PNC Bank, National Association

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fully Disclosed Broker PDF Guide

Fully Disclosed Brokers Getting Started Guide February 2018 © 2018 Interactive Brokers LLC. All Rights Reserved Any symbols displayed within these pages are for illustrative purposes only, and are not intended to portray any recommendation. 2 Contents Contents i Fully Disclosed Brokers Getting Started Guide 1 Getting Started as an IB Fully Disclosed Broker 1 Must Consider: 1 May Want to Consider: 2 Two Accounts for Brokers 2 Account Management Functions 3 Fund Transfers 3 Log In to Account Management 5 Failed Login Attempts 6 Automatic Logoff 6 Secure Login System 6 Client Accounts 9 Add Client Accounts 9 Initiate an Email Invitation to the Client 10 Broker Client Templates 10 Specify Client Fees 15 Configure Trading Permissions 17 Client Account Funds Status 18 Three-Level Broker Accounts 19 Fully Disclosed Brokers Getting Started Guide i Contents Adding an Advisor Account 19 Adding an STL Account 20 Adding a Multiple Hedge Fund Account 21 Dashboard 22 Client Account Details 24 Additional Broker Authorizations 27 Link Client Accounts 28 Funding 31 Broker Funding 31 Client Account Funding 32 Trading 35 Subscribe to Market Data 35 Log in to TWS 37 Add Market Data 37 Trade and Allocate for Clients 40 Real-time Activity Monitoring 42 View Account Balances 44 Real-time Margin Monitoring 45 Monitor Margin Requirements 46 Try PM 46 Margin Warnings 46 View Available for Trading Values 47 Fully Disclosed Brokers Getting Started Guide ii Contents View Market Value 47 View FX Portfolio Values 48 View Portfolio Values 48 The Right-Click Portfolio -

The Pnc Financial Services Group Announces First Quarter 2019 Earnings Conference Call Details

CONTACTS: MEDIA: INVESTORS: Media Relations Bryan Gill (412) 762-4550 (412) 768-4143 [email protected] [email protected] THE PNC FINANCIAL SERVICES GROUP ANNOUNCES FIRST QUARTER 2019 EARNINGS CONFERENCE CALL DETAILS Annual Shareholders Meeting To Be Held April 23 PITTSBURGH, March 5, 2019 – The PNC Financial Services Group, Inc. (NYSE: PNC) expects to issue financial results for the first quarter of 2019 Friday, April 12, as previously announced, at approximately 6:45 a.m. (ET). PNC Chairman, President and Chief Executive Officer William S. Demchak and Chief Financial Officer Robert Q. Reilly will hold a conference call for investors the same day at 9:30 a.m. (ET). Separately, PNC will hold its Annual Meeting of Shareholders Tuesday, April 23, 2019. Event details are as follows: First Quarter 2019 Earnings Investor Conference Call: Friday, April 12, at 9:30 a.m. (ET) • Dial-in numbers: (877) 272-3498 and (303) 223-4362 (international). • Accessible at www.pnc.com/investorevents will be a link to the live audio webcast, presentation slides, earnings release and supplementary financial information; a webcast replay will be available for 30 days. • Conference call replay will be available for one week at (800) 633-8284 and (402) 977-9140, Conference ID 21916444. 2019 Annual Meeting of Shareholders: Tuesday, April 23, at 11 a.m. (ET) • Meeting location: The PNC Financial Services Group, Inc., The Tower at PNC Plaza – James E. Rohr Auditorium, 300 Fifth Avenue, Pittsburgh, Pennsylvania 15222. • Dial-in numbers: (877) 402-9134 and (303) 223-4385 (international). • Live audio webcast accessible at www.pnc.com/investorevents or www.pnc.com/annualmeeting; webcast replay available for 30 days. -

In the United States District Court for the Eastern District of Texas Marshall Division

Case 2:08-cv-00462-DF -CE Document 1 Filed 12/04/08 Page 1 of 13 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF TEXAS MARSHALL DIVISION LEON STAMBLER, § § Plaintiff, § § v. § CIVIL ACTION NO. 2:08cv462 § MERRILL LYNCH & CO., INC; § JURY TRIAL DEMANDED MERRILL LYNCH, PIERCE, FENNER & § SMITH INCORPORATED; THE CHARLES § SCHWAB CORPORATION; CHARLES § SCHWAB & CO, INC.; CHARLES § SCHWAB BANK; E*TRADE FINANCIAL § CORPORATION; E*TRADE BANK; § FIDELITY BROKERAGE SERVICES, LLC; § NATIONAL FINANCIAL SERVICES, LLC; § FMR LLC; MORGAN STANLEY; § MORGAN STANLEY & CO. § INCORPORATED; JACK HENRY & § ASSOCIATES, INC.; METAVANTE § TECHNOLOGIES, INC.; METAVANTE § CORPORATION; PAYPAL, INC.; § AMERICAN EXPRESS COMPANY; § AMERICAN BANK OF COMMERCE; § BB&T CORPORATION; BRANCH § BANKING AND TRUST COMPANY; THE § COLONIAL BANCGROUP, INC.; § COLONIAL BANK; FIRST NATIONAL § BANK GROUP, INC.; FIRST NATIONAL § BANK; HSBC NORTH AMERICA § HOLDINGS INC.; HSBC USA INC.; HSBC § BANK USA, NATIONAL ASSOCIATION; § HSBC NATIONAL BANK USA; § LEGACYTEXAS GROUP, INC.; § LEGACYTEXAS BANK; THE PNC § FINANCIAL SERVICES GROUP, INC.; § PNC BANK, NATIONAL ASSOCIATION; § PNC BANK, DELAWARE; PROSPERITY § BANCSHARES, INC.; PROSPERITY § BANK; STERLING BANCSHARES, INC.; § STERLING BANK; SUNTRUST BANKS, § INC.; SUNTRUST BANK; TEXAS § CAPITAL BANCSHARES, INC.; TEXAS § CAPITAL BANK, NATIONAL § 1 Case 2:08-cv-00462-DF -CE Document 1 Filed 12/04/08 Page 2 of 13 ASSOCIATION; U.S. BANCORP; U.S. § BANK NATIONAL ASSOCIATION; § ZIONS BANCORPORATION; ZIONS § FIRST NATIONAL BANK; and AMEGY § BANK NATIONAL ASSOCIATION § § Defendants. § § PLAINTIFF’S ORIGINAL COMPLAINT Plaintiff LEON STAMBLER files this Original Complaint against the above-named Defendants, alleging as follows: I. THE PARTIES 1. Plaintiff LEON STAMBLER (“Stambler”) is an individual residing in Parkland, Florida. 2. Defendant MERRILL LYNCH & CO., INC. -

Financial Institutions Portfolio, Series 46 Fact Card

VAN KAMPEN UNIT TRUSTS Financial Institutions Portfolio, Series 46 A sector unit trust Portfolio composition As of day of deposit Objective Asset management & custody banks Real estate services This portfolio seeks capital appreciation. The Bank of New York Mellon Corporation BK CB Richard Ellis Group, Inc. - CL A CBG portfolio seeks to achieve its objective by investing Franklin Resources, Inc. BEN Regional banks in a portfolio of stocks issued by companies Northern Trust Corporation NTRS BancorpSouth, Inc. BXS diversified within the financial services industry. Consumer finance East West Bancorp, Inc. EWBC The portfolio also seeks current dividend income American Express Company AXP Fifth Third Bancorp FITB as a secondary objective. Capital One Financial Corporation COF Huntington Bancshares, Inc. HBAN Diversified banks PNC Financial Services Group, Inc. PNC Trust specifics Comerica, Inc. CMA SunTrust Banks, Inc. STI Deposit information Wells Fargo & Company WFC SVB Financial Group SIVB Public offering price per unit1 $10.00 Investment banking & brokerage Zions Bancorporation ZION Minimum investment ($250 for IRAs) $1,000.00 Residential REITs Charles Schwab Corporation SCHW Deposit date 05/11/10 Raymond James Financial, Inc. RJF Apartment Investment & Management Termination date 05/08/12 Life & health insurance Company - CL A AIV Distribution date 09/25/10, 12/25/10, 03/25/11, AvalonBay Communities, Inc. AVB Aflac, Inc. AFL 06/25/11, 09/25/11, 12/25/11, Equity Residential EQR Lincoln National Corporation LNC 03/25/12 and final Retail REITs MetLife, Inc. MET Record date 09/10/10, 12/10/10, 03/10/11, Prudential Financial, Inc. PRU Simon Property Group, Inc. -

The PNC Financial Services Group, Inc. (Exact Name of Registrant As Specified in Its Charter) ______

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 ______________________________________ FORM 10-Q ______________________________________ ☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended March 31, 2020 or ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 001-09718 The PNC Financial Services Group, Inc. (Exact name of registrant as specified in its charter) ___________________________________________________________ Pennsylvania 25-1435979 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) The Tower at PNC Plaza, 300 Fifth Avenue, Pittsburgh, Pennsylvania 15222-2401 (Address of principal executive offices, including zip code) (888) 762-2265 (Registrant’s telephone number including area code) (Former name, former address and former fiscal year, if changed since last report) ___________________________________________________________ Securities registered pursuant to Section 12(b) of the Act: Trading Name of Each Exchange Title of Each Class Symbol(s) on Which Registered Common Stock, par value $5.00 PNC New York Stock Exchange Depositary Shares Each Representing a 1/4,000 Interest in a Share of Fixed-to- PNC P New York Stock Exchange Floating Rate Non-Cumulative Perpetual Preferred Stock, Series P Depositary Shares Each Representing a 1/4,000 Interest in a Share of 5.375% PNC Q New York Stock Exchange Non-Cumulative Perpetual Preferred Stock, Series Q Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

The Following Revised Public Summary of the PNC Financial Services Group, Inc.’S (PNC) 165(D) and IDI Resolution Plans Has Been Posted at PNC’S Request

The following revised public summary of The PNC Financial Services Group, Inc.’s (PNC) 165(d) and IDI Resolution Plans has been posted at PNC’s request. This version is substantively identical to the version that the Federal Reserve and Federal Deposit Insurance Corporation posted on their respective websites on January 10, 2013. However, this revised version addresses certain formatting and other cosmetic issues with the prior version. The PNC Financial Services Group, Inc. PNC Bank, National Association Resolution Plan: Public Executive Summary Table of Contents I. Introduction and Executive Summary .............................................................................................. 3 II. Material Entities .................................................................................................................................. 5 III. Core Business Lines .......................................................................................................................... 7 IV. Summary Financial Information Regarding Assets, Liabilities, Capital and Major Funding Sources .............................................................................................................................................. 10 V. Derivatives and Hedging Activities.................................................................................................. 16 VI. Memberships in Material Payment, Clearing and Settlement Systems.................................... 18 VII. Foreign Operations .......................................................................................................................... -

Case Study Project ����� PNC Financial Services Group Location ���� Pittsburgh, PA Product ����� DC Flexzone™ Grid

case study Project ..... PNC Financial Services Group Location .... Pittsburgh, PA Product ..... DC FlexZone™ Grid the challenge: In 2002, PNC Financial Services Group became the first major U.S. bank to apply green building practices to all its newly constructed branches. The result: PNC now has more LEED®- certified buildings than any other company in the world. “Any time we construct a building, we want to include state-of-the- art technology,” explains Mike Gilmore, PNC Director of Design and Construction Services. “And, not just technology for now, but for years down the road.” the solution: Gilmore sees the increased use of direct current (DC) in commercial buildings as one of those technologies. “As DC becomes more prevalent, it only makes sense to go in that direction,” he states. As evidence of that belief, PNC was the first company in the country to install DC FlexZone grid, a ceiling suspension system from Armstrong that can distribute safe, low voltage DC power to electrical devices in a space. Installed at PNC Realty Services Group’s offices, the grid powered lay-in light fixtures, pendants, and wall washers in both open plan and closed spaces. “As a leader in sustainability, we’re interested in anything that saves energy,” Gilmore says. “The grid goes an extra step because it deals with direct current, which saves the energy needed to convert AC to DC.” In addition to its energy-saving potential, the grid also improves the flexibility of interior spaces by providing ‘plug and play’ capabilities for moving light fixtures without the need to re-wire. -

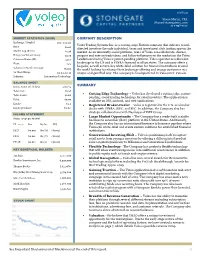

See Important Disclosures and Disclaimers at the End of This Report

1/28/20 Shane Martin, CFA [email protected] 214-987-4121 MARKET STATISTICS ($CAD) COMPANY DESCRIPTION Exchange / Symbol OTC: VLEOF Voleo Trading Systems Inc. is a cutting-edge Fintech company that delivers to self- Price: $0.05 directed investors the only individual, team and investment club trading app on the Market Cap ($mm): $5.38 market. As an inherently social platform, users of Voleo can collaborate, discuss, Enterprise Value ($mm): $3.76 propose and vote on trade ideas, and follow influencers in the market on the Voleo Common Shares (M): 107.7 Leaderboard using Voleo’s patent-pending platform. Voleo operates as a discount brokerage in the US and is FINRA-licensed in all 50 states. The company offers a Float: 74% bespoke, as well as turn-key white-label solution for financial institutions around Volume (3 Month Average): 76,012 the world looking to enhance their brokerage offering and engage customers in a 52 Week Range: $0.04-$0.30 unique and gamified way. The company is headquartered in Vancouver, Canada. Industry: Information Technology BALANCE SHEET ($mm, except per sh data) 9/30/19 SUMMARY Total Cash: $1.98 • Cutting Edge Technology – Voleo has developed a cutting edge, patent- Total Assets: $2.68 pending, social trading technology for retail investors. The application is Debt: $0.00 available on iOS, android, and web applications. Equity: $2.2 • Registered Broker-Dealer – Voleo is registered in the U.S. as a broker- Equity per share: $0.02 dealer with FINRA, SIPC, and SEC. In addition, the Company also has strategic collaborations with Nasdaq and TMX Group. -

Leadership That Lifts Us All Recognizing Outstanding Philanthropy 2017 - 2018

Leadership That Lifts Us All Recognizing Outstanding Philanthropy 2017 - 2018 uwswpa.org Thank you to our 2017 sponsors: Premier Gold Dear Friends, As philanthropic leaders who, through their generous gifts of time and treasure, demonstrate their commitment to tackling our community’s most pressing problems, we should be proud of the impact we make on the lives of people who need our help. Through our gifts – Tocqueville Society members contributed nearly $10 million to the United Way 2017 Campaign – the most vulnerable members of our community are getting much-needed support: Dan Onorato • local children like Alijah (page 18) are matched with caring mentors who are helping them plan to continue their education after high school; • seniors like Jean (page 4) are receiving support that helps them remain in the homes they love; • people with disabilities like Kenny (page 9) are getting the opportunity to find 1 meaningful work; and • women like Sarah (page 43) are able to overcome challenges in order to gain greater financial stability. On behalf of our community, thank you for your support. Your gift helps United Way put solutions into action, making a difference and encouraging hope for a better David Schlosser tomorrow for everyone. With warmest regards Dan Onorato David Schlosser 2017 Tocqueville Society Co-Chair 2017 Tocqueville Society Co-Chair 2017 Top Tocqueville Corporations The Tocqueville Society Tocqueville Society Membership Growth United Way recognizes these United Way’s Tocqueville Society is corporations that had the largest comprised of philanthropic leaders 2011 430 number of Tocqueville Society and volunteer champions who donors for the 2017 campaign, give $10,000 or more annually to regardless of company size or United Way, creating a profound 2012 458 overall campaign total. -

Agreement for Prime Brokerage Clearance Services

Agreement for Prime Brokerage Clearance Services This Agreement sets forth the terms and conditions under which the Clearing Broker, TradeStation Securities, Inc., its successors and assigns (the “Clearing Broker”) will clear securities transactions for you (hereinafter, “Customer”) with such broker- dealer as Customer may designate, from time to time, as Customer’s prime broker (“Prime Broker”), provided that the Clearing Broker has entered into a Prime Brokerage Agreement with Customer’s Prime Broker with respect to Customer’s prime brokerage transactions (hereinafter referred to as “Prime Brokerage Transaction(s)”). For the avoidance of doubt, the Clearing Broker is either (i) an executing self-clearing firm or (ii) the clearing firm of an introducing broker acting as an executing broker. 1. Establishment of Account The Clearing Broker will clear Customer’s Prime Brokerage Transactions in a broker-dealer credit account established in the name of Prime Broker and designated for Customer’s benefit. On the settlement date for each Prime Brokerage Transaction, the Clearing Broker will deliver or receive Customer’s securities to or from Prime Broker against payment in full by or to Prime Broker on Customer’s behalf. 2. Customer Trades Customer hereby authorizes the Clearing Broker to inform Prime Broker on the OMGEO/DTC ID System, or any successor system, of all the details of each Prime Brokerage Transaction Customer instructs to be cleared by the Clearing Broker for Customer’s account, including, but not limited to, the contract amount, the security involved, the number of shares or number of units, and whether the transaction was a long, short or short exempt sale or a purchase (collectively, the “Trade Data”), and Customer hereby agrees to inform Prime Broker of the Trade Data on trade date by the time designated to Customer by Prime Broker. -

It's All About People

IT’S ALL ABOUT PEOPLE. Lyons Bancorp, Inc. 2019 ANNUAL REPORT Mission Profile The Lyons National Bank is an independent, hometown, community Lyons Bancorp, Inc. is a financial holding company headquartered bank with an expanding geographic market. Our mission is to in Lyons, New York, with assets of $1.16 billion as of December 31, safely and profitably serve all of our customers and communities 2019. Lyons Bancorp, Inc. has one banking subsidiary, The Lyons with the most professional service available. We will accomplish National Bank. The Lyons National Bank is a community bank with this by making a commitment to our most valuable assets— offices in Clyde, Lyons, Macedon, Newark, Ontario, and Wolcott our employees—to treat them with integrity, compensate them in Wayne County, Jordan in Onondaga County, Canandaigua, appropriately and provide them with the necessary systems, Farmington (coming 2020) and Geneva in Ontario County, technology, and appropriate training to enable them to become Penn Yan in Yates County, Waterloo in Seneca County, Fairport well-respected professionals. Our employees, in turn, will provide in Monroe County, and Auburn in Cayuga County. The Lyons our growing customer base with superior service and respect and National Bank has one subsidiary, Lyons Realty Associates Corp. will be leaders in promoting the quality of life in the communities we serve. Our Culture—WOW! WOW! is having a positive attitude and personal conviction to Vision provide customers and fellow employees with a level of service that The vision of The Lyons National Bank is to be the employer and exceeds their expectations during each and every encounter. -

Investment and Trading Disclosures Booklet – Equities & Options

TradeStation Securities, Inc. Investment and Trading Disclosures Booklet – Equities & Options Margin Disclosure Statement Margin Lending Program Truth-in-Lending Disclosure Statement Risks Regarding The Use Of Stop Orders During Volatile Market Conditions Equity Stop Order And Stop Limit Order Disclosure Day Trading Risk Disclosure Extended Trading Hours Risk Disclosure Penny Stock Disclosure Characteristics And Risks Of Standardized Options Special Statement For Uncovered Options Writers Important Risk Disclosures With Respect To Fully Paid Or Excess Margin Securities Lending Transactions Anti-Money Laundering Requirements Disclosure Business Continuity Plan Disclosure TradeStation Securities, Inc. Investment and Trading Disclosures Booklet – Equities & Options Margin Disclosure Statement Your brokerage firm is furnishing this document to you to provide some basic facts about purchasing securities on margin, and to alert you to the risks involved with trading securities in a margin account. Before trading stocks in a margin account, you should carefully review the margin agreement provided by your firm. Consult your firm regarding any questions or concerns you may have with your margin accounts. When you purchase securities, you may pay for the securities in full or you may borrow part of the purchase price from your brokerage firm. If you choose to borrow funds from your firm, you will open a margin account with the firm. The securities purchased are the firm’s collateral for the loan to you. If the securities in your account decline in value, so does the value of the collateral supporting your loan, and, as a result, the firm can take action, such as issue a margin call and/or sell securities in any of your accounts held with the member, in order to maintain the required equity in the account.