Economic Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Gandhi As Mahatma: Gorakhpur District, Eastern UP, 1921-2'

Gandhi as Mahatma 289 of time to lead or influence a political movement of the peasantry. Gandhi, the person, was in this particular locality for less than a day, but the 'Mahatma' as an 'idea' was thought out and reworked in Gandhi as Mahatma: popular imagination in subsequent months. Even in the eyes of some local Congressmen this 'deification'—'unofficial canonization' as the Gorakhpur District, Eastern UP, Pioneer put it—assumed dangerously distended proportions by April-May 1921. 1921-2' In following the career of the Mahatma in one limited area Over a short period, this essay seeks to place the relationship between Gandhi and the peasants in a perspective somewhat different from SHAHID AMIN the view usually taken of this grand subject. We are not concerned with analysing the attributes of his charisma but with how this 'Many miracles, were previous to this affair [the riot at Chauri registered in peasant consciousness. We are also constrained by our Chaura], sedulously circulated by the designing crowd, and firmly believed by the ignorant crowd, of the Non-co-operation world of primary documentation from looking at the image of Gandhi in this district'. Gorakhpur historically—at the ideas and beliefs about the Mahatma —M. B. Dixit, Committing Magistrate, that percolated into the region before his visit and the transformations, Chauri Chaura Trials. if any, that image underwent as a result of his visit. Most of the rumours about the Mahatma.'spratap (power/glory) were reported in the local press between February and May 1921. And as our sample I of fifty fairly elaborate 'stories' spans this rather brief period, we cannot fully indicate what happens to the 'deified' image after the Gandhi visited the district of Gorakhpur in eastern UP on 8 February rioting at Chauri Chaura in early 1922 and the subsequent withdrawal 1921, addressed a monster meeting variously estimated at between 1 of the Non-Co-operation movement. -

Thirty-Second Annual List of Papers

1923.] LIST OF PUBLISHED PAPERS 485 THIRTY-SECOND ANNUAL LIST OF PAPERS READ BEFORE THE AMERICAN MATHEMATICAL SOCIETY AND SUBSEQUENTLY PUBLISHED, INCLUDING REFERENCES TO THE PLACES OF PUBLICATION ALEXANDER, J. W. A proof and extension of the Jordan-Brouwer separa tion theorem. Read April 29, 1916. Transactions of this Society, vol. 23, No. 4, pp. 333-349; June, 1922. Invariant points of a surface transformation of given class. Read Dec. 28, 1922. Transactions of this Society, vol. 25, No. 2, pp. 173- 184; April, 1923. BARNETT, I. A. Differential equations with a continuous infinitude of variables. Read Dec. 28, 1918. American Journal of Mathematics, vol. 44, No. 3, pp. 172-190; July, 1922. Linear partial differential equations with a continuous infinitude of variables. Read Dec. 28, 1918, and April 24, 1920. American Journal of Mathematics, vol. 45, No. 1, pp. 42-53; Jan., 1923. BELL, E. T. On restricted systems of higher indeterminate equations. Read (San Francisco) June 18, 1920. Transactions of this Society, vol. 22, No. 4, pp. 483-488; Oct., 1921. Anharmonic polynomial generalizations of the numbers of Bernoulli and Euler. Read (San Francisco) April 9, 1921. Transactions of this Society, vol. 24, No. 2, pp. 89-112; Sept., 1922. Periodicities in the theory of partitions. Read (San Francisco) April 8, 1922. Annals of Mathematics, (2), vol. 24, No. 1, pp. 1-22; Sept., 1922. Relations between the numbers of Bernoulli, Euler, Genocchi, and Lucas. Read (San Francisco) April 8, 1922. Messenger of Mathe matics, vol. 52, No. 4, pp. 56-64, and No. 5, pp. 65-68; Aug. -

Germany 1919-1941 U.S

U.S. MILITARY INTELLIGENCE REPORTS : GERMANY 1919-1941 U.S. MILITARY INTELLIGENCE REPORTS: GERMANY, 1919-1941 Edited by Dale Reynolds Guide Compiled by Robert Lester A Microfilm Project of UNIVERSITY PUBLICATIONS OF AMERICA, INC. 44 North Market Street • Frederick, MD 21701 Copyright© 1983 by University Publications of America, Inc. All rights reserved. ISBN 0-89093^26-6. Note on Sources The Documents in this Collection are from the National Archives and Record Service, Washington, D.C., Record Group #165. Mil- itary Intelligence Division Files: Germany. TABLE OF CONTENTS Red Index 1 Reel I 1 Reel II 6 Reel III 10 Reel IV 15 Reel V 18 Reel VI 22 Reel VII 25 Reel VIII 29 Reel IX 31 Reel X 33 Reel XI 33 Reel XII 34 Reel XIII 35 Reel XIV 38 Reel XV 39 Reel XVI 41 Reel XVII 43 Reel XVIII 45 Reel XIX 47 Reel XX 49 Reel XXI 52 Reel XXII 54 Reel XXIII 56 Reel XXIV 58 Reel XXV 61 Reel XXVI 63 Reel XXVII 65 Reel XXVIII 68 Subject Index 71 Dates to Remember February 3,1917 Severance of U.S. Diplomatic Relations with Germany; Declara- tion of War November 11,1918 Armistice December 1, 1918 U.S. Troops of the 3rd Army cross the Rhine and Occupy the Rhine Province July 2,1919 Departure of the U.S. 3rd Army; the U.S. Army of the Rhine Occupies Coblenz in the Rhine Province December 10, 1921 Presentation of Credentials of the U.S. Charge d'Affaires in Berlin April 22, 1922 Withdrawal of U.S. -

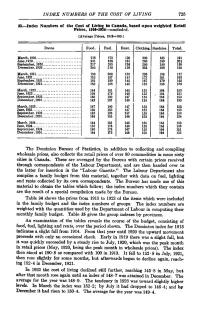

INDEX NUMBERS of the COST of LIVING 725 33.—Index Numbers of the Cost of Living in Canada, Based Upon Weighted Retail Prices

INDEX NUMBERS OF THE COST OF LIVING 725 33.—Index Numbers of the Cost of Living in Canada, based upon weighted Retail Prices, 1910-1934—concluded. (Average Prices, 1913=100.) Dates. Food. Fuel. Rent. Clothing. Sundries. Total. March, 1920 218 173 120 260 185 191 June,1920 231 186 133 260 190 201 September, 1920 217 285 136 260 190 199 December, 1920. 202 218 139 235 190 192 March, 1921 180 208 139 195 188 177 June,1921 152 197 143 173 181 163 September, 1921 161 189 145 167 170 162 December, 1921. 150 186 145 158 166 156 March, 1922 144 181 145 155 164 153 June, 1922 139 179 146 155 . 164 151 September, 1922. 140 190 147 155 164 153 December, 1922. 142 187 146 155 164 153 March, 1923 147 190 147 155 164 155 June,1923 139 182 147 155 164 152 September, 1923. 142 183 147 155 164 153 December, 1923. 146 185 146 155 164 154 March, 1924 144 181 146 155 164 153 June,1924 133 176 146 155 164 149 September, 1924. 140 176 147 155 164 151 December, 1924. 144 175 146 155 164 152 The Dominion Bureau of Statistics, in addition to collecting and compiling wholesale prices, also collects the retail prices of over 80 commodities in some sixty cities in Canada. These are averaged by the Bureau with certain prices received through correspondents of the Labour Department, and are then handed over to the latter for insertion in the "Labour Gazette." The Labour Department also compiles a family budget from this material, together with data on fuel, lighting and rents collected by its own correspondents. -

The Paris Peace Conference (1919-1920) and Its Aftermath

The Paris Peace Conference (1919-1920) and Its Aftermath The Paris Peace Conference (1919-1920) and Its Aftermath: Settlements, Problems and Perceptions Edited by Sorin Arhire and Tudor Roşu The Paris Peace Conference (1919-1920) and Its Aftermath: Settlements, Problems and Perceptions Edited by Sorin Arhire and Tudor Roşu This book first published 2020 Cambridge Scholars Publishing Lady Stephenson Library, Newcastle upon Tyne, NE6 2PA, UK British Library Cataloguing in Publication Data A catalogue record for this book is available from the British Library Copyright © 2020 by Sorin Arhire, Tudor Roşu and contributors All rights for this book reserved. No part of this book may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the copyright owner. ISBN (10): 1-5275-4224-6 ISBN (13): 978-1-5275-4224-2 Cover Image: Sturdza Palace (photo taken around 1930) which was the headquarters of the Romanian Ministry of Foreign Affairs, 1919-1920. Source: Diplomatic Archives of Romanian Ministry of Foreign Affairs, Bucharest. TABLE OF CONTENTS Introduction ................................................................................................ 1 Sorin ARHIRE and Tudor ROȘU Chapter One ............................................................................................... 3 The Romanian Americans and the Paris Peace Conference: The Trianon Treaty (4 June 1920) Constantin I. STAN and Mădălina OPREA Chapter -

À Magazine of Verse Edited by Harriet Monroe March 1921

Vol. XVII No. VI À Magazine of Verse Edited by Harriet Monroe March 1921 543 Cass Street, Chicago $3.00 per Year Single Numbers 25c DEAR POETRY: I always feel that I ought to renew my thanks for your enterprise and faith, which are so ceaselessly at work on the task of renewing me. Ferdinand Schevill Vol. XVII No. VI POETRY for MARCH, 1921 PAGE A House Ford Madox Hueffer 291 Eidolon : ....... Leslie" Nelson Jennings 311 Two Poems Fannie Stearns Gfford 312 Death in the Sun—Apology Shadow Songs Jeannette Marks 314 Rose Toada—Ebony—The Broken Door Purple Margaret Steele Anderson 315 The Debt—A Prayer Jessie MacDonald 316 Three Poems Edwin Ford Piper 318 March Wind—Whispering Often—Home Their Wide Range H. M. 322 Thames Morasses Ezra Pound 325 Reviews: Koral Grisaille Helen Birch-Bartlett 329 Crucible Emanuel Carnevali 332 Evelyn Scott Lola Ridge 334 Gregorian Elizabethan Isidor Schneider 337 Prophet or Poet? .... Nelson Antrim Crawford 341 A New-Englander H. L. Davis 343 Robert Bridges Once More H. L. Davis 344 A Critic of Poetry Richard Aldington 345 Correspondence: Australian and U. S. Copyrights . H. W'. Stewart 348 Notes and Books Received 349, 350 Manuscripts must be accompanied by a stamped and self-addressed envelope. Inclusive yearly subscription rates: In the United States, Mexico, Cuba and American possessions, $3.00 net; in Canada, $3.15 net; in all other countries in the Postal Union, $3.25 net. Entered as second-class matter Nov. 15, 1912, at the post-office, at Chicago, Ill., under the Act of March 3, 1879. -

TROTSKY PROTESTS TOO MUCH by Emma Goldman

Published Essays and Pamphlets TROTSKY PROTESTS TOO MUCH By Emma Goldman PRICE TWOPENCE In America Five Cents Published by THE ANARCHIST COMMUNIST FEDERATION [Glasgow, Scotland, 1938] INTRODUCTION. This pamphlet grew out of an article for Vanguard, the Anarchist monthly published in New York City. It appeared in the July issue, 1938, but as the space of the magazine is limited, only part of the manuscript could be used. It is here given in a revised and enlarged form. Leon Trotsky will have it that criticism of his part in the Kronstadt tragedy is only to aid and abet his mortal enemy, Stalin. It does not occur to him that one might detest the savage in the Kremlin and his cruel regime and yet not exonerate Leon Trotsky from the crime against the sailors of Kronstadt. In point of truth I see no marked difference between the two protagonists of the benevolent system of the dictatorship except that Leon Trotsky is no longer in power to enforce its blessings, and Josef Stalin is. No, I hold no brief for the present ruler of Russia. I must, however, point out that Stalin did not come down as a gift from heaven to the hapless Russian people. He is merely continuing the Bolshevik traditions, even if in a more relentless manner. The process of alienating the Russian masses from the Revolution had begun almost immediately after Lenin and his party had ascended to power. Crass discrimination in rations and housing, suppression of every political right, continued persecution and arrests, early became the order of the day. -

Houlton Times, March 9, 1921

If Low Insurance Means Anything to You, Help the Inspector- --Houlton’s Rate Depends on His Report j TT AROOSTOOK TIMES SHIRE TOWN OF Cary Library April 13, 1860 AROOSTOOK COUNT! To OULTON TIMES December 27, 1916 HOULTON, MAINE, WEDNESDAY, MARCH 9, 1921 VOL. LXI No. 10 E U S BOWLERS APRIL TERM S. J. COURT PAST MASTER’S NIGHT QUARTERLY MEETING BOWLERS GUESTS We are informed by Michael M. The annual Past Masters night of CHAUTAUQUA OF THE UNITED SWAMP CAPT. FARMER’S Clark, Clerk of Courts, that the April Monument Lodge No. 96 F. & A. M. PIN PICKERS term of the Supreme Judicial Court, was held on Wednesday with a large BAPTIST ASSOCIATION The Elks bowling team played a OF PRESQUE ISLE at Houlton, is scheduled to open on PROGRAM Beginning Wednesday afternoon return match against Capt. Parmer s April 19th, Patriots Day, and that by a en( ance- andf continuing through Thursday, the picked team Thursday evening, Mar virtue of R. S. Chap. 82, Sec. 52 no Two candidates received the M. M. United Baptist churches of South 3d, on the S. A. alleys, the result be- Royally Entertained by court can be held on that day, there- degree worked by the following A Fine List of Entertainers Aroostook will meet with the First In* that when they lett, Capt. Farmer fore the following day “ Shall be officers, most of whom were Past Baptist church for their Quarterly and his crew were trying to dig them Mooseleuk Club of deemed the first day of the term for Masters for this Summer’s Meeting. -

The Forty Thieves: Churchill, the Cairo Conference, and the Policy Debate Over Strategies of Colonial Control in British Mandatory Iraq, 1918—1924

The Forty Thieves: Churchill, the Cairo Conference, And the Policy Debate Over Strategies Of Colonial Control in British Mandatory Iraq, 1918—1924 James D. Terry A thesis submitted to the Faculty of the University of North Carolina at Chapel Hill in partial fulfillment of the requirements for the degree of Master of Arts in the Department of History. Chapel Hill 2008 Approved by: Dr. Richard H. Kohn Dr. Joseph T. Glatthaar Dr. Richard A. Soloway ©2008 James D. Terry ALL RIGHTS RESERVED ii Abstract JAMES TERRY: The Forty Thieves: Churchill, the Cairo Conference, and The Policy Debate Over Strategies of Colonial Control in British Mandatory Iraq, 1918-1924 (Under the direction of Dr. Richard Kohn) After World War I, Great Britain found itself unexpectedly occupying vast swaths of the Middle East, including the modern-day nation of Iraq. The final disposition of its Middle Eastern possessions was initially unclear, and the British government explored several policy options before finally selecting air policing, a novel colonial control scheme wherein aircraft would be used in lieu of ground forces to provide a British military presence in Iraq. This thesis examines the process by which Britain chose air policing as its best strategy for Iraq. Air policing was intensely controversial from the very beginning. The internal debate it sparked within the government was intense and bitter. That air policing ultimately won out over rival policy options was due to a combination of factors, including Churchill’s advocacy, financial cuts, manpower reductions, and policymakers’ determining that air policing represented the best possibility for Great Britain to maintain influence in Iraq. -

The Foreign Service Journal, June

AMERICAN uJNbuLAiti JUL 12 . 1921 KOBE.JAPAN I CONSUL1 LLETIN piTDi ISHED MONTHLY WITH THE COOPERATION OF THE AMERICAN CONSULAR ASSOCIATION TO FURTHER AMERICAN INTERESTS IN FOREIGN LANDS THROUGH THF. CONSULAR SFRVICE No. 4 VOL. 3 JUNE 1921 AMERICAN COTTON AT LIVERPOOL Phntnarabh furnished by Consul Horace Lee Washington, showing American cotton on dock at Liverpool awaiting removal to storage warehouse. More than eleven million centals (100 lbs each)l oj' A™encan cott0n were imported at Liverpool during 1919, and the value thereof exceeded $530,000,00u. EDITOR & PUBLISHER, J. W. YOUNG, TIFFIN BUILDING, Long Island City, N. Y. Rogers Introduces New Bill Original Proposals of Massachusetts Representative for Reorganization of Foreign Service Extended to Include Pension System—Hearings This Summer Possibly. Immediately upon the meeting of Congress in special Counselors of Embassy would be recommissioned Foreign session, April 11th, Representative John Jacob Rogers of Service officers of Class I, and those acting as Counselors Massachusetts introduced a bill (H. R. 17) “for the of Legation would be recommissioned Foreign Service reorganization and improvement of the Foreign Service officers of Class II. Secretaries of Class I, not Counselors of the United States, and for other purposes.” The chief of Embassy or Legation, would be recommissioned For¬ features of the bill, which is a considerably enlarged eign Service officers of Class III, and so on. revision of the bill for the improvement of the Service On the consular side, Consuls General of Classes I and (H. R. 11058) which Mr. Rogers had before the last II would be recommissioned Foreign Service officers of session of Congress, are these: Class I. -

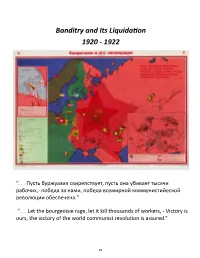

Map 10 Banditry and Its Liquidation // 1920 - 1922 Colored Lithographic Print, 64 X 102 Cm

Banditry and Its Liquidation 1920 - 1922 “. Пусть буржуазия свирепствует, пусть она убивает тысячи рабочих,- победа за нами, победа всемирной коммунистийеской революции обеспечена.” “. Let the bourgeoisie rage, let it kill thousands of workers, - Victory is ours, the victory of the world communist revolution is assured.” 62 Map 10 Banditry and Its Liquidation // 1920 - 1922 Colored Lithographic print, 64 x 102 cm. Compilers: A. N. de-Lazari and N. N. Lesevitskii Artist: S. R. Zelikhman Historical Background and Thematic Design The Russian Civil War did not necessarily end with the defeat of the Whites. Its final stage involved various independent bands of partisans and rebels that took advantage of the chaos enveloping the country and contin- ued to operate in rural areas of Ukraine, Tambov Province, the lower Volga, and western Siberia, where Bol- shevik authority was more or less tenuous. Their leaders were by and large experienced military men who stoked peasant hatred for centralized authority, whether it was German occupation forces, Poles, Moscow Bol- sheviks, or Jews. They squared off against the growing power of the communists, which is illustrated as series of five red stars extending over all four sectors. The red circle identifies Moscow as the seat of Soviet power, while the five red stars, enlarging in size but diminishing in color intensity as they move further from Moscow, represent the increasing strength of Communism in Russia during the years 1920-22. The stars also serve as symbolic shields, apparently deterring attacking forces that emanate from Poland, Ukraine, and the Volga region. The red flag with the gold emblem of the hammer-and-sickle in the upper hoist quarter, and the letters Р. -

The Russian Revolution (1917-1921), Vol. I by William Henry Chamberlin

The Russian Revolution (1917-1921), Vol. I By William Henry Chamberlin. New York: The Macmillan Co., 1935 Book Review By Daniel Kendie, Ph.D. Chamberlin was the Moscow correspondent of the Christian Science Monitor from 1922- 1932. By taking advantage of his presence there, he produced two remarkable volumes on the Russian Revolution. It took him twelve years of study and research. The first volume is a narrative account of daily events in Russia from 1917 to 1921. It begins with the downfall of the Czar in March 1917, and ends with the introduction of the New Economic Policy (NEP) in March 1921. The volume is fairly well documented. Newspapers, historical magazines, memoirs, and archival materials are utilized. Chamberlin’s personal encounters with some of the leading actors in the historical drama have also given him an added advantage. Journalists are often criticized for resorting to sensationalism in order to help increase the circulation of newspapers. Chamberlin, however, does not write like a journalist–but like a scholar. Although one can see where he stands (i.e. sympathy for the revolutionaries), on the whole, he does not get emotionally involved. He is reasonably detached and fairly objective. In the introductory chapters, Chamberlin provides the historical background against which the Russian Revolution of 1917 took place. This section of the book is essential for those who do not know much about Russia. He describes the heavy hand of the Russian past, which left strong imprints on the psychology and character of the masses, and on the ultimate outcome of the Russian Revolution itself.