KPN Q4 2020 Press Release

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TV Channel Distribution in Europe: Table of Contents

TV Channel Distribution in Europe: Table of Contents This report covers 238 international channels/networks across 152 major operators in 34 EMEA countries. From the total, 67 channels (28%) transmit in high definition (HD). The report shows the reader which international channels are carried by which operator – and which tier or package the channel appears on. The report allows for easy comparison between operators, revealing the gaps and showing the different tiers on different operators that a channel appears on. Published in September 2012, this 168-page electronically-delivered report comes in two parts: A 128-page PDF giving an executive summary, comparison tables and country-by-country detail. A 40-page excel workbook allowing you to manipulate the data between countries and by channel. Countries and operators covered: Country Operator Albania Digitalb DTT; Digitalb Satellite; Tring TV DTT; Tring TV Satellite Austria A1/Telekom Austria; Austriasat; Liwest; Salzburg; UPC; Sky Belgium Belgacom; Numericable; Telenet; VOO; Telesat; TV Vlaanderen Bulgaria Blizoo; Bulsatcom; Satellite BG; Vivacom Croatia Bnet Cable; Bnet Satellite Total TV; Digi TV; Max TV/T-HT Czech Rep CS Link; Digi TV; freeSAT (formerly UPC Direct); O2; Skylink; UPC Cable Denmark Boxer; Canal Digital; Stofa; TDC; Viasat; You See Estonia Elion nutitv; Starman; ZUUMtv; Viasat Finland Canal Digital; DNA Welho; Elisa; Plus TV; Sonera; Viasat Satellite France Bouygues Telecom; CanalSat; Numericable; Orange DSL & fiber; SFR; TNT Sat Germany Deutsche Telekom; HD+; Kabel -

Global Pay TV Fragments

Global pay TV fragments The top 503 pay TV operators will reach 853 million subscribers from the 1.02 billion global total by 2026. The top 50 operators accounted for 64% of the world’s pay TV subscribers by end-2020, with this proportion dropping to 62% by 2026. Pay TV subscribers by operator ranking (million) 1200 1000 143 165 38 45 800 74 80 102 102 600 224 215 400 200 423 412 0 2020 2026 Top 10 11-50 51-100 101-200 201+ Excluded from report The top 50 will lose 20 million subscribers over the next five years. However, operators beyond the top 100 will gain subscribers over the same period. Simon Murray, Principal Analyst at Digital TV Research, said: “Most industries consolidate as they mature. The pay TV sector is doing the opposite – fragmenting. Most of the subscriber growth will take place in developing countries where operators are not controlled by larger corporations.” By end-2020, 13 operators had more than 10 million pay TV subscribers. China and India will continue to dominate the top pay TV operator rankings, partly as their subscriber bases climb but also due to the US operators losing subscribers. Between 2020 and 2026, 307 of the 503 operators (61%) will gain subscribers, with 13 showing no change and 183 losing subscribers (36%). In 2020, 28 pay TV operators earned more than $1 billion in revenues, but this will drop to 24 operators by 2026. The Global Pay TV Operator Forecasts report covers 503 operators with 726 platforms [132 digital cable, 116 analog cable, 279 satellite, 142 IPTV and 57 DTT] across 135 countries. -

ECC REPORT 143 Electronic Communications Committee

ECC REPORT 143 Electronic Communications Committee (ECC) within the European Conference of Postal and Telecommunications Administrations (CEPT) PRACTICAL IMPROVEMENTS IN HANDLING 112 EMERGENCY CALLS: CALLER LOCATION INFORMATION Lisbon, April 2010 ECC REPORT 143 Page 2 0 EXECUTIVE SUMMARY Each year in the European Union several millions of citizens dial the emergency call number to access emergency services. Due to increasing penetration of mobile telephony in the society, the share of emergency calls emanating from mobile networks is rapidly outgrowing emergency calls for fixed networks; this causes that an emergency situation mobile callers are increasingly not able to indicate the precise location for an optimum response. Similarly, VoIP services are substituting voice calls over traditional networks, customers increasingly use VoIP for emergency calls and expecting the same reliability and completeness of the emergency calls service. Location information is normally represented by data indicating the geographic position of the terminal equipment of a user. These data vary in range, indicating in a general way where the user is or very precise, pinpointing the user’s whereabouts to within a few meters. Some location data are effectively a subset of signalling data as they are necessary for setting up a telephone connection. In the framework of Enhanced emergency call services, the availability of location information must serve three main goals: Route the calls to the right emergency call centre; Locate the caller and/or the incident site. Dispatch the most appropriate emergency response team(s); The Report identify the most relevant regulatory principles applicable to caller location requirements in the context of emergency calls and analyses the location information standards produced by ETSI as a Standard Development Organization for fixed, mobile and IP communications networks. -

Global Pay TV Operator Forecasts

Global Pay TV Operator Forecasts Table of Contents Published in October 2016, this 190-page electronically-delivered report comes in two parts: A 190-page PDF giving a global executive summary and forecasts. An excel workbook giving comparison tables and country-by-country forecasts in detail for 400 operators with 585 platforms [125 digital cable, 112 analog cable, 208 satellite, 109 IPTV and 31 DTT] across 100 territories for every year from 2010 to 2021. Forecasts (2010-2021) contain the following detail for each country: By country: TV households Digital cable subs Analog cable subs Pay IPTV subscribers Pay digital satellite TV subs Pay DTT homes Total pay TV subscribers Pay TV revenues By operator (and by platform by operator): Pay TV subscribers Share of pay TV subscribers by operator Subscription & VOD revenues Share of pay TV revenues by operator ARPU Countries and operators covered: Country No of ops Operators Algeria 4 beIN, OSN, ART, Algerie Telecom Angola 5 ZAP TV, DStv, Canal Plus, Angola Telecom, TV Cabo Argentina 3 Cablevision; Supercanal; DirecTV Australia 1 Foxtel Austria 3 Telekom Austria; UPC; Sky Bahrain 4 beIN, OSN, ART, Batelco Belarus 2 MTIS, Zala Belgium 5 Belgacom; Numericable; Telenet; VOO; Telesat/TV Vlaanderen Bolivia 3 DirecTV, Tigo, Entel Bosnia 3 Telemach, M:Tel; Total TV Brazil 5 Claro; GVT; Vivo; Sky; Oi Bulgaria 5 Blizoo, Bulsatcom, Vivacom, M:Tel, Mobitel Canada 9 Rogers Cable; Videotron; Cogeco; Shaw Communications; Shaw Direct; Bell TV; Telus TV; MTS; Max TV Chile 6 VTR; Telefonica; Claro; DirecTV; -

Monthly Industry Overview

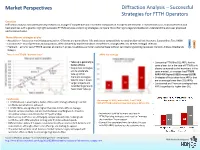

Market Perspectives Diffraction Analysis – Successful Strategies for FTTH Operators Overview Diffraction Analysis conducted primary research on a range of competitive and incumbent companies in Europe to benchmark FTTH/B services so as to analyse trends and best practices with a goal to: highlight successful FTTH/B services and pricing strategies; compare fibre offerings to legacy broadband; understand the end-user proposed and perceived value. Three different strategies at play ARPU • Acquisition – focuses on maximising penetration. Offerings are generally no frills and priced competitively to existing alternatives: Networx; Superonline; Teo; HKBN TAKE • Constrained – mix of premium and acquisition, often dictated by market condition: Rostelecom; Orange; KPN; Izzi; M-Net; Portugal Telecom - UP • Premium – aims for sexy FTTH/B services at premium prices, to address a smaller customer base without cannibalising existing revenues: Verizon; Altibox; Bredbands Bolaget There is no FTTH/B “demand issue” ARPU by strategy • Take-up is generally a • Comparing FTTH/B to DSL ARPU for the factor of time same player (or in the case of FTTH/B only • Acquisition strategies players compared to the incumbent in the aim to accelerate same market), on average has FTTH/B take-up while ARPU 46% higher (US$55 versus US$38) Premium strategies • Strategies of Acquisition have ARPUs that tend to slow it down are on average lower than DSL ARPUs • Larger projects and • Constrained and Premium strategies have incumbents generally ARPUs significantly higher than DSL -

Playout Delay of TV Broadcasting

Master Thesis Playout delay of TV broadcasting Wouter Kooij 06/03/2014 University of Twente Faculty of Electrical Engineering, Mathematics and Computer Science Nederlandse Organisatie voor toegepast-natuurwetenschappelijk onderzoek, TNO Supervisors UT Prof. Dr. Ir. Boudewijn R. Haverkort Dr.ir. Pieter-Tjerk de Boer Supervisors TNO Ir. Hans Stokking Ray van Brandenburg, M.Sc. Date of the graduation 13/03/2014 Contents Acknowledgments 3 Nomenclature 5 1. Background 7 1.1. Introduction . .7 1.2. Research questions . .7 1.3. Outline . .8 2. Related Work 11 3. TV content delivery networks 13 3.1. Introduction . 13 3.2. Overview . 13 3.2.1. Analog TV . 14 3.2.2. Terrestrial, Satellite and Cable TV (DVB) . 15 3.2.3. IPTV . 15 3.3. TV Content delivery chain elements . 18 4. Delays in TV content delivery networks 21 4.1. Introduction . 21 4.2. Encoding and decoding . 22 4.2.1. Coding types . 23 4.2.2. Conclusion . 25 4.3. Transmission delays . 25 4.4. IPTV Techniques . 26 4.5. Delays in the KPN Chain . 26 5. Design and development of a playout difference measurement system 29 5.1. Introduction . 29 5.2. Content recognition techniques . 29 5.2.1. Audio fingerprinting . 31 5.3. Overview . 35 5.4. Reference time-source . 38 5.4.1. GPS as time-source . 38 5.4.2. GPS architecture in Android . 39 5.4.3. Obtaining GPS time in Android . 41 i Contents Contents 5.4.4. NTP as time-source . 44 5.4.5. NTP implementation in Android . 45 5.4.6. -

Fritz-Handleiding-Ziggokpn-7490.Pdf

Handleiding: Hoe sluit je de FRITZ!Box aan achter een Ziggo of KPN modem Pagina | 1 Inhoudsopgave Pagina 1 - Voorblad Pagina 2 - Inhoudsopgave Pagina 3 - Voorwoord / Tips Pagina 4 - Instellen van de taal Pagina 5 - Instellen van het land Pagina 6 - Kiezen van de Annex verbinding Pagina 7 - Kiezen van het password Pagina 8 - 9 - Kiezen van de Internet Service Provider Pagina 9 - 10 - Set Up Internet Connection / Instellen snelheid DSL line Pagina 11 - 12 - Opslaan instellingen en testen internet connectie Pagina 13 - Einde van het instellen van de internetverbinding Pagina 14 - Instellen telefonie Ziggo via de FRITZ!Box Pagina 15 - Verbindingstype telefonie kiezen Pagina 16 - Ingeven telefoonnummer / Eind instellen telefonie Pagina 17 - Slotwoord / Tel.nr Helpdesk AVM / FAQ Pagina | 2 Het instellen van de FRITZ!Box als u een Ziggo of KPN modem/router heeft Allereerst bedankt voor de aanschaf van de FRITZ!Box. Wij wensen u er veel plezier mee! Via deze handleiding lopen we stap voor stap met u door wat u moet doen om de FRITZ!Box in de juiste instellingen te krijgen. Dit neemt enkele minuten in beslag. De handleiding is alleen om uw internet en telefonie in te stellen. Aan het TV signaal verandert niets en zal gewoon via uw Ziggo of KPN modem blijven gaan. Het is aan te raden om uw Ziggo of KPN modem in Bridge mode te zetten. Dit houdt in dat de Ziggo of KPN modem geen enkel signaal meer uitzendt wat storing kan geven. Hij geeft alleen nog via de LAN 1 poort internet door naar de FRITZ!Box. -

Status for the Implementation of DVB-T in the CEPT Area October 2005

WG RRC-06(05) Status for the implementation of DVB-T in the CEPT area October 2005 Introduction The ITU Regional Radiocommunications Conference RRC-06 shall establish a new agreement and associated frequency plans, including a new plan for terrestrial digital television (DVB-T) in the frequency bands 174 - 230 MHz (Band III) and 470 - 862 MHz (Bands IV/V). In preparation for the RRC-06 the CEPT has decided to follow the implementation of DVB-T. A significant number of CEPT countries have made a commitment to DVB-T with pilot or test transmissions taking place and planning studies under way for nation-wide coverage. Furthermore, a number of countries already have operational transmissions. In order to inform the WG RRC-06 on the implementation of DVB-T the ERO is maintaining this overview document. It consists of a table with figures on frequencies, transmitters, receivers and population coverage. Additional information is provided in the text following the table in the form of notes for each country. Please note that the map indicates the current status of implementation of DVB-T in CEPT countries and not the actual coverage. An updated overview is to be presented at each WG RRC-06 meeting. Last update: 06 October 2005. Next WG RRC-06 meeting: 31 January – 02 February 2006 1 National service launch date announced or already on air (11) Frequecy planning or test transmissions going on (20) Considering (1) No information (15) DVB-T implementation in the CEPT area 06-10-2005 Figure 1: DVB-T status in Europe 2 DVB-T implementation progress overview Country Co- Number of transmitters Percentage of households that can already, or are Number of Date of ordination (not number of stations) expected in the near future to, receive the quoted DVB-T last update in progress In operation Total after one year number of multiplexes receivers from now in use e.r.p. -

12/FINAL Working Party on Telecommunication And

Unclassified DSTI/ICCP/TISP(2005)12/FINAL Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development 07-Apr-2006 ___________________________________________________________________________________________ English - Or. English DIRECTORATE FOR SCIENCE, TECHNOLOGY AND INDUSTRY COMMITTEE FOR INFORMATION, COMPUTER AND COMMUNICATIONS POLICY Unclassified DSTI/ICCP/TISP(2005)12/FINAL Working Party on Telecommunication and Information Services Policies MULTIPLE PLAY: PRICING AND POLICY TRENDS English - Or. English JT03207142 Document complet disponible sur OLIS dans son format d'origine Complete document available on OLIS in its original format DSTI/ICCP/TISP(2005)12/FINAL FOREWORD This report was presented to the Working Party on Telecommunication and Information Services Policies in December 2005 and was declassified by the Committee for Information, Computer and Communications Policy in March 2006. The report was prepared by Mr. Yoshikazu Okamoto and Mr. Taylor Reynolds of the OECD’s Directorate for Science, Technology and Industry. It is published under the responsibility of the Secretary- General of the OECD. © OECD/OCDE 2006 2 DSTI/ICCP/TISP(2005)12/FINAL TABLE OF CONTENTS MAIN POINTS.............................................................................................................................................. 6 Regulatory issues........................................................................................................................................ 7 INTRODUCTION -

Playout Delay of TV Broadcasting

Master Thesis Playout delay of TV broadcasting Wouter Kooij 11/03/2014 University of Twente Faculty of Electrical Engineering, Mathematics and Computer Science Nederlandse Organisatie voor toegepast-natuurwetenschappelijk onderzoek, TNO Supervisors UT Prof. Dr. Ir. Boudewijn R. Haverkort Dr.ir. Pieter-Tjerk de Boer Supervisors TNO Ir. Hans Stokking Ray van Brandenburg, M.Sc. Date of the graduation 13/03/2014 Contents Acknowledgments 3 Nomenclature 5 1. Background 7 1.1. Introduction . .7 1.2. Research questions . .7 1.3. Outline . .8 2. Related Work 11 3. TV content delivery networks 13 3.1. Introduction . 13 3.2. Overview . 13 3.2.1. Analog TV . 14 3.2.2. Terrestrial, Satellite and Cable TV (DVB) . 15 3.2.3. IPTV . 15 3.3. TV Content delivery chain elements . 18 4. Delays in TV content delivery networks 21 4.1. Introduction . 21 4.2. Encoding and decoding . 22 4.2.1. Coding types . 23 4.2.2. Conclusion . 25 4.3. Transmission delays . 25 4.4. IPTV Techniques . 26 4.5. Delays in the KPN Chain . 26 5. Design and development of a playout difference measurement system 29 5.1. Introduction . 29 5.2. Content recognition techniques . 29 5.2.1. Audio fingerprinting . 31 5.3. Overview . 35 5.4. Reference time-source . 38 5.4.1. GPS as time-source . 38 5.4.2. GPS architecture in Android . 39 5.4.3. Obtaining GPS time in Android . 41 i Contents Contents 5.4.4. NTP as time-source . 44 5.4.5. NTP implementation in Android . 45 5.4.6. -

European Pay TV Operator Forecasts: Table of Contents

European Pay TV Operator Forecasts: Table of Contents Published in September 2012, this 140-page electronically-delivered report comes in two parts: A 110-page PDF giving a global executive summary, country/operator analysis and forecasts. An 30-page excel workbook giving comparison tables and country-by- country forecasts in detail for 95 operators across 25 territories from 2007 to 2017. Countries and operators covered: Country No of ops Operators Austria 3 Telekom Austria; UPC; Sky Belgium 4 Belgacom; Numericable; Telenet; VOO Croatia 2 Digi TV; Max TV/T-HT Czech 4 Digi TV; Telefonica; Skylink; UPC Denmark 6 Canal Digital; Viasat; You See; Stofa; Boxer; TDC Finland 6 Digita; Elisa; Teliasonera; DNA; Canal Digital; Viasat France 6 Orange; SFR; CanalSat; Numericable; Free; TNT Germany 5 KBW; KDG; DT; Sky; Unitymedia Greece 1 Nova Hungary 3 T-Home; Digi TV; UPC (cable & DTH) Ireland 2 UPC; Sky Italy 3 Mediaset; Sky; Telecom Italia Netherlands 5 UPC; Canal Digitaal; Tele 2; Ziggo; KPN/Digitenne Norway 5 Canal Digital; Viasat; Riks TV; Telenor; Get Poland 8 N; TNK; TP/Orange; Vectra; Multimedia Polska; Cyfra Polsat; Cyfra+; UPC Portugal 3 PT; Zon; Cabovisao Romania 3 Romtelecom; RCS-RDS/Digi TV; UPC Russia 7 NTV Plus; Tricolor; Akado; MTS; ER Telecom; Rostelecom; Beeline Serbia 1 SBB Slovakia 4 UPC; RCS-RDS; Skylink; Slovak Telekom Spain 3 Ono; Canal Plus; Telefonica Sweden 5 Canal Digital; Viasat; Com Hem; Telia; Boxer Switzerland 2 Swisscom; UPC/Cablecom Ukraine 1 Volia UK 3 Sky; Virgin; BT Forecasts (2007-2017) contain the following detail for each country: By country: TV households Digital cable subs Analog cable subs Pay IPTV subscribers Pay digital DTH subs Pay DTT homes By operator (and by platform by operator): Subscribers Subscription & VOD revenues ARPU Liberty Global and BSkyB to continue European pay TV dominance Pay TV subscriptions for the 95 operators across 25 countries covered in a new report from Digital TV Research will increase from a collective 96.2 million in 2007 to 140.9 million by 2017. -

Hbbtv in Europe V5b English

HbbTV Forum Nederland Overview of Interactive Television services according to the HbbTV standard in Europe March 27th 2014 contacts: Frank Visser +31 6 514 89 675 Rob Koenen +31 6 117 83 117 European overview: Robert Briel - Broadband TV News http://www.hbbtv.nu Contents 1 HbbTV: an open standard for interactive TV services ..............................................................................................3 2 HbbTV in Europe ......................................................................................................................................................3 3 HbbTV application categories...................................................................................................................................4 3.1 Subdivision in four categories.............................................................................................................4 3.2 Practical examples..............................................................................................................................4 4 HbbTV local, regional, national, and international operators....................................................................................5 4.1 Of local and regional importance........................................................................................................5 4.2 Thematic services...............................................................................................................................5 4.3 International........................................................................................................................................5