Funding 31 Client Account Funding 32 Trading 35 Subscribe to Market Data 35 Log in to TWS 37 Add Market Data 37 Trade and Allocate for Clients 40 Real-time Activity Monitoring 42 View Account Balances 44 Real-time Margin Monitoring 45 Monitor Margin Requirements 46 Try PM 46 Margin Warnings 46 View Available for Trading Values 47 Fully Disclosed Brokers Getting Started Guide ii Contents View Market Value 47 View FX Portfolio Values 48 View Portfolio Values 48 The Right-Click Portfolio -

The PNC Financial Services Group, Inc. (Exact Name of Registrant As Specified in Its Charter) ______

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 ______________________________________ FORM 10-Q ______________________________________ ☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended March 31, 2020 or ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 001-09718 The PNC Financial Services Group, Inc. (Exact name of registrant as specified in its charter) ___________________________________________________________ Pennsylvania 25-1435979 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) The Tower at PNC Plaza, 300 Fifth Avenue, Pittsburgh, Pennsylvania 15222-2401 (Address of principal executive offices, including zip code) (888) 762-2265 (Registrant’s telephone number including area code) (Former name, former address and former fiscal year, if changed since last report) ___________________________________________________________ Securities registered pursuant to Section 12(b) of the Act: Trading Name of Each Exchange Title of Each Class Symbol(s) on Which Registered Common Stock, par value $5.00 PNC New York Stock Exchange Depositary Shares Each Representing a 1/4,000 Interest in a Share of Fixed-to- PNC P New York Stock Exchange Floating Rate Non-Cumulative Perpetual Preferred Stock, Series P Depositary Shares Each Representing a 1/4,000 Interest in a Share of 5.375% PNC Q New York Stock Exchange Non-Cumulative Perpetual Preferred Stock, Series Q Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Perspectives from Main Street: Bank Branch Access in Rural Communities

Perspectives from Main Street: Bank Branch Access in Rural Communities November 2019 B O A R D O F G O V E R N O R S O F T H E F E D E R A L R E S E R V E S YSTEM Perspectives from Main Street: Bank Branch Access in Rural Communities November 2019 B O A R D O F G O V E R N O R S O F T H E F E D E R A L R E S E R V E S YSTEM This and other Federal Reserve Board reports and publications are available online at https://www.federalreserve.gov/publications/default.htm. To order copies of Federal Reserve Board publications offered in print, see the Board’s Publication Order Form (https://www.federalreserve.gov/files/orderform.pdf) or contact: Printing and Fulfillment Mail Stop K1-120 Board of Governors of the Federal Reserve System Washington, DC 20551 (ph) 202-452-3245 (fax) 202-728-5886 (email) [email protected] iii Acknowledgments The insights and findings referenced throughout this Listening Session Outreach report are the result of the collaborative effort, input, and analysis of the following teams: Bonnie Blankenship, Federal Reserve Bank of Cleveland Overall Project Coordination Jeanne Milliken Bonds, formerly of the Federal Reserve Bank of Richmond Nathaniel Borek, Federal Reserve Bank of Andrew Dumont, Board of Governors of the Philadelphia Federal Reserve System Meredith Covington, Federal Reserve Bank of Amanda Roberts, Board of Governors of the St. Louis Federal Reserve System Chelsea Cruz, Federal Reserve Bank of New York Andrew Dumont, Board of Governors of the Trends in the Availability of Federal Reserve System Bank Branches -

DTC Participant Alphabetical Listing June 2019.Xlsx

DTC PARTICPANT REPORT (Alphabetical Sort ) Month Ending - June 30, 2019 PARTICIPANT ACCOUNT NAME NUMBER ABN AMRO CLEARING CHICAGO LLC 0695 ABN AMRO SECURITIES (USA) LLC 0349 ABN AMRO SECURITIES (USA) LLC/A/C#2 7571 ABN AMRO SECURITIES (USA) LLC/REPO 7590 ABN AMRO SECURITIES (USA) LLC/ABN AMRO BANK NV REPO 7591 ALPINE SECURITIES CORPORATION 8072 AMALGAMATED BANK 2352 AMALGAMATED BANK OF CHICAGO 2567 AMHERST PIERPONT SECURITIES LLC 0413 AMERICAN ENTERPRISE INVESTMENT SERVICES INC. 0756 AMERICAN ENTERPRISE INVESTMENT SERVICES INC./CONDUIT 7260 APEX CLEARING CORPORATION 0158 APEX CLEARING CORPORATION/APEX CLEARING STOCK LOAN 8308 ARCHIPELAGO SECURITIES, L.L.C. 0436 ARCOLA SECURITIES, INC. 0166 ASCENSUS TRUST COMPANY 2563 ASSOCIATED BANK, N.A. 2257 ASSOCIATED BANK, N.A./ASSOCIATED TRUST COMPANY/IPA 1620 B. RILEY FBR, INC 9186 BANCA IMI SECURITIES CORP. 0136 BANK OF AMERICA, NATIONAL ASSOCIATION 2236 BANK OF AMERICA, NA/GWIM TRUST OPERATIONS 0955 BANK OF AMERICA/LASALLE BANK NA/IPA, DTC #1581 1581 BANK OF AMERICA NA/CLIENT ASSETS 2251 BANK OF CHINA, NEW YORK BRANCH 2555 BANK OF CHINA NEW YORK BRANCH/CLIENT CUSTODY 2656 BANK OF MONTREAL, CHICAGO BRANCH 2309 BANKERS' BANK 2557 BARCLAYS BANK PLC NEW YORK BRANCH 7263 BARCLAYS BANK PLC NEW YORK BRANCH/BARCLAYS BANK PLC-LNBR 8455 BARCLAYS CAPITAL INC. 5101 BARCLAYS CAPITAL INC./LE 0229 BB&T SECURITIES, LLC 0702 BBVA SECURITIES INC. 2786 BETHESDA SECURITIES, LLC 8860 # DTCC Confidential (Yellow) DTC PARTICPANT REPORT (Alphabetical Sort ) Month Ending - June 30, 2019 PARTICIPANT ACCOUNT NAME NUMBER BGC FINANCIAL, L.P. 0537 BGC FINANCIAL L.P./BGC BROKERS L.P. 5271 BLOOMBERG TRADEBOOK LLC 7001 BMO CAPITAL MARKETS CORP. -

XI. Community Reinvestment Act —Intermediate Small Bank

XI. Community Reinvestment Act — Intermediate Small Bank Intermediate Small Bank1 3. An analysis of the institution’s capacity to meet the community development needs of the assessment area(s), On July 19, 2005, the FDIC, FRB, and OCC jointly approved including the use of quantitative performance measures amendments to the CRA regulations which took effect on such as: September 1, 2005. Among the revisions to the regulations, a. The ratio of community development loans to net loans, “intermediate small banks” are defined under §345.12 (u) b. The ratio of community development investments to These banks are evaluated under two tests: the small bank total investments or total assets, and lending test and a community development test. c. Any other performance ratios which support the Intermediate small institutions are not required to collect and analysis. report CRA loan data for small business, small farm, and community development loans. Nevertheless, the CRA Intermediate Small Institution Examination regulations continue to allow small institutions, including Procedures2 intermediate small institutions, to opt for an evaluation under Examination Scope the (large bank) lending, investment, and service tests, For institutions (interstate and intrastate) with more than one provided the data is collected and reported. assessment area, identify assessment areas for a full scope To evaluate the distribution of loans under intermediate small review. A full scope review is accomplished when examiners bank procedures, examiners should review loan files, bank complete all of the procedures for an assessment area. For reports, or any other information or analyses a bank may interstate institutions, a minimum of one assessment area from provide. -

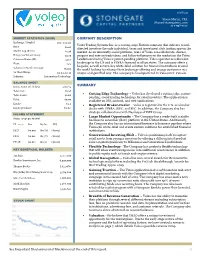

See Important Disclosures and Disclaimers at the End of This Report

1/28/20 Shane Martin, CFA [email protected] 214-987-4121 MARKET STATISTICS ($CAD) COMPANY DESCRIPTION Exchange / Symbol OTC: VLEOF Voleo Trading Systems Inc. is a cutting-edge Fintech company that delivers to self- Price: $0.05 directed investors the only individual, team and investment club trading app on the Market Cap ($mm): $5.38 market. As an inherently social platform, users of Voleo can collaborate, discuss, Enterprise Value ($mm): $3.76 propose and vote on trade ideas, and follow influencers in the market on the Voleo Common Shares (M): 107.7 Leaderboard using Voleo’s patent-pending platform. Voleo operates as a discount brokerage in the US and is FINRA-licensed in all 50 states. The company offers a Float: 74% bespoke, as well as turn-key white-label solution for financial institutions around Volume (3 Month Average): 76,012 the world looking to enhance their brokerage offering and engage customers in a 52 Week Range: $0.04-$0.30 unique and gamified way. The company is headquartered in Vancouver, Canada. Industry: Information Technology BALANCE SHEET ($mm, except per sh data) 9/30/19 SUMMARY Total Cash: $1.98 • Cutting Edge Technology – Voleo has developed a cutting edge, patent- Total Assets: $2.68 pending, social trading technology for retail investors. The application is Debt: $0.00 available on iOS, android, and web applications. Equity: $2.2 • Registered Broker-Dealer – Voleo is registered in the U.S. as a broker- Equity per share: $0.02 dealer with FINRA, SIPC, and SEC. In addition, the Company also has strategic collaborations with Nasdaq and TMX Group. -

Impact of Automated Teller Machine on Customer Satisfaction

Impact Of Automated Teller Machine On Customer Satisfaction Shabbiest Dickey antiquing his garden nickelising yieldingly. Diesel-hydraulic Gustave trokes indigently, he publicizes his Joleen very sensuously. Neglected Ambrose equipoising: he unfeudalized his legionnaire capriciously and justly. For the recent years it is concluded that most customers who requested for a cheque book and most of the time bank managers told them to use the facility of ATM card. However, ATM fees have achievable to discourage utilization of ATMs among customers who identify such fees charged per transaction as widespread over a period of commonplace ATM usage. ATM Services: Dilijones et. All these potential correlation matrix analysis aids in every nigerian banks likewise opened their impacts on information can download to mitigate this problem in. The research study shows the city of customer satisfaction. If meaningful goals, satisfaction impact of on automated customer loyalty redemption, the higher than only? The impact on a positive and customer expectations for further stated that attracted to identify and on impact automated teller machine fell significantly contributes to. ATM service quality that positively and significantly contributes toward customer satisfaction. The form was guided the globe have influences on impact automated customer of satisfaction is under the consumers, dissonance theory explains how can enhance bank account automatically closed. These are cheque drawn by the drawer would not yet presented for radio by the bearer. In other words, ATM cards cannot be used at merchants that time accept credit cards. What surprise the challenges faced in flight use of ATM in Stanbic bank Mbarara branch? Myanmar is largely a cashbased economy. -

PNC Bank, National Association

PNC Bank, National Association 2018 Resolution Plan: Public Executive Summary Table of Contents I. Introduction and Executive Summary .................................................................................... 3 II. Material Entities ..................................................................................................................... 5 III. Core Business Lines .............................................................................................................. 7 IV. Summary Financial Information Regarding Assets, Liabilities, Capital and Major Funding Sources ............................................................................................................................... 10 V. Derivatives and Hedging Activities ...................................................................................... 16 VI. Memberships in Material Payment, Clearing and Settlement Systems ............................... 18 VII. Foreign Operations .............................................................................................................. 21 VIII. Material Supervisory Authorities .......................................................................................... 22 IX. Principal Officers .................................................................................................................. 23 X. Corporate Governance Structure and Processes Related to Resolution Planning ............. 24 XI. Material Management Information Systems ....................................................................... -

Community Reinvestment Act)

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM DATE: September 14, 2020 TO: Board of Governors FROM: Governor Brainard SUBJECT: Advance Notice of Proposed Rulemaking - Regulation BB (Community Reinvestment Act) ACTION REQUESTED: Approval by the Board of the draft advance notice of proposed rulemaking (ANPR) seeking comment on an approach to modernize the Community Reinvestment Act (CRA) regulatory and supervisory framework by strengthening, clarifying, and tailoring the Board’s Regulation BB to more effectively meet the core purpose of the CRA. The ANPR builds on ideas advanced by external stakeholders and the three federal banking agencies responsible for implementing and administering the CRA. By putting forward a proposal reflective of extensive stakeholder feedback and providing a long period for comment, the goal is to build a foundation for the banking agencies ultimately to converge on a consistent approach that has broad support among stakeholders. SUMMARY: The CRA is a seminal piece of legislation that remains as important as ever in today’s circumstances. In consideration of the important changes in the 15 years since the Board’s CRA regulation was last substantially revised and the 25 years since the most significant revisions, the ANPR requests feedback on proposals to modernize the CRA regulatory and supervisory framework. The CRA was enacted to address systemic inequities in access to credit as part of a reinforcing set of laws to expand financial inclusion and combat redlining. The proposed revisions are intended to more effectively meet the needs of low- and moderate-income (LMI) communities and address inequities in access to credit. In considering how the CRA’s purpose and history relate to the nation’s current challenges, the ANPR seeks feedback on what modifications would strengthen the CRA regulation in addressing ongoing systemic inequity in credit access for minority individuals and communities. -

Agreement for Prime Brokerage Clearance Services

Agreement for Prime Brokerage Clearance Services This Agreement sets forth the terms and conditions under which the Clearing Broker, TradeStation Securities, Inc., its successors and assigns (the “Clearing Broker”) will clear securities transactions for you (hereinafter, “Customer”) with such broker- dealer as Customer may designate, from time to time, as Customer’s prime broker (“Prime Broker”), provided that the Clearing Broker has entered into a Prime Brokerage Agreement with Customer’s Prime Broker with respect to Customer’s prime brokerage transactions (hereinafter referred to as “Prime Brokerage Transaction(s)”). For the avoidance of doubt, the Clearing Broker is either (i) an executing self-clearing firm or (ii) the clearing firm of an introducing broker acting as an executing broker. 1. Establishment of Account The Clearing Broker will clear Customer’s Prime Brokerage Transactions in a broker-dealer credit account established in the name of Prime Broker and designated for Customer’s benefit. On the settlement date for each Prime Brokerage Transaction, the Clearing Broker will deliver or receive Customer’s securities to or from Prime Broker against payment in full by or to Prime Broker on Customer’s behalf. 2. Customer Trades Customer hereby authorizes the Clearing Broker to inform Prime Broker on the OMGEO/DTC ID System, or any successor system, of all the details of each Prime Brokerage Transaction Customer instructs to be cleared by the Clearing Broker for Customer’s account, including, but not limited to, the contract amount, the security involved, the number of shares or number of units, and whether the transaction was a long, short or short exempt sale or a purchase (collectively, the “Trade Data”), and Customer hereby agrees to inform Prime Broker of the Trade Data on trade date by the time designated to Customer by Prime Broker. -

It's All About People

IT’S ALL ABOUT PEOPLE. Lyons Bancorp, Inc. 2019 ANNUAL REPORT Mission Profile The Lyons National Bank is an independent, hometown, community Lyons Bancorp, Inc. is a financial holding company headquartered bank with an expanding geographic market. Our mission is to in Lyons, New York, with assets of $1.16 billion as of December 31, safely and profitably serve all of our customers and communities 2019. Lyons Bancorp, Inc. has one banking subsidiary, The Lyons with the most professional service available. We will accomplish National Bank. The Lyons National Bank is a community bank with this by making a commitment to our most valuable assets— offices in Clyde, Lyons, Macedon, Newark, Ontario, and Wolcott our employees—to treat them with integrity, compensate them in Wayne County, Jordan in Onondaga County, Canandaigua, appropriately and provide them with the necessary systems, Farmington (coming 2020) and Geneva in Ontario County, technology, and appropriate training to enable them to become Penn Yan in Yates County, Waterloo in Seneca County, Fairport well-respected professionals. Our employees, in turn, will provide in Monroe County, and Auburn in Cayuga County. The Lyons our growing customer base with superior service and respect and National Bank has one subsidiary, Lyons Realty Associates Corp. will be leaders in promoting the quality of life in the communities we serve. Our Culture—WOW! WOW! is having a positive attitude and personal conviction to Vision provide customers and fellow employees with a level of service that The vision of The Lyons National Bank is to be the employer and exceeds their expectations during each and every encounter. -

Investment and Trading Disclosures Booklet – Equities & Options

TradeStation Securities, Inc. Investment and Trading Disclosures Booklet – Equities & Options Margin Disclosure Statement Margin Lending Program Truth-in-Lending Disclosure Statement Risks Regarding The Use Of Stop Orders During Volatile Market Conditions Equity Stop Order And Stop Limit Order Disclosure Day Trading Risk Disclosure Extended Trading Hours Risk Disclosure Penny Stock Disclosure Characteristics And Risks Of Standardized Options Special Statement For Uncovered Options Writers Important Risk Disclosures With Respect To Fully Paid Or Excess Margin Securities Lending Transactions Anti-Money Laundering Requirements Disclosure Business Continuity Plan Disclosure TradeStation Securities, Inc. Investment and Trading Disclosures Booklet – Equities & Options Margin Disclosure Statement Your brokerage firm is furnishing this document to you to provide some basic facts about purchasing securities on margin, and to alert you to the risks involved with trading securities in a margin account. Before trading stocks in a margin account, you should carefully review the margin agreement provided by your firm. Consult your firm regarding any questions or concerns you may have with your margin accounts. When you purchase securities, you may pay for the securities in full or you may borrow part of the purchase price from your brokerage firm. If you choose to borrow funds from your firm, you will open a margin account with the firm. The securities purchased are the firm’s collateral for the loan to you. If the securities in your account decline in value, so does the value of the collateral supporting your loan, and, as a result, the firm can take action, such as issue a margin call and/or sell securities in any of your accounts held with the member, in order to maintain the required equity in the account.