(“Wells Fargo”) Commends the Securities and Exchange Commission

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fully Disclosed Broker PDF Guide

Fully Disclosed Brokers Getting Started Guide February 2018 © 2018 Interactive Brokers LLC. All Rights Reserved Any symbols displayed within these pages are for illustrative purposes only, and are not intended to portray any recommendation. 2 Contents Contents i Fully Disclosed Brokers Getting Started Guide 1 Getting Started as an IB Fully Disclosed Broker 1 Must Consider: 1 May Want to Consider: 2 Two Accounts for Brokers 2 Account Management Functions 3 Fund Transfers 3 Log In to Account Management 5 Failed Login Attempts 6 Automatic Logoff 6 Secure Login System 6 Client Accounts 9 Add Client Accounts 9 Initiate an Email Invitation to the Client 10 Broker Client Templates 10 Specify Client Fees 15 Configure Trading Permissions 17 Client Account Funds Status 18 Three-Level Broker Accounts 19 Fully Disclosed Brokers Getting Started Guide i Contents Adding an Advisor Account 19 Adding an STL Account 20 Adding a Multiple Hedge Fund Account 21 Dashboard 22 Client Account Details 24 Additional Broker Authorizations 27 Link Client Accounts 28 Funding 31 Broker Funding 31 Client Account Funding 32 Trading 35 Subscribe to Market Data 35 Log in to TWS 37 Add Market Data 37 Trade and Allocate for Clients 40 Real-time Activity Monitoring 42 View Account Balances 44 Real-time Margin Monitoring 45 Monitor Margin Requirements 46 Try PM 46 Margin Warnings 46 View Available for Trading Values 47 Fully Disclosed Brokers Getting Started Guide ii Contents View Market Value 47 View FX Portfolio Values 48 View Portfolio Values 48 The Right-Click Portfolio -

The PNC Financial Services Group, Inc. (Exact Name of Registrant As Specified in Its Charter) ______

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 ______________________________________ FORM 10-Q ______________________________________ ☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended March 31, 2020 or ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 001-09718 The PNC Financial Services Group, Inc. (Exact name of registrant as specified in its charter) ___________________________________________________________ Pennsylvania 25-1435979 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) The Tower at PNC Plaza, 300 Fifth Avenue, Pittsburgh, Pennsylvania 15222-2401 (Address of principal executive offices, including zip code) (888) 762-2265 (Registrant’s telephone number including area code) (Former name, former address and former fiscal year, if changed since last report) ___________________________________________________________ Securities registered pursuant to Section 12(b) of the Act: Trading Name of Each Exchange Title of Each Class Symbol(s) on Which Registered Common Stock, par value $5.00 PNC New York Stock Exchange Depositary Shares Each Representing a 1/4,000 Interest in a Share of Fixed-to- PNC P New York Stock Exchange Floating Rate Non-Cumulative Perpetual Preferred Stock, Series P Depositary Shares Each Representing a 1/4,000 Interest in a Share of 5.375% PNC Q New York Stock Exchange Non-Cumulative Perpetual Preferred Stock, Series Q Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

See Important Disclosures and Disclaimers at the End of This Report

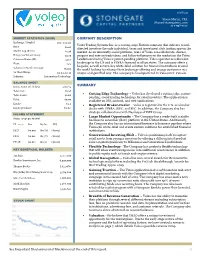

1/28/20 Shane Martin, CFA [email protected] 214-987-4121 MARKET STATISTICS ($CAD) COMPANY DESCRIPTION Exchange / Symbol OTC: VLEOF Voleo Trading Systems Inc. is a cutting-edge Fintech company that delivers to self- Price: $0.05 directed investors the only individual, team and investment club trading app on the Market Cap ($mm): $5.38 market. As an inherently social platform, users of Voleo can collaborate, discuss, Enterprise Value ($mm): $3.76 propose and vote on trade ideas, and follow influencers in the market on the Voleo Common Shares (M): 107.7 Leaderboard using Voleo’s patent-pending platform. Voleo operates as a discount brokerage in the US and is FINRA-licensed in all 50 states. The company offers a Float: 74% bespoke, as well as turn-key white-label solution for financial institutions around Volume (3 Month Average): 76,012 the world looking to enhance their brokerage offering and engage customers in a 52 Week Range: $0.04-$0.30 unique and gamified way. The company is headquartered in Vancouver, Canada. Industry: Information Technology BALANCE SHEET ($mm, except per sh data) 9/30/19 SUMMARY Total Cash: $1.98 • Cutting Edge Technology – Voleo has developed a cutting edge, patent- Total Assets: $2.68 pending, social trading technology for retail investors. The application is Debt: $0.00 available on iOS, android, and web applications. Equity: $2.2 • Registered Broker-Dealer – Voleo is registered in the U.S. as a broker- Equity per share: $0.02 dealer with FINRA, SIPC, and SEC. In addition, the Company also has strategic collaborations with Nasdaq and TMX Group. -

PNC Bank, National Association

PNC Bank, National Association 2018 Resolution Plan: Public Executive Summary Table of Contents I. Introduction and Executive Summary .................................................................................... 3 II. Material Entities ..................................................................................................................... 5 III. Core Business Lines .............................................................................................................. 7 IV. Summary Financial Information Regarding Assets, Liabilities, Capital and Major Funding Sources ............................................................................................................................... 10 V. Derivatives and Hedging Activities ...................................................................................... 16 VI. Memberships in Material Payment, Clearing and Settlement Systems ............................... 18 VII. Foreign Operations .............................................................................................................. 21 VIII. Material Supervisory Authorities .......................................................................................... 22 IX. Principal Officers .................................................................................................................. 23 X. Corporate Governance Structure and Processes Related to Resolution Planning ............. 24 XI. Material Management Information Systems ....................................................................... -

Agreement for Prime Brokerage Clearance Services

Agreement for Prime Brokerage Clearance Services This Agreement sets forth the terms and conditions under which the Clearing Broker, TradeStation Securities, Inc., its successors and assigns (the “Clearing Broker”) will clear securities transactions for you (hereinafter, “Customer”) with such broker- dealer as Customer may designate, from time to time, as Customer’s prime broker (“Prime Broker”), provided that the Clearing Broker has entered into a Prime Brokerage Agreement with Customer’s Prime Broker with respect to Customer’s prime brokerage transactions (hereinafter referred to as “Prime Brokerage Transaction(s)”). For the avoidance of doubt, the Clearing Broker is either (i) an executing self-clearing firm or (ii) the clearing firm of an introducing broker acting as an executing broker. 1. Establishment of Account The Clearing Broker will clear Customer’s Prime Brokerage Transactions in a broker-dealer credit account established in the name of Prime Broker and designated for Customer’s benefit. On the settlement date for each Prime Brokerage Transaction, the Clearing Broker will deliver or receive Customer’s securities to or from Prime Broker against payment in full by or to Prime Broker on Customer’s behalf. 2. Customer Trades Customer hereby authorizes the Clearing Broker to inform Prime Broker on the OMGEO/DTC ID System, or any successor system, of all the details of each Prime Brokerage Transaction Customer instructs to be cleared by the Clearing Broker for Customer’s account, including, but not limited to, the contract amount, the security involved, the number of shares or number of units, and whether the transaction was a long, short or short exempt sale or a purchase (collectively, the “Trade Data”), and Customer hereby agrees to inform Prime Broker of the Trade Data on trade date by the time designated to Customer by Prime Broker. -

It's All About People

IT’S ALL ABOUT PEOPLE. Lyons Bancorp, Inc. 2019 ANNUAL REPORT Mission Profile The Lyons National Bank is an independent, hometown, community Lyons Bancorp, Inc. is a financial holding company headquartered bank with an expanding geographic market. Our mission is to in Lyons, New York, with assets of $1.16 billion as of December 31, safely and profitably serve all of our customers and communities 2019. Lyons Bancorp, Inc. has one banking subsidiary, The Lyons with the most professional service available. We will accomplish National Bank. The Lyons National Bank is a community bank with this by making a commitment to our most valuable assets— offices in Clyde, Lyons, Macedon, Newark, Ontario, and Wolcott our employees—to treat them with integrity, compensate them in Wayne County, Jordan in Onondaga County, Canandaigua, appropriately and provide them with the necessary systems, Farmington (coming 2020) and Geneva in Ontario County, technology, and appropriate training to enable them to become Penn Yan in Yates County, Waterloo in Seneca County, Fairport well-respected professionals. Our employees, in turn, will provide in Monroe County, and Auburn in Cayuga County. The Lyons our growing customer base with superior service and respect and National Bank has one subsidiary, Lyons Realty Associates Corp. will be leaders in promoting the quality of life in the communities we serve. Our Culture—WOW! WOW! is having a positive attitude and personal conviction to Vision provide customers and fellow employees with a level of service that The vision of The Lyons National Bank is to be the employer and exceeds their expectations during each and every encounter. -

Investment and Trading Disclosures Booklet – Equities & Options

TradeStation Securities, Inc. Investment and Trading Disclosures Booklet – Equities & Options Margin Disclosure Statement Margin Lending Program Truth-in-Lending Disclosure Statement Risks Regarding The Use Of Stop Orders During Volatile Market Conditions Equity Stop Order And Stop Limit Order Disclosure Day Trading Risk Disclosure Extended Trading Hours Risk Disclosure Penny Stock Disclosure Characteristics And Risks Of Standardized Options Special Statement For Uncovered Options Writers Important Risk Disclosures With Respect To Fully Paid Or Excess Margin Securities Lending Transactions Anti-Money Laundering Requirements Disclosure Business Continuity Plan Disclosure TradeStation Securities, Inc. Investment and Trading Disclosures Booklet – Equities & Options Margin Disclosure Statement Your brokerage firm is furnishing this document to you to provide some basic facts about purchasing securities on margin, and to alert you to the risks involved with trading securities in a margin account. Before trading stocks in a margin account, you should carefully review the margin agreement provided by your firm. Consult your firm regarding any questions or concerns you may have with your margin accounts. When you purchase securities, you may pay for the securities in full or you may borrow part of the purchase price from your brokerage firm. If you choose to borrow funds from your firm, you will open a margin account with the firm. The securities purchased are the firm’s collateral for the loan to you. If the securities in your account decline in value, so does the value of the collateral supporting your loan, and, as a result, the firm can take action, such as issue a margin call and/or sell securities in any of your accounts held with the member, in order to maintain the required equity in the account. -

Bank of America Corporation Resolution Plan

Bank of America Corporation Resolution Plan Public Executive Summary July 1, 2015 1 Where you can find more information: Bank of America Corporation (the “Company”) files annual, quarterly, and special reports, proxy statements, and other information with the Securities and Exchange Commission (“SEC”), including reports that are filed under Sections 13(a), 13(c), 14, and 15(d) of the Securities Exchange Act of 1934. Any document that is filed with the SEC at the Public Reference Room of the SEC at 100 F Street, N.E., Room 1580, Washington, D.C. 20549 may be read and copied. The filings may be inspected over the Internet at the SEC’s website, www.sec.gov. The reports and other information filed by the Company with the SEC also are available at its website, www.bankofamerica.com. Except as specifically incorporated by reference into this document, information contained in those filings is not part of this document. Certain information in this document has been extracted from the Company’s Annual Report on Form 10-K for the year ended December 31, 2014 (the “2014 Form 10-K”) and the Quarterly Report for the period ended March 31, 2015 (the “First Quarter Form 10-Q”) filed with the SEC. Information contained in reports and other filings the Company makes or has made with the SEC subsequent to the date of the 2014 Form 10-K and First Quarter Form 10-Q may modify or update and supersede the information contained in the 2014 Form 10-K, the First Quarter Form 10-Q and provided in this document. -

Pool Account PDF Guide

February 2018 © 2018 Interactive Brokers LLC. All Rights Reserved Any symbols displayed within these pages are for illustrative purposes only, and are not intended to portray any recommendation. Contents Contents i Proprietary Trading Group Pool Account Getting Started Guide 5 Getting Started as a Proprietary Trading Group Pool Account 5 Must Consider: 5 May Want to Consider: 6 Log In to Account Management 7 Failed Login Attempts 8 Automatic Logoff 8 Secure Login System 8 Funding 11 Master Account Funding 11 Check Account Funds Status 12 Configuration 13 Set Trading Permissions 13 Add Users to the Master Account 14 Modify User Access Rights 17 Delete Users from an Account 19 Trading 21 Subscribe to Market Data 21 Log in to TWS 22 Proprietary Trading Group Pool Account Getting Started Guide i Contents Add Market Data 23 Real-time Activity Monitoring 26 View Account Balances 28 Real-time Margin Monitoring 29 Monitor Margin Requirements 30 Try PM 30 Margin Warnings 31 View Available for Trading Values 31 View Market Value 31 View FX Portfolio Values 32 View Portfolio Values 32 The Right-Click Portfolio Menu 33 Reporting 35 Activity Statements 35 Customized Activity Statements 39 Third-Party Downloads 39 Trade Confirmations 40 Flex Queries 41 Margin Reports 42 Stress Test Report 43 Value at Risk Report 43 PortfolioAnalyst 45 Proprietary Trading Group Pool Account Getting Started Guide ii Contents Other Features 47 Use Post-Trade Allocations 47 Opening a Paper Trading Account 49 Paper Trading Account Reset 50 Paper Trading Account Statements -

Business Brokerage Application

BUSINESS BROKERAGE APPLICATION COMPLETE YOUR E*TRADE APPLICATION IN THREE EASY STEPS The Business Brokerage Application you requested begins on the following page. To complete your application, simply: 1. SCROLL DOWN AND FILL OUT EACH FIELD BY TYPING IN THE APPROPRIATE INFORMATION. If you’d like to complete the application by hand, skip this step and move on to Step 2. 2. ONCE YOU HAVE PROVIDED THE REQUESTED INFORMATION, REVIEW YOUR APPLICATION TO ENSURE IT IS COMPLETE AND PRINT IT BY CLICKING THE BUTTON ON THE TOP TOOLBAR. 3. SIGN AND DATE YOUR APPLICATION, AND MAIL IT TO THE APPROPRIATE ADDRESS: By overnight mail: By regular mail: E*TRADE Securities LLC E*TRADE Securities LLC Harborside Financial Center P.O. Box 484 501 Plaza 2 Jersey City, NJ 07303-0484 34 Exchange Place General Fax Number: 1-866-650-0003 Jersey City, NJ 07311 From Outside the US: +1-678-624-6950 General Fax Number: 1-866-650-0003 From Outside the US: +1-678-624-6950 *Note: Please include a Fax Cover Sheet when submitting documents by facsimile. Notarized, certified or original documents cannot be submitted by facsimile and should be mailed. 1 If your application requires additional documents, please be sure to enclose them with your application. Please refer to the chart below to determine if additional documents are required: Important note: If we are unable to verify your company, we will also need a copy of IRS Letter 147C which validates your company's Tax ID number. You can obtain this letter by contacting the IRS's Business and Specialty Tax Line at 1-800-829-4933. -

Three Easy Ways to Fund Your Tradestation Equities Account

Three Easy Ways to Fund Your TradeStation Equities Account If you have questions about funding or making deposits to your account, call Client Services at 1.800.871.3577 or 954.652.7920. Minimum initial equities account opening requirement is $500 for cash accounts and $2,000 for margin accounts. For more information on funding your account, please visit our website. Equities and Options Accounts 1 Wire Transfer You may transfer money electronically from one of your existing bank or brokerage accounts to Beneficiary/Recipient Name: Beneficiary Bank Name: your TradeStation account. Deposited funds will be TradeStation Securities, Inc. JPMorgan Chase available for trading the next business day if received by 4 p.m. ET. TradeStation does not charge any fees Beneficiary Account # at Bank: for receiving wire transfers, though many banks and 066628636 Beneficiary Bank ABA#: brokerages charge fees for sending them. Wires 021-000-021 received from foreign bank accounts may incur Beneficiary Address: additional intermediary bank charges. 8050 SW 10th Street, Suite 2000 Beneficiary Bank SWIFT Code (A Swift Code is required Plantation, FL 33324 • 954.652.7000 for wire deposits initiated outside the United States). INSTRUCTIONS: Please do not wire funds until CHASUS33 your account is approved and you have confirmed Instructions for Beneficiary (The title of your TradeStation that the account is ready to receive a wire. For Securities account and the title of the account from which you Beneficiary Bank Address: all incoming wires, the sending bank/firm must are transferring funds must match). One Chase Manhattan Plaza 7th floor reference the title of your TradeStation Securities, New York, NY 10005 • 877.204.1123 Further Credit To: <TradeStation Account Title> Inc. -

Notification for Prior Approval to Acquire by Merger E*TRADE

NOTIFICATION to the BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM by MORGAN STANLEY for prior approval to acquire by merger E*TRADE FINANCIAL CORPORATION Pursuant to Sections 4(j) and 4(k) of the Bank Holding Company Act of 1956, as amended, and Regulation Y promulgated thereunder, and Section 163(b) of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 _____________________ March 25, 2020 _____________________ FR Y-4 OMB Number 7100-0121 Approval expires July 31, 2021 Page 1 of 2 Board of Governors of the Federal Reserve System ... o·i ·co~i~:~ ... : i.: Notification by a Bank Holding Company to ~ .. .. .. Acquire a Nonbank Company and/or Engage in Nonbanking Activities—FR Y-4 Morgan Stanley Corporate Title of Notificant 1585 Broadway Street Address New York NY 10036 City State Zip Code Hereby provides the Board with a notice pursuant to: □ (1) Section 4(c)(8) and 4(j) of the Bank Holding Company Act of 1956, as amended (“BHC Act”— 12 U.S.C. § 1843), under the “Expedited action for certain nonbanking proposals by well-run bank holding companies” as described in section 225.23 of Regulation Y; or (2) Section 4(c)(8) and 4(j) of the BHC Act, under the “Procedures for other nonbanking proposals” as described in section 225.24 of Regulation Y; for prior approval to engage directly or indirectly in certain nonbanking activities, de novo, through acquisition of the assets of a going concern, or through direct or indirect ownership, control, or power to vote at least ___________ (100%) of the voting shares of: E*TRADE Financial Corporation Corporate Title of Company to be Acquired and/or Description of Nonbanking Activity (refer to section 225.28 of Regulation Y, as applicable) 671 North Glebe Road Street Address Arlington Virginia 22203 City State Zip Code Does notificant request confidential treatment for any portion of this submission? ~ Yes ~ As required by the General Instructions, a letter justifying the request for confidential treatment is included.